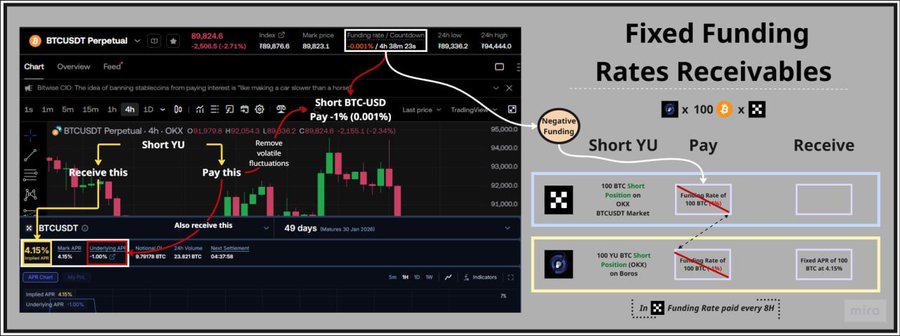

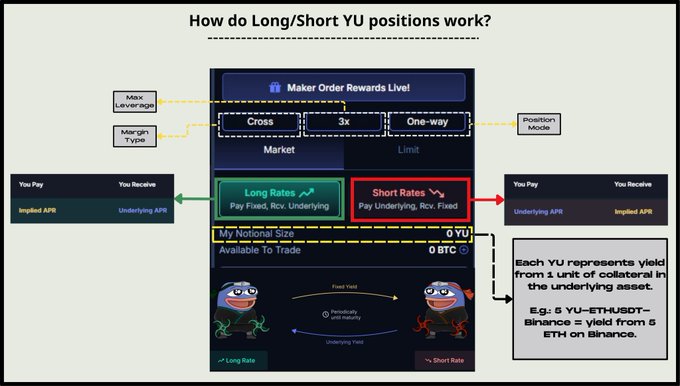

How to Boros – Fixing funding rate receivables In a positive funding environment, traders holding SHORT positions on perpetual exchanges receive funding payments at every interval. Each exchange runs on its own cycle. However, there are still times when the funding rate suddenly turns negative for a period, causing short positions to pay the funding rate, making it a real cost burden for anyone carrying short exposure. For example, a short BTCUSDT perpetual position on @okx currently paying 0.001% every 8 hours, equal to about 1% APR. But, these fluctuations can be hedged by locking in a fixed APR through @boros_fi. This method is especially useful for entities with large funding-rate exposure, such as @ethena_labs. Instead of accepting a stream of funding that can flip between positive and negative and create uncertainty in future yield, they can swap the floating funding stream into a fixed APR on Boros. To achieve this, a trader holding a short position on a perp exchange also opens a short YU position on Boros for the same market. The goal is to convert the funding they receive from the perp exchange into a predictable fixed return. Consider the example below 👇 Currently, a user is holding a 100-BTC short on OKX. The funding rate was previously positive, but it has now shifted to −0.001%. TN | PendleBoros and 9 othersEvery 8 hours, instead of receiving positive funding, he must now pay funding to Long OI. To neutralize this risk, he hedges by opening a short YU position with the corresponding size on Boros (YU-100BTC-OKX). Under this setup, every 8 hours on OKX he pays the current funding rate of −0.001% (−1% APR). However, this cost is offset by the short YU position on Boros, where he pays the same underlying APR of −1% (Pay -1% = Receilocksve 1%) and lock in a fixed APR of 4.15% through the implied APR at the time he opened the position. Still confused? Here is a quick reminder of how Long/Short YU works on Boros: TN | PendleBoros and 9 othersA short YU position has two components. 🔹The trader receives a fixed APR, equal to the implied APR at execution. 🔹The trader pays the underlying APR, which is the actual funding rate from the source exchange. For anyone hedging the funding rate they currently receive, the key variable is the implied APR at entry. If the implied APR is attractive, opening a short YU locks in that level as fixed income. The higher the implied APR, the more favorable the fixed return. A special 10% fee rebate when you hedge the funding rate by using this link: boros.pendle.finance/join/NEON...

From Twitter

Disclaimer: The content above is only the author's opinion which does not represent any position of Followin, and is not intended as, and shall not be understood or construed as, investment advice from Followin.

Like

Add to Favorites

Comments

Share

Relevant content