BTC has been trading sideways for a long time, but the silent flames of the trade war have spread to the entire world.

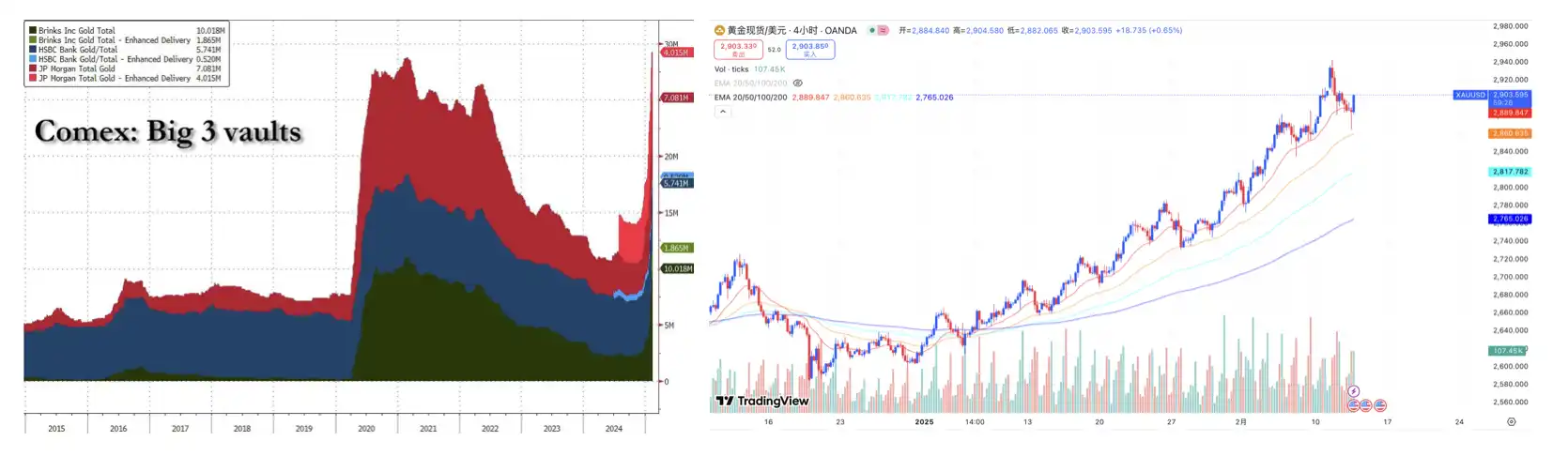

The "three major vaults" of COMEX: Brinks, HSBC, and JPMorgan Chase have seen a sharp increase in their gold holdings within a few days, reaching a new historical high, as institutional investors are frantically increasing their gold positions. During the period of BTC's high-level sideways fluctuation since January, gold has surged by more than 13%.

The Macroeconomic Historical Roles of Gold, the US Dollar, and Bitcoin

When discussing the relationship between the raging bull market in gold and its impact on BTC prices, we first need to review the historical roles of the two and the US dollar.

Gold, the natural currency, has been the darling of many, and people's faith in gold has created its supreme hedging property.

80 years ago, the United States and 44 other countries established the Bretton Woods system, of which China was also a founding member. The Bretton Woods system was a gold standard system with a fixed exchange rate, where other member countries' currencies were pegged to the US dollar, and the US dollar was pegged to gold at a rate of $35 per ounce, with each US dollar containing 0.888 grams of gold, which member governments could exchange dollars for gold at the Federal Reserve at this price.

In 1971, gold soared, the US dollar plummeted, and the US ran out of gold, unable to redeem it. President Nixon announced the closure of the gold convertibility window, the US dollar's credit collapsed, and the Bretton Woods system collapsed. This was the natural contradiction indicated by the Triffin dilemma, as the US could not simultaneously export dollars and goods to other countries, and in the 1960s, the US continued to export dollars and import goods, leading to a growing trade deficit that constantly eroded the US dollar's credit.

Since then, the gold standard has completely withdrawn from the historical stage, entering the era of fiat currency, with gold defeated by the US dollar, no longer a currency but a financial asset. The long-term bear market in gold and the long-term bull market in US dollar assets have begun since then.

When the Nasdaq bubble burst in the 21st century, the Federal Reserve aggressively cut interest rates and maintained low interest rates for a long time, continuously engaging in quantitative easing, rapidly expanding its balance sheet by purchasing medium- and long-term US Treasuries to increase the money supply, injecting liquidity into the market to stimulate investment and consumer spending, and stimulate corporate expansion.

For the US government, quantitative easing stabilized the financial markets, stimulated economic recovery, and brought incremental corporate investment and consumer spending, but for the global market, this quantitative easing-driven supply increase was undoubtedly a form of blood-sucking. The pricing of major asset classes is still primarily in US dollars, and the Federal Reserve "prints money" on its own, injecting massive liquidity into the US economy, and this liquidity does not come out of thin air but is extracted from other economies.

Many economies' important way to counter the "US dollar hegemony" that causes their own assets to be "bled and devalued" is for their central banks to purchase gold to maintain a partial anchor between their economies and gold.

It was also at the time of the Federal Reserve's first large-scale quantitative easing that BTC, "this peer-to-peer electronic payment system," emerged.

BTC has no central issuing authority and is not directly controlled by the government or financial institutions. Its total supply is strictly limited to 21 million, and the government cannot increase its supply like issuing fiat currency. In periods of monetary expansion and high inflationary pressure, BTC's scarcity theoretically gives it better value-preserving ability and can to some extent resist the erosion of assets by inflation.

Since Satoshi Nakamoto invented BTC, it should have become a hedge asset to counter monetary expansion and high inflationary pressure, a tool for all people and economies to attack the Federal Reserve's quantitative easing and maintain the stability of their own asset values as much as possible.

"When the author finished writing this book, he was already dead."

Nowadays, with factors such as Strategy's continuous bond issuance to purchase BTC and the influx of large amounts of US risk capital into BTC ETFs, BTC's hedging property has been infinitely compressed, becoming a US dollar asset strongly correlated with the US stock market.

The Recent Gold Bull Market

On February 12, another 600,000 ounces of gold were delivered to the COMEX vaults, bringing the total inventory to 36.1 million ounces, with the physical gold reserves of the "three major vaults" of JPMorgan Chase, HSBC, and Brinks already exceeding the pandemic peak and reaching a new historical high.

Over the past 20 years, the pricing logic of gold prices has been basically determined by: counterbalancing US dollar credit, capital hedging, and investment flows. When these three factors act in the same direction, gold often sees the largest gains.

Purchasing gold as a crisis hedge to some extent indicates that institutional investors' fear of the financial market is increasing, possibly due to the risk of economic recession and the uncertainty of monetary policy, and the smart money in the market is preparing in advance for a major imminent recession or hyperinflation event; on the other hand, it reflects the Trump administration's imposition of tariffs on the world and the trade war. Non-US currency markets are engaged in a strong anti-US dollar movement, with the central banks of the BRICS countries seeing a surge in demand for gold purchases, accelerating the development of a trade settlement system supported by gold.

In addition, there are also direct reasons related to UK-US import and export tariffs, with the market partially expecting that the Trump administration's imposition of global tariffs will lead to a higher tax-inclusive price for physical gold flowing from the UK to the US, and a large number of arbitrage traders are frantically moving gold from the UK to the US.

A major gold supply bank's gold trader based in Singapore said, "Gold prices are soaring, and in Asia, gold demand has almost disappeared, while in the US, there is a great opportunity, and naturally, almost every bank has to seize it - to transfer gold to the New York Commodity Exchange (COMEX) for delivery to earn arbitrage profits." A large spot-futures price spread has emerged, with US futures gold trading at a $40 premium to spot gold on February 3, Indian gold prices at a $15 discount, and Chinese prices at only a $1 discount. In this situation, gold shorts can only try to replenish gold inventories to meet potential delivery demand, and COMEX's gold inventories have started to "flywheel."

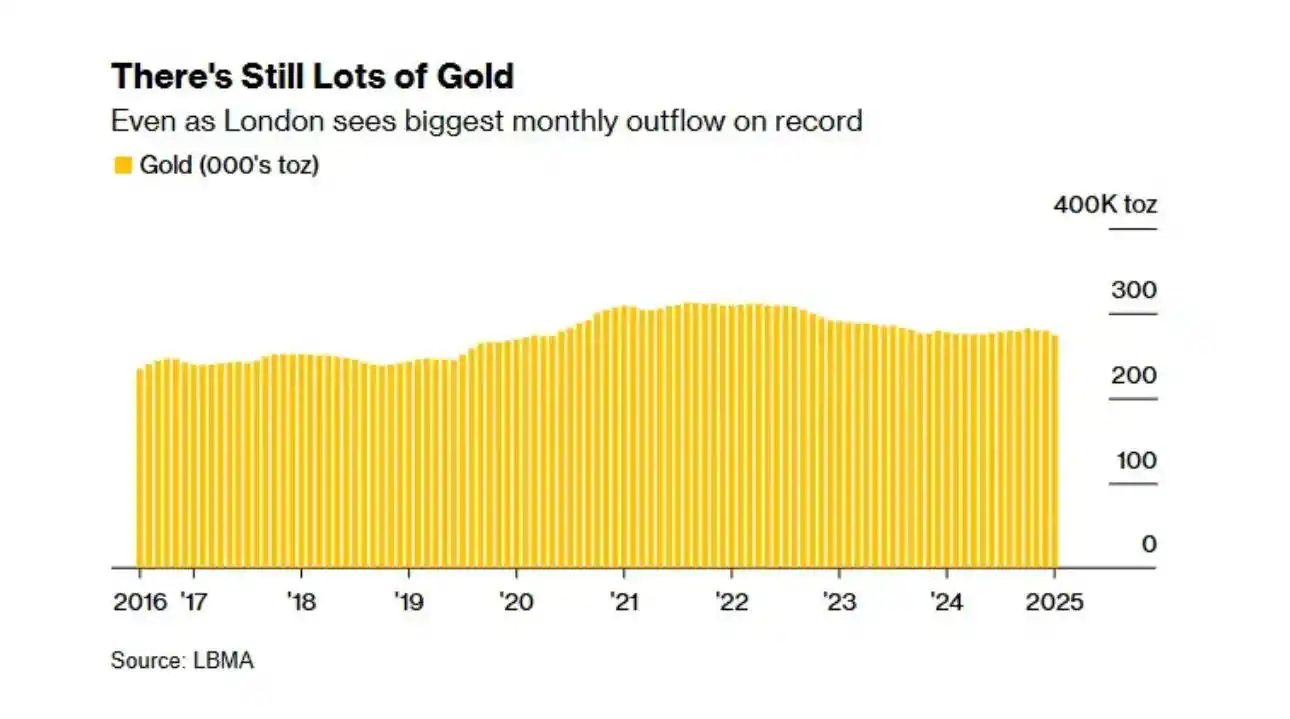

Large amounts of gold are being moved from London to New York, and according to data collected by the London Bullion Market Association, London's gold holdings decreased by 151 tons, or 1.74%, in January 2025, the largest monthly decline since 2016.

Arbitrage traders, hedge funds, and central banks around the world seem to be following their respective investment logics and taking the same action - buying gold, naturally leading to a sharp rise in gold prices. This is an independent market for gold, independent of the 10-year US Treasury yield and the US dollar index.

The Policy Swings of the Trump Administration

Let's go back and discuss the Trump administration's past governance policies and some of the current policies it is implementing.

During the previous administration, the Trump government's policies generally showed a "strong dollar" tendency, with its first Treasury Secretary explicitly stating that the US would continue to implement a "strong dollar" policy, pursue protectionism, and impose tariffs, causing the US's trading partners to lower their exchange rates to increase exports, which to some extent supported the US's fiscal expansion and the US dollar.

The current Trump administration is continuing the policies of the previous administration, adopting protectionism and tax cuts, and the "strong dollar" remains the main policy. Whether it is the US dollar index or the 10-year US bond yield, the consensus on the major trend has already been confirmed.

The uncertainty of small-scale tariffs, the Trump administration's vacillation on imposing tariffs on different countries and different categories of assets, and its verbal intervention in the exchange rate are tightening expectations of a strong US dollar. Trump sometimes expresses support for a strong US dollar and emphasizes the importance of the US dollar as the global reserve currency, and sometimes criticizes the US dollar as being too strong, believing that a strong US dollar will harm the export competitiveness of US manufacturing. The uncertainty of policy expectations may lead to a change in the major trend, or it may just be a small-scale fluctuation, continuing the major upward trend.

But this uncertainty risk has basically confirmed that gold has transitioned to a safe-haven environment, and a large number of institutional investors have increased their allocation to gold to hedge the uncertain risks of the global economic recovery.

What about BTC?

The continuous inflow of the COMEX gold vault may confirm that gold has transitioned to a safe-haven environment, with geopolitical changes, increasing debt concerns, and potential stock market instability, which may drive institutions to return to the gold market, with bond yields remaining volatile and the stock market facing increasing downside risks.

At this time, BTC, as mentioned in the previous text, should play the role of a safe-haven asset, but due to the Trump administration's crypto policies and the large number of US-listed companies holding BTC, and the increasing importance of BTC ETFs as a buying power globally, it has become a dollar asset.

Currently, gold and BTC are in a delicate relationship of opposition and unity. To some extent, their pricing logic is complementary, but there are also areas where they "suck blood" from each other. Cryptocurrencies represented by BTC are the most sensitive to liquidity, while gold is the most sensitive to risk.

From the perspective of liquidity, the Fed's rate cuts will inject a large amount of liquidity from stable bonds into the gold and Bitcoin markets; from the perspective of safe-haven, when a major crisis occurs, gold can accommodate more safe-haven capital, while BTC is more likely to fluctuate with the ups and downs of the US stock market.

Therefore, in the short term, if the macroeconomic environment does not undergo major changes, the bull market in gold may not have a significant resonance effect on BTC, and when the safe-haven sentiment subsides, it may lead to the outflow of some safe-haven assets and their inflow into the risk markets represented by BTC and US stocks.

When we observe the price index changes of BTC/GOLD, the current situation seems to have fallen below the lower bound of the range since 2025. If it cannot fully recover in the next two weeks, the cooperation between BTC's bulls and gold's shorts may fail, and the upward breakthrough may fail, which may mean in the future that market risk appetite has decreased, reducing investment in risk assets represented by BTC and increasing investment in safe-haven assets represented by gold.

When we zoom in and observe the volume and price patterns of BTC/GOLD at the daily level. Reviewing the BTC/GOLD breakthrough chart since November 6.

The volume and price pattern starting from the first arrow is the volume and price pattern of the initial breakthrough, at which time the macroeconomic environment was Trump preparing to be elected President of the United States, becoming the first "crypto president" in history. The first candle starting from the arrow has synchronized volume and price, and the upper shadow is very short, basically confirming the strong demand; the next candle has significantly reduced trading volume, a relatively short body, and weak selling pressure; the next candle continues to rise sharply, with the volume lower than the previous sharply rising candle but the body longer, indicating that the selling pressure has not yet appeared. The next two candles have short bodies and relatively long upper shadows, and are blocked after touching the dense area of the 2021 high, proving that the dense area of the 2021 high still has pressure, but has never effectively broken below the small-level previous high, and the small-level previous high has been effectively converted to support.

The volume and price pattern starting from the second arrow is the volume and price pattern of the breakthrough being blocked, at which time the macroeconomic environment was Trump's confirmation as President of the United States, and the cryptocurrency market was fermenting the crypto narrative after Trump's election as President. The trading volume of the second arrow is significantly larger than the previous one, but the body length is basically the same, and the upper shadow is longer, indicating that the selling pressure is very strong, and there was a huge supply here, and the breakthrough here requires stronger force to be effective, and the next candle has a very long lower shadow but very small trading volume, and the buying pressure here is not strong, which is more likely to be the seller's test of the buyer's strength.

The volume and price pattern starting from the third arrow is the volume and price pattern of the support rebound, at which time the macroeconomic environment was the impact of the uncertainty of tariffs. But the trading volume of this candle increased rapidly, basically confirming that the pressure of the small-level previous high has been effectively converted to support, but the next candle is pressed down by the dense area of the 2021 chips, the trading volume is reduced, but it still attacks the support level downward, indicating that the selling pressure is weak, and the buying pressure is even weaker. The subsequent continuation to the present is a narrow oscillation around the previous high.

Does this mean that in the longer term, BTC will only serve as a risk asset investment, and not as a safe-haven asset?

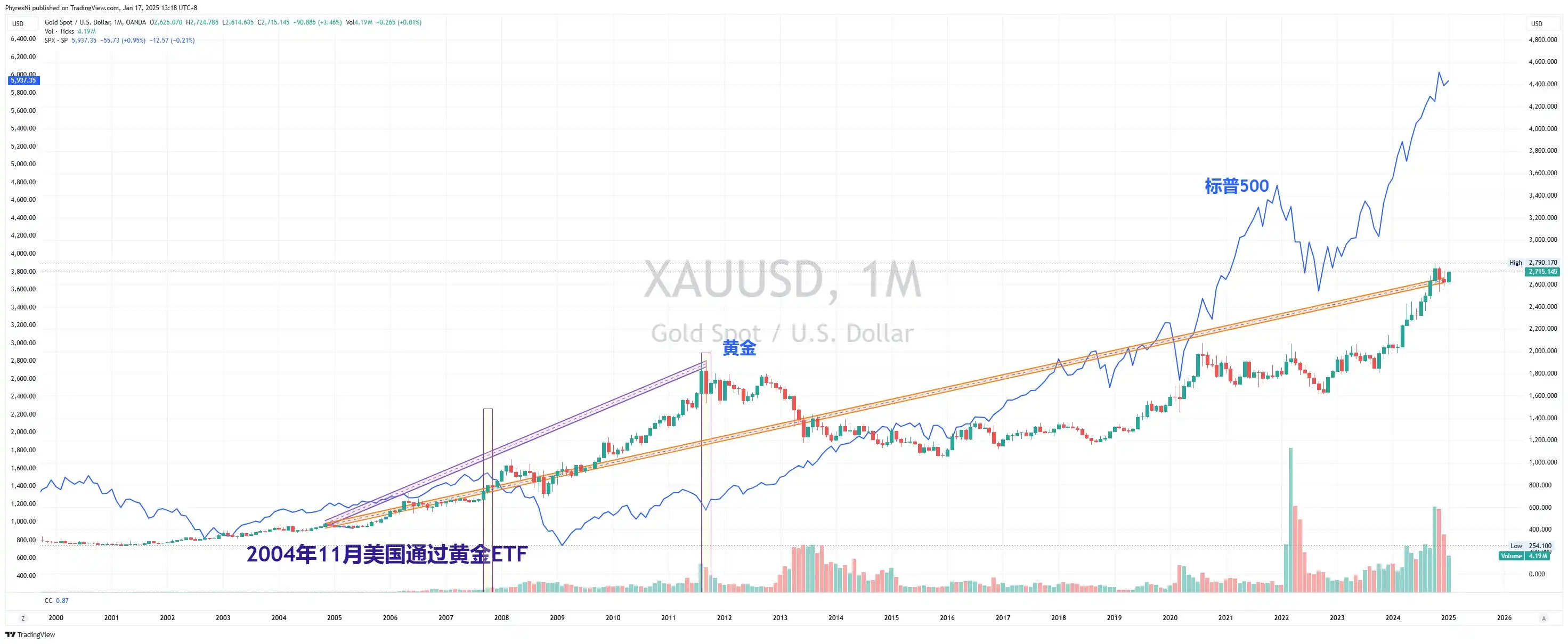

Let's look back at the analogy of the buying power brought by the gold ETF in 2004.

After the US approved the gold ETF in November 2004, gold and the S&P 500 showed a positive correlation for a period of time, but when the real crisis occurred, the price performance of gold was obviously able to withstand more pressure. The 2008 subprime crisis caused the S&P 500 to halve from its high of 1500 to less than 700 points, while gold only fluctuated in a wide range and did not form a major downward trend, and when the economy recovered, gold also regained all its losses and hit new highs. When the economy had fully recovered and all assets had emerged from the shadow of the economic crisis, gold experienced a major oscillation and consolidation.

If the passage of the BTC ETF is interpreted as more people in the market recognizing the value of BTC, after a real crisis adjustment, BTC's resistance and resilience may be redefined, and its pricing logic may also change, perhaps it will return to its initially designed position: a "digital gold" that fights inflation.

Welcome to join the official BlockBeats community:

Telegram subscription group: https://t.me/theblockbeats

Telegram discussion group: https://t.me/BlockBeats_App

Twitter official account: https://twitter.com/BlockBeatsAsia