The number of millionaire households is increasing, but much of their wealth is trapped in assets that are difficult to liquidate quickly.

According to an 18-month survey conducted by the now-defunct New-York Tribune in 1892, at the height of the Gilded Age, there were 4,047 millionaires in the country, with the paper listing them in a special edition.

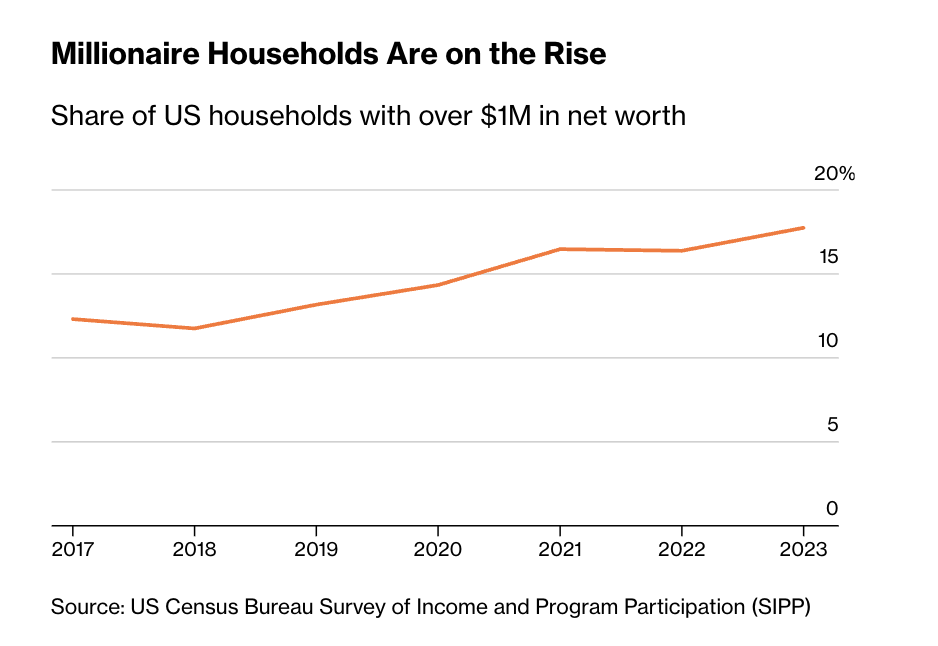

Today, the number of millionaire households in the United States has exceeded 24 million, accounting for nearly one-fifth of the total number of American households, according to a Bloomberg analysis of government survey data through 2023.

Fully one-third of modern millionaires were created since 2017, thanks to rapid growth in property values and the stock market.

Millionaire families are on the rise

Percentage of U.S. households with a net worth exceeding $1 million

Source: U.S. Census Bureau Survey of Income and Program Participation (SIPP)

That doesn't mean they have plenty of cash on hand.

In fact, a growing number of millionaires have their wealth locked up in assets that are difficult to liquidate quickly or easily, such as home equity, and a growing number of age-restricted retirement assets, such as 401(k)s and individual retirement accounts (IRAs). Add to that the impact of inflation and higher interest rates, and financial advisors say $1 million is no longer enough to guarantee a secure retirement, let alone a gateway to the wealthy.

"The word 'millionaire' used to mean automatic affluence," said Ashton Lawrence, an advisor at Mariner Wealth Advisors in Greenville, South Carolina. "Now the goalposts have changed. It's still an important milestone, but it's no longer enough for most people."

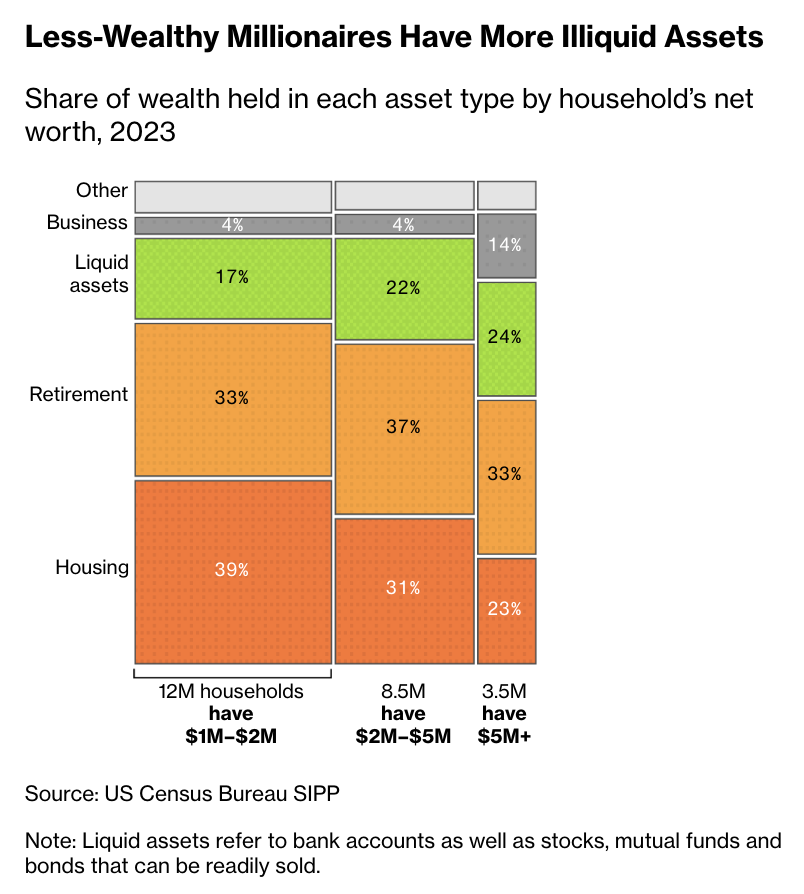

The $1 million threshold used in Bloomberg's analysis takes into account debt and other liabilities. Nevertheless, few of today's millionaires have anywhere near $1 million to spend. For households that "barely make the millionaire scale," with a net worth between $1 million and $2 million, the vast majority of their wealth is illiquid. In 2023, about 66% of their wealth will be tied up in primary residences and retirement accounts, an 8 percentage point increase since 2017.

To freely spend their wealth, millionaires typically need higher asset levels. In 2023, households with a net worth of $5 million or more had about 24% of their wealth stored in easily accessible bank or brokerage accounts, compared with just 17% of households with a net worth approaching $1 million.

Millionaires with less wealth have more illiquid assets

The proportion of various assets in household net assets in 2023

Source: U.S. Census Bureau SIPP

Note: Liquid assets are bank accounts and stocks, mutual funds, and bonds that can be sold at any time.

The Bloomberg analysis used data from the U.S. Census Bureau's Survey of Income and Program Participation, which tracks long-term changes in the wealth of tens of thousands of households. A separate analysis of the Federal Reserve's Survey of Consumer Finances from 1989 to 2022 showed similar rapid growth in the number and share of millionaire households in recent years, confirming the increasing share of millionaires' net worth held by home equity and retirement account balances.

Of course, $1 million is still a life-changing sum for most Americans. The median household income in the U.S. was $83,730 in 2024, while the median account balance in Vanguard Group 's 4.8 million retirement plans last year was just $38,000.

Although the latest data shows that the number of American millionaires has jumped 50% in six years, they still face a series of factors that hinder the mobility of their wealth. For example, high interest rates have exacerbated liquidity problems. To raise funds for major expenses, investors and homeowners can often borrow against their assets, but the costs have risen significantly. According to the latest Bankrate survey of the largest lenders, the average interest rate on home equity lines of credit (HELOC) loans is 7.89%, almost double the rate homeowners paid in early 2022. Margin loan rates at major retail brokerages such as Fidelity, Vanguard, and Charles Schwab now start at 10% or 11%, depending on the size of the portfolio.

“When interest rates are higher, we feel less wealthy, regardless of the value of our assets,” said Nicole Gopoian Wirick, a financial planner and president of Prosperity Wealth Strategies.

So-called "paper millionaires" have always been able to simply sell their assets. However, now they have more reasons to hesitate. Selling a home not only involves significant hassles and transaction costs, but also requires finding a new place to live at a time when housing affordability in the United States has plummeted. Moving may mean forgoing mortgage rates that are well below current market rates. Even if they have substantial assets beyond their homes and age-restricted retirement accounts, accessing that wealth is not easy. Advisors warn clients that selling large amounts of stock could trigger hefty tax bills.

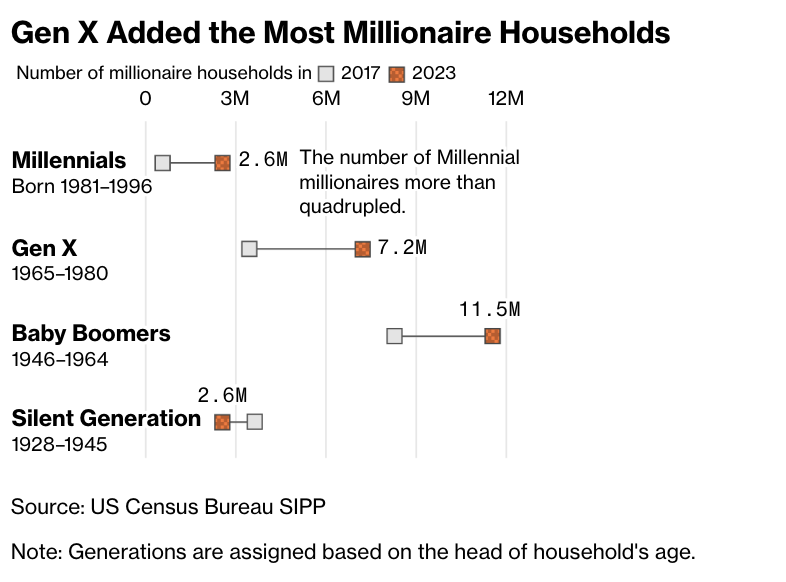

There are significant differences in the number of millionaires and the distribution of their wealth across generations. As the "Silent Generation" gradually dies out, the only millionaires to see a decline are those born before 1946. At the same time, older Americans have had more time to accumulate 401(k) or IRA retirement savings accounts and can freely access these funds starting six months before their 60th birthday. According to a Bloomberg analysis, only about 27% of the wealth of millennial millionaires is held in retirement accounts, compared to 37% for baby boomers.

Generation X has the largest number of new millionaire households

Source: U.S. Census Bureau SIPP

Note: Generational divisions are based on the age of the household head.

Advisors say even millionaire status isn't enough to convince wealthy clients to quit their jobs. However, the amount needed to stop working and maintain a pre-retirement lifestyle can vary from person to person. "Factors like inflation, longer lifespans, taxes, and geographic location all influence how much money you need," says Ashton Lawrence.

Millionaires may still be able to afford a comfortable middle-class life, but for many, the classic millionaire lifestyle - vacation homes, private jet and yacht charters, haute couture shopping - is becoming increasingly out of reach.

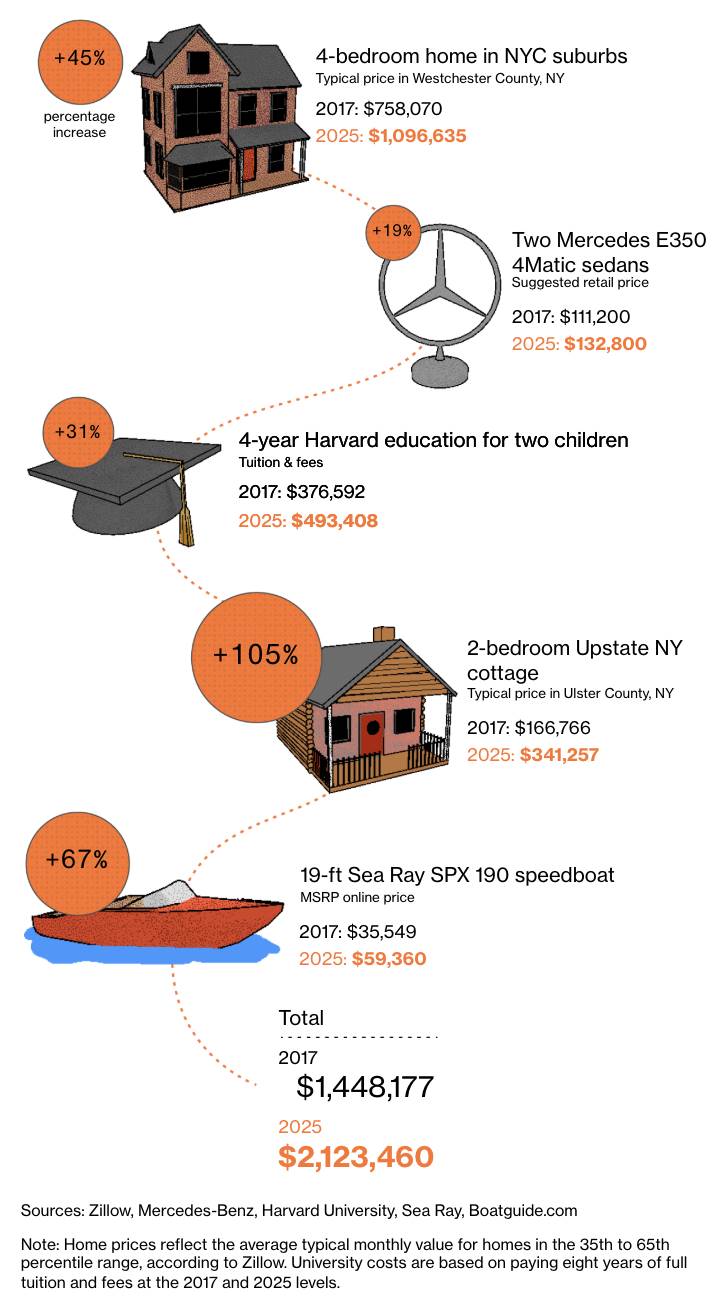

Take the lifestyle of a wealthy New York family: a four-bedroom home, two new Mercedes sedans, Ivy League educations for two children, a small upstate vacation home, and a 19-foot speedboat. Less than a decade ago, these expenses totaled about $1.4 million. By 2023, the same lifestyle had climbed to $2.1 million.

The millionaire lifestyle isn't what it used to be

Spending, a hallmark of affluent lifestyles, has nearly doubled since 2017.

Sources: Zillow, Mercedes-Benz, Harvard University, Sea Ray, Boatguide.com

Note: Home price data is based on Zillow's typical monthly average value for homes in the 35th to 65th percentile range. College costs are based on eight years of full tuition and fees in 2017 and 2025.

“That’s one of the indirect reasons some young people are frustrated about not having the same standard of living as their parents,” said Thomas Murphy, a senior financial planner at Murphy & Sylvest Wealth Management in Dallas. “They thought $1 million was going to solve all their financial problems, but now the real number they need to be thinking about is $10 million.”