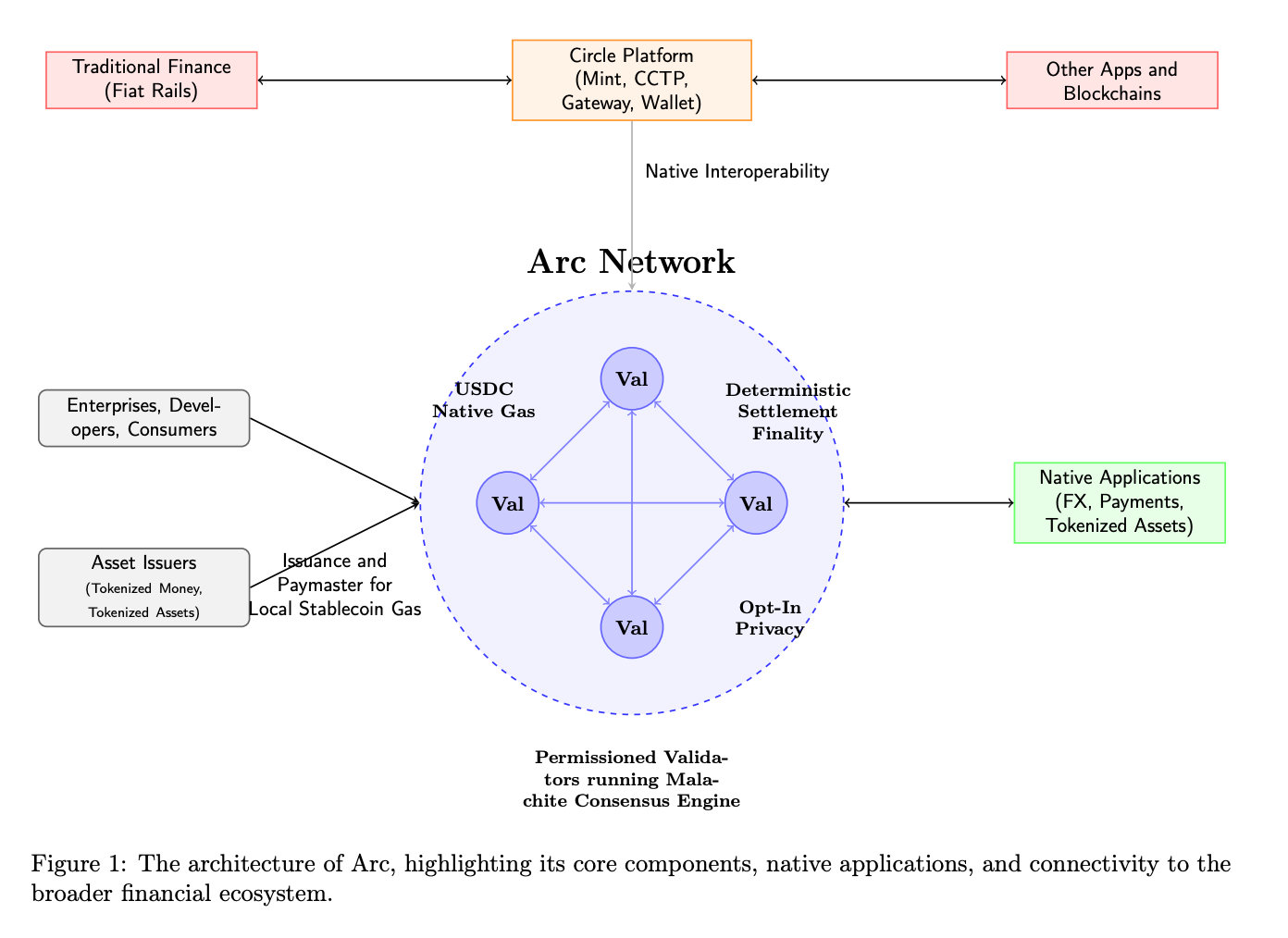

This is a blockchain tailored for stablecoin (USDC):

USDC serves as the native gas, eliminating the need to hold ETH or other volatile tokens; it features an institutional-grade quote request system supporting 7×24 on-chain settlement; with transaction confirmations under 1 second, it can provide balance and transaction privacy options for enterprises, meeting compliance requirements.

These features are more like a technological declaration of monetary sovereignty. Arc is open to all developers, but the rules are set by Circle.

From Centre to Arc, Circle has completed a triple jump:

First jump: Obtaining minting rights (USDC);

Second jump: Building financial channels (APIs, CCTP);

Third jump: Establishing a sovereign territory (Arc)

This path almost recreates the historical evolution of central banks in the digital world:

From private banks issuing banknotes, to monopolizing currency issuance rights, to controlling the entire financial system - only Circle is moving faster.

And this "digital central bank dream" is not the only one being pursued.

Similar Ambitions, Different Paths

In the stablecoin battlefield of 2025, major players all have a "central bank dream", just with different paths.

Circle chose the most challenging but potentially most valuable path: USDC → Arc blockchain → Complete financial ecosystem.

Circle is not satisfied with being just a stablecoin issuer, but wants to control the entire value chain - from currency issuance to clearing systems, from payment rails to financial applications.

Arc's design is filled with "central bank thinking":

First, monetary policy tools, with USDC as native gas, giving Circle capabilities similar to a "benchmark interest rate"; second, clearing monopoly, with a built-in institutional-grade RFQ forex engine that mandates on-chain forex settlement through its mechanism; lastly, rule-making power, with Circle retaining control over protocol upgrades and deciding which functions go online and which behaviors are allowed.

The most challenging part is ecosystem migration - how to convince users and developers to leave Ethereum?

Circle's answer is not migration, but supplementation. Arc is not meant to replace USDC on Ethereum, but to provide solutions for use cases that existing public chains cannot satisfy. For instance, enterprise payments requiring privacy, forex transactions needing instant settlement, or on-chain applications requiring predictable costs.

This is a bold bet. If successful, Circle will become the "Federal Reserve" of digital finance; if it fails, billions of dollars invested could be wasted.

PayPal's approach is pragmatic and flexible.

PYUSD was first launched on Ethereum in 2023, expanded to Solana in 2024, went live on the Stellar network in 2025, and recently covered Arbitrum.

PayPal hasn't built a dedicated public chain, but instead allows PYUSD to flexibly spread across multiple usable ecosystems, with each chain serving as a distribution channel.

In the early stages of stablecoins, distribution channels are indeed more important than infrastructure development. When ready-to-use options exist, why build your own?

Capturing user mindshare and usage scenarios first, and considering infrastructure issues later, especially given PayPal's 20 million merchant network.

Tether is like the de facto "shadow central bank" of the crypto world.

It barely interferes with USDT usage, releasing it like cash, with circulation being a market matter. Especially in regions and use cases with unclear regulation and KYC difficulties, USDC became the only choice.

Tether CEO Paolo Ardoino once stated that USDT primarily serves emerging markets (such as Latin America, Africa, Southeast Asia), helping local users bypass inefficient financial infrastructure, more like an international stablecoin.

With 3-5 times more trading pairs than USDC on most exchanges, Tether has formed a powerful liquidity network effect.

Most interestingly, Tether's approach to new chains is to not actively build but support others' building. For example, supporting stablecoin-specific chains like Plasma and Stable. It's like placing bets, maintaining presence in various ecosystems at minimal cost, waiting to see which one emerges.

In 2024, Tether's profits exceeded $10 billion, surpassing many traditional banks; instead of using these profits to create its own chain, it continued buying government bonds and Bitcoin.

Tether is betting that as long as sufficient reserves are maintained and no systemic risks emerge, inertia will maintain USDT's dominant position in stablecoin circulation.

These three models represent different judgments about the future of stablecoins.

PayPal believes in user supremacy. With 20 million merchants, technical architecture is secondary. This is network thinking.

Tether believes in liquidity supremacy. As long as USDT remains the base trading currency, everything else is unimportant. This is exchange thinking.

Circle believes in infrastructure supremacy. Controlling the rails means controlling the future. This is central bank thinking.

The reason for this choice might be from Circle CEO Jeremy Allaire's congressional testimony: "The dollar is at a crossroads, and monetary competition is now a technological competition."

Circle sees more than just the stablecoin market, but the standard-setting rights for digital dollars. If Arc succeeds, it could become the "Federal Reserve System" for digital dollars. This vision is worth the risk.

2026: Critical Time Window

The time window is narrowing. With regulation advancing and competition intensifying, when Circle announced Arc would launch on mainnet in 2026, the crypto community's first reaction was:

Too slow.

In an industry that values "rapid iteration", taking nearly a year from testnet to mainnet seems like a missed opportunity.

But if you understand Circle's situation, this timing isn't bad.

On June 17th, the US Senate passed the GENIUS Act. This is the first federal-level stablecoin regulatory framework.

For Circle, this is a long-awaited "legitimization". As the most compliant stablecoin issuer, Circle has almost met all GENIUS Act requirements.

2026 is precisely the time when these details will be implemented and the market adapts to new rules. Circle doesn't want to be the first to take risks, but also doesn't want to arrive too late.

Enterprise customers value certainty most, and Arc provides exactly that - certain regulatory status, certain technical performance, certain business model.

If Arc successfully launches and attracts sufficient users and liquidity, Circle will establish its leadership in stablecoin infrastructure. This could open a new era where a private company operates like a "central bank".

If Arc performs poorly or is overtaken by competitors, Circle might have to rethink its positioning. Perhaps ultimately, stablecoin issuers can only be issuers, not infrastructure leaders.

Regardless of the outcome, Circle's attempt is driving the entire industry to think about a fundamental question: In the digital age, who should control the power of money?

The answer to this question may become clear in early 2026.