Written by: Michael Howell

Translated by: Block unicorn

Asset allocation is usually done in a vacuum, with little consideration of the monetary policy investors will face. The standard method is to establish a portfolio allocated in a 60:40 ratio, investing in stocks (risk assets) and high-quality bonds (safe assets). The rationale is that these two asset classes are often negatively correlated, especially during economic recessions.

Although this thinking forms the cornerstone of modern wealth management, in reality, it only applies during specific times and under special circumstances. These time periods lasted from the early 1980s until the Global Financial Crisis (GFC) in 2008/09. This approach was not applicable in the 1970s and can be argued to be inapplicable today.

The key to understanding wealth management and asset valuation lies in inflation. In short, although we obviously want to become wealthier, our primary focus is at least maintaining the actual wealth level. Assets should not be compared with each other (such as bonds versus stocks), but should be compared with inflation.

Inflation can be a difficult concept to measure, but for illustration purposes, assume it represents the loss of purchasing power of paper currency. Inflation can originate from monetary inflation, i.e., "printing money," or from cost inflation, such as rising oil prices and declining productivity.

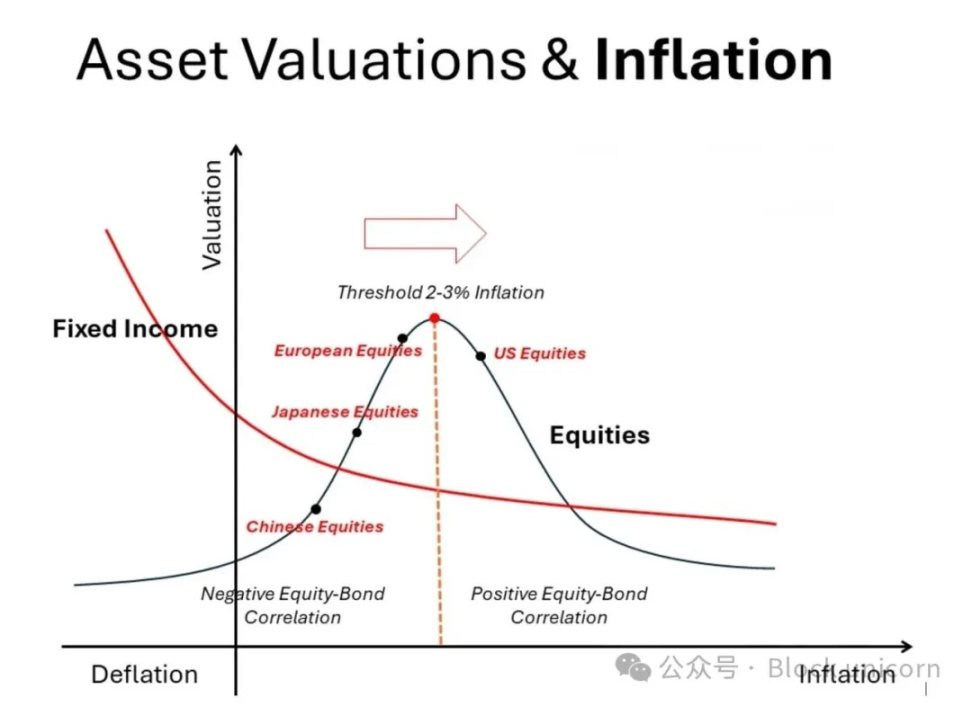

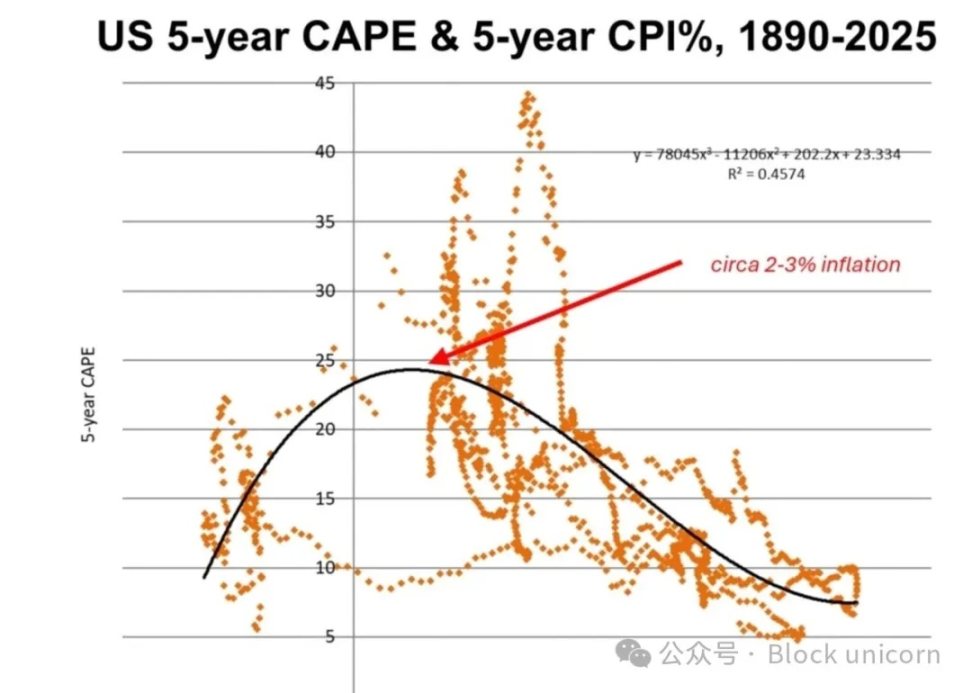

The following diagram shows how inflation affects the valuation of different asset classes. The chart is illustrative, but can be empirically constructed using long-term data published by academic Robert Shiller on his website. We have used data since 1880 to demonstrate our version. The curves are fitted using polynomial regression.

High-quality bonds (such as US Treasuries) exhibit a monotonic relationship: as inflation accelerates, their valuation declines (yields rise); as deflation approaches, their valuation increases (yields fall). Textbooks also acknowledge this trade-off. Physical assets (not shown in the chart), such as residential real estate, land, gold, or perhaps Bitcoin, follow a completely opposite path. As inflation accelerates, their valuation and prices rise accordingly.

In contrast, the relationship between stocks and inflation is more complex and non-linear. This is not mentioned in financial textbooks. On both sides of the 2-3% inflation "sweet spot" (where price-to-earnings valuation peaks), increases and decreases in inflation rates lead to valuation declines. In other words, to the left of this valuation peak, stocks and bonds are negatively correlated (the "risk parity" area), while on the right side, they are positively correlated. The change in correlation patterns requires significant adjustments in portfolio construction.

Most of our investment experience since the 1980s has been in the "low" inflation area, mostly around and to the left of this valuation peak. This not only strongly supports a large allocation to stocks but also proves that holding bonds is reasonable due to their negative correlation with stocks, as even small changes in inflation rates demonstrate. This is especially evident during economic weakness or when testing deflation. Japan's history has proven what happens to stock and bond valuations within the "extremely low" inflation zone.

But this was not characteristic of the inflationary period in the 1970s. At that time, physical assets were in high demand, while financial assets performed poorly. The reasons can be seen through the same chart. On the right side of the valuation peak, around 2-3% inflation and above, both stock and bond valuations decline. Moreover, their decline is synchronized. This correlation weakens the rationale for holding both assets in a portfolio. In fact, the opposite and positive performance of physical assets against inflation enhances the reason for including them in the portfolio.

Rising Monetary Inflation

Our recent research has mainly focused on the accumulation of monetary inflation risk, i.e., governments deliberately devaluing paper currency. [We maintain a neutral stance on cost inflation.] The chart includes a rightward arrow as a reminder. In other words, the 60:40 asset allocation (or "risk parity" approach) is facing a serious threat. Looking forward, investors should now be thinking about: reducing bond holdings and increasing physical assets.

Admittedly, the chart we drew shows that the right tail of the stock valuation bell curve is lower than the bond valuation line. Of course, this is not always the case. Unlike bond coupons, stock returns and dividends may rise with inflation. Different stocks will have different valuation trends, as some stocks are better at hedging inflation and thus may maintain relatively high valuations. On the other hand, many businesses struggle to remain profitable in high-inflation environments. However, we are discussing general situations here, not specific details.

Global bond yields are gradually rising. This is more driven by increased term premiums rather than higher policy rates. This suggests that yield increases may be jointly caused by rising inflation uncertainty and concerns that high government spending will lead to more bond supply.

Looking across markets, we believe the United States currently faces greater inflation uncertainty, both due to its massive fiscal deficit and the expected increase in "business taxes" due to tariff imposition. More importantly, fiscal deficits are increasingly funded by short-term securities, which increases the risk of monetary inflation.

Japan recently experienced an inflation rise, mainly due to rising wage costs, but this is after experiencing decades of deflation and intermittent disinflation. In other words, placing Japan on the above chart, its stock valuations might rise to the 2-3% inflation "sweet spot". Clearly, at current low levels, the 1.5% Japanese Government Bond (JGB) yield does not look attractive.

China is currently in a post-"tariff shock" deflationary phase, possibly at an earlier stage than Japan. Chinese stock market valuations are low, but further monetary stimulus and a more robust economy could easily shift investor sentiment back to the stock market.

Meanwhile, according to inflation standards, European stocks are close to the ideal "sweet spot," but they are between the US and Asian markets. In other words, if inflation continues to rise (we believe the world is heading towards stagflation), European stock valuations are more likely to follow the US and gradually be adjusted downward.

Asset Allocation Conclusion

The 60:40 or "risk parity" model, favored by wealth managers for decades, faces severe challenges in a monetary inflation environment. We tend to reduce bond allocations or at least shift some bonds towards inflation-linked bonds (TIPS).

Asset portfolios should be tailored to investors, but using the 60:40 financial asset benchmark as an example, we are more inclined to strategically adjust the asset portfolio to 60:10:10:10:10. Here, 10% might be allocated to TIPS; 10% held in cash; 10% increased in gold and precious metals, 10% invested in Bitcoin. We exclude specialized physical assets like premium residential real estate and land, not because they are unattractive, but because they are less liquid and typically a permanent and non-tradable component of investor wealth.

Moderate inflation rise might be beneficial to the stock market overall. We have depicted nominal positions of different markets in the chart above. It can be said that Wall Street is "past its peak" due to inflation issues in the US economy. European inflation rates remain moderate, while China and Japan are emerging from deflationary/low-inflation environments that favor bonds over stocks. It might be worth investing in these Asian markets, but be wary of their greater geopolitical risks.