Author: Ignas | DeFi Research

Compiled by: TechFlow

What fascinates me about the crypto market as a part of finance and trading is that it clearly tells you what is right and what is wrong.

Especially in this chaotic world, whether it's politics, art, journalism or many other industries, the line between truth and lies is blurred. Cryptocurrency is simple and direct: if you are right, you make money; if you are wrong, you lose money. It's that simple.

But even then, I fell into a very basic trap: I didn’t re-evaluate my portfolio when market conditions changed. When trading Altcoin, I became too complacent with “untouchable HODL” assets like ETH.

Of course, adapting to new realities is easier said than done.

There are so many variables we need to consider that we often choose simple narratives, such as HODL (hold for the long term), because it does not require us to actively monitor the market.

But what if the era of HODL is over? What is the role of cryptocurrency in this changing world? What are we missing out on?

In this blog, I will share what I believe are the major changes taking place in the market.

The End of the HODL Era

Let's travel back to the beginning of 2022:

ETH’s price is currently hovering around $3,000 after a sharp drop, down from its previous high of $4,800. BTC’s price is around $42,000. However, both subsequently fell by 50% due to interest rate hikes, the collapse of centralized finance (CeFi), and the collapse of FTX.

Despite this, the Ethereum community remains optimistic: ETH is about to migrate to PoS (Proof of Stake), and the EIP proposal for ETH destruction was launched just a few months ago. The narrative of ETH as "Ultrasound Money" and an environmentally friendly, energy-efficient blockchain is very popular.

However, for the rest of 2022, ETH and BTC performed poorly, while SOL suffered a brutal decline, with its price plummeting 96% to just $8.

Ethereum has won the L1 war, while other L1s must either migrate to L2 or face extinction.

I remember attending meetings during the bear market where most people were convinced that ETH would rebound the strongest, so they bought ETH heavily while underweighting BTC, completely ignoring SOL. The strategy was simple: HODL, then sell at the peak of the bull market in 2024/25 . Easy peasy.

However, reality slapped me in the face!

Since then, SOL has rebounded, while Ethereum has faced the strongest panic selling (FUD) ever.

The “ultrasonic money” narrative is dead (at least for now), and the environmental (ESG) narrative never really caught on.

HODLing ETH was the biggest mistake I made in this cycle. I believe this is a regret shared by many people.

My bullish logic for ETH is that it will become the most productive asset in the crypto market.

Through restaking, ETH will gain "superpowers" to protect not only Ethereum, but also the entire critical DeFi and crypto infrastructure. ETH's restaking income will soar, and airdrop rewards will continue to accumulate through restaking ETH.

As yields increase, demand for ETH and its price should rise. Bottom line: To the moon!

Obviously, this did not happen as the value proposition of restaking was never clear and Eigenlayer did not do well with token issuance.

So what does all this have to do with HODL’s Metaverse being dead?

For many, ETH has been a “buy it and forget it” asset. If BTC goes up, ETH usually goes up more, so it seems meaningless to hold BTC.

When my bullish logic for ETH based on the re-staking narrative failed to materialize, I should have recognized it and adjusted my strategy in time. However, I became lazy and complacent and was unwilling to admit my mistakes. I told myself: ETH will rebound one day, right?

HODL is bad advice not only for ETH, but for other assets as well, with perhaps the only exception being BTC (more on that later).

The crypto market moves so fast that it is unrealistic to expect to retire after holding an asset for a few months or even years. Looking at the charts, most Altcoin have given back the gains they made in this bull cycle. Obviously, profits come from selling, not holding.

One successful memecoin trader said that instead of HODLing, he usually holds a memecoin for less than a minute.

While there are still people trying to sell you the dream of HODL, it is more of a “quick in and out” cycle than true HODL.

BTC is the only macro crypto asset

The only exception to the “quick in and out” strategy is BTC.

Some attribute BTC’s outperformance to Michael Saylor’s “unlimited buy order” because we have successfully promoted BTC as “digital gold” to institutional investors.

However, the battle is far from over.

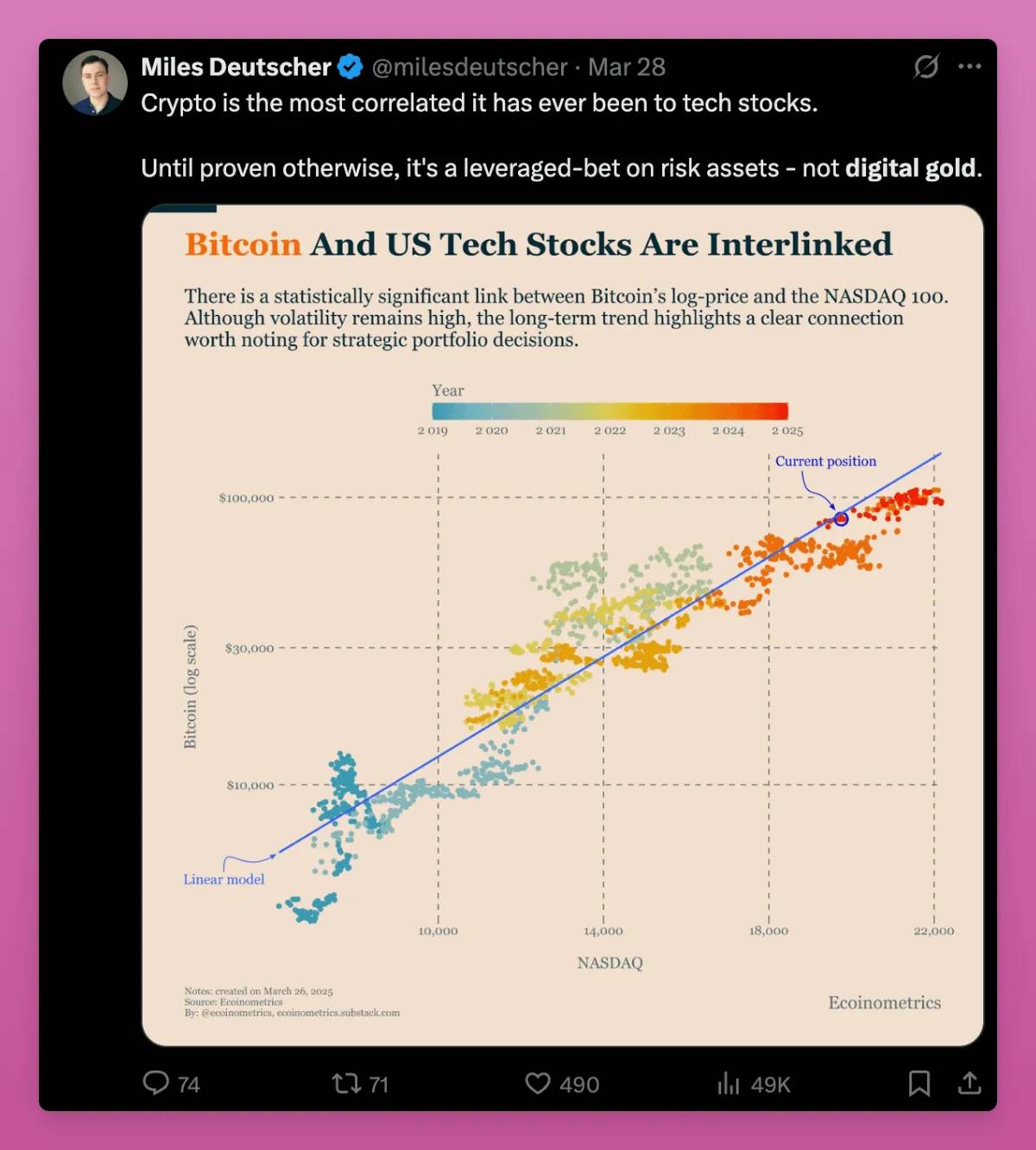

Many crypto commentators still view BTC as a high-volatility risk asset, similar to betting on the S&P 500.

This view contradicts research from Blackrock, which found that the risk and return drivers of BTC differ from those of traditional risk assets, making it unsuitable for the “Risk On/Risk Off” model in traditional financial frameworks, an analytical approach used by some macroeconomic commentators.

I shared some observations about the less obvious truth in the post Crypto Truth and Lies in 2025: What Do You Believe Is the Truth?

I believe Bitcoin (BTC) is moving from those who view it as a highly leveraged stock bet to those who view it as a digital, safe-haven, gold-like asset. Mexican billionaire Ricardo Salinas is an example of someone who is holding on to BTC.

BTC is the only true macro crypto asset. The value of ETH, SOL, and other crypto assets is usually evaluated based on fees, trading volume, and total value locked (TVL), but BTC has surpassed these frameworks and become a macro asset that even Peter Schiff can understand.

This transformation is not yet complete, but the transition from a risky asset to a safe-haven asset is an opportunity. Once BTC is generally recognized as a safe-haven asset, its price will reach $1 million .

Corruption in the private equity market

When every relatively successful key opinion leader (KOL) started transforming into a “venture capitalist” (VC), investing in projects at low valuations and selling them after the token generation event (TGE), I felt that something was wrong in the market.

However, nothing better describes the current state of the crypto private placement market than this post by Noah.

Here are the core elements of the private equity market changes over the past few years:

In the early days (2015-2019), private market participants were true believers. They supported Ethereum, funded DeFi pioneers like MakerDAO and ETHLend (now Aave), and advocated long-term holding (HODLing).

The goal isn’t just to make a quick profit, but to create something meaningful.

In the DeFi summer of 2020-2022, everything changed. Suddenly, everyone was chasing the newer, hotter tokens.

Venture capital firms (VCs) are pouring money into projects with tokens that have ridiculous valuations and no practical utility.

The rules of the game are simple: participate in private rounds at low prices, hype up projects, and then dump tokens to retail investors. When these projects collapsed, we should have learned lessons from them, but nothing changed.

After the FTX incident (2023-2025), the private equity market became more nihilistic. VCs began to fund "soulless token machines" (i.e. projects that recycled old ideas, had founders with questionable backgrounds (such as Movement), and had no real use cases).

Private round valuations were set at 50x revenue (if the project had revenue), which ultimately led to the public market having to absorb these losses. As a result, 80% of tokens in 2024 fell below the private round price within six months of listing.

This is a predatory phase .

Today, retail investors’ trust is gone, and VCs are in a mess.

Many VC investment projects are traded at prices even lower than their seed round valuations, and some of my KOL friends are also suffering from losses.

However, the private equity market is showing some signs of recovery:

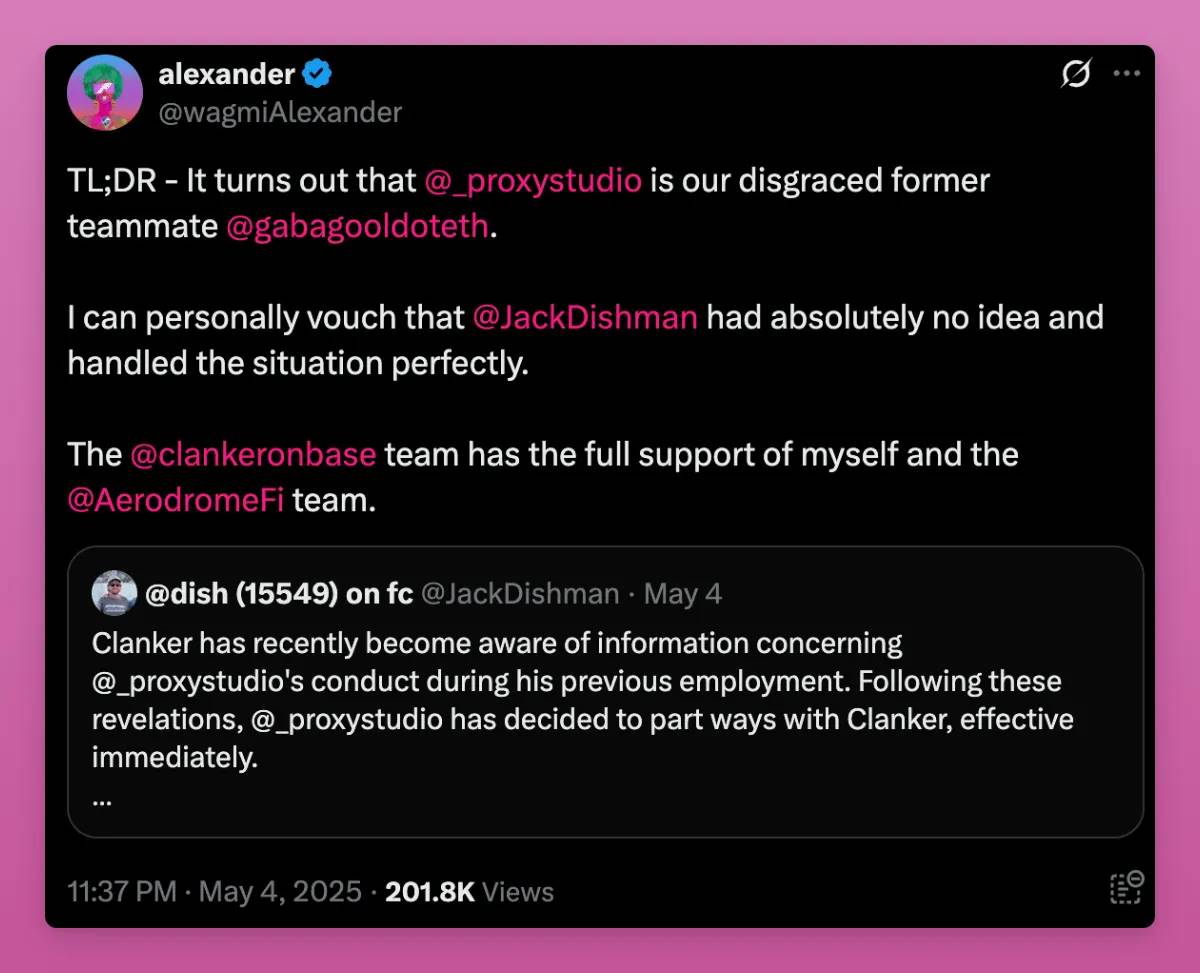

Movement co-founder and Gabagool (former Aerodrome “runaway”) were hit with backlash and kicked out of the industry. We need more clean-ups like this.

Valuations in both private and public markets are falling.

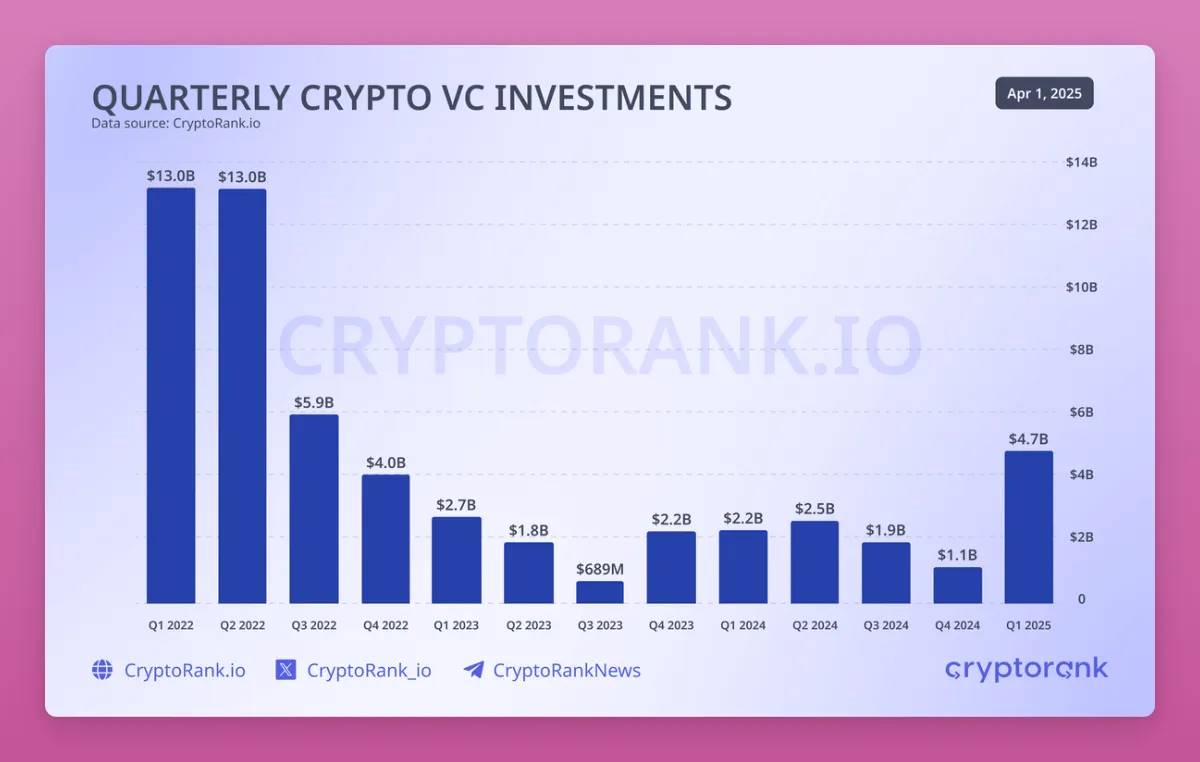

Crypto VC funding has finally rebounded: $4.8 billion was raised in Q1 2025, the highest level since Q3 2022, and funds are beginning to flow into areas with real utility.

According to CryptoRank’s “2025 Q1 Crypto VC State Report” :

Q1 2025 was the strongest quarter since Q3 2022. While the $2 billion Binance deal played a central role, 12 other large rounds of over $50 million signaled a return of institutional interest.

Capital has flowed to areas with real utility and revenue potential, including centralized finance (CeFi), blockchain infrastructure and services. Emerging focus areas such as artificial intelligence (AI), decentralized physical infrastructure networks (DePIN) and real world assets (RWA) have also attracted strong attention.

DeFi leads in number of funding rounds, but funding rounds are smaller, reflecting more conservative valuations.

We are experimenting with new token issuance models that reward early supporters rather than insiders.

Echo and Legion are leading the trend, and Base has already launched a group on Echo. The Kaito InfoFi metaverse also shows a strong bullish trend, because even people without financial capital can benefit from it as long as they have social influence.

The market seems to have learned its lesson, and the ecosystem is gradually recovering (although KOLs still occupy the best resources).

Goodbye DeFi , Welcome Onchain Finance

Remember the short story of Yield Aggregators? Yearn Finance led the trend, and then countless forked projects followed.

Today, we have entered the era of Yield Aggregators 2.0, only now we call them “Vault Strategies”.

As DeFi becomes more complex and various protocols emerge, Vaults become an attractive option: deposit assets and get the best risk-adjusted returns.

However, the main difference now compared to the first phase of yield aggregators is the rapidly increasing centralization of asset management.

Vaults have teams of "strategists" - usually "institutional investors" - who use your money to chase the best investment opportunities. For them, it's a win-win: they earn income on your capital and collect management fees at the same time.

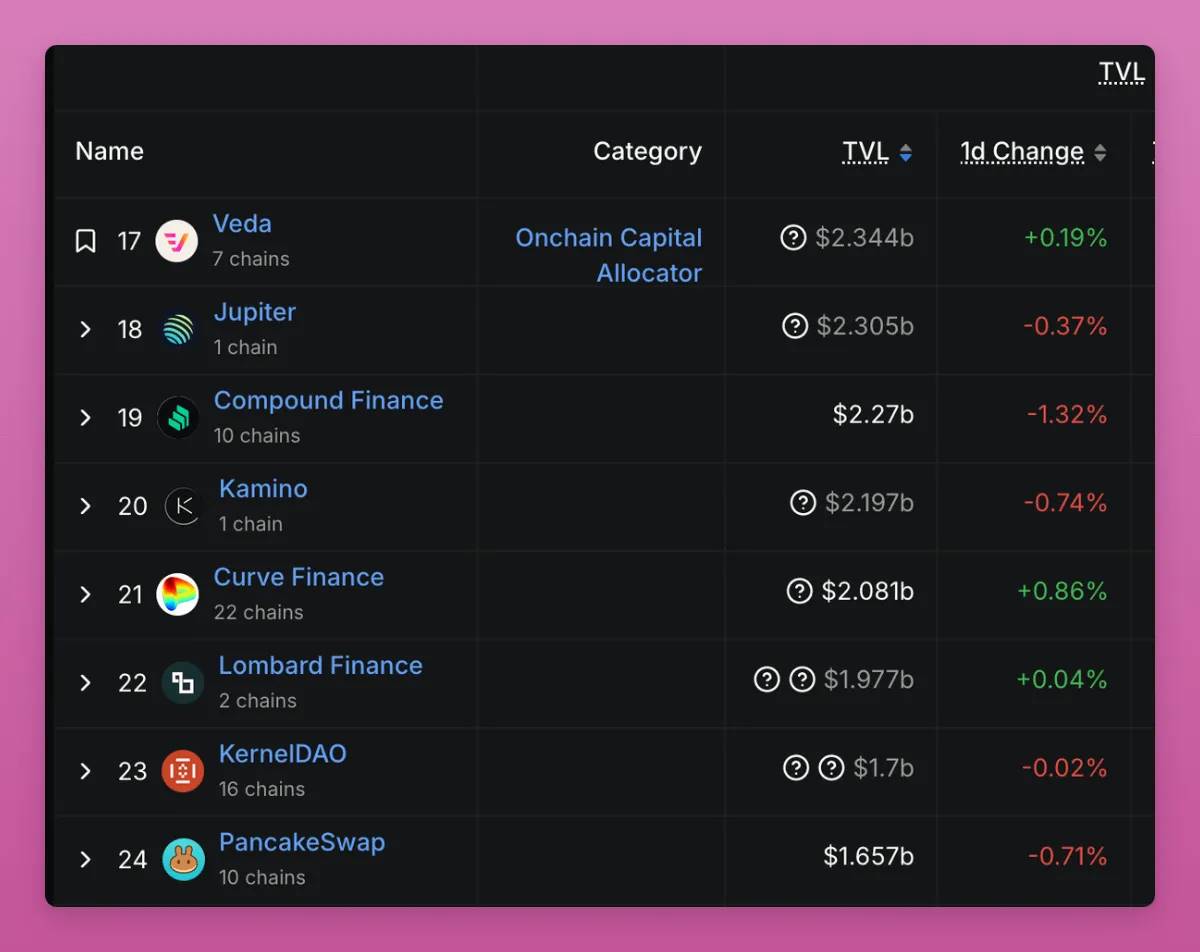

Some examples include strategy teams like MEV Capital, Seven Seas, Gauntlet, and Veda, which work with protocols like Etherfi, Upshift, and Mellow Protocol.

Veda alone has become the 17th largest “protocol” in DeFi, surpassing even Curve, Pancakeswap, or Compound Finance.

However, vaults are just the tip of the iceberg. The true vision of decentralization in DeFi has long been dead, and it has evolved into Onchain Finance.

Think about it: the fastest growing sectors in DeFi and crypto are real world assets (RWA), interest-earning assets, and risk-free arbitrage stablecoins like Ethena and Blackrock’s BUIDL, completely deviating from the original vision of DeFi.

Or projects like BTCfi (and Bitcoin L2) that rely on multi-sig wallets where you have to trust the custodian not to run away.

Note: Not targeting Lombard, just using this as an example of the confluence of trends in Vault and BTCfi.

This trend has been underway since Maker transitioned from decentralized DAI to an interest-bearing RWA protocol. Truly decentralized protocols are few and far between today (Liquity is one example).

This isn’t necessarily a bad thing, though: RWAs and tokenization allow us to move beyond the era of DeFi Ponzi schemes based on loops and leverage.

But it also means that the risk factors are expanding, making it more complicated to truly understand where your funds are. I would not be surprised to see CeDeFi protocols misusing user funds.

Remember: hidden levers will always find a way to penetrate the system.

The DAO — A Joke?

Similarly, the decentralization illusion of decentralized autonomous organizations (DAOs) is also being shattered.

Past theories were based on the “ Progressive Decentralization” theory proposed by a16z in January 2020.

The theory holds that:

The protocol first finds product-market fit (PMF) → As the network effect grows, the community gains more power → the team "hands over the baton" to the community, achieving full decentralization.

However, 5 years later, I think we are returning to centralization. Take the Ethereum Foundation as an example, it is getting more actively involved to expand L1.

I have mentioned in my previous blog " Market Fear State and Future Outlook #6 " that the DAO model faces many problems:

Voting apathy

Increased risk of lobbying (vote buying)

Execution Paralysis

Arbitrum and Lido’s DAOs are moving toward higher centralization (either through more active team participation or the BORG mechanism), but Uniswap has seen significant upheaval.

The Uniswap Foundation voted to allocate $165 million for liquidity mining rewards to drive the development of Uniswap v4 and Unichain. Another conspiracy theory is that this money is to meet the liquidity threshold of the Optimism OP funding program .

Regardless, the DAO delegates are furious. Why is the foundation paying out all $UNI rewards while Uniswap Labs (a centralized entity) makes millions in Uniswap front-end fees?

Recently, a top 20 representative resigned from his position as a Uniswap representative.

The following are the author’s core points:

Governance Illusion: Formalized Governance of DAO Uniswap’s DAO appears to be open, but in fact it marginalizes different voices. Although the proposal follows the process (discussion, voting, forum), these processes seem to have been “predetermined” long ago, simplifying governance to a “ritual”.

Concentration of Power: The Operations of the Uniswap Foundation The Uniswap Foundation further consolidates power by rewarding loyalty, suppressing criticism, and focusing on superficial image rather than accountability.

Failure of decentralization If DAOs focus more on branding than actual governance, they may become irrelevant. A DAO lacking real accountability is more like a “dictatorship with a few extra steps.”

Ironically, as the main coin holder of Uniswap, a16z has failed to promote the progressive decentralization of Uniswap.

It could be said that DAO was just a smokescreen to avoid regulatory scrutiny that centralized crypto companies might face.

Therefore, tokens that are simply used as voting tools are no longer worth investing in. Real revenue sharing and actual utility are the key.

Goodbye DAOs, welcome LMAOs — Lobbied, Mismanaged, Autocratic Oligopolies .

DEX's Challenge to CEX: The Rise of Hyperliquid

Here's one of my conspiracy theories:

FTX launched Sushiswap because they were concerned that Uniswap could threaten their spot market position. Even if FTX did not directly launch Sushiswap, it may have provided close support in terms of development and funding.

Similarly, the Binance team (or the BNB ecosystem) launched PancakeSwap for the same reason.

Uniswap poses a significant threat to centralized exchanges (CEXs), but it does not challenge CEXs’ more profitable perpetual contract trading business.

How profitable are perpetual contracts? It’s hard to know exactly, but you can get a glimpse from the reviews.

Hyperliquid poses a different threat. It not only targets the perpetual contract market, but also attempts to enter the spot market while building its own smart contract platform.

Currently, Hyperliquid’s share of the perpetual contract market has grown to 12.5%.

It is shocking that Binance and OKX actually launched a blatant attack on Hyperliquid with JELLYJELLY. Although Hyperliquid survived, HYPE investors must now take the risk of possible future attacks more seriously.

This attack may no longer be a similar means, but from regulatory pressure. Especially when CZ (CZ) gradually becomes a "national strategic encryption consultant", who knows what he will tell politicians? Maybe: "Oh, these perpetual exchanges that don't do KYC are really bad."

Regardless, I hope Hyperliquid can challenge CEX’s spot market business, provide a more transparent asset listing process, and avoid high costs that drag down the protocol’s finances.

I have a lot to say about HYPE as it is one of my most held Altcoin.

But what is certain is that Hyperliquid has become part of a movement to challenge CEXs, especially after the Binance/OKX attack.

Protocols Evolved into Platforms

If you follow me on Twitter, you may have seen my posts recommending Fluid in the context of the evolution of protocols into platforms.

The core idea is that protocols are at risk of becoming commoditized, while user-facing applications reap the majority of the benefits.

Has Ethereum fallen into the commoditization trap?

To avoid this trap, protocols need to become like the Apple Store, allowing third-party developers to build on top of them so that value remains within the ecosystem.

Uniswap v4 and Fluid attempt to do this with Hooks, while teams like 1inch and Jupiter have developed their own mobile wallets. LayerZero also just announced vApps.

I believe this trend will accelerate. Projects that can capture liquidity, attract users, and monetize traffic while rewarding token holders will be the big winners.

Crypto Industry and the Transformation of the New World Order

I wanted to discuss more about the areas of major change in the crypto industry, from stablecoins to the loss of Crypto Twitter (CT), because the crypto industry is becoming more complex.

Crypto Twitter is providing less and less “Alpha” (exclusive information) these days because the industry is no longer a closed circle.

In the past, we could launch a “Ponzi scheme” with simple rules of the game, and regulators either misunderstood crypto or ignored it, thinking it would go away on its own.

But as time goes by, regulatory discussions become more common in CT. Fortunately, the US is becoming more supportive of the crypto industry, and the rise of stablecoins, tokenization, and Bitcoin as a store of value makes us feel like we are on the verge of mass adoption.

But that could change quickly: the U.S. government may finally realize that Bitcoin is indeed undermining the dollar.

The regulatory and cultural environment outside the United States is very different.

The EU has become increasingly concerned with control, especially in its transformation from a welfare state to a war state, and many controversial decisions have been pushed forward in the name of “security”.

Rather than prioritizing the crypto industry, the EU sees it as a threat:

“EU plans to ban anonymous crypto accounts and privacy coins by 2027”

“EU regulators to impose punitive capital rules on insurers holding crypto”

We need to assess the attitude towards encryption in the context of the overall political situation. The general trend is deglobalization, and countries are gradually closing their doors to entry and exit.

EU close to banning visa exemptions for "investment-for-citizenship" countries

In China, exit bans become more frequent as political control tightens

The role of crypto in the new world order and its transition remains a major unknown.

When capital controls kick in, will crypto become a tool for capital freedom, or will countries try to suppress crypto with tighter regulation?

In his “Trend Ring Model of Culture and Politics,” Vitalik explained that the crypto industry is still forming its own norms and has not yet solidified like banking or intellectual property laws.

The 1990s internet took a “let it grow” attitude with few rules and restrictions. In the 2000s and 2010s, the attitude of social media became “this is dangerous, must be controlled!” And in the 2020s, encryption and artificial intelligence are still struggling fiercely between openness and regulation.

The government was behind the times, but now they are catching up.

I hope they choose to embrace openness, but the global trend toward closed borders deeply concerns me.