Author: Byron Gilliam

Translated by: TechFlow

"The social objective of skilled investment should be to defeat the dark forces of time and ignorance that envelop our future."

—— John Maynard Keynes, famous economist

Storytime for Crypto Investors

Although investment involves numerous figures, people generally believe that investment is more of an art than a science.

"The selection of common stocks is a difficult art," Benjamin Graham once warned.

Warren Buffett, Graham's lifelong student, further clarified, "Investment is an art... putting cash in now with the expectation of getting more cash in the future."

Almost all investments ultimately boil down to predicting future cash flows.

But Peter Lynch reminds us that investors "trained rigidly to quantify everything" are at a significant disadvantage.

However, this does not mean, as some financial nihilists claim, that "valuation is just a meme."

Instead, it means that applying and interpreting quantifiable valuation metrics is itself a creative activity.

Choosing which valuation metric applies to which investment is a subjective decision—and knowing how to interpret these results is even more so.

For example, low valuation does not necessarily mean a stock is cheap, and high valuation does not necessarily mean a stock is expensive (often the opposite is true).

A stock might look very cheap on some metrics but extremely expensive on others.

And there is no obvious correlation between these valuations and actual returns.

This often feels frustrating—if cheap stocks won't rise and expensive stocks won't fall, why bother figuring all this out?

I believe it's worth studying because this is precisely what makes investment interesting and engaging—and if that's the case, the fun of crypto investment is just beginning.

Until recently, crypto investors had very limited data choices, with almost no available data beyond token price and market cap.

This made everything in the crypto realm a "story"—but that's okay!

Investment is essentially the art of storytelling.

However, the best investment stories are often told through numbers, and the crypto realm is gradually developing such conditions as more protocols begin generating revenue, with more of this revenue being allocated to token holders.

Moreover, thanks to efforts by institutions like Blockworks Research , these numbers are becoming more accessible. Their analysts package this data into easy-to-understand charts and reports for our reference.

This helps the crypto realm move towards a higher narrative stage: storytelling through numbers.

Let's look at some current figures.

Ethereum vs. Solana

Judging from crypto Twitter and podcasts, Ethereum's market sentiment seems to have hit a new low, especially compared to Solana.

But if a traditional finance (TradFi) newcomer directly looks at the data, they might draw a completely different conclusion.

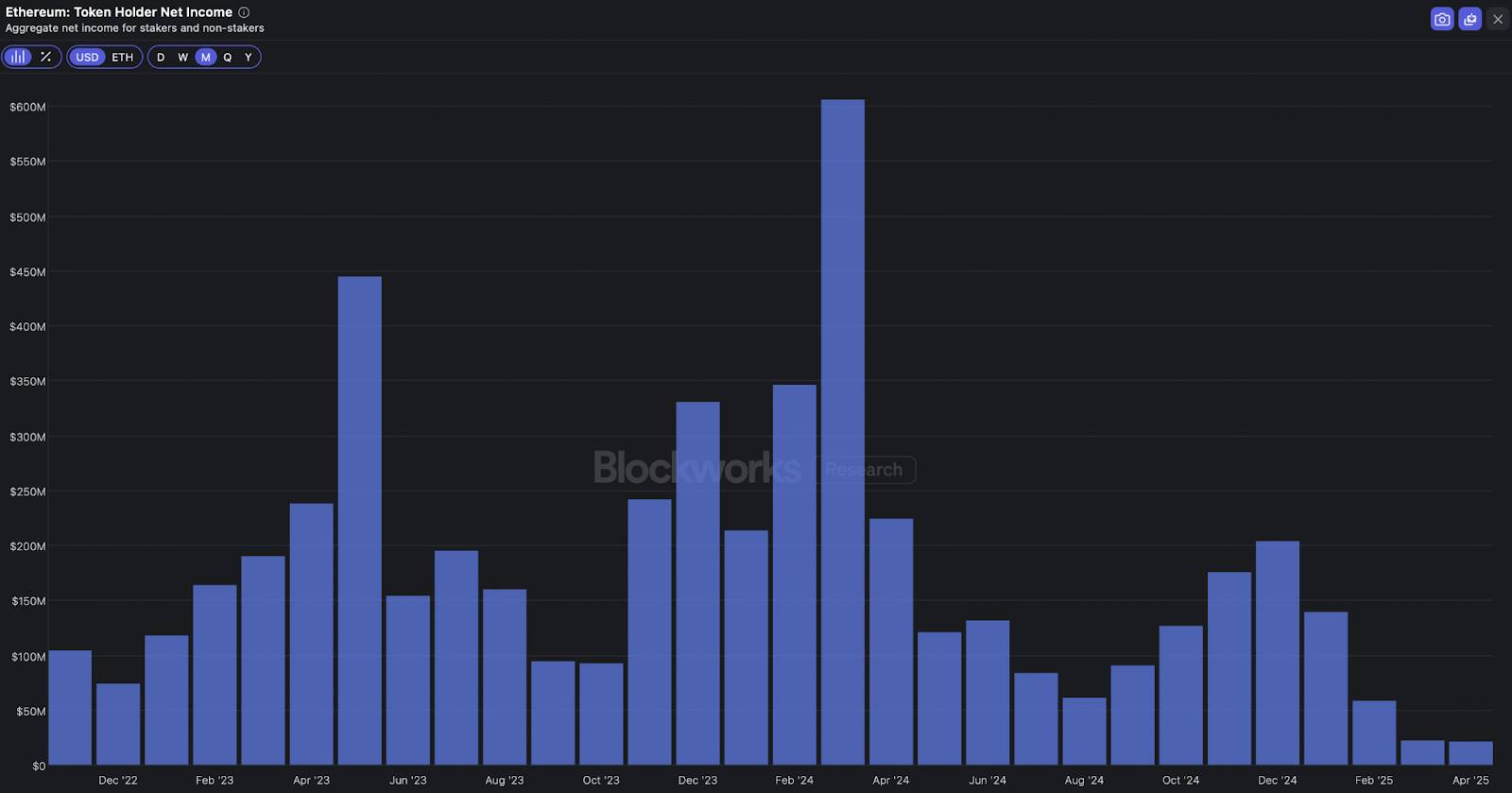

According to Blockworks Research data, Solana recorded $36 million in "token holder net income" in April, making the SOL token's annualized yield multiplier 178 times—which might be reasonable if current activity levels are considered low.

In comparison, Ethereum's token holder net income in April was $21 million, making the ETH token's yield multiplier as high as 841 times.

A traditional finance (TradFi) investor seeing that ETH's valuation multiplier is 5 times that of SOL would not immediately think, "Wow, why is everyone so pessimistic about Ethereum?"

But they also wouldn't immediately conclude that the market views Solana 5 times more positively than Ethereum.

Instead, they might conclude that Solana's revenue valuation is lower, possibly because it primarily comes from "low-quality" meme coin trading activity; while Ethereum's revenue valuation is higher, at least partly because it includes higher-quality activities, such as income related to real-world assets (RWAs).

Now we have some angles to analyze: if you believe meme coin trading activity is not so low-quality, SOL might be undervalued; if you believe real-world assets are the future trend, ETH might not be overvalued.

Of course, you can dig deeper for more information.

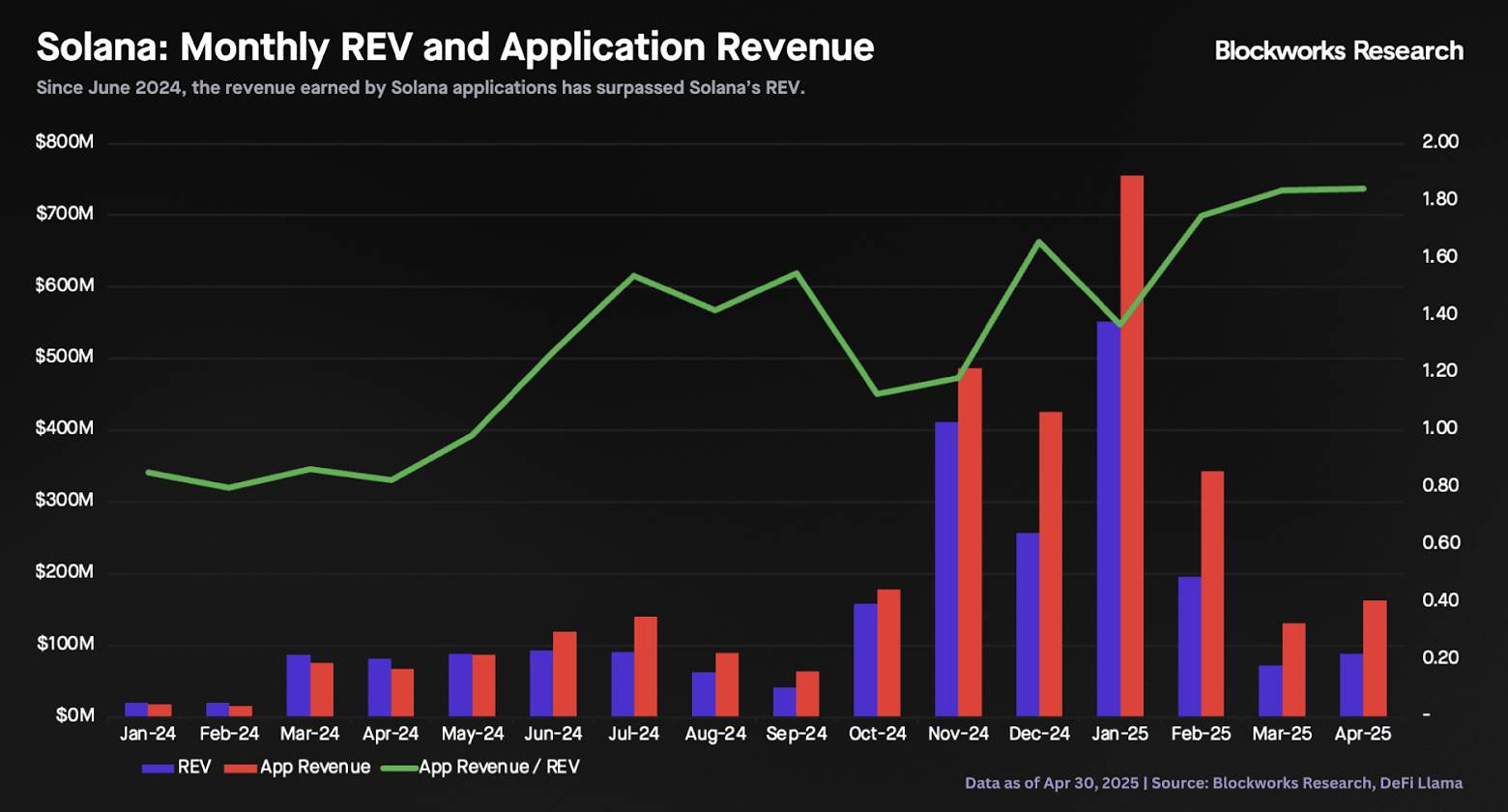

According to Blockworks Research data, the total income of all Solana applications is only about 1.8 times Solana's own income.

For a platform business, this is a very high take rate—far above Apple's 30% cap, which the US government even considers monopolistic.

This could mean Solana's income is too high, so its token valuation multiplier should be low; or it could indicate that Solana has a business moat, so its token valuation multiplier should be high.

Whichever the case, it's a story worth paying attention to.

Hyperliquid

Hyperliquid is a semi-decentralized crypto exchange with a somewhat unique story: the protocol generated $43 million in revenue in April and almost entirely allocated this income to token holders.

Unsurprisingly, this model has helped its token perform exceptionally recently. As Blockworks Research's Boccaccio noted in a recent report: "The aid fund uses trading fees for token buybacks every 10 minutes, creating continuous buying pressure."

Every 10 minutes!

It's hard to make a clear judgment because in traditional finance, no company returns 100% of its income to shareholders—let alone every 10 minutes.

From its valuation, the crypto market seems somewhat hesitant about this.

The HYPE token's trading valuation is about 17 times its annualized income (based on market cap), which would typically be considered expensive.

But in this case, income and profitability seem to be the same thing, so if you believe HYPE can continue winning business from centralized exchanges, such a valuation still seems quite reasonable.

Boccaccio notes that HYPE's trading valuation multiplier is significantly higher than its decentralized peers, but these peers might not be appropriate comparisons.

"Hyperliquid's L1 only needs to capture a small portion of Binance's daily trading volume to significantly increase its trading volume... capturing just 10-15% of BTC/USDT trading volume from Binance could increase HyperCore's trading volume by 50%."

"Therefore, the growth multiplier is reasonable," Boccaccio concluded.

Of course, the size of this multiplier depends on how much you trust the story.

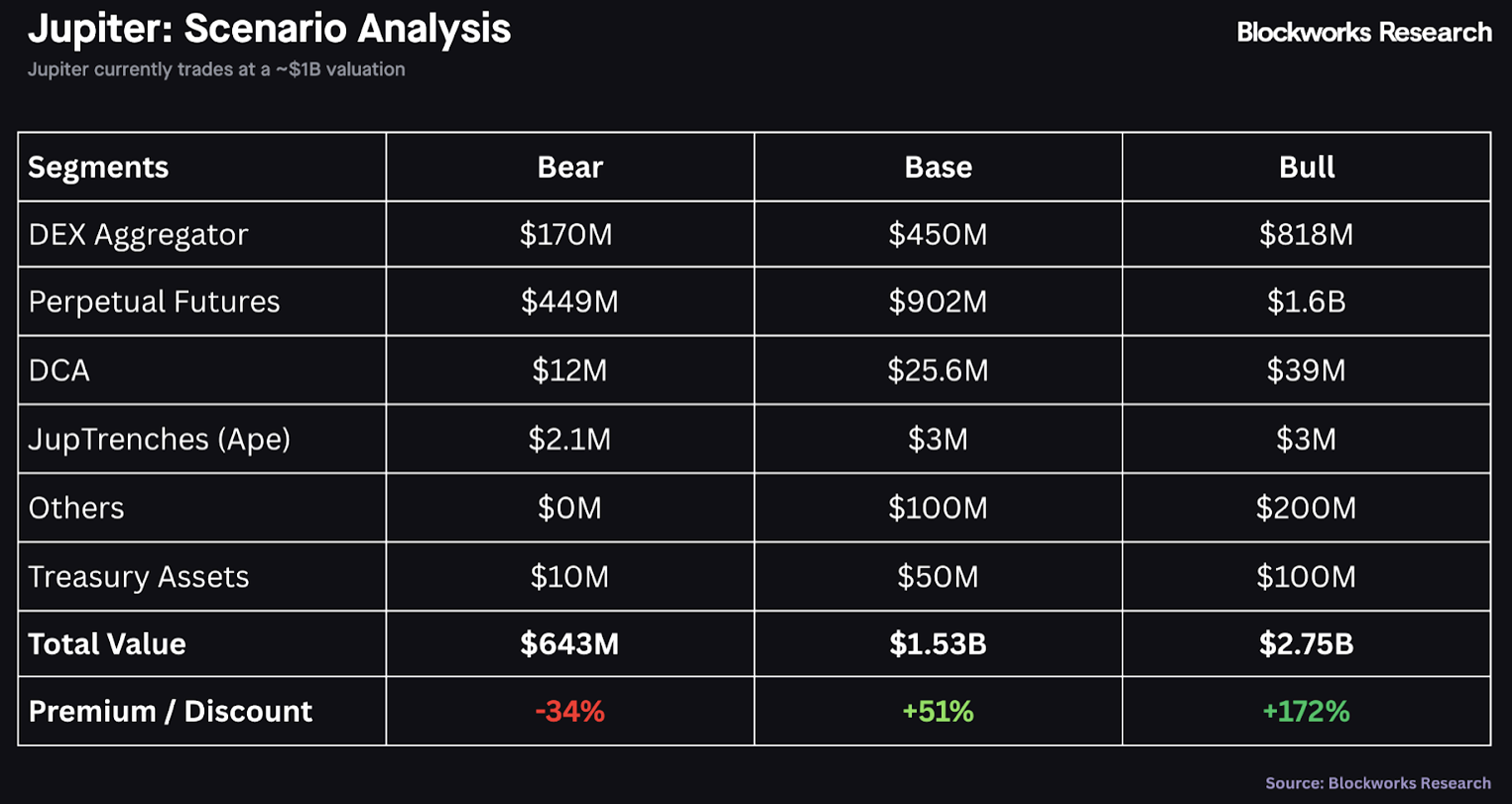

Jupiter

Jupiter is a decentralized exchange (DEX) aggregator on Solana that returns a relatively modest 50% of income to token holders (also through buybacks)—but its income is equally impressive.

Marc Arjoon estimates that Jupiter could generate $280 million in revenue in the next 12 months, meaning the JUP token's yield is about 11.5% based on market cap.

In the stock market, an 11.5% yield would typically mean the related business is struggling, but that doesn't seem to be the case here.

Jupiter is the "default router on Solana," Arjoon wrote, "currently unrivaled in the aggregation domain," and "the fourth highest-earning app among all crypto dapps".

More importantly, it is being operated like a true enterprise: "Jupiter's strategic actions in 2024-2025 indicate that it is an organization actively entering a high-growth phase, ambitiously positioning itself as the top crypto super app for Solana."

This sounds nothing like a company that should have an 11.5% yield rate.

Of course, many risks still exist, which Arjoon detailed in his recent report.

But his conclusion is that "Jupiter's current trading valuation multiple is attractive compared to peers, indicating significant upside potential even without multiple expansion."

He even quantified this through a segment valuation analysis, which comforted my traditional financial background:

This looks like a good story.

Helium

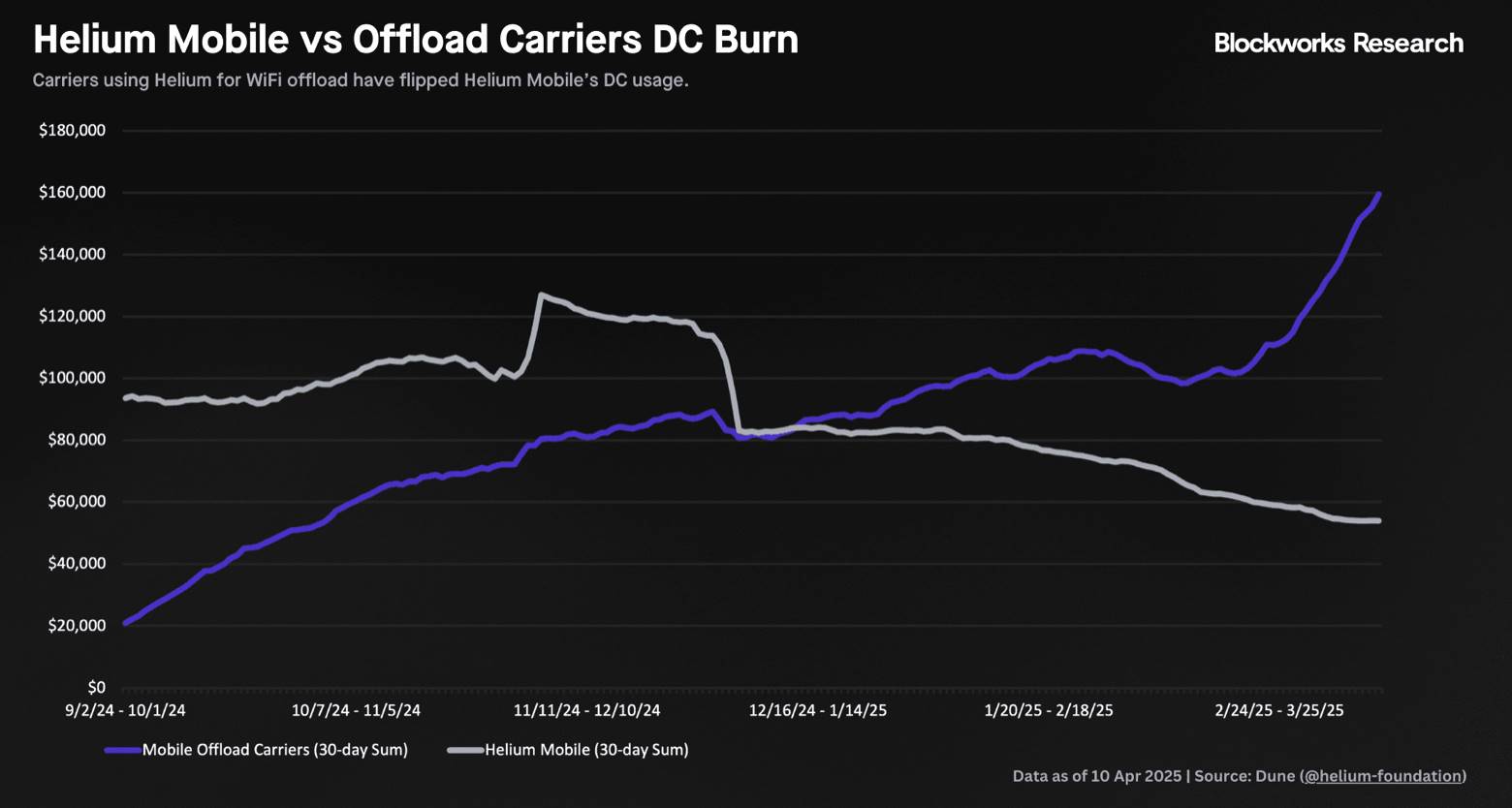

Helium, a decentralized telecommunications service provider, has long been a hot topic in the crypto field - it was established as early as 2013.

But now, it's more than just a story, it's a story with data: "Income measured by Data Credit Burn is accelerating, with a quarter-on-quarter growth of 43%," wrote Nick Carpinito from Blockworks Research in a recent report.

"More importantly, Helium's revenue sources are gradually shifting from Helium Mobile to Mobile Offload, which now accounts for about three times the Data Credit Burn and is growing quarter-on-quarter by nearly 180%, an astonishing growth rate for a DePIN protocol in enterprise budgets."

"Mobile Offload" is the blue line in the chart, with a quarterly growth rate of 180%, which is a shocking number for anyone.

Helium's HNT token seems to have reflected this in its valuation, currently trading at about 120 times annual sales.

But Carpinito mentioned in the 0xResearch podcast that he expects revenue to further accelerate growth because "AT&T allows its US users to connect to the Helium network, driving a surge in data credit usage".

Therefore, "In the next 12 months, we are likely to see an unprecedented rise in HNT price, and this rise will be more stable than previous Helium price fluctuations based on speculation."

In the crypto field, it is very rare to hear someone make such a price prediction based on non-speculative factors.

And it's refreshing.

Pendle

Lastly, Pendle is a "yield trading" protocol, and its new product "Boros" will allow users to speculate on yields from any on-chain or off-chain source, starting with funding rates.

"This implementation is similar to the classic interest rate swap market, where traders can pay floating rates to obtain fixed rates, or pay fixed rates to obtain floating rates, and support leveraged trading," explained Luke Leasure from Blockworks Research.

For a traditional finance person like me, this sounds somewhat complex, but obviously, it's a huge market: "The perpetual futures market settles nearly $60 trillion annually, with outstanding amounts in the hundreds of billions. Boros will enter an entirely new, massive, and undeveloped market," Leasure said, predicting that Boros could potentially double Pendle's revenue.

This is rarely heard in traditional finance.

In an optimistic scenario, Leasure estimates that Pendle's vote-escrowed token might be trading at just 1.6 times earnings:

1.6 times!

In the stock market, a valuation this low would only occur when a company is about to collapse, but this is clearly not Pendle's situation.

Nevertheless, this is not investment advice (at least not from me), because Pendle's story is quite complex - like most projects in the crypto field.

But at least now, these stories can be told through numbers.

—Byron Gilliam