This report was written by Tiger Research, analyzing the potential and expected scenarios for Upbit and Bithumb's chain construction against the backdrop of global exchanges' self-chain launch trends.

TL;DR

Global major exchanges are launching their own chains to secure new revenue sources. It cannot be ruled out that Upbit and Bithumb will also join this competition.

Possible scenarios are four: OP Stack-based Layer 2, Korean won stablecoin infrastructure, utilizing the liquidity characteristics of the Korean market, and tokenization of unlisted stocks. Each can be a differentiated approach reflecting the unique market environment of Korea.

Of course, regulatory constraints and technical complexity remain significant hurdles. Realization in the short term is not easy. However, it is clear that these two exchanges must seek new growth drivers amid declining trading volumes and intensifying global competition.

1. READY, SET, LAUNCH: The Beginning of Exchange Self-Chain Competition

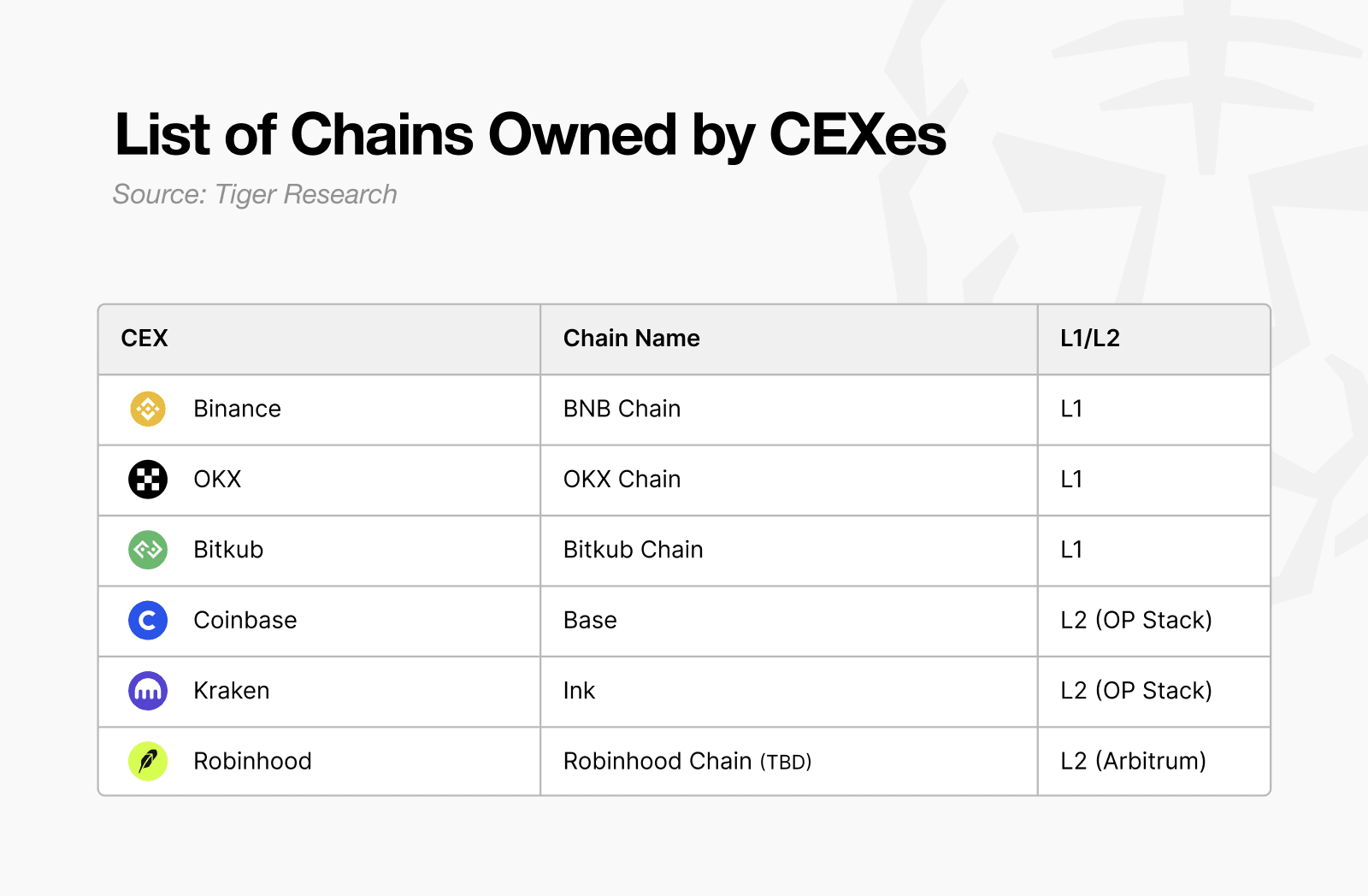

Cryptocurrency exchanges are diving into blockchain infrastructure competition in earnest. With Coinbase's Base, Kraken's Ink, and recently Robinhood joining, the competitive landscape has become even more intense.

Behind this fierce competition lies the limitation of the existing fee-based business model. While the exchange's fee-based model is the most stable and proven revenue source in the cryptocurrency industry, its structural characteristics heavily dependent on market conditions necessitate revenue diversification. Additionally, while exchanges previously competed within the limited scope of their regulatory jurisdictions, the competitive stage is now expanding to a global dimension. Moreover, decentralized exchanges (DEX) have challenged the centralized exchanges' dominance by recording over 25% market share at one point.

Simultaneously, as the cryptocurrency industry's integration into the institutional framework accelerates, exchanges are rapidly finding derivative business opportunities utilizing blockchain infrastructure beyond simple transaction mediation. Ultimately, with these changes intertwining, exchanges' self-chain competition is bound to accelerate further.

2. What If: If Upbit and Bithumb Launch Their Own Chains

In a situation where global exchanges are competing to launch their own chains, the natural question is, "Is there a possibility for Korea's major exchanges, Upbit and Bithumb?" To determine this, we need to examine the current situation and previous attempts of these exchanges.

(Translation continues in the same manner)Here's the English translation:The biggest reason is the development complexity and the scale of required resources. Layer 1 development and operation require massive resources. Even in Layer 2, where rollup services have lowered entry barriers, substantial professional manpower is required, as evidenced by the fact that approximately 40 developers were deployed for Kraken's Ink project. From the exchange's perspective, independently building and operating such infrastructure inevitably becomes a significant burden. Moreover, their purpose is not focused on building high-performance infrastructure itself, but on expanding business based on infrastructure through platform business.

Regulatory risks are added to this. Layer 1 requires native token issuance, but in Korea's regulatory environment, token issuance is practically impossible and the possibility of regulatory sanctions is high. Therefore, like Coinbase's approach, a Layer 2 model without native token issuance will be the most realistic alternative.

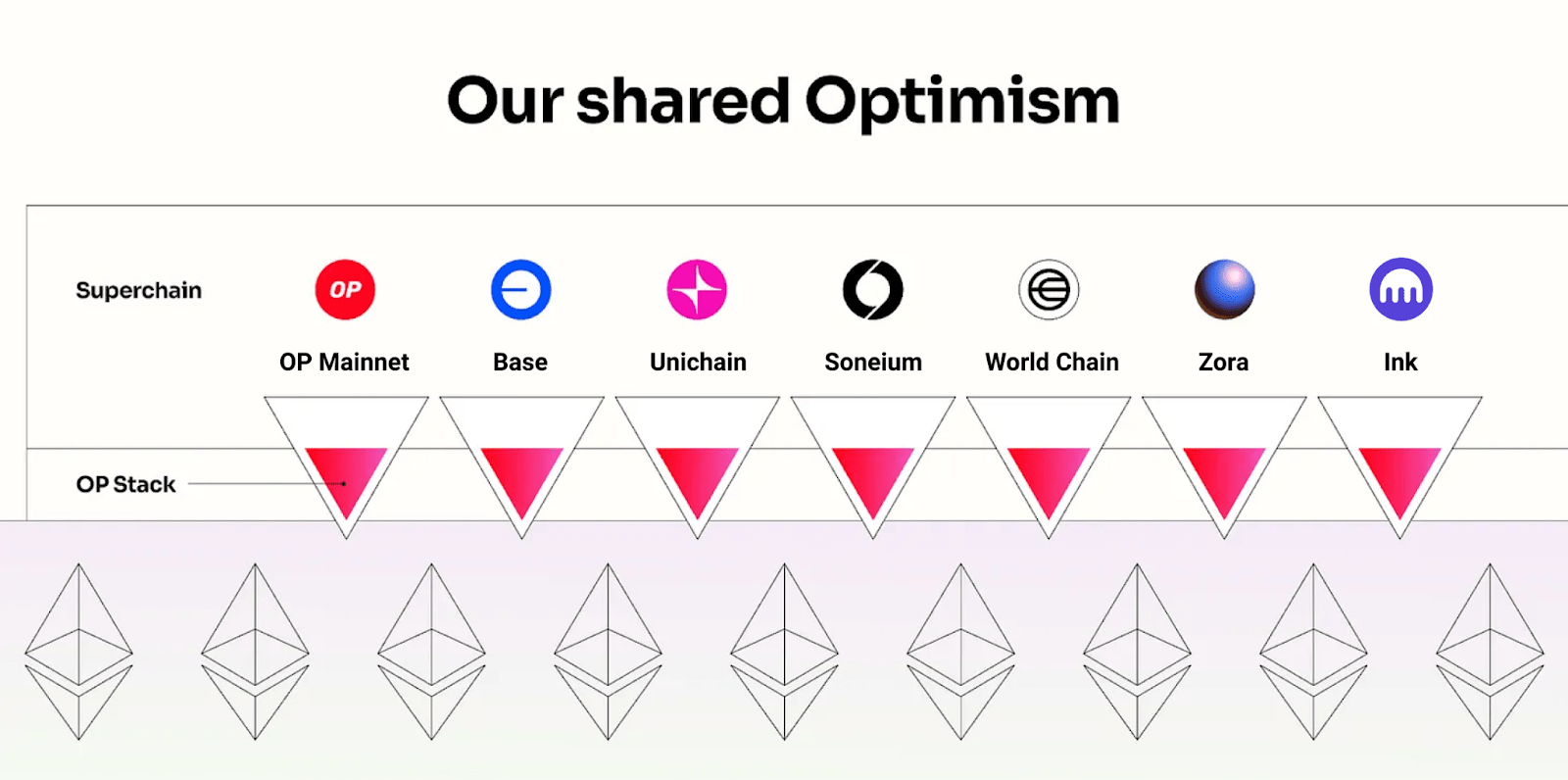

While multiple stacks exist for Layer 2 development, the Optimism (OP) stack has been virtually adopted as a standard by global exchanges. Coinbase's Base and Kraken's Ink are both built on this foundation and have established themselves as an exchange-type reference model. Robinhood exceptionally chose Arbitrum, as its strategic objectives were different. While Coinbase and Kraken pursued broad ecosystem expansion emphasizing interoperability, Robinhood focused on on-chain conversion of its financial services, making Arbitrum, which offers high customization flexibility, more suitable.

Upbit and Bithumb have similar goals. Both exchanges must expand to on-chain services using their large user base to overcome the limitations of their existing fee-centric model and create new revenue streams, and for this, openness and interoperability are key. Therefore, if Upbit and Bithumb launch their own chain, the most likely option would be a public Layer 2 based on the OP stack.

Scenario 2: Korean Won Stablecoin Infrastructure

Another scenario for Upbit and Bithumb launching their own chain is building a dedicated infrastructure centered on Korean won stablecoin.

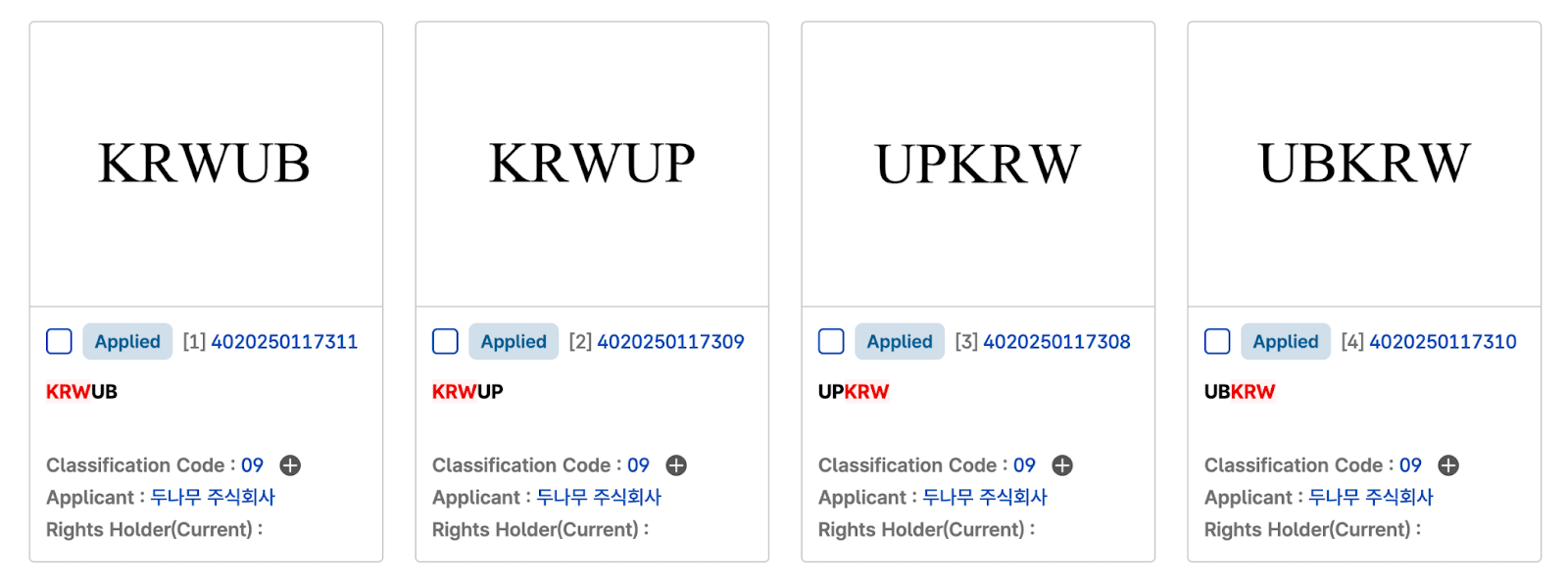

Both exchanges are indeed showing active movements in the stablecoin market. Upbit and Bithumb have each filed trademarks related to stablecoins, and Upbit especially has officially announced plans to enter the won stablecoin market in collaboration with Naver Pay, the country's top simple payment service. Focusing on Upbit, which has the highest probability, the realistic scenario is Naver Pay issuing a won-based stablecoin while Upbit provides the blockchain infrastructure. This is because the Virtual Asset User Protection Act prohibits exchanges from trading virtual assets issued by themselves or their special relationships.

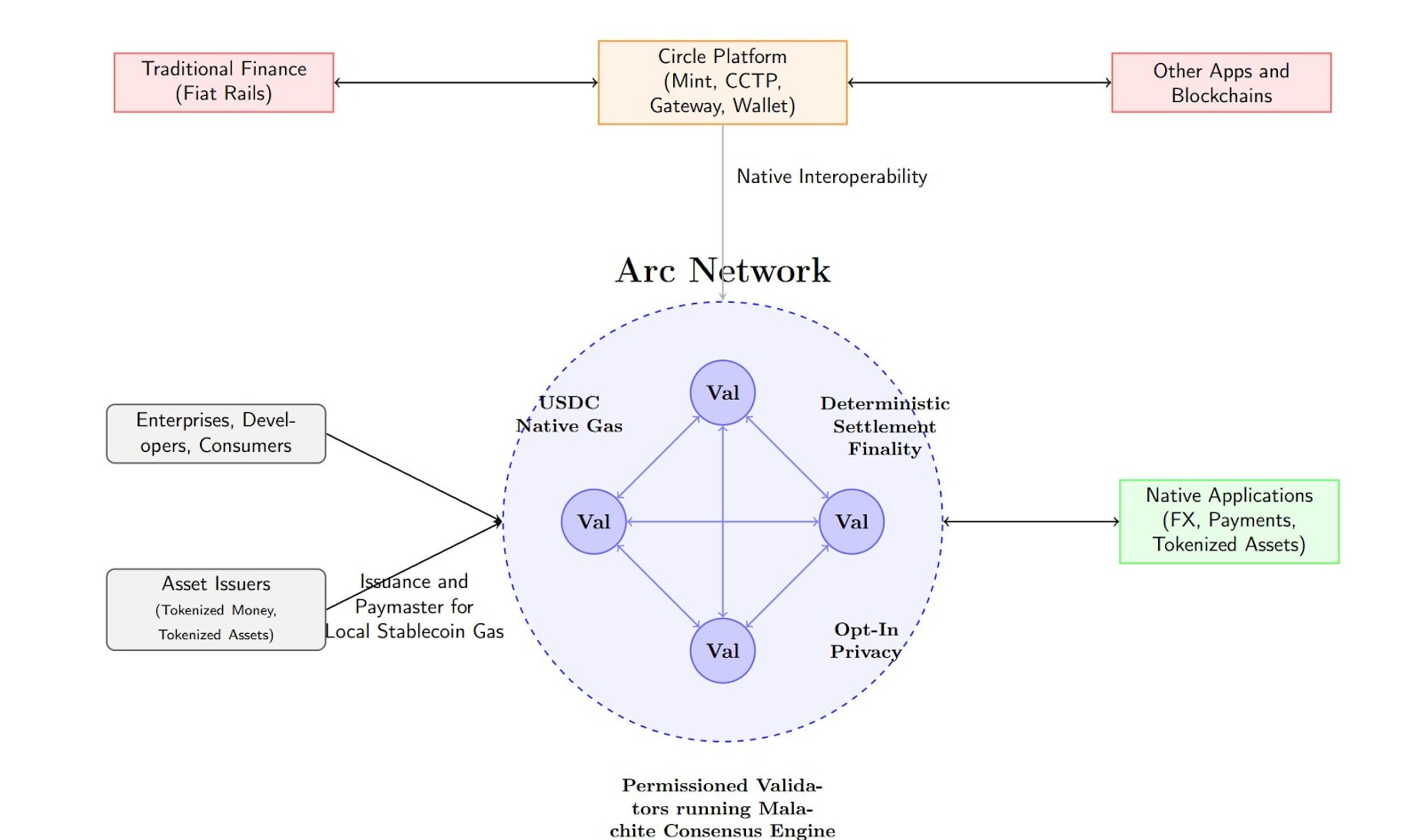

In this case, the key is building a dedicated infrastructure optimized for stablecoins. It can implement differentiated services by adding real-life payment or privacy protection features, and design a structure where network gas fees are paid with won stablecoins. This is similar to USDC's Arc Network model, aiming for an ecosystem where all transactions revolve around stablecoins. Such a structure provides users with a stable cost structure while creating practical demand for won stablecoins and establishing a continuous utilization foundation.

However, technical constraints exist. Optimism fundamentally uses Ethereum for gas fees and does not support custom gas token functionality. Therefore, in this case, a Layer 2 based on Arbitrum, which allows customization, or building a Layer 1 with won stablecoin as the native token, might be more suitable alternatives.

Scenario 3: Leveraging Korea's Liquidity Characteristics

One potential play for Upbit and Bithumb is to leverage Korea's liquidity characteristics. Currently, Korea records the world's second-largest liquidity in terms of legal tender, but this liquidity remains confined within exchange internal systems.

Exchanges can issue wrapped tokens such as upBTC and bbBTC based on deposited assets. Coinbase's cbBTC is a representative example. These wrapped tokens can be utilized on other chains, but if exchanges provide convenience like one-click integration within their apps, users are likely to remain within the chain built by the exchange. In this case, project teams looking to leverage rich liquidity will have reasons to choose that chain, the ecosystem will be activated, and exchanges can secure infrastructure-based revenue. Furthermore, it is judged that they can directly attempt additional business models such as direct lending using wrapped tokens. Scenario 4: Entering the Pre-IPO Stock Tokenization Market Another strategy that Upbit and Bithumb can choose is to enter the pre-IPO stock tokenization market. Dunamu, which operates Upbit, has already gained experience through Securities Plus Unlisted, but this remains a P2P trading model that simply connects buyers and sellers. It has clear structural limitations with low transaction success rates and limited liquidity. If they tokenize unlisted stocks based on their own chain, the situation changes. Tokenized stocks can be traded continuously through liquidity pools or market makers, and ownership transfer can be automated and processed transparently through smart contracts. Beyond simply improving trading efficiency, features such as automatic dividends, conditional trading, and programmable shareholder rights can be implemented on the chain, enabling financial product designs that were impossible with existing securities systems. It is also noteworthy that Naver is currently pursuing the acquisition of Dunamu's Securities Plus Unlisted stake. If Upbit provides chain infrastructure and Naver handles platform operation and physical stock management, this could be a realistic division of labor given the regulatory environment. In other words, by separating trading infrastructure and securities management roles, they can reduce institutional risks and enter the tokenization market by complementing the limitations of existing services. Conclusion We have examined various scenarios of what Upbit and Bithumb's own chains might look like. However, in reality, there are many obstacles to overcome. The biggest constraint is regulation. Since Korea follows a positive regulatory approach, services not specified in laws are difficult to introduce. With both exchanges being designated as large corporate groups, regulatory burdens have increased, and the lack of Web3 native leadership, like Base's Jesse Pollak, is also considered a limitation. Adding technological complexity, the possibility of their own chains becoming a reality in the short term is low. Nevertheless, the possibility of them attempting this still exists. Domestic trading volume has continued to decline since peaking in 2021, and global competition is becoming increasingly fierce. The existing fee-based model clearly has growth limitations, and previous attempts to diversify revenue have not yielded significant results. To ensure continuous growth, new momentum is needed, and bold experiments like building their own chains can be one axis of this. This can be the most realistic business diversification strategy that leverages the user base and liquidity advantages these two exchanges possess.Tiger Research Report Usage Guide

Tiger Research supports the fair use of reports. This is a principle that allows broad use for public interest purposes while not affecting commercial value. According to fair use rules, reports can be used without prior permission, but when citing Tiger Research reports, you must 1) clearly state 'Tiger Research' as the source, and 2) include the Tiger Research logo. If republishing or reconstructing materials, separate consultation is required. Use without prior permission may lead to legal action.