Written by: Hashkey Capital

1. Market Overview

1.1 Cryptocurrency Market Fundamentals

Since the first half of 2024, the cryptocurrency market has experienced significant growth, with its total market capitalization soaring from $2.31 trillion to $3.33 trillion, a 44.2% increase. This growth was supported by several key milestones, including the approval of a spot Bitcoin ETF in the first half of 2024, and Donald Trump's overwhelming victory in the second half of the year - his deregulatory and pro-crypto policies injected optimism into the industry. Bitcoin's dominance also rose accordingly, from 53.4% to 56.8%, mainly due to the doubling of Bitcoin ETF assets under management, reflecting the growing interest of institutional investors.

Despite the launch of the Ethereum ETF in the second half of 2024, its performance has been relatively lackluster compared to the Bitcoin ETF. Institutional investors' preference for Bitcoin remains evident, as evidenced by the declining ETH/BTC ratio.

Solana also performed well, with its SOL price rising 29.3% since the first half of 2024. In addition to the price increase, Solana's ecosystem saw a net inflow of $2 billion in 2024.

In 2024, DeFi's market share further expanded, with the total locked value (TVL) more than doubling since the beginning of the year. Thanks to deeper liquidity and the established brand effect of decentralized exchanges on platforms such as Solana and Base, the trading volume ratio of DEX/CEX increased from 9.37% at the beginning of the year to 11.05% at the end of the year, and the overall trading volume increased significantly, with an annualized trading volume of US$2.67 trillion. The more simplified listing process has also encouraged more projects to turn to a DEX-based strategy, thereby supporting a more diverse range of long-tail asset transactions. It is worth noting that Solana and Base's DeFi TVL market share in 2024 more than doubled to 7.17% and 3%, respectively.

As the "killer application" in the crypto space, the adoption of stablecoins has also accelerated significantly, with its market value increasing by 26.8% from 1H 2024 to a record high of over $205 billion, and new entrants such as Ethena have further boosted this trend with their competitive yields. Looking ahead, the potential approval of ETFs for other institutional preferred assets such as XRP and SOL will bring positive catalysts to the market.

1.2 Macro Environment and Politics

politics

The political situation in the United States has changed. In the November 2024 election, Trump defeated Harris and was re-elected president. At the same time, the Republican Party won the majority of seats in both the upper and lower houses. This time, the Trump regime will have greater voice and execution power. Trump's America First and isolationist policies will also bring great uncertainty to the international situation, which may make countries follow the example of the United States and start trade protection and economic trade regionalization. During the campaign, Trump's policy on the cryptocurrency market was very friendly. He declared that he would allow self-hosted wallets, vigorously develop US dollar stablecoins, select crypto-friendly economic politicians, and consider setting BTC as a US treasury reserve asset. Whether he can truly promote the development of the crypto market still requires his actual policies after taking office.

Europe is mainly affected by the Russian-Ukrainian war. The war seems to be in a tug-of-war. The war may continue for a long time, leading to rising energy prices in Europe. At the same time, the Russian-Ukrainian war has also increased military spending in European countries. In terms of the power of political parties in various countries, the right-wing parties have significantly strengthened their voice. In the Netherlands, the far-right Liberal Party has become the largest party in the House of Commons; in Germany, the Choice Party ranked second in the European Parliament elections, surpassing the ruling Social Democratic Party. In addition, right-wing parties in Italy, Finland, the Czech Republic, Slovakia and other countries have also played an important role in the government. Under the influence of the United States, restricting illegal immigration and economic isolation are also major issues in European countries. Europe's policies in the crypto market are more in a follow-up state. The Crypto Asset Market Regulation Act (MiCA), which was officially implemented at the end of 24, also clarified the regulatory scheme for stablecoins and cryptocurrency entities. At the same time, European countries have maintained strict scrutiny of crypto tax regulation.

Other geopolitical areas

The war in the Middle East continues. Hamas launched a large-scale terrorist attack on Israel last year. In the following year, Israel launched operations in the Gaza Strip and beheaded many Hamas senior officials. The situation entered the final stage. At the same time, Iran and Lebanon also had friction with Israel and armed conflicts broke out. The Syrian civil war led to the fall of the Assad regime. In South America, Argentina's Miller came to power and carried out a lot of reforms, removing a large number of government departments and dollarizing the currency. After taking office, he achieved certain results and reduced Argentina's overall inflation rate. Many countries and regions in South America are also advocates of Bitcoin. Argentina, Brazil, El Salvador, etc. have promoted legislation to allow crypto to be legally regulated and circulated in the country.

economy

In 2024, the global GDP growth rate will be 2.6%, and the inflation rate will be 2.5%. The overall recession during the COVID-19 period has been overcome, and the growth rate has returned to the level before the COVID-19 outbreak. After two years of interest rate hikes, the United States has finally partially controlled inflation. Starting in September 2024, the Federal Reserve cut interest rates by 25bps for three consecutive meetings. At present, inflation seems to be under control, and the economy is moving towards a stable landing. The eurozone has been more affected by geopolitical wars, which has led to high energy prices. In addition, the European Central Bank has been forced to raise interest rates in response to the high interest rates of the Federal Reserve, which has also led to slow economic growth. China and emerging market countries have maintained a relatively high growth rate, but both face considerable challenges. Due to sluggish domestic consumption and boycotted exports, China is in a state of deflation, facing problems such as high unemployment and business difficulties. At the same time, with the bursting of the real estate bubble, there are a large number of related debts and bad debt risks. Emerging market countries have been affected by the US dollar interest rate hike, resulting in a serious depreciation of their currencies in some countries.

Source: Performance of major stock market indices in various countries in 2024

Looking at the development of the US economy in 2024, it is still in a leading position in the world. The three major US indexes have all risen sharply, among which the Nasdaq, which is dominated by technology companies, has risen by more than 28%, and the S&P500 has also risen by 15.2%. The United States has basically been fighting inflation for a long time throughout the year. Under the extremely tight capital situation, technology companies still have an amazing growth potential. AI technology companies represented by Nvidia have performed the best this year, and the development of AI has not disappointed investors' expectations. AI large models represented by ChatGPT have subverted many fields such as careers, education, and artistic creation, and have doubled the output efficiency. And with the continuous improvement of computing power, AI will also be put into practical application in more fields.

Another bright spot on the list is the Nikkei Index. As the yen remains at zero interest rate during the global interest rate hike cycle, international investors flock to the Japanese stock market for carry trading, which also drives the Japanese stock market higher and the yen depreciates. The capital's pursuit and the export trade advantages brought by the depreciation of the yen have improved the profitability of Japanese companies, which has also made the Japanese stock market finally hit a new high more than 30 years after the bubble burst.

2. Bitcoin

2.1 Product and protocol design

In the second half of 2024, there are some important software upgrades on Bitcoin, such as the flexible transaction forwarding strategy introduced in Bitcoin Core 28.0 and BOLT12 for the Lightning Network. These client upgrades may affect various application scenarios. For example, Bitcoin Core's implementation of V3 transactions now supports zero-fee transaction forwarding, which may affect the development of MEV-related business models adopted by mining pools.

Discussions about the design of the Bitcoin protocol layer are also ongoing, focusing mainly on soft fork proposals. There are disagreements among many developers, as can be seen from the OP_NEXT summit held in late 2024 and its subsequent discussions. At present, these discussions can be roughly divided into several camps: one is to add new opcodes such as OP_CTV and OP_CAT to implement restriction clauses or other more flexible functions; the other is LNHANCE, which introduces a whole set of tools to improve the Lightning Network; and some developers go a step further and promote the so-called "Great Script Restoration".

In these discussions, no consensus has been reached. Some discussions focus on whether some upgrades are too focused on specific areas and lack diversity (such as OP_CTV), while other discussions focus on whether some proposals are too flexible (such as OP_CAT), which may lead to unexpected uses such as recursive restrictions, thereby causing unforeseen risks at the protocol level. At the same time, some developers advocate that consensus cleanup should be carried out first, rather than blindly pursuing functional upgrades.

Discussions about these proposals are mainly conducted on the mailing list. There is also a feedback form in the community to collect opinions from developers of various backgrounds. In addition, there have been several studies analyzing the transactions currently active on signet related to soft fork proposals.

Source: https://en.bitcoin.it/wiki/Covenants_support

However, it is foreseeable that there will still be many heated discussions and disputes during future soft fork activations, just like the previous Taproot soft fork upgrade. By 2025, we are expected to see some form of consensus and development.

The implementation of BitVM, another much-discussed implementation, is still progressing steadily. Similar to the previous report, the current focus is still on the design and implementation of cross-chain bridges. Recently, some cross-chain bridge test versions based on BitVM have started running, such as BitLayer.

2.2 Layer 2 - Lightning Network

The number of publicly accessible Lightning Network channels has not changed much, with the total remaining at around 5,000 BTC. The number of nodes has remained basically stable, but the number of channels has continued to decrease. This may indicate that the liquidity of the Lightning Network is gradually concentrating in the hands of some large node service providers, or that some early channels have been closed due to security patch updates.

However, the Lightning Network's protocols and application ecosystem are still evolving. For example, BOLT12 (offer) has been adopted by many clients and can support static payment methods, thereby improving user experience.

In addition, some Layer 1 networks (such as Nervos CKB, etc.) are actively developing Layer 2 solutions that comply with the BOLT specification to achieve compatibility and interoperability with the Lightning Network.

In this area, the main focus is still on evaluating the feasibility of the business model. Since token issuance is usually not used as a means of fundraising or integrated into business operations, investment and financing decisions must pay more attention to the performance indicators of the project, such as the number of users and asset size.

As the payments space continues to gain traction, the Lightning Network’s ability to support payment services makes it a promising solution for widespread adoption. Service-oriented projects, especially those that leverage the Lightning Network as a settlement layer for cross-border transactions, are likely to gain more attention. Service-oriented projects that offer the Lightning Network as a settlement layer for cross-border, peer-to-peer (P2P) and business-to-business (B2B) transactions, such as Breez Technology, are expected to gain more attention and momentum. Future developments in this space depend on the issuance of stablecoins on the Lightning Network, with possible implementations including RGB and Taproot Assets mentioned below.

2.3 Layer 2 - Side Chains

The performance of Layer 2 sidechains is mixed. Some projects have declined since their peak, while others have continued to grow. As shown in the chart below, the TVL of various Layer 2 projects also shows a clear alternating trend.

Source: DeFi llama

The challenges facing Bitcoin's second layer (L2) and BTCFi are multifaceted, with a key issue being reliance on unsustainable TVL surges and airdrop incentives. While approaches to using points to incentivize TVL have been tried, the key factor remains building a robust ecosystem to ensure lasting liquidity. The primary driver for depositing Bitcoin into L2 solutions is the opportunity to gain Bitcoin-denominated, low-risk returns. However, in terms of asset composability, BTCFi can achieve better liquidity abstraction and protocol layer stacking by leveraging existing infrastructure. If Bitcoin L2 can focus on building an ecosystem around improving the utility of BTCFi, rather than simply replicating the EVM chain, there is still a lot of room for growth.

So, in summary, the keys to Bitcoin L2’s success are: 1) ensuring asset security (whether third-party custody or self-custody); and 2) pursuing a vertical integration strategy (which will better serve BTCFi).

2.4 On-chain assets

Assets on the Bitcoin chain can generally be divided into two categories: meta-protocol and CSV (client-side verification). However, in general, these assets have not shown significant appreciation with the rise in Bitcoin prices and have low activity. Altcoins on the Bitcoin chain have not generally outperformed other altcoins.

BRC20, Runes

BRC20, Runes, and other meta-protocol assets have underperformed recently. Their market cap and growth are far less than many of this year’s popular meme assets, which also confirms the short lifespan and cyclical nature of such assets in the absence of strong utility. These easily replaceable tokens are now being replaced by newer meme and AI agent narratives.

RGB

As the earliest CSV protocol, RGB is still being promoted recently. There are already some technical implementations that can support integration with the Lightning Network. The narrative of RGB is mostly about the issuance of Tether stablecoins, but the specific implementation plan is not yet clear. In terms of further programmability, it may take some time for AluVM to support more flexible development possibilities. Therefore, overall, the performance of RGB-type protocols and assets remains to be seen.

Taproot Assets

Taproot Assets was launched by Lightning Labs, the Lightning Network development team, and can realize the function of minting stablecoins at a lower cost and achieving instant settlement on Bitcoin. Tether has also announced that it will issue stablecoins based on Taproot Assets.

For the on-chain asset track, since the experience and liquidity support of DEX on the Bitcoin chain are not yet sufficient to support the demand for better performance of tokens, CEX is still important for such assets. At the same time, due to the natural support of CEX exchanges for technologies such as cold and hot wallets, it may cause certain difficulties for the integration of some new asset types. At the same time, due to the natural support of CEX exchanges for technologies such as cold and hot wallets, it may cause certain difficulties for the integration of some new asset types.

2.5 BTCFi

BTCFi can provide Bitcoin holders with additional Bitcoin-denominated returns, and as the infrastructure continues to improve, the overall locked value is expected to grow.

Source: DeFi Llama

In addition, as mentioned in the L2 section above, the types of returns pursued by BTC assets have shifted from L2 to staking, liquid staking, and liquid re-staking, which can stack multiple returns and also drive the growth of various BTCFi projects. Among them, Babylon, the cornerstone of this revenue path, has attracted a large amount of TVL denominated in Bitcoin after several stages of controlled testing, which highlights the community's urgent need to improve the practicality of BTC by leveraging Bitcoin's decentralized and proven security. As a gateway to the BTCFi ecosystem, Babylon enables Bitcoin holders to participate directly. In addition, various LST projects have also emerged to unlock liquidity and promote DeFi activities. The design of these LST projects generally draws on mature DeFi design concepts, introducing methods such as veModel and Pendle into the protocol; at the same time, the liquidity layer and the rewards extracted by each partner are uniformly abstracted. In the past six months, the composability of these protocols has become more mature. However, the recent Solv controversy, as well as questions about how BTCFi’s TVL is calculated and how the promised returns will be delivered, have cast a shadow on BTCFi’s 2025 launch.

A key focus this year has been finding ways to keep staked assets in efficient use and circulation, rather than sitting idle. Projects like Yala, as well as other lending and stablecoin initiatives, are leveraging the native infrastructure of the Bitcoin blockchain. With the market's bullish stance on BTCFi, these projects are poised for significant growth and development opportunities. However, on the other hand, with the rising cost of capital in a bull market, this also poses a significant challenge to the project's listing strategy. Protocols that can more flexibly mobilize Bitcoin liquidity and support a richer asset class will have a better chance of success.

3. Ethereum

Although the ETH ETF was launched in the United States on July 23, 2024, its performance failed to replicate the success of the Bitcoin ETF forerunner, nor did it have a positive catalytic effect on the underperforming Ethereum price. Its ETH/BTC ratio has dropped from 0.054 in January to 0.037 in December, which highlights that institutional investors are far more interested in Bitcoin than Ethereum. In addition, since the Dencun upgrade, the gas fee on Layer 2 is significantly lower than that of Ethereum, which has led to more funds flowing into Layer 2 projects such as Base, which recorded a net inflow of approximately US$3.2 billion in 2024, while Ethereum had a net outflow of nearly US$8 billion.

However, in 2025, driven by a crypto-friendly Trump administration, the Ethereum ETF had its best month of December, recording a record net inflow of about $2 billion. Meanwhile, the EVM remains the most dominant and active virtual machine in the ecosystem, prompting many developers to continue building EVM-compatible networks and applications, such as MegaETH and Monad, which are among the most anticipated launches in 2025. Given Solidity's simplicity, battle-tested security, and Ethereum's vast ecosystem, we believe Ethereum and its EVM ecosystem will continue to dominate in 2025, although competing alternatives may gradually erode its market share.

3.1 L2s

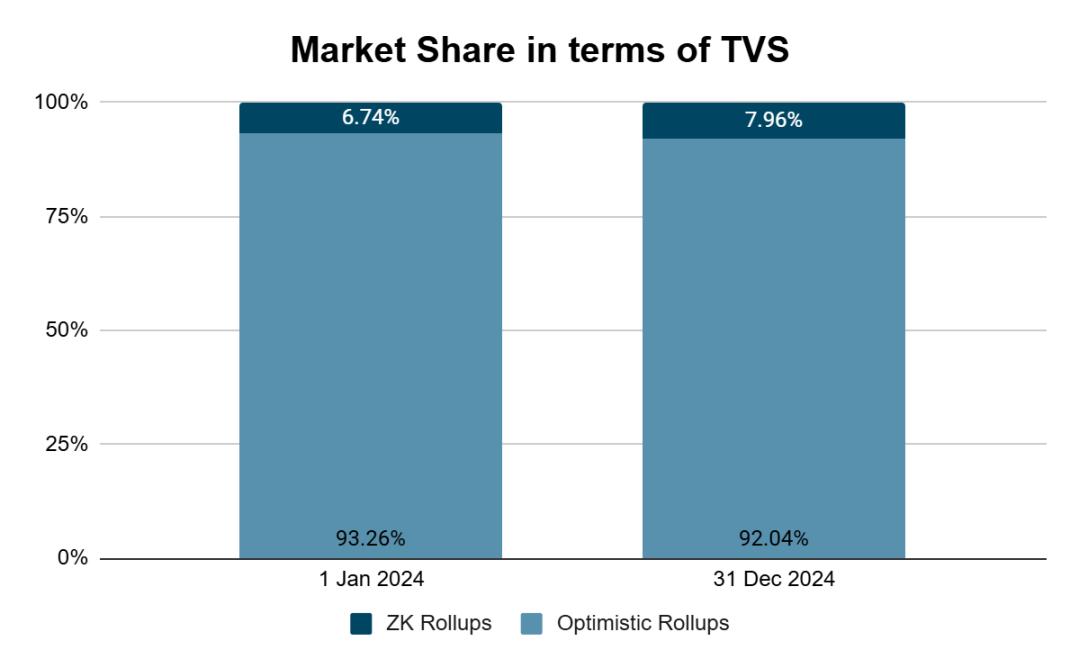

Since the Dencun upgrade that introduced blob data storage, rollups transaction fees have been reduced by more than 90%, resulting in net inflows of $3.5 billion, $2.1 billion, and $1.7 billion to leading Layer 2s such as Base, OP Mainnet, and Arbitrum, respectively. As a result, rollups usage has increased significantly in 2024: Layer 2 daily transactions increased from 5.18 million to 16.86 million, an increase of more than 325%, and the number of daily active addresses also increased from 989,000 to 2.18 million. These mainstream rollups are full of optimism, highlighting users' preference for low cost and high efficiency. In contrast, although zk rollups have a lower risk of fraud, their fees are relatively high.

Source: L2Beat, HashKey Capital

Base's significant inflow of funds can be attributed to multiple factors, including a smooth consumer experience, a strategic partnership with Coinbase, and the launch of popular consumer applications such as Farcaster and Virtuals Protocol, which have attracted a large number of users to join Base. The number of daily active users has surged from 68,324 to 1.6 million. In 2024, the DeFi activity on Base increased significantly, its stablecoin market grew from US$178 million to US$3.6 billion, and daily decentralized exchange (DEX) trading volume also soared from US$21.6 million to US$1.7 billion. In addition, Base also announced an important cooperation with Stripe. According to the cooperation, Stripe will add support for USDC on Base to its crypto payment products and add USDC to its fiat-to-crypto channel. At the same time, Coinbase Wallet will also integrate Stripe's currency listing function, enabling users to seamlessly purchase cryptocurrencies with credit cards. Looking ahead, we believe that the success of consumer applications on Base will attract more consumer-centric innovations, and developers will leverage Base’s strategic partnership with Coinbase to further expand the market.

Currently, Arbitrum, the largest rollup in terms of TVL, is also one of the main beneficiaries of the L2 shift. The launch of Arbitrum Stylus enables developers to easily write smart contracts in a variety of developer-friendly languages (such as Rust, C, C++), and this development has opened the door to more than 10 million developers worldwide. Upgrades such as ArbOS 32 and Nitro v3.2.0 further enhance network security and effectively prevent potential denial of service attacks. The future development roadmap of the protocol covers measures such as multi-client support, adaptive pricing, chain clusters, and decentralization of sorters, which will drive the network to achieve a higher degree of collaboration between Arbitrum orbit chains and create cumulative value for the Arbitrum community.

In the second half of 2024, OP Superchain continued to gain momentum, with new chains such as Unichain, Ink, and Sonieum joining the ecosystem. By the end of the year, the total number of chains based on OP-Stack reached 56, accounting for 43% of all L2/3 chains, and Superchain's transaction volume accounted for more than 56% of all L2 transactions. The number of active developers on the OP Stack chain has also surged from less than 900 to 3,446, and these data are positively reinforcing the network effect built by OP Superchain. However, most of the activity is still led by Base, which has firmly established itself as a top Superchain member. New entrants such as UniSwap's Unichain, Kraken's Ink, and Sony's Sonieum can also take advantage of their respective network effects and are expected to get a share of Base. Overall, we believe that competition between OP Stack, Arbitrum Orbit, and zkSync’s Hyperchain will intensify further in 2025, with each competing for a virtuous cycle of network effects with unique and competitive value propositions.

While the Dencun upgrade has benefited many L2 networks, with blob capacity approaching target utilization since November, the upgrade has also sparked discussion about whether it is cannibalizing Ethereum itself. With the Pectra upgrade expected to be launched in Q1 2025, which aims to increase target/max blob capacity from 3-6 to 6-9, we expect L2 networks with unique positioning and value propositions to further consolidate and improve user stickiness, becoming a serious competitor to alt-L1 networks.

Source: Dune analytics (@hildobby)

3.2 Re-staking

In 2024, the number of staked Ethereum showed an overall upward trend, reaching a peak of 34.5 million as of November 10, 2024; at the same time, the yield rate continued to decline, falling to 3% by the end of the year, highlighting the inverse relationship between the reward rate and staked Ethereum.

This phenomenon has prompted users to seek alternative yield in the form of liquid re-collateralized tokens, either through liquidity provision or lending activities. As a result, re-collateralized protocols such as Eigenlayer have attracted a large amount of TVL, although their growth momentum has weakened in the second half of 2024, with TVL falling from 5.11 million ETH to 4.44 million ETH at the end of the year. We believe this is mainly due to the delay in the launch of the slashing mechanism, which is expected to be enabled in the first quarter of 2025.

In the second half of 2024, while Karak’s performance as a re-staking platform was mediocre, Symbiotic’s total value locked (TVL) grew significantly, surging from $307 million to $2.12 billion, an increase of more than 5 times. This growth highlights the attractiveness and competitiveness of Symbiotic’s flexible re-staking mechanism, which attracts a wider and more diverse range of stakers.

As restaking solidifies its importance as a critical economic and infrastructure pillar, future catalysts will depend on the successful rollout of slashing mechanisms and the flexibility afforded to AVS, stakers, and node operators to strike the optimal balance between economic security and the yields provided.

3.3 Ethereum future roadmap and EIP proposal

2025 will be one of the most important years in Ethereum's development history as it plans to undergo a major upgrade - Pectra. This upgrade is expected to be completed in the first quarter of 2025, but it was not smooth sailing at first as clients and researchers had heated debates over multiple EIP proposals. These EIPs are extremely difficult to implement, making the original schedule challenging. However, after many rounds of discussions, the EIP version that incorporates Pectra was finally determined. If it can be executed smoothly, the Pectra upgrade is expected to be completed as planned. The following are several key EIP proposals that will have a profound impact on Ethereum's adoption and scalability:

Key EIP Proposals

EIP-7691: Expand Blobs target capacity and reduce L2 fees

The upgrade plans to increase the target blob size of Ethereum blocks from 3 to 6, further reducing L2 transaction fees. Blob fees have been close to the target cap since November 2024, and fees are likely to increase exponentially as demand exceeds the target blob capacity. Therefore, the upgrade will help control the cost of L2, making it more competitive with Alt-L1 in 2025.

EIP-7702: Implement smart contract functionality for EOA accounts

This proposal replaces the earlier EIP-3074, which aims to introduce smart contract capabilities for EOA (externally owned accounts). ERC-4337 has been slow to adopt because it requires additional adaptation from applications and protocols. EIP-7702 will greatly improve the user experience by natively integrating account abstraction in the underlying network. We are excited about the fact that it will bring better wallet UX and enhanced security mechanisms to prevent users from inadvertently signing fraudulent transactions.

EIP-7251: Optimize validator management and reduce network load

The proposal aims to ease the network load by increasing the maximum Ethereum stake limit for validators from 32 ETH to 2048 ETH to reduce the number of active validators. This will reduce the pressure on Ethereum's consensus layer and improve network efficiency.

Looking ahead, Ethereum’s core research team has reorganized Ethereum’s long-term development roadmap, aiming to conduct a major upgrade in 2029, introducing core technologies such as zero-knowledge proofs (zk proofs) and post-quantum cryptography to completely change Ethereum’s consensus layer.

Currently, due to the continued decline in L1 transaction fees, Ethereum is in a state of net inflation for most of 2024. Therefore, Ethereum needs to make adjustments to the issuance curve of staking rewards in the future, while attracting high-throughput applications to run on its platform to create greater value for holders.

Source: Glassnode

Source: Artemis.xyz

Other infrastructure

Sequencer

Since most Ethereum L2s rely on a single sequencer to run, this centralization risk raises concerns about censorship resistance and network resilience. The concept of Decentralized Shared Sequencing aims to enhance the network's resilience during periods of high traffic and redistribute value capture through a decentralized network of sequencer node operators. The importance of this concept has become more prominent as liquidity fragmentation and interoperability challenges have intensified, especially in Rollup ecosystems that run independent sequencers.

In 2024, Metis became the first Ethereum Rollup to achieve decentralization of the sorter. Currently, the main players in the decentralized sorting track include Astria, Espresso, Rome Protocol, etc. As the adoption rate of decentralized sorting increases, the field is expected to usher in greater growth in 2025. Rollup projects such as Arbitrum, Optimism, and Linea have announced plans to decentralize their sorters. Other innovative sorting designs are also being explored, such as the Solana shared sorter proposed by Rome Protocol, which utilizes Solana's localized fee market and high-performance network, and may receive greater attention.

The future success of decentralized sorting will depend on the Rollup ecosystem’s need for decentralization, including: censorship resistance, value redistribution, and enhanced network activity, while also balancing transaction latency and economic incentive alignment to effectively manage the distributed sorter network.

Data availability and modular blockchain

The data availability track is still occupied by Ethereum Blobs, Celestia, Avail, and EigenDA. As RaaS (Rollup-as-a-Service) makes Rollup deployment more seamless, the demand for data availability solutions continues to grow. Currently, 23 Rollups have adopted Celestia, of which Eclipse is its largest customer and consumes the largest amount of data availability Blobs. At the same time, EigenDA is also deeply integrated with the Rollup stack architecture by Altlayer, a leading RaaS provider. EigenDA currently has a throughput of 15MB/s and aims to reach 1GB/s in the future, but is still limited by the trust assumptions of its Data Availability Committee (DAC).

Currently, Ethereum's DA is expensive and slow, which provides an opportunity for data availability solutions to capture the market, which can solve this problem by increasing data throughput and reducing costs. In the long term, Ethereum's vision is to provide low-cost data availability solutions, starting with the Pectra upgrade and eventually implementing PeerDAS. Therefore, it will be a favorable strategy for Rollup-oriented data availability solutions to align with the Ethereum ecosystem.

Source: HashKey Capital

Intent and Chain Abstraction

Chain abstraction in the Web3 space remains an important narrative, especially as the ecosystem evolves from monolithic, isolated networks to a modular network architecture, with each layer of the technology stack being optimized for performance. However, as this innovation continues to develop, the issue of cross-chain liquidity fragmentation has resurfaced. To address this challenge, the Chain Abstraction Coalition was established last year, with more than 60 blockchains including Arbitrum, Berachain, Linea, BNB, etc. Other major players such as Particle Network and Xion have also launched Universal Accounts and Meta Accounts, respectively, promoting the popularity of chain abstraction solutions. Particle Network's UniversalX (a trading platform based on Universal Account) has been integrated with 12 EVM networks and Solana. Xion's Meta account user number has also exceeded 4 million, fully demonstrating the need and importance of chain abstraction.

One of the most significant developments in the cross-chain interoperability space in Q2 2024 was the launch of the ERC-7683 proposal. ERC-7683 aims to address pressing interoperability challenges facing blockchain networks by building a universal filler network to support a shared liquidity layer. The introduction of this standard is expected to be an important milestone in cross-chain interoperability. We believe that ERC-7683 is likely to be favored by more protocols seeking to improve user experience and gain wider adoption on their platforms.

AI Agents and Intent-Driven DeFi Transactions

In August 2024, Circle Research published a research report exploring the feasibility of using large language models (LLMs) (such as OpenAI GPT-3.5 Turbo) to perform intent-based transactions. With the continuous improvement of the reasoning ability of large language models and the maturity of AI agent technology, this field is rapidly innovating and bringing new breakthroughs to the DeFi trading experience. In the future, innovations in this direction will expand the boundaries of DeFi transactions based on AI agents and significantly improve the user experience. A case worth noting is the AI agent Griffain, which can automatically execute transactions through users' natural language requests, further lowering the user operation threshold and improving the usability of cross-chain DeFi.

4. Solana

Solana performed well in 2024, with a price increase of about 75%, mainly due to its improved competitiveness with Ethereum, and its SOL/ETH ratio increased from 0.04 to 0.06, making it one of the best blue-chip performers. Relying on its unique SVM architecture - supporting localized fee markets and parallel transaction processing - Solana provides lower fees and higher throughput. As a result, many high-performance decentralized applications choose to build on this network, and this influx of innovative applications has greatly improved Solana's fundamentals. Developments in DeFi in 2024 include the launch of cbBTC on Solana, incentive activities for PYUSD usage, and Solana's liquidity re-staking model to help improve platform liquidity. As a leading indicator of network adoption, the market value of stablecoins more than tripled in 2024 to $5.1 billion. In addition to its growing popularity among retail users, Solana has also achieved significant growth in developer adoption. According to a recent report from Electric Capital, Solana will attract more new developers than any other blockchain by 2024, surpassing Ethereum for the first time. Institutional adoption of Solana is also becoming more evident, with partnerships with Shopify and Visa further strengthening the network’s growth.

Obviously, Solana has demonstrated lasting competitiveness in multiple fields, including DeFi, NFT, DePIN, payments, consumer-facing applications, and many other fields, attracting many important projects and partners. In 2024, the focus of the Solana ecosystem will be mainly on DePIN, meme, PayFi and other fields:

DePIN

At the beginning of 2023, the top DePIN project Helium officially migrated to Solana. With the advantages of low fees and high TPS of the Solana network, it promoted the connection and management of communication equipment and became one of the world's largest IoT wireless networks. At the same time, it also left a strong user community in the Solana ecosystem. The HNT token FDV reached a maximum of $2.2 billion, completing the Solana DePIN template. Since then, another major DePIN head project Render Network has also migrated to the Solana network, also using Solana's platform advantages to provide decentralized computing and rendering services. The token FDV once exceeded $8 billion, and the network revenue increased by 3 times in 2024. In addition, with the continuous development of artificial intelligence, the capabilities of various multimodal large language models are becoming increasingly apparent. This growth, and the increasing number of applications based on these large language models, in turn, has driven greater demand for computing resources such as GPUs. As one of the most influential computing power projects in 2024, io.net's native token $IO has been highly anticipated since the launch of its primary market financing and mining incentive plan. After going online, its fully diluted valuation (FDV) has exceeded US$4.8 billion.

Based on such a strong user and community foundation, a large number of highly-anticipated DePIN projects have emerged in the Solana ecosystem in 2024, such as Hivemapper, Cudis, Grass, XNET, etc. In addition to the platform performance advantages, the popularity of these DePIN projects is also an important reason why Solana has become the preferred platform for DePIN project parties.

Meme

2024 can be regarded as the first year of Memecoin. The status of Memecoin in this cycle can even be compared to Defi in the previous cycle. It closely combines new cultural and social forms with Crypto and also imports a large number of users into the crypto industry. Because of the low threshold and frequent user transactions of Memecoin, it needs a platform like Solana with high TPS, low transaction fees and stable fees to provide users with the most friendly trading environment. At the same time, it also needs an active community to quickly gain community attention. These are the advantages that Solana has.

It is worth noting that Pump.fun, a memecoin launch platform, has achieved great success, and multiple memecoins (such as PNUT, FARTCOIN, MOODENG, and GOAT) have contributed considerable trading volume on Solana, and Solana's trading volume has largely surpassed Ethereum since the fourth quarter of 2024. Solana/Ethereum weekly DEX trading volume increased from 48.85% to 137.47%.

On the other hand, data analysis platforms are also important for early discovery of Meme investment opportunities. In addition to general platforms such as Dexscreener and Dextool, GMGN.ai, which was launched with the Meme craze, provides more direct functions, such as Pump.fun line chart service, address tracking, SmartMoney/KOL wallet tracking, etc., which better meet the needs of Memecoin investors. At the same time, a large number of TG bots have also emerged, providing users with timely transaction reminders through on-chain or community sentiment analysis, such as Solana Early Birds, Pump Alert, etc.

Solana's Memecoin has proven time and again the activity of the Solana ecosystem, and also proved the rationality of the existence of Memecoin. It is not air, but a culture and value, and a carrier of community power with much stronger liquidity than NFT.

PayFi

PayFi is a new concept proposed by Lily Liu, Chairman of the Solana Foundation. It aims to build a new financial market around the time value of money. It integrates the unique advantages of web3, such as the efficient programmability of crypto payment, the low friction and composability of defi behaviors such as trading and lending. It hopes to bring more traditional assets into web3, establish a new financial market, and make global financial payment activities more convenient and low-cost.

A big difference or advantage of the Solana ecosystem compared to other ecosystems is that it has a lot of out-of-the-box infrastructure, such as Solana Pay. The goal of Solana Pay is not just to "pay with cryptocurrency", but to create a new era of payment and commerce. Solana enables users to pay merchants with almost instant confirmation, with minimal and predictable fees. Solana Pay is available as an integrated plug-in option in Shopify-supported stores. In addition, Solana has also partnered with VISA to open offline payment channels.

Looking ahead

While Firedancer has not yet been activated, future activations and adoption will further improve the performance and security of the network, enabling it to capture more market share from Ethereum. Released in early 2024, the Solana plugin provides greater granularity, flexibility, and programmability in token issuance, which we believe will drive more institutional adoption on-chain while maintaining enterprise-grade security. The potential for Solana ETF approval, stablecoin market growth, institutional adoption, and increasing DeFi activity will all be positive catalysts for the Solana ecosystem.

Ethereum vs Solana DEX volumes

Source: Artemis.xyz

Solana Fundamentals (2024)

Source: Artemis.xyz

In the coming year, we will continue to focus on the following areas:

Solana itself: Solana has two potential benefits in 2025. One is the possible launch of the SOL ETF, and the other is the launch of the Firedancer client. These two points will be long-term benefits for Solana. Of course, there will be a huge amount of SOL unlocked in the secondary market in the short term. You can choose the right time to invest in SOL tokens.

Solana SVM and Layer 2: Solana's current TPS may not be enough to support the future ecological prosperity. In addition to the main network's own Firedancer upgrade, SVM is also an opportunity. Of course, Solana's Layer 2 not only solves the problem of network scalability, but also serves as a bridge for the Solana ecosystem, settling applications from other ecosystems on the Solana main network, bringing Solana more transaction volume and ecological activity.

application

Community-driven applications: Solana’s community is undoubtedly the most active community in the crypto industry. If Ethereum is driven by the technical community and is prone to producing new infra innovations, then Solana is driven by the user community and is prone to producing phenomenal applications. Even an application scenario like Meme, which has no practical use, has attracted the attention of countless users, and this attention is the most valuable resource for developing applications.

Out-of-the-box applications: Solana is clearly working hard to go out-of-the-box in all areas. In terms of infrastructure, it has solved payment and deposit and withdrawal problems, and has also launched the Solana phone as a carrier for applications and Payfi. In terms of users, it has already made an impact in the traditional world through meme, DePIN, etc. In terms of business, it has many traditional partners such as VISA and Shopify. If there is any ecosystem in the Crypto industry that can go out of the box the fastest, it must be Solana. The mass adoption that the currency circle pursues will also occur first in the Solana ecosystem.

5. Alt-L1s

Alt-L1s continue to gain strong traction in 2024, offering investors a different experience than Ethereum and competing on multiple fronts, such as a more active ecosystem, lower latency, higher throughput, and lower transaction fees. Here are some important and emerging Alt L1s to watch in 2025.

Berachain

Unlike traditional PoS networks, Berachain introduces a completely new consensus mechanism. Through a unique Proof of Liquidity (PoL) mechanism, Berachain rewards liquidity providers with governance tokens, thereby ensuring incentive alignment between validators, dApps, and users while maintaining decentralization. Berachain's BeaconKit modular consensus client is also EVM-compatible, enabling it to access the vast Ethereum ecosystem while providing competitive features such as Single Slot Finality and Optimistic Payload Building. Before its launch on February 6, 2025, Berachain has already gained significant attention, with its TVL (total locked value) exceeding $1.5 billion, mainly from pre-deposited vaults of its multiple partners. After the launch, with its large and enthusiastic community support, Berachain has jumped to become the eighth largest network measured by TVL, surpassing Sui and Avalanche. The future success of the network will depend on how it meets demand through innovative incentive mechanisms and applications.

TON

One of the most watched narratives in 2024 is TON, especially in Q2 and Q3. With more than 900 million Telegram monthly active users (MAU), TON attracted a lot of attention in 2024. Among them, the highly anticipated game Catizen has 4.7 million monthly active users and is one of the most popular Telegram mini-games in 2024.

Most blockchain networks face cold start problems and incentive mechanism problems, but TON has a natural competitive advantage by relying on the deep integration of Telegram, allowing a large user group to seamlessly enter the chain interaction through TON wallets (such as UXUY), TON trading robots and Telegram mini games. This advantage is verified in the data:

TON daily active users (DAU) increased from 27,725 to 293,539 in 2024

TON DeFi TVL has grown more than 10 times since the beginning of 2024, from $13.51 million to $261.7 million

However, since Q4, as market attention has begun to shift to other hot spots, TON's ecosystem and performance have not been as expected, and its underlying architecture has caused a lot of difficulties for projects such as the top DeFi protocol migration, causing TVL to decline at the end of the year. In 2025, TON's growth will rely on establishing a closer partnership with Telegram and exploring innovative channels beyond the simple click-to-earn model to attract new users and activate its ecosystem.

Kaia

Kaia is a new blockchain platform formed by the merger of Klaytn and Finschia blockchains, and will be officially launched on August 29, 2024. As a fully EVM-compatible platform, Kaia seamlessly integrates LINE and KakaoTalk, the world's two largest messaging apps, with a combined user base of over 250 million.

Kaia has solved the common cold start problem of Web3 projects, but it is also crucial to have a good user experience. To simplify the user chain, Kaia provides a series of optimization measures:

Account Abstraction Support

Gas Fee Delegation

Keyless MPC Wallets, reducing technical complexity for retail users

Since its launch, Kaia's total locked value (TVL) has grown from $37 million to $60 million, showing that user engagement and adoption of the network are on the rise. Although Kaia has gained a huge advantage by integrating LINE and KakaoTalk, its success still depends on how effectively the application acquires and retains users. To promote the ecological prosperity of various fields of Web3, Kaia and LINE NEXT jointly launched the Kaia Wave program, a $10 million incentive program, including: NEXT WEB SDK access rights, LINE NEXT's Dapp Portal integration, marketing resources, financial support, etc.

Although both have a good user base, the difference between Kaia and TON is that Kaia's user base is mainly concentrated in Japan, Taiwan, and Thailand; the GTM and ecological support strategies of both parties are also different. Therefore, at the current stage of Kaia's ecology, it is still necessary to examine the data and quality of the project itself before investing. As Kaia launches the first batch of 32 Web3 services under the Kaia Wave plan to accelerate the expansion of its mini dApp ecosystem, we remain optimistic about Kaia's future development.

Move

The Move ecosystem gained wider adoption in 2024, with the number of monthly active developers developing on the Move language growing from 1,014 to more than 1,500 by the end of 2024. Move is an open source programming language based on Rust developed by Facebook (Diem team), with advantages in security, scalability and ease of use. In the Move ecosystem, there are two blockchains that occupy the main market perception: Sui and Aptos. Both are positioned as high-performance L1, but in 2024, Sui is significantly better than Aptos in several key indicators, including FDV (fully diluted valuation), TVL (total locked value), net capital inflows, and DEX trading volume.

Source: Artemis.xyz

Source: Artemis.xyz

Sui recorded $1.2 billion in net inflows in 2024, with its native token price soaring nearly 500%. The market value of stablecoins on Sui has achieved significant growth in 2024, from less than $10 million to $370.77 million, mainly due to Sui's support for native USDC, FDUSD, and USDY. Since the launch of native USDC on Sui, its TVL has increased by more than 70%, reaching $1.6 billion by the end of 2024. As the stablecoin market size grows, DEX trading volume has also risen sharply. Cetus DEX was listed on Binance in November, driving its trading volume to grow significantly. Other DeFi protocols such as Navi, Bluefin, and Haedal have also benefited from this trend, with both TVL and trading volume rising. In the Sui ecosystem, you can continue to pay attention to crypto-native applications. Looking ahead, we believe that Sui will continue to attract capital with the increasing DeFi activity, institutional adoption of asset tokenization, and the rise of consumer applications.

Aptos also achieved significant growth in 2024. In 2024, Aptos' TVL increased from $117.81 million to $975.52 million, an increase of more than 8 times. At the same time, the market value of stablecoins on Aptos also increased by more than 12 times in 2024, from $49.27 million to $633.22 million. The number of daily active users of Aptos has increased from 88,000 to 1,100,000. But Aptos focuses more on institutional directions such as RWA tokenization, stablecoins and BTCFi. For example, leading asset management companies such as BlackRock and Franklin Templeton have deployed their tokenized funds in Aptos. After the team adjustment, whether the Aptos ecosystem will change remains to be seen in 2025.

Movement is another network worth watching besides Sui and Aptos. In Q4 2024, Movement announced the launch of the mainnet beta version of M2, its Ethereum scaling solution based on the Move language. M2 combines the advantages of MoveVM while allowing applications to take advantage of Ethereum's security and deep liquidity.

Movement Network also provides a modular toolkit that supports the deployment of Move-Rollups, and developers can freely choose: data availability solutions, cross-chain atomic settlement using M1 shared sequencer, and fast finality settlement (FFS). (Fast Finality Mechanism).

In the current narrative context where modular architecture has become the mainstream trend, whether M2 and Move-Rollups can compete with existing Rollups with their unique architecture will become a focus worthy of attention in 2025.

MegaETH

MegaETH is an EVM-compatible blockchain with up to 100,000 TPS transaction throughput, powerful computing power, and millisecond block times, enabling developers to build low-latency, high-computation applications. Despite the emergence of many new chains in the blockchain industry, existing blockchains still face significant limitations in transaction throughput and computing power. MegaETH addresses these challenges by introducing Node Specialization, and its architecture separates the roles of Sequencer, Prover, Full Node, and Replica Node to optimize overall performance. This innovative architecture enables each node type to match specialized hardware requirements, thereby improving execution efficiency while maintaining decentralization. MegaETH also focuses on real-time transaction processing and state synchronization, which is critical for high-frequency, low-latency applications. The discussion about MegaETH was very lively, detailing its innovative real-time blockchain technology, which is expected to improve Ethereum's scalability and attract high-performance applications. It will be exciting to see how MegaETH will compete with competitors such as Monad and Solana in attracting high-performance applications after its upcoming launch.

Monad

Monad is an L1 blockchain that implements Optimistic Parallel Execution across multiple EVM instances while maintaining compatibility with Ethereum bytecode. The core of this technological breakthrough is its custom consensus mechanism, MonadBFT. MonadBFT is different from HotStuff BFT in that it focuses on reducing latency, thereby increasing transaction confirmation speed. In addition, Monad integrates MonadDB, its proprietary database that natively implements the Patricia Tree Structure, optimizes data storage at the disk and memory levels, and reduces computational bottlenecks. Monad also supports asynchronous I/O, allowing the CPU to execute other transactions in parallel while processing the current transaction, thereby greatly improving throughput. This architecture enables Monad to achieve up to 10,000 transactions per second, providing 1 second block time and 1 second finality. Given the strong support provided by the Foundation through various hackathons, it is worth watching the development of Monad. The Monad Foundation continues to play an active role in the development of the ecosystem, organizing 65 builder events around the world and accelerating 46 early-stage projects through Mach and Jumpstart in 2024. We remain optimistic about the launch of Monad and the future growth of the ecosystem.

Competitive Landscape

It’s clear that the narrative for 2024 is no longer limited to the Ethereum vs. Solana battle. More and more alternative L1 projects are emerging - we believe they are expected to gain a larger market share in 2025.

L1 Competition Landscape

Source: CoinMarketCap, DeFi Llama, artemis.xyz, and respective website information, based on latest available data as of 11 Feb 2025. As Berachain recently launched, the statistics are incomplete.

6. Other tracks

6.1 Meme

In 2024, the Meme track became the best performing crypto field, with an overall increase of 218%, further highlighting the role of Meme as a barometer of the attention economy and culture-driven economy. Among them, Ethereum, Base and Solana are the three most active public chains in the Meme ecosystem. The launch of Pump.fun has become a milestone in the crypto industry. Its standardized token issuance framework completely abstracts the technical complexity of creating and issuing Meme coins, greatly releasing retail demand and significantly increasing the transaction volume of Meme coins on Solana. In addition to Pump.fun, the prosperity of Solana ecosystem Meme also benefits from the ecological support of the Solana Foundation. At the same time, Memes on Ethereum, such as Pepe and SHIB, still have highly sticky communities, while Memes in the Base ecosystem tend to be more AI-themed, which is reflected in the success of Virtuals Protocol. Similar to Pump.fun, Virtuals Protocol provides retail users with the ability to seamlessly create and issue AI Agents, further expanding the Meme narrative.

Driven by the meme coin craze, new tools continue to emerge to help retail users seize market opportunities more efficiently. For example, Kaito, an AI-driven analysis platform, provides users with deeper market insights. Photon and GMGN.AI both focus on efficient sniping and trading, taking advantage of the high volatility of the meme coin market.

Although most meme coins fail and have short lifespans, the meme track has become an important part of the industry and is expected to continue to grow. In the future, Solana and Base will maintain their leading position in this field with their established meme communities.

6.2 AI

In 2024, AI is one of the hottest fields. From the infrastructure at the beginning of the year to the explosion of agents in the second half of the year, the development of AI in crypto covers the upstream and downstream industries of AI. As shown in the figure below, Agents+applications, as the end close to the end user, conform to the rapid development rhythm of crypto industry developers. At the same time, the upstream of AI is more difficult for crypto teams due to cost requirements and development cycle. Therefore, Agents ushered in a big explosion in the second half of the year.

Ecological flow chart, source: HashKey Capital

The explosion of Agents in the second half of the year was catalyzed by the successful transformation of Virtuals Protocol in the second half of 2024, which launched several very successful Agents such as AIXBT. This is the first time that agents are positioned as an asset rather than just a tool. With the rising interest and speculation in trading AI agents, Virtuals Protocol has firmly established itself as a leader in this field.

At present, the functional categories of agents cover the following dozen categories. The ones that are popular in the crypto market are social media robots, on-chain execution, and VC agents. We expect that agents will continue to maintain a diverse ecosystem.

Agents functions and application scenarios, source: HashKey Capital

However, these agents with different functions/application scenarios have not really matured and landed, and most of them are still in the stage of telling stories. But the enthusiasm for the development framework for agents has also lasted for more than two months, indicating that this enthusiasm is not just at the level of speculative trading. Among them, ElizaOS is the framework with the highest degree of development, and it is the core framework of ai16z. Other development frameworks differ in development languages, such as the RIG framework launched by @arcdotfun, which is a Rust-based system, and ZerePY is an open source python framework based on Zerebro. There are also development frameworks that focus on coordinating resource API interface scheduling, such as FXN.

Due to the prevalence of meme culture, the combination of AI tokens (including AI Agents) and memes has also become a hot topic in the community. Although the valuations of most of these memes are between $1M and $5M, and the risk of price fluctuations is huge, it can still be found that the narrative hotspots in these memes are becoming more and more professional, such as virtual towns, anti-learning, jailbreaking, multi-agents, etc.

The huge paradigm shift brought about by AI makes us believe that this technology can be applied to multiple fields, including Crypto, so we will continue to focus on implementable Agents and the collaboration between Agents, such as multi-agents infra, tools and economy.

6.3 RWA

Since the beginning of the year, the value of the RWA market has increased by 63%, from $8.36 billion to $13.67 billion, with most of the tokenized assets mainly distributed in two major asset classes: private credit and US Treasuries. By the end of the year, there were more than 66,931 asset holders and more than 115 asset issuers, including well-known institutional issuers such as Franklin Templeton and BlackRock.

Several key events this year helped shape the RWA narrative, including the announcement of tokenization services from BNB, Tether, Hedera, Visa, etc. This year also saw the formation of the Tokenized Asset Coalition, an industry organization that aims to bring the next trillion-dollar asset to the blockchain.

We appear to be at an inflection point for RWA tokenization, and this new momentum can be attributed to the continued maturity of tokenization technology, regulatory clarity, and growing awareness of using blockchain technology to improve efficiency. In addition to private blockchains used by institutions, public blockchains are becoming an increasingly popular option. Among them, Ethereum remains the dominant public blockchain favored by asset issuers due to its battle-tested security and mature ecosystem. Other popular RWA blockchains include Plume Network, Stellar, Polygon, Solana, and Avalanche.

Private placement credit

In the Web3 RWA (real asset) space, private lending has seen significant growth, with total value locked (TVL) growing by nearly 50% to over $16 billion since the beginning of the year. Major protocols in this space include Huma Finance, Maple, Centrifuge, and Goldfinch. Maple Finance has originated over $5 billion in loans, while Centrifuge and Goldfinch have originated over $560 million and $168 million, respectively. Huma Finance, a facilitator of cross-border payment financing, has facilitated over $1.4 billion in transactions in its first year of operations. While these numbers are just the tip of the iceberg compared to the traditional private lending market, it also highlights the market demand for such platforms. However, the growth in demand for private lending does not mean that the space is immune to default risk, which is not unfamiliar to participants in decentralized private lending protocols. Therefore, prudent underwriting and collateral management, executed in a transparent manner, will help to enhance confidence in the space. Finally, implementing KYC/AML and identity solutions through privacy-preserving soul-bound tokens or zkTLS, with a keen understanding of laws in each region, may also be key to driving the next stage of growth in the industry.

U.S. Treasury Bonds

Overall, the sub-sector has seen a rapid increase in TVL since the beginning of the year, from $769 million to $3.96 billion as of December 31, 2024. In March, BlackRock, the world’s largest asset manager, launched a tokenized fund called BUIDL, backed by money market securities such as cash, T-bills, and repurcha