On September 17, the Federal Reserve announced a 25 basis point interest rate cut, marking another directional shift in monetary policy. This easing measure follows three rate cuts by the end of 2024, and follows five consecutive on-hold periods in 2025. This decision was driven by a confluence of factors: a significant cooling in the US labor market, with job growth stagnating in August and previous figures significantly revised downward, and the unemployment rate rising to 4.3%, further convincing the market that support for "full employment" is waning. Meanwhile, while inflation remains above the 2% target, maintaining a year-on-year growth rate of around 2.9% in August, the market generally believes that the price disruptions caused by tariffs are only temporary. Against this backdrop, the Fed appears to be prioritizing employment stability over inflation control, and is, in part, responding to continued pressure from President Trump to cut interest rates.

It's worth noting that this policy tussle isn't just a shift in monetary policy; it also reveals unprecedented divisions within the Federal Reserve. At the July meeting, two members cast a rare dissenting vote, a first since 1993. Meanwhile, Trump's frequent pressure on Powell has further fueled the tension surrounding this policy adjustment. The market generally believes that this rate cut will not only impact future financial market trends and policy expectations, but may also reshape global capital flows, becoming a key turning point in this monetary cycle.

How to view this interest rate cut

The Fed's 25 basis point rate cut is more of a "risk management cut" than a signal of aggressive easing. The dot plot shows that the median forecast for the 2025 interest rate has been lowered from 3.9% to 3.6%. This means that on top of the one rate cut already in place, there is still 50 basis points of room for further cuts this year, with a high probability of another cut in October and December. As of now, the probability of another 25 basis point rate cut by the Fed in October is 87.5%. By 2026 and 2027, the median forecast has continued to decline to 3.4% and 3.1%, respectively, reinforcing the market's judgment of moderate easing in the medium and long term. However, the long-term interest rate anchor remains stable at 3.0%, indicating that the Fed's "neutral interest rate" has not changed.

The underlying signals are quite subtle: On the one hand, inflation risks remain elevated, with overall PCE growth likely to rise to 2.7% year-on-year in August, and core PCE remaining at 2.9%, prompting officials to refrain from drastic policy easing. On the other hand, downside risks in the labor market necessitate proactive defenses. Consequently, Powell's team has opted for a "small and slow approach," guiding the market through meeting-by-meeting decisions and expectation management, rather than drastically swinging policy.

Politically, this interest rate decision can be seen as a defensive counterattack by Powell's conservative faction against the Trump camp, safeguarding the Fed's independence. With the exception of new Fed Governor Milan, who continued to implement the president's will, most officials opted for rationality and unity, leaving only a small amount of room on the dot plot. In the short term, the market may be comforted by the possibility of two consecutive rate cuts, but the outcome clearly shows that Trump has lost the upper hand in this round of negotiations with the Fed.

Historical interest rate cuts: Market performance during interest rate cut cycles

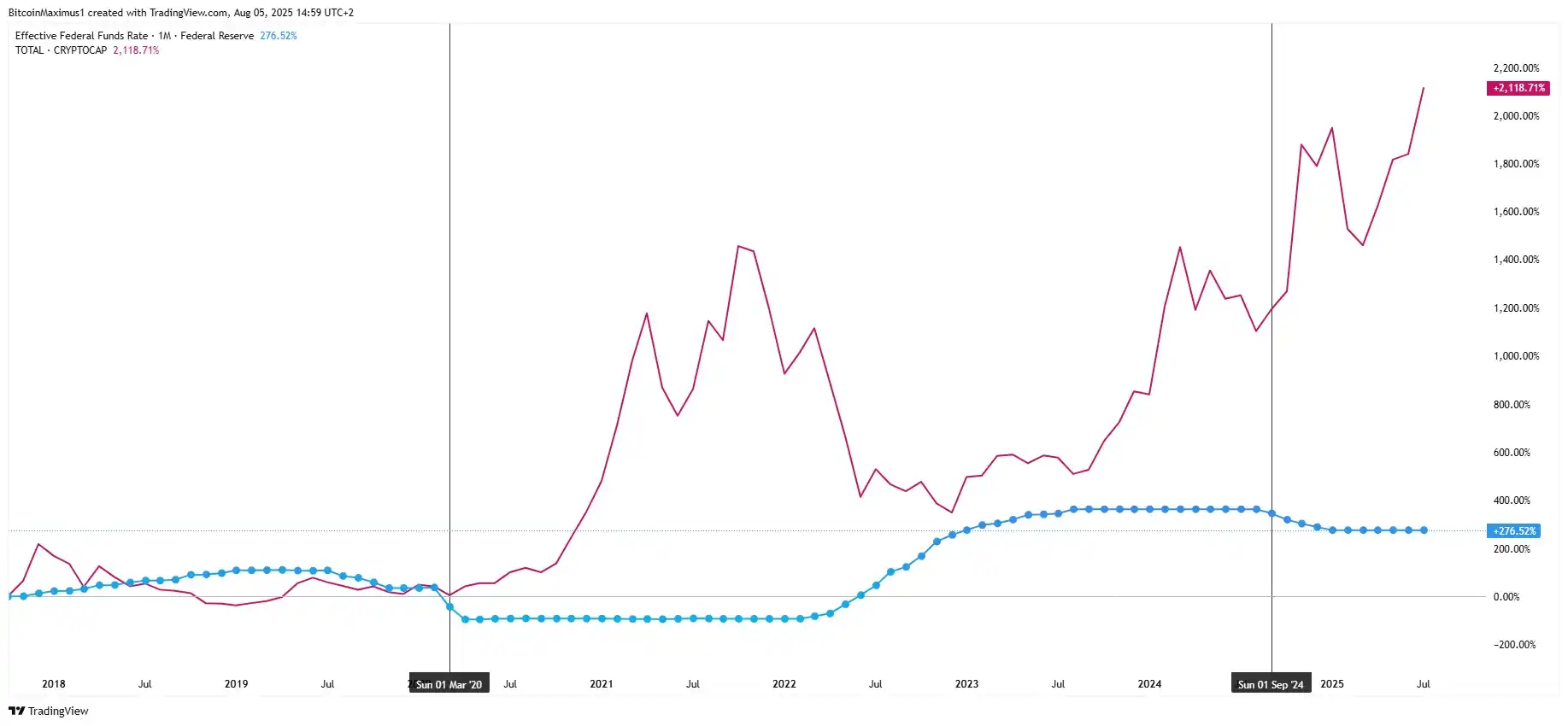

Historically, the Federal Reserve's interest rate cuts can be broadly categorized into two types: precautionary and bailout. The cuts in 1990, 1995, and 2019 fall into the former category. These occurred before a full-blown recession and were primarily intended to hedge potential risks, often injecting new growth momentum into the market. The cuts in 2001 and 2008, on the other hand, were forced upon them by the financial crisis and ultimately led to sharp market declines. Currently, with a weak US labor market, tariffs, and geopolitical uncertainty, while inflation has shown signs of easing, the overall environment resembles more of a precautionary approach than a crisis. This is precisely why risky assets have continued their strong performance this year, with both Bitcoin and US stocks reaching record highs.

Related reading: " With another step towards interest rate cuts, will the market start a wild bull market after September? "

Plotting the path of interest rate cuts alongside cryptocurrency market capitalization reveals a strong correlation: falling interest rates often coincide with bullish cycles in the crypto market. The rate cuts in 2020 and 2024 both marked the beginning of parabolic rallies in cryptocurrencies. This pattern further confirms that falling interest rates have a significant positive impact on risky assets like cryptocurrencies.

How do institutions view the market after the interest rate cut?

Coinbase's research report indicates that the crypto bull market has room to continue into the early fourth quarter of 2025, driven by ample liquidity, a favorable macroeconomic environment, and supportive regulatory developments. Bitcoin is considered the biggest beneficiary, and its performance is expected to continue to exceed market expectations. Unless energy prices fluctuate sharply, driving inflationary pressures, the immediate risks of disrupting the path of US monetary policy are quite limited. Meanwhile, technological demand for digital asset treasuries (DATs) will continue to inject incremental capital into the crypto market. Although the "September curse" has long plagued the market—Bitcoin fell against the US dollar in September for six consecutive years from 2017 to 2022—this seasonal pattern has been broken in 2023 and 2024.

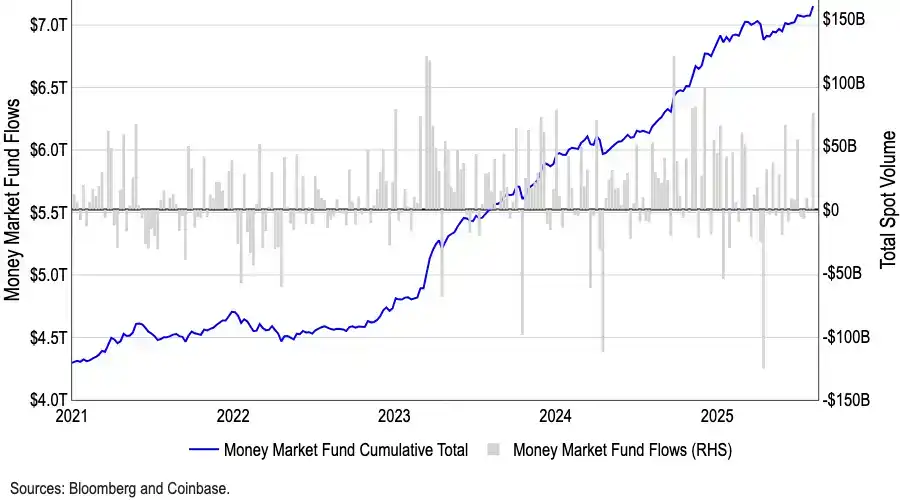

US money market funds have reached a record $7.2 trillion, with a significant amount of capital trapped in low-risk instruments. Historically, outflows from money market funds have correlated positively with gains in riskier assets. With the implementation of interest rate cuts, the attractiveness of these yields will gradually diminish, potentially unleashing more capital into cryptocurrencies and other high-risk assets. This unprecedented cash pile is arguably the most potent potential trigger for this bull market.

Furthermore, from a structural perspective, funds have begun to gradually shift away from BTC. BTC's market dominance has fallen from 65% in May to 59% in August. Meanwhile, the total Altcoin market capitalization has grown by over 50% since early July, reaching $1.4 trillion. While CoinMarketCap's "Altcoin Season Index" remains around 40, well short of the 75 threshold that traditionally defines an altcoin season, this discrepancy between a low indicator and a surge in market capitalization reveals that funds are selectively flowing into specific sectors, particularly ETH. ETH not only benefits from institutional interest in ETFs exceeding $22 billion, but also carries the core narrative of stablecoins and RWAs, making it a more attractive asset than BTC.

Other institutions are equally optimistic about BTC's price. Sean Dawson of Derive predicts that Bitcoin could reach $140,000 by the end of the year, and could even reach $250,000 if institutional funds continue to flow in. Bitmine CEO Tom Lee stated in a CNBC interview, "Bitcoin could easily reach $200,000 before the end of this year." BitMEX co-founder Arthur Hayes also predicted in an interview that Bitcoin could reach $200,000 by the end of 2025, citing the potential for the US government's Treasury bond repurchase program to release liquidity into the market and divert investor funds to higher-risk assets.

However, some stock traders are hedging against short-term volatility risks, as the 25 basis point rate cut has been largely priced in. Options traders predict that the S&P 500 index could see a two-way swing of about 1% on Wednesday, the largest single-day swing in nearly three weeks. IUR Capital CEO Gareth Ryan stated that the key will depend on whether the dot plot confirms additional rate cuts at the end of 2025 and in the first quarter of 2026. If so, the stock market reaction may be relatively mild; if the intentions are ambiguous, the market may experience greater volatility. JPMorgan Chase's trading desk also warned that the meeting could become a "good news" event.

Click here to learn about BlockBeats' BlockBeats job openings

Welcome to join the BlockBeats official community:

Telegram group: https://t.me/theblockbeats

Telegram group: https://t.me/BlockBeats_App

Official Twitter account: https://twitter.com/BlockBeatsAsia