Written by: Zuo Ye

Crypto is doing payments, Fintech is creating stablecoins.

Over the past year, the crypto industry's development has been a two-way journey with traditional financial enterprises, Web 2.0 giants, and global politicians. Trump's air coin marked the end of crypto liquidity, but reconciliation has just begun.

Advisors from Pakistan, crypto mining sites in Bhutan, and sky-high financing in the Middle East ultimately became the final straws that crushed retail investors - they might as well go make a wish in the wishing pool, perhaps still clinging to a glimmer of hope.

The Era of Crypto Stagnation

Humans are strange creatures. When things were traditional, they pursued freedom; now that things are free, they pursue tradition.

Humans' only learned lesson is that they learn no lessons.

I still remember when the Bitcoin Spot ETF passed, everyone thought Bitcoin would change the world. Now, everyone believes Bitcoin is just a mapping asset of M2, unable to effectively hedge against inflation, and after being stripped away by ETF, it can no longer serve as a catalyst for the crypto bull market, becoming a dead-end street.

Humans' only learned lesson is that they learn no lessons +1.

When Trump arrived with his air coin in the loyal crypto space, the silence after the surge was not surprising. PumpFun's self-rescue, Binance Wallet's offensive, or whether Boop is truly a Binance CXO all became a farce, and not even a profitable one.

Image description: Current crypto landscape, image source: @zuoyeweb3

There's nothing new under the sun; crypto has only stagnation.

First, Ethereum, the "human civilization-level innovation", couldn't withstand the drop from 4000 to 1500, and needs to rely on Risc-V to return to the L1 battle. If EVM can be transformed, why not directly change PoS to PoW? Can Ethereum's bet on L1 and adding Risc-V truly save itself?

Being commanded by enemies is the most foolish behavior. Unfortunately, Solana is the commander this time. Solana's L1 bet was before and after FTX.

Essentially, SVM L2 or expansion layers are a parasitic behavior on Solana, like remoras on a whale - not intentionally, but present. Meanwhile, ETH L2 is like barnacles on Ethereum, brought by Ethereum itself.

The market paradigm we were once familiar with is gone forever. ETH is not Money, Stablecoin is Money.

Moreover, ineffective information is infecting the entire market. KOL Summer will quickly transform into KOL Agency Summer, then CEX Summer. Just look at the Dubai music festival's grand scene - project parties, KOLs, and exchanges are ultimately trade-oriented. Exchanges are inherently transaction acceptance points, an unsolvable situation.

This is not a criticism of KOLs, but an acknowledgment of market rules. From early 3 AM community AMAs, community-based Bihu, to the past media wars, KOLs' peak of popularity is also their endpoint. Guiding trades is the moment of trust and influence clearance.

However, this cycle also shows new differentiation trends, though still involving ineffective information, generally divided into two categories:

1. Garbage shilling, downstream markets

2. Old money endorsement, proclaiming existence

Next, the breakdown and persistence of VCs. Relying on US dollar capital, Silicon Valley, Middle Eastern, and European VCs are all planning the next stage. Lonely Chinese VCs, continuously beaten by LPs and ROI, have nothing to do with innovation anymore. They're rapidly becoming market makers - since everything leads to trading, why not save steps and do it themselves?

True innovation was previously in Huaqing Jiayuan, and will be in Shenzhen Tech Park in the future. Chinese Founders must seek funding in Silicon Valley and Wall Street, but projects truly meeting the market's next stage won't be recognized by investors within existing frameworks.

The crypto space doesn't need FA. Meme cannot be shorted.

The reason is simple: trading paths are too short. Exchanges are eyeing any traffic, willing to cast a wide net to not miss opportunities. The only beneficiaries become former big factory 'ers who escaped to CEX, where not just ByteDance is moving, but also the feeding troughs of wage slaves.

In 2018, ByteDance's average employee tenure was 4 months. By 2024, it's risen to 7-8 months, but more people are still being transferred to society, with crypto big factories only valuing top CEXs.

Today's bold statement: VC beneficiaries are top university graduates, CEX beneficiaries are big factory rejects. They bring not just professionalism and impressive resumes, but deeper hierarchical operating standards and decreased capital efficiency due to increased intermediary costs.

That vibrant crypto era, where everything competed and people only wanted to make money, is gone forever.

Continuous institutionalization has become crypto's shackle. The crypto space is more like the internet, and the internet is more like XXX.

Invention is the Mother of Demand

I'm not FUDing crypto. More accurately, my attitude is "confident in the crypto industry, worried about my own future". This is no longer a niche industry with get-rich-quick opportunities. Practitioners are being massively replaced by internet and finance industries. Crypto OGs and ground pushers will either go to jail, become subordinates, or become big shot subordinates after jail. Baby's hunting tigers tonight.

Too much complaining prevents digestion. We shouldn't continue discussing VCs and exchanges. Either restart like Ethereum or explore new ecosystems. In every crypto crisis, new asset issuance methods are born - like ERC-20 supporting DeFi, NFT supporting BAYC, now entering the stablecoin stage.

Note that the previous on-chain activity's core was Ethereum and lending, "Lego-style" capital efficiency amplification. This round's Ethereum and staking model hasn't replicated miracles. In our timeline, Tencent didn't invent WeChat; Xiaomi's Mi Chat rose instead.

Yield-Bearing Stablecoins (YBS) become a new invention. They'll create new demands - not because stablecoin needs aren't satisfied (USDT is doing fine), but because YBS can be done this way. Ethena was invented. Reference: US seigniorage ending, stablecoin super cycle.

YBS will become a new asset issuance form. Based on mental history, I have three future predictions pointing to different outcomes:

YBS becomes a new asset issuance method, Ethereum successfully "changes chips". ETH replaces BTC as the new crypto engine, Restaking ETH becomes true Money;

YBS becomes a new asset issuance method, Ethereum falls into obscurity. YBS will be consumed by government bonds and US dollar assets, Fintech 2.0 becomes reality, Web 3.0 becomes a pipe dream;

YBS doesn't become a new asset issuance method, Ethereum dies silently. Then blockchain will "remove coins and keep chains". Fintech 1.0 was PayPal replacing banks, Stripe was electronic acquiring innovation. Coinless blockchain would be at most Fintech 1.5.

To summarize, Fintech 2.0 is financial blockchain, Fintech 1.5 is coinless blockchain technology.

Stablecoins are becoming a new asset issuance mode - something no VC report ever predicted, not even Ethena itself. If we believe the market is the optimal solution, VCs and exchanges' biggest problem isn't learning Vitalik's technical narrative, but not respecting market rules.

In the current crypto landscape, exchanges, stablecoins, and public chains are essentially the big three. Binance, USDT, and Ethereum form the main cast, with others being suppliers and distribution channels. Exchanges and public chains are relatively stable; the battlefield is now concentrated on stablecoins. Not only are USDC and BlackRock advancing, but the on-chain answer is YBS - a matter of global significance, unavoidable responsibility.

PS, Exchange stability refers to Binance's dominance, public chain stability means Ethereum's revival. Solana's replacement is still in progress.

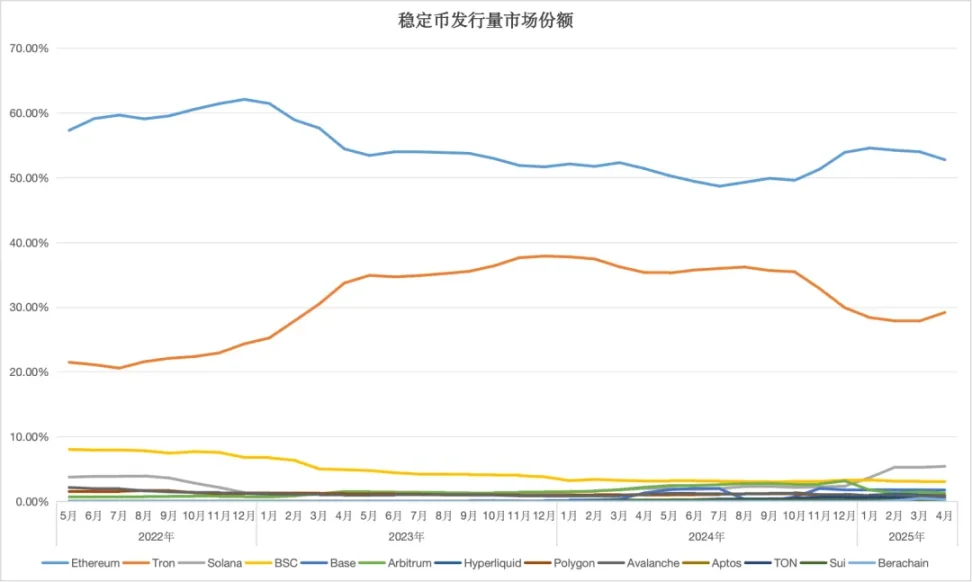

Image description: Stablecoin market issuance volume, image source: @zuoyeweb3

In the current market landscape, Ethereum and TRON dominate, but Solana has not given up on catching up. Especially since Ethereum has not been completely defeated, there are always reports of Solana DEX trading volume surpassing the Ethereum ecosystem. However, in terms of real asset issuance, ETH+ERC-20 USDT still firmly holds the top position.

This is the main reason why I believe Ethereum's fundamentals are not problematic. People's price expectations for ETH are $10,000, while for SOL it's $1,000, with completely different base points.

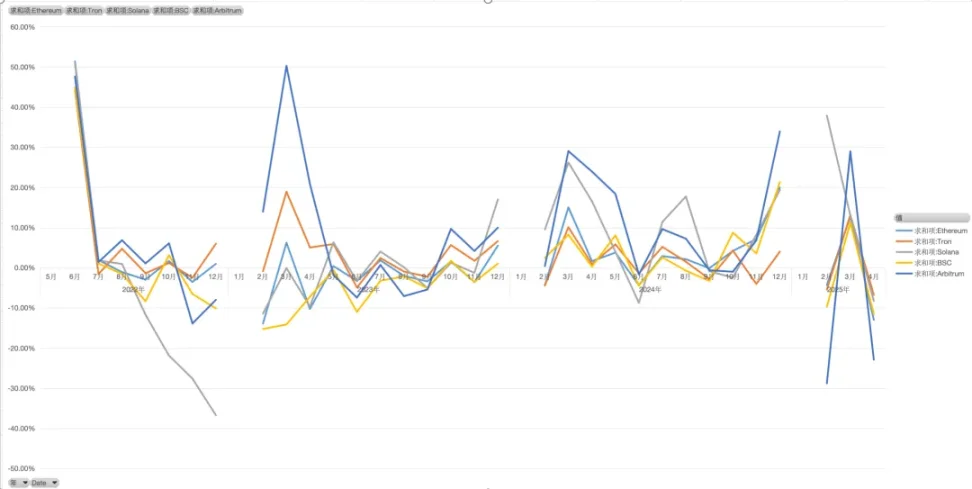

Image description: Stablecoin growth rate, image source: @zuoyeweb3

Especially when comparing the growth rates of different chains, we can find they are basically synchronized. Except for Solana being close to death in 2022, the rest of the time they remain consistent with Ethereum. We can conclude that in terms of correlation, stablecoins across different chains have not developed an independent trend and are still an overflow from Ethereum.

Accordingly, this demonstrates the importance of Ethereum and stablecoin pairing. The significance of YBS lies in anchoring, with a $230 billion stablecoin market cap, USDe and other YBS are still just "others".

As I've said before, YBS must become a new asset issuance method to transmit ETH's asset attributes to the monetary level. Otherwise, the spring of RWA will be the crypto winter.

Conclusion

Ethereum only has a technological narrative, and users only embrace stablecoins.

We hope users will embrace YBS, not USDT. This is the current situation and our divergence from the market.

Pursuing niche interests is very mainstream. Look at the through-type taillights and the globally spread LABUBU. Briefly mentioning blockchain payment, payment is not a problem, but before YBS, backed by crypto native assets, becomes mainstream, forcefully pushing blockchain payment is "result before cause" - payment should be the direction of YBS.

Cryptocurrency should not become Fintech 2.0; the path cannot become narrower.