CZ publicly endorsed a token with real money for the first time, and the balance in the Perp DEX sector is beginning to tilt.

“Eight years ago, I bought some BNB in my first month at TGE and have held them ever since (excluding the portion used for consumption).”

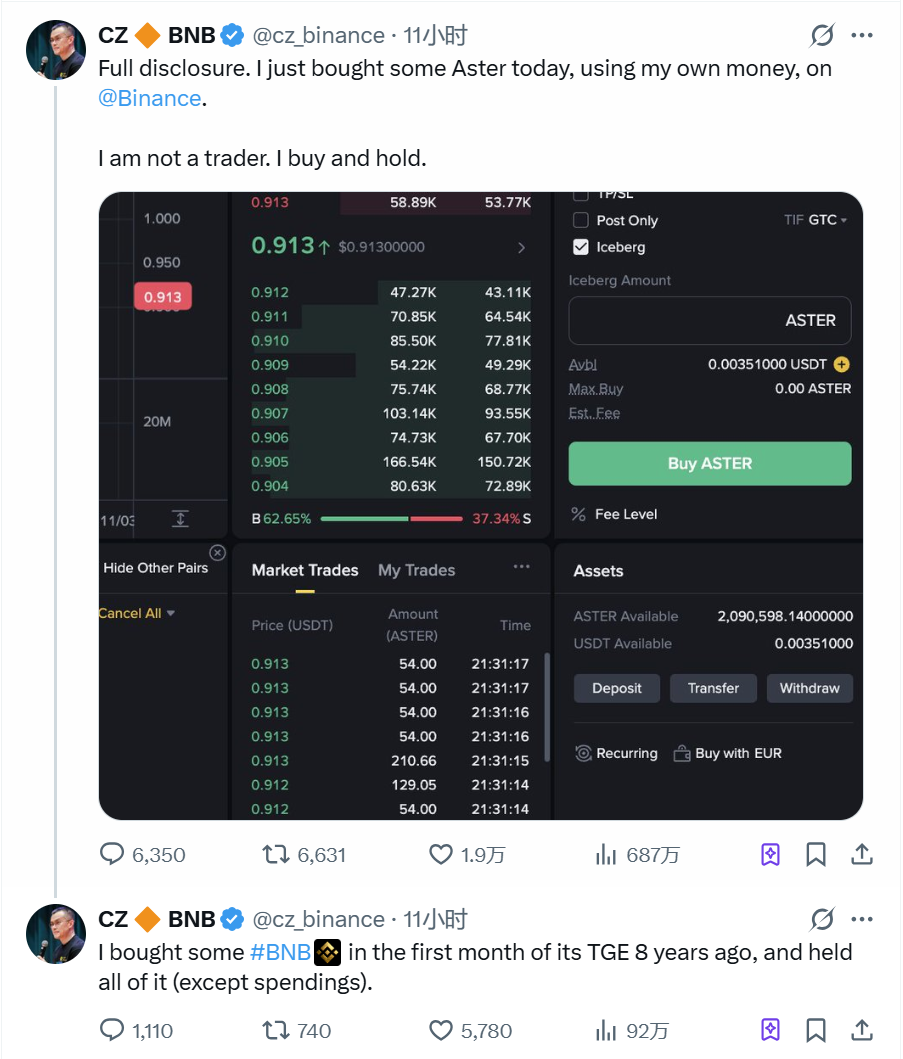

On the evening of November 2nd, Binance founder CZ(CZ) posted this cryptic message on social media after disclosing that he had purchased 2.09 million Aster (ASTER) tokens. This was no ordinary statement. According to CZ's public Binance account records, the average price of this transaction was locked at $0.913, with a total value exceeding $1.9 million.

Following the announcement, ASTER's stock price surged from $0.90 to around $1.25, a nearly 30% increase within an hour, pushing its market capitalization back above $2 billion.

Unlike his previous actions of simply forwarding project updates or liking innovative features, this is CZ's first public disclosure of his personal investment activities since leaving his position as CEO of Binance. He emphasized that he is not a trader but a long-term holder, which is consistent with his usual investment style.

CZ's Ambition: From BNB to ASTER, a Deep Defense of the Binance Ecosystem

CZ's support for Aster is by no means a spur-of-the-moment decision. As early as September of this year, he interacted with Aster-related content on social media multiple times, praising its Hidden Order feature and pointing out that "it was implemented in just 18 days after its launch, which is much faster than more than 30 similar projects."

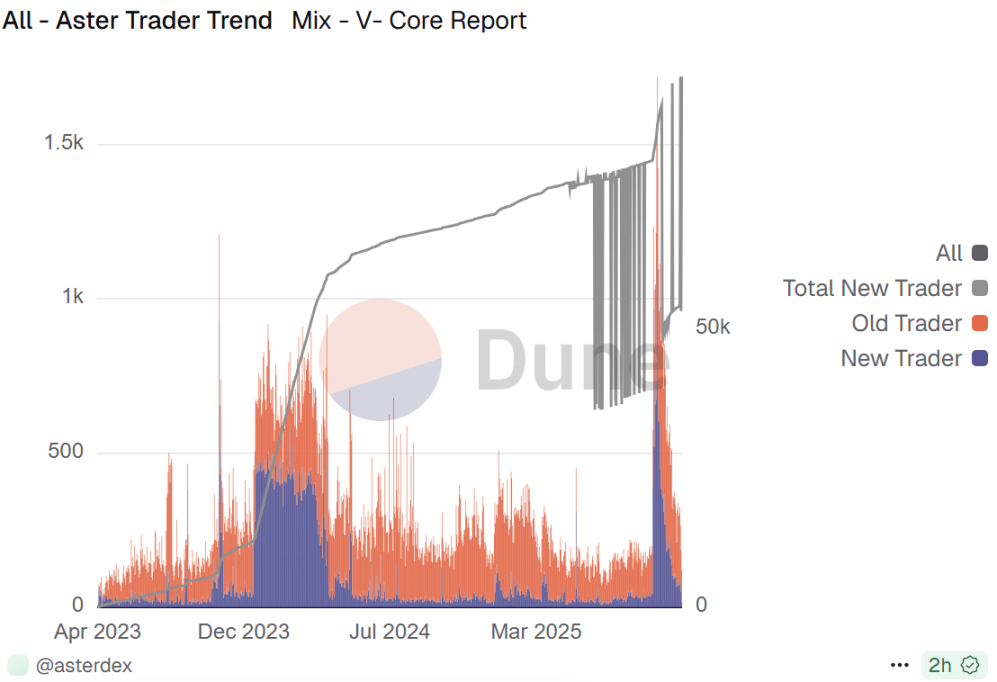

At the time, Aster had just completed its token generation event (TGE). Driven by CZ's shill, its token price surged by 1650% within 24 hours, soaring from $0.0089 to $0.78, with trading volume exceeding $310 million and the number of users surging by 330,000.

CZ's open acquisition of Aster reflects his strategic positioning in the decentralized perpetual exchange (Perp DEX) sector. YZi Labs (formerly Binance Labs), which he founded, is the incubator behind Aster, making Aster a true rising force within the "Binance ecosystem." For Binance, supporting Aster is a combination of defense and offense. Defensively, if Aster grows into a leading platform, Binance will indirectly benefit due to its capital relationship, avoiding complete marginalization. Offensively, through Aster, Binance can proactively position itself in the decentralized sector, thus maintaining a buffer against competitors like Hyperliquid.

Aster's Rise: A 2500% Surge in Three Weeks, Technological Advantages Build a Moat

Aster is not a project that appeared out of nowhere; it is a decentralized perpetual contract exchange formed by the merger of Astherus and APX Finance at the end of 2024. The merged Aster aims to solve the inefficiency of separating yield generation from trading activity in DeFi, creating an ecosystem that seamlessly connects yield and trading.

Aster's core innovation lies in its "Trade & Earn" model, which allows users to use yield-generating assets as margin for perpetual contract trading, enabling multiple sources of capital income. Simultaneously, Aster offers 24/7 non-custodial trading, supporting cryptocurrency and traditional stock perpetual contracts, thus becoming a bridge connecting traditional finance and DeFi.

Aster demonstrates a significant advantage in its technical architecture. Its underlying architecture employs an "off-chain order book + on-chain clearing" system, achieving a transaction confirmation speed of only 0.3 seconds, far exceeding Hyperliquid's 1.2 seconds. Furthermore, Aster supports leverage trading up to 1001x, significantly higher than the industry average.

Aster offers a dual-mode trading experience: Simple mode provides one-click execution and is protected by MEV, suitable for novice users; Pro mode offers advanced tools such as order books, hidden orders, and grid trading to meet the needs of professional traders. This dual-mode design allows it to attract users at different levels. In the past three weeks, the price of Aster tokens has surged from a low of $0.07 to $1.79, a cumulative increase of 2500%. Its daily transaction fee revenue is approaching Tether's, just $3 million shy of surpassing it.

Hyperliquid's competitive advantage: sub-second transactions and first-mover advantage

Faced with Aster's strong rise, Hyperliquid, the current king of the decentralized perpetual contract track, is no pushover.

Hyperliquid is an L1 public blockchain built specifically for financial transactions, and like Ethereum and Solana, it is an independent blockchain. Hyperliquid's core advantage lies in its technical architecture. It uses the self-developed Hyperliquid Chain to achieve sub-second transaction confirmation, a throughput of up to 200,000 TPS, and liquidity comparable to centralized exchanges.

This extreme technological optimization makes Hyperliquid's trading experience almost indistinguishable from centralized exchanges. In terms of liquidity, Hyperliquid also demonstrates its leading position.

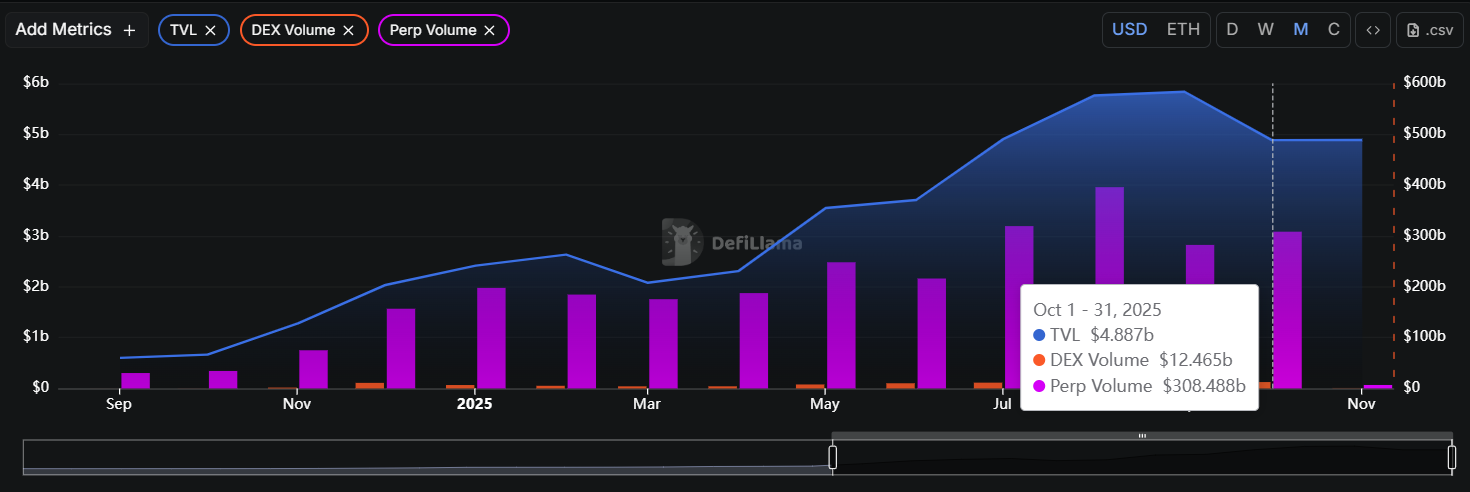

As of October 2025, the platform's total value locked (TVL) was approximately $4.8 billion, accounting for 80% of the Perp DEX market share. Its cumulative trading volume has exceeded $2.3 trillion, and its open interest has reached $15.2 billion.

Hyperliquid's token economics model is also ingeniously designed. HYPE token stakers can enjoy annualized returns of up to 40%, as well as fee discounts. The platform injects 93% of its fees into the Assistance Fund (AF), which is used to buy back and burn HYPE tokens, creating a positive feedback loop.

However, Hyperliquid is facing internal challenges. Under its token economics arrangement, HYPE will enter a 24-month linear unlocking period on November 29th, releasing approximately $500 million worth of tokens each month, which could create sustained selling pressure.

Competition Heats Up: The Battle Behind the Data

Looking at key metrics, the competition between Aster and Hyperliquid has fully commenced. In terms of trading volume, Aster has performed strongly since its launch, with a peak daily trading volume of $42 billion, while Hyperliquid's average daily trading volume is approximately $7.9 billion.

However, Hyperliquid still maintains its lead in terms of user base.

As of the end of October, Hyperliquid had 688,000 users, while Aster, despite rapid growth, had 1.848 million users (including airdrop users), but its actual active trading users still lagged behind Hyperliquid. Transaction fees are a key dimension of competition between the two.

Aster's base rates are slightly lower than Hyperliquid's (Aster maker 0.01%/taker 0.035%, Hyperliquid maker 0.01%/taker 0.045%), a pricing strategy that is highly attractive to high-frequency trading users.

In terms of asset coverage, Aster supports perpetual contracts for 40 cryptocurrencies, 15 more than Hyperliquid, and has added popular coins such as SOL and APT.

More importantly, Aster also offers perpetual stock contracts, such as those for Apple and Tesla, further expanding its product offerings.

In terms of technical architecture, the two represent two different development paths: Hyperliquid focuses on building its own L1 and pursuing ultimate transaction speed; Aster, on the other hand, focuses on multi-chain routing and emphasizes cross-chain liquidity aggregation. The former represents performance first, while the latter pays more attention to the boundless connection of liquidity.

Risks and Challenges: Hidden Concerns Facing Aster

Despite Aster's outstanding performance, the risks lurking behind it cannot be ignored.

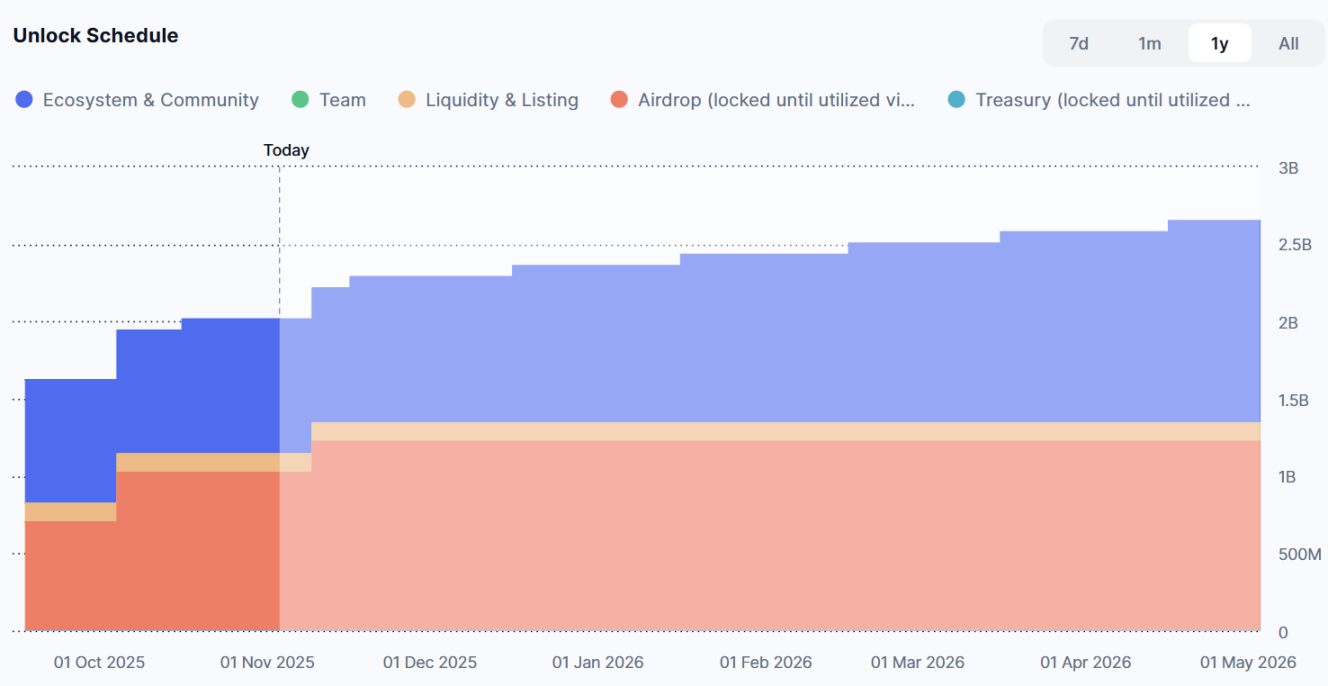

In terms of token economics, ASTER has a total supply of 8 billion tokens and will have two cliff-like unlocks in November: approximately 200 million tokens (2.5% of the total supply) will be unlocked on November 10, worth approximately $240 million; and approximately 72.73 million tokens (0.91% of the total supply) will be unlocked on November 17, worth approximately $87.276 million.

Large-scale unlocking could create significant selling pressure in a market with limited liquidity. To address this challenge, Aster has launched the S3 buyback program, committing to using 70%-80% of transaction fees to repurchase ASTER shares on the open market, executed daily until the cumulative amount reaches a target range.

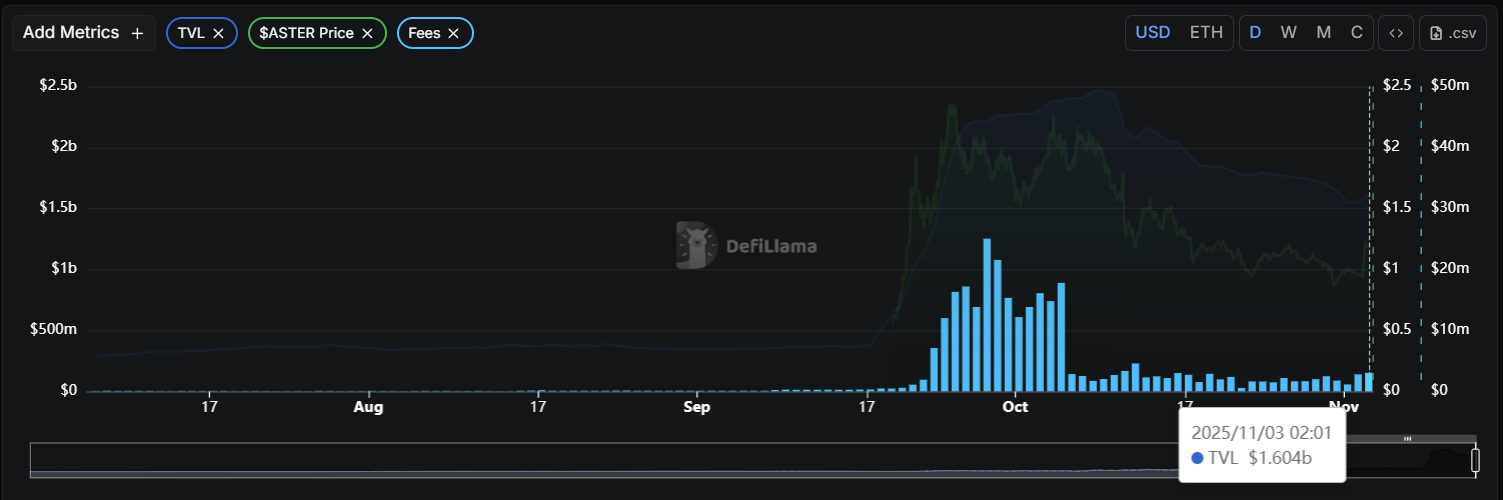

According to DefiLlama data, Aster's daily transaction fees have recently exceeded $2 million, which translates to approximately $1.35 million to $1.54 million in daily repurchase amounts.

On October 31, the official announcement further stated that 50% of all repurchase funds would be used for burning to reduce supply and solidify ASTER's long-term value.

Market Restructuring: The Future Direction of the Perp DEX Track

Aster's rapid rise is changing the competitive landscape of the decentralized derivatives market.

Previously, Hyperliquid held a dominant position, occupying 80% of the market share, which led to stagnation in innovation in the industry and persistently high transaction fees.

Aster's entry into the market is forcing the industry to iterate its technology. In response to competition, Hyperliquid has announced a "0.02% fee package" to be launched in October and is accelerating the development of cross-chain transaction functionality. This healthy competition ultimately benefits the entire decentralized perpetual contract ecosystem.

The competition in the Perp DEX sector is essentially a battle between ecosystem collaboration and technological idealism. Aster has expanded rapidly by leveraging the resources of the Binance ecosystem, achieving astonishing growth figures in a short period.

Hyperliquid, on the other hand, maintains a large user base and deep liquidity by leveraging its technological advantages and first-mover advantage. This competition has also attracted more investment to the decentralized contract (DPC) field.

Since the beginning of this year, over $500 million in venture capital has flowed into this sector, and more than 10 new projects are expected to launch in the next six months, with the sector's size potentially exceeding $50 billion.

From a broader perspective, decentralized derivatives trading is still in its early stages of development. Currently, the trading volume of the entire decentralized perpetual contract market accounts for only about one-tenth of that of centralized exchanges, indicating huge potential for growth.

Especially during September and October of this year, a large influx of new users arrived, with daily increases even exceeding the levels seen during the bull market of early 2024. Faced with a large unlock in November, Aster attempted to alleviate selling pressure through an on-chain buyback mechanism. However, Hyperliquid, with its solid technological foundation, deeper liquidity, and more mature token economic model, continues to maintain strong competitiveness.

Whether Aster can surpass Hyperliquid in the long run remains to be seen. When the market refocuses on fundamentals, projects like Hyperliquid, with real technological advantages and stable cash flow, are more likely to prevail in the long-term competition.