Author: Trend Research

Since the 1011 market crash, the entire cryptocurrency market has been sluggish, with market makers and investors suffering heavy losses. It will take time for funds and sentiment to recover.

However, the crypto market is never short of new volatility and opportunities, and we remain optimistic about the future.

Because the trend of mainstream crypto assets merging with traditional finance to form a new business model has not changed, it has instead rapidly built up its competitive advantage during periods of market downturn.

I. Strengthening of Wall Street Consensus

On December 3, Paul Atkins, Chairman of the U.S. Securities and Exchange Commission (SEC), said in an interview with FOX News at the New York Stock Exchange: "In the next few years, the entire U.S. financial market may migrate to the blockchain."

Atkins stated:

(1) The core advantage of tokenization is that if assets exist on the blockchain, the ownership structure and asset attributes will be highly transparent. However, currently listed companies often do not know who their shareholders are, where they are located, or where their shares are held.

(2) Tokenization is also expected to enable “T+0” settlement, replacing the current “T+1” transaction settlement cycle. In principle, on-chain delivery payment (DVP) / receipt payment (RVP) mechanism can reduce market risk and improve transparency, while the time difference between clearing, settlement and fund delivery is one of the sources of systemic risk.

(3) It is believed that tokenization is an inevitable trend in financial services, and mainstream banks and securities firms are already moving towards tokenization. It may not even take 10 years for the whole world to realize it...maybe in a few years. We are actively embracing new technologies to ensure that the United States maintains its leading position in areas such as cryptocurrencies.

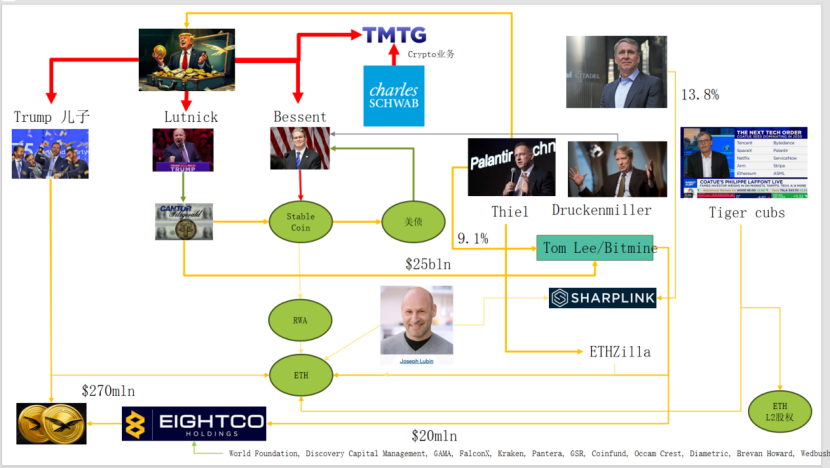

In reality, Wall Street and Washington have already built a deeply embedded capital network, forming a new narrative chain: US political and economic elites → US Treasury bonds → stablecoins/crypto treasury companies → Ethereum + RWA + L2

This diagram shows the intricate connections between the Trump family, traditional bond market makers, the Treasury, technology companies, and crypto companies, with the lines connecting the green ellipses forming the main structure:

(1) Stable Coin (USDT, USDC, WLD, and the underlying US dollar assets, etc.)

The majority of reserve assets consist of short-term U.S. Treasury bonds and bank deposits, held through brokerages like Cantor.

(2) US Treasuries (2) US Treasuries (United States Treasury Bonds)

Issuance and management are handled by the Treasury/Bessent side.

Palantir, Druckenmiller, Tiger Cubs, etc. are used as low-risk interest rate base positions.

It is also a yield asset pursued by stablecoins/treasury corporations.

(3)RWA(3)RWA

From US Treasury bonds, mortgages, and accounts receivable to housing finance

Tokenization is accomplished through the Ethereum L1/L2 protocol.

(4) ETH & ETH L2 Equity

Ethereum is the main chain that supports RWA, stablecoins, DeFi, and AI-DeFi.

L2 equity/tokens are claims on future trading volume and transaction fee cash flow.

This chain expresses:

US dollar credit → US Treasury bonds → stablecoin reserves → various crypto treasuries/RWA protocols → ultimately deposited on ETH/L2.

Looking at RWA's TVL (Total Value Leverage), compared to other public chains that experienced a drop of 1011, ETH is the only public chain that quickly recovered from the decline and rebounded. Currently, its TVL is 12.4 billion, representing 64.5% of the total crypto supply.

II. Ethereum's Exploration of Value Capture

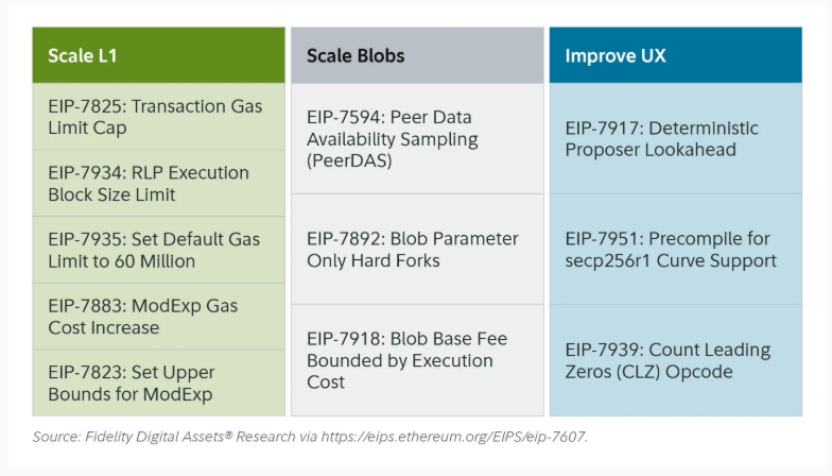

The recent Ethereum Fusaka upgrade hasn't caused much of a stir in the market, but from the perspective of network structure and economic model evolution, it's a "milestone event." Fusaka isn't just about scaling through EIPs like PeerDAS; it's an attempt to address the problem of insufficient value capture on the L1 mainnet caused by the development of L2.

Through EIP-7918, ETH introduced a "dynamic floor price" for the blob base fee, binding its lower limit to the L1 execution layer base fee, requiring blobs to pay DA fees at a unit price of at least 1/16 of the L1 base fee; this means that rollups can no longer occupy blob bandwidth at near-zero cost for extended periods, and the corresponding fees will flow back to ETH holders in the form of burning.

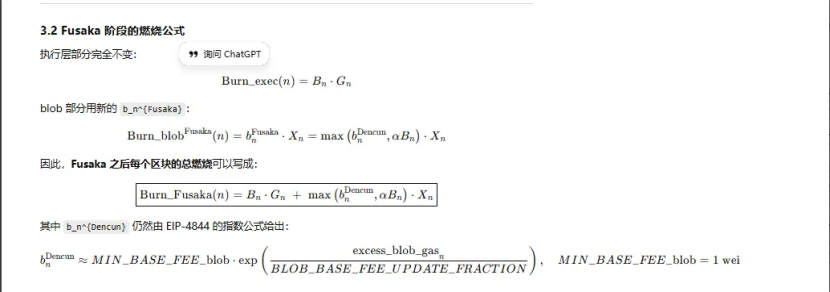

Of all Ethereum upgrades, three were related to "burning":

(1) London (single-dimensional): Only the execution layer is burned. ETH begins to experience structural burning due to L1 usage.

(2) Dencun (Dual-dimensional + blob market independence): Burning execution layer + blob, L2 data writing to blob will also burn ETH, but when demand is low, the blob part is almost 0.

(3) Fusaka (Dual-dimensional + blob bound to L1): To use L2 (blob), you must pay at least a fixed percentage of the L1 base fee and have it burned. L2 activity is more stably mapped to ETH burning.

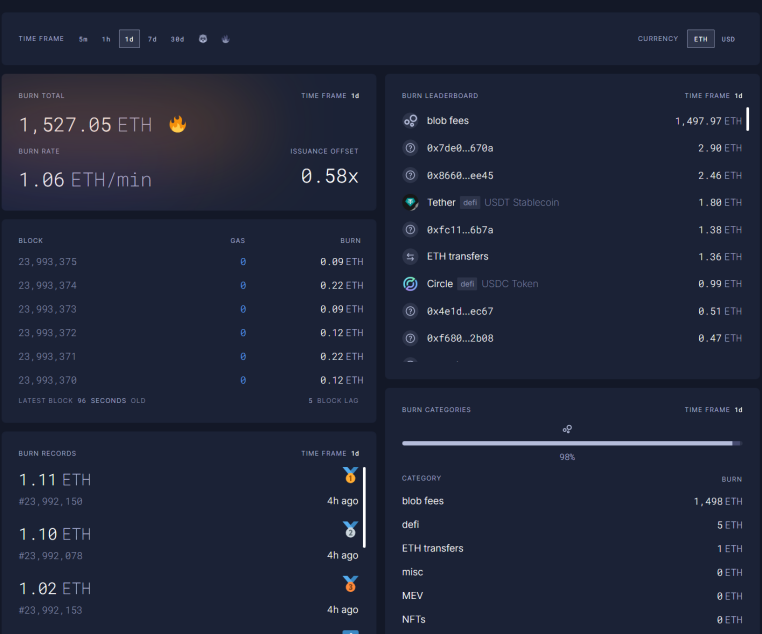

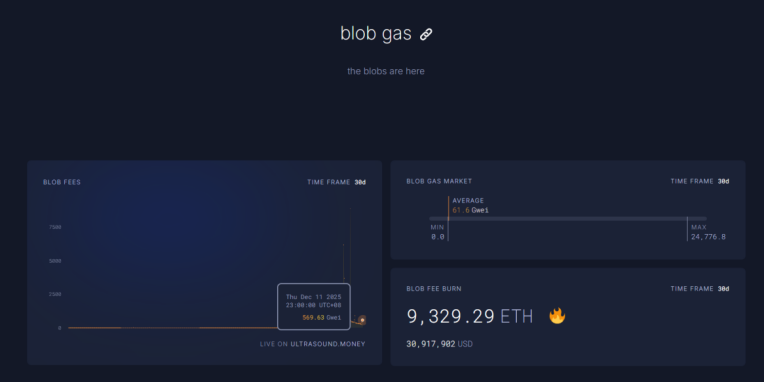

Currently, blob fees in the first hour of trading on December 11th at 23:00 have reached 569.63 billion times the amount before the Fusaka upgrade, burning 1527 ETH in one day. Blob fees have become the largest contributor to the burning, accounting for as much as 98%. As ETH L2 becomes more active, this upgrade is expected to bring ETH back to deflation.

III. Ethereum's technical indicators are strengthening.

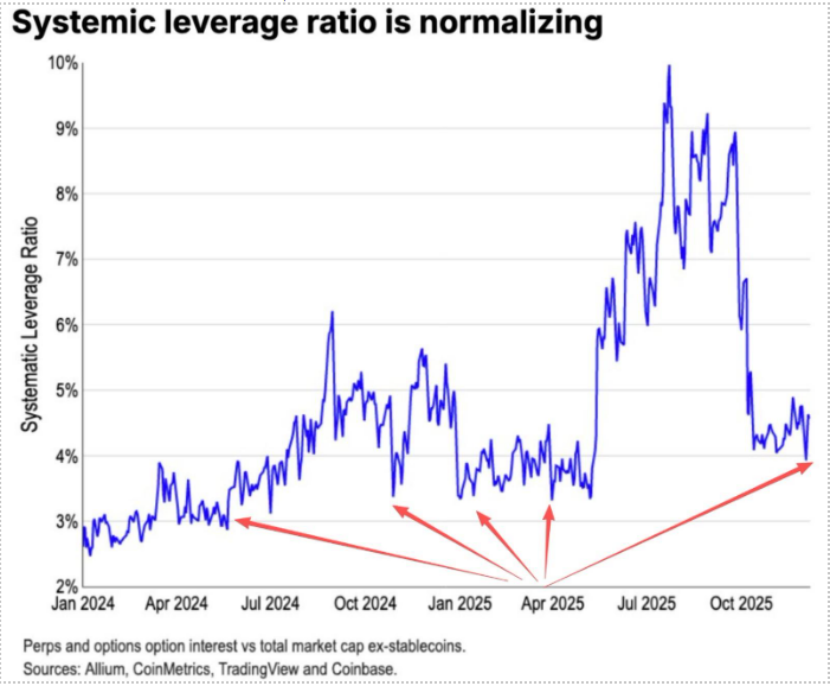

During the ETH futures margin trading crash of October 11th, the leveraged positions were largely liquidated, eventually spilling over into the spot market. Simultaneously, many long-time ETH investors, lacking faith in the cryptocurrency, reduced their holdings and exited the market. According to Coinbase data, speculative leverage in the crypto has fallen to a historically low level of 4%.

A significant portion of past ETH short positions came from the traditional Long BTC/Short ETH pair, which generally performed very well during past bear markets. However, this time things have been different. The ETH/BTC ratio has been trading sideways since November, showing signs of resistance.

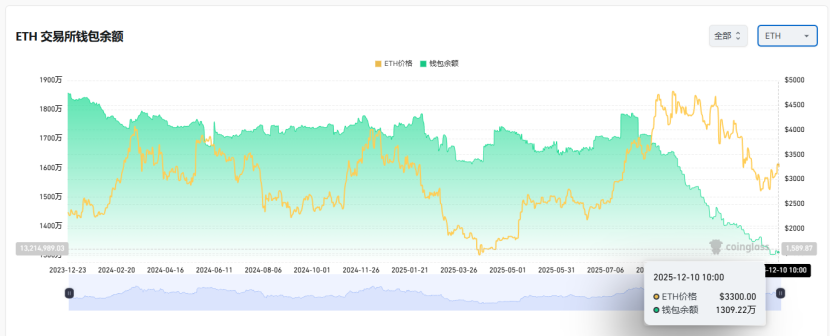

ETH currently has 13 million coins in circulation on exchanges, which is about 10% of the total supply and is at a historical low. As the Long BTC / Short ETH pair expires in November, and the market is in a state of extreme panic, a "short squeeze" opportunity may gradually emerge.

As we approach the turn of 2025–2026, both China and the US have released friendly signals regarding their future monetary and fiscal policies:

The US will be proactive in the future, cutting taxes, lowering interest rates, and relaxing crypto regulations, while China will appropriately ease monetary policy and maintain financial stability (suppressing volatility).

Amid expectations of relatively relaxed monetary policy in both China and the US, which suppresses downward volatility in assets, and with extreme panic and funds and sentiment not yet fully recovered, ETH remains in a favorable "buying zone."