From getting rich by hoarding cryptocurrencies to selling them to repair watches, the capital market is no longer unconditionally rewarding stories of holding cryptocurrencies.

Written by: ChandlerZ, Foresight News

On November 3, US-listed semiconductor company Sequans Communications (NYSE:SQNS) redeemed 50% of its convertible bonds by selling 970 bitcoins. This transaction reduced the company's total debt from $189 million to $94.5 million. Sequans now holds 2,264 bitcoins, down from 3,234 previously. Based on current market prices, the company's net asset value in bitcoins is approximately $240 million, and the debt-to-net-worth ratio decreased from 55% to 39%.

This debt reduction is expected to strengthen the company's previously announced ADS buyback program. Sequans focuses on wireless 4G/5G cellular technology in the Internet of Things (IoT) sector and announced earlier this year that it would adopt Bitcoin as a primary asset allocation.

Coincidentally, Ethereum treasury company ETHZilla (stock code ETHZ) announced at the end of October that it had sold approximately $40 million worth of ETH to advance its share buyback program. Previously, in August, the ETHZilla board authorized a share buyback program of up to $250 million. According to the company's announcement, "ETHZilla plans to use the remaining proceeds from the sale of Ethereum for additional share buybacks and intends to continue selling Ethereum to repurchase shares until its share price's discount to net asset value (NAV) returns to a normal level."

ETHZilla is not the only Ethereum treasury to approve a share buyback program. SharpLink Gaming (SBET), the second-largest Ethereum treasury, has also approved a share buyback program of up to $1.5 billion to repurchase shares when its stock price is equal to or below the net asset value of its cryptocurrency holdings.

Other cryptocurrencies are similar. Forward Industries, a treasury company, announced it has filed a supplemental resale prospectus with the U.S. Securities and Exchange Commission and authorized a new $1 billion stock buyback program. The company's board of directors authorized the buyback program on November 3, allowing the company to repurchase up to $1 billion of its outstanding shares, with the authorization period ending on September 30, 2027. Buybacks can be conducted through open market purchases, block trades, and privately negotiated transactions. The supplemental resale prospectus registers a portion of the common stock previously issued in a private placement in September 2025, allowing designated shareholders to resell these securities, but the company will not receive proceeds from any potential resale.

When treasury companies stop hoarding cryptocurrencies and instead sell crypto assets to repair their balance sheets and maintain their stock prices, is the DAT model coming to an end?

Stock prices are sluggish, with most falling by more than half from their peak.

As the crypto market continues its decline following the October black swan event, skepticism surrounding the DAT (Digital Aid and Tax) model is intensifying. Just a few months ago, these companies were seen as leverage points for wealth creation during the crypto bull market. However, the current market reversal is forcing a brutal correction of this highly volatile, highly leveraged model.

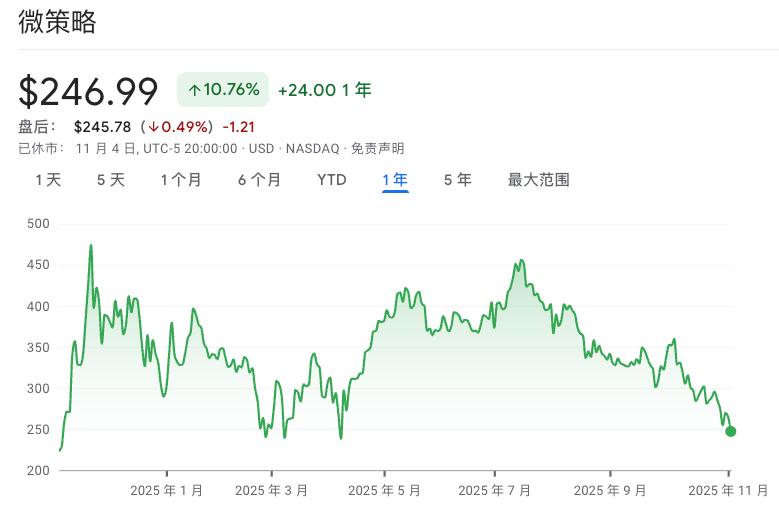

Market data shows that leading altcoin Strategy (MSTR) has fallen nearly 55% from its peak in this bull market, with a year-to-date decline of over 15%. Other Altcoin, such as Treasure, have suffered even more severe losses, generally plummeting from their highs or even losing 90% of their value. Yesterday alone, MSTR fell another 6.88%, bringing its cumulative decline from its peak to 54.69%.

Strategy's stock price change over the past year

Ethereum-based Bitmine (BMNR) fell 7.93% yesterday, down 75.61% from its high; SharpLink Gaming (SBET) fell 10.77% yesterday, down 90.76% from its high; BTCS Inc (BTCS) fell 9.12% yesterday, down 63.61% from its high; SOL-based Upexi (UPXI) fell 8.85% yesterday, down 84.71% from its high; DeFi Development (DFDV) fell 9.41% yesterday, down 83.49% from its high; LTC-based Lite Strategy (LITS) fell 8.33% yesterday, down 80.42% from its high; and TRX-based Tron Inc (TRON) fell 9.13% yesterday, down 82.87% from its high.

S&P issues its first rating for Strategy, giving it a "junk" grade of B-.

S&P Global Ratings recently issued its first credit rating for Strategy, assigning it a "junk" grade of B-. This marks the first time a major international rating agency has given a formal rating to a publicly traded company whose core asset is Bitcoin. S&P noted that while Strategy holds approximately 640,000 Bitcoins, worth about $74 billion at current market prices, the company's debt and dividends are denominated in US dollars, posing a significant currency mismatch risk. A sharp drop in Bitcoin prices could lead to liquidity problems and even debt restructuring for the company.

As of October 2025, the total debt amounted to nearly $15 billion, of which $5 billion in convertible bonds would mature starting in 2028, and the company would also need to pay more than $640 million in preferred stock dividends annually. S&P noted in its report that this highly concentrated structure on a single asset makes the company's capital structure vulnerable. In the event of sharp currency fluctuations, it could be forced to sell assets or restructure its debt, a restructuring considered close to default in credit rating systems. S&P also acknowledged the company's financing capabilities in the capital markets and its management of convertible bond risks, stating that if the company can reduce its reliance on convertible bond financing and improve its dollar liquidity in the future, its rating may be upgraded.

The market's focus is shifting. In the past, the capital market's pricing logic for DAT companies was extremely simplistic: holding a large amount of Bitcoin or Ethereum automatically resulted in a valuation premium on the balance sheet. However, as cryptocurrency prices weakened and liquidity tightened, this narrative began to fail. Investors returned to the most fundamental questions: Where is the company's cash flow? Can it maintain operations without relying on rising cryptocurrency prices? In other words, holding cryptocurrency no longer equates to value. The volatility of treasury assets is now viewed as a risk factor, not a growth engine. The market is beginning to reward companies that can manage risk, optimize structure, and control leverage, rather than those who blindly add to their holdings based on belief.

Meanwhile, the divergence among DAT companies is becoming increasingly apparent. Bitcoin and Ethereum treasury companies can still attract some institutional attention due to their asset liquidity and brand stability, but the story of Altcoin treasuries is fading. Altcoin like Forward, Upexi, and HYPD, which once relied on hype and high leverage to grab market attention, have now become the sector experiencing the most severe pullbacks. The October crash was essentially a liquidation. Blue-chip DAT companies deleveraged and repaired their balance sheets by selling coins, while Altcoin treasuries were passively eliminated in the collapse of leverage. The cyclical nature of the crypto market once again confirms a simple rule: during an uptrend, leverage acts as an amplifier; during a downtrend, it becomes a winch.

When the market stops paying for stories, companies must regain trust through structure, strategy, and transparency. Future DAT will no longer be synonymous with crypto faith, but rather a more mature form of asset management, potentially more cautious and complex.