On its first financial report night after going public, Circle submitted a complex answer of "accounting loss and operational growth".

The second quarter's total revenue and reserve earnings were $658 million, a 53% year-on-year increase, with adjusted EBITDA of $126 million, a 52% year-on-year increase. Meanwhile, USDC continued to expand in circulation, with end-of-period circulation reaching $61.3 billion and a 28% market share of stablecoins. However, due to two non-cash factors triggered by the IPO - large share-based compensation and fair value changes in convertible bonds totaling $591 million - the company recorded a net loss of $482 million.

Beyond the financial report day, the competitive framework of the industry was quickly rewritten this summer. The 'GENIUS Act' was officially implemented, putting the boundary between "bank-issued stablecoins" and "licensed non-bank issuers" on the table. Circle's Chief Strategy Officer, Dante Disparte, directly stated in a recent interview: The real competition has just begun, and it remains to be seen whether banks will rashly issue coins.

Circle's cooperation landscape is also expanding.

Management mentioned in the conference call the deepening cooperation with mainstream exchanges like Binance and OKX, as well as integration with payment networks such as Stripe, Visa, Mastercard, and banking infrastructure providers like Fiserv. At the same time, the rise of USDC balance on the Coinbase platform and new partner distribution agreements have also pushed up this quarter's distribution-related costs. These structural tensions of "growth-sharing-cost" are shaping USDC's business model and ecosystem distribution path.

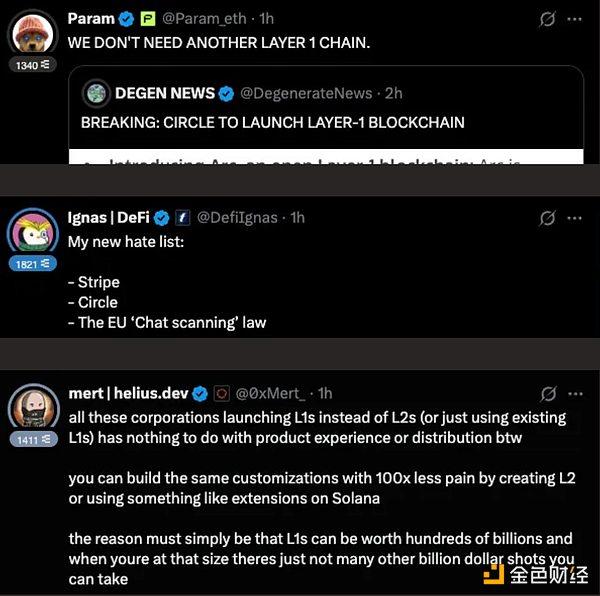

Simultaneously, Circle announced its self-developed blockchain Arc for stablecoin finance. Using USDC as its native Gas, it aims for ultra-high settlement speed and low volatility fees, and introduces optional privacy and compliance-auditable disclosure mechanisms for institutional scenarios, seen as a key step from "single issuer" to "full stack platform".

Last night, Circle's CEO Jeremy Allaire answered the most concerned questions in the financial report conference call and The Information live interview:

· Why is there an accounting loss under high growth?

· The future competitive relationship between banks and non-bank stablecoins under the 'Genius Act' background;

· The "game-like cooperation" with exchanges and layout of new partners;

· Whether considering applying for a license in Hong Kong;

· Strategic goals and industry ecosystem position of the Arc chain

Beating has integrated the key questions and answers to help readers quickly and accurately understand Circle management's views on the industry and the company's plans (to read the full conference call, please refer to the 'Circle 2025 Q2 Financial Report Conference Call Full Text' below):

Subscription Fees, Service Fees, and Transaction Fees: Management Plans to Increase Revenue Sources

1. In the second quarter, Circle's revenue increased by 53% year-on-year, but reserve interest still dominates. How will the company reduce its dependence?

Jeremy Allaire: Our goal is to build the world's largest, regulated stablecoin network, which is still in its early stages. Whether the stablecoin market grows at a compound annual rate of 90% or 25%, the inflow will be massive, and we hope to continue expanding USDC's market share.

In the past, the company mainly monetized through USDC's monetary volume and relied on partners to drive distribution. But since last year, we have launched new products at the protocol layer, blockchain infrastructure, developer tools (such as Circle Wallets), and application layer (such as Circle Payments Network, CPN), with related revenue growing 250% year-on-year this quarter.

The next step is to introduce subscription fees, service fees, transaction fees, and other higher-margin models, which we have communicated on Wall Street and could be substantial in the coming years.

Adjusted EBITDA increased 52% year-on-year, with a 50% profit margin. This quarter's RLDC profit margin increased by over 200 basis points, largely from new business growth. We are building a full-stack system from infrastructure, stablecoin layer to payment network and developer tools, operating synergistically and forming multiple monetization channels, which is a necessary condition for driving the internet financial system's development.

2. USDC circulation was $61 billion in the second quarter. What drives its growth? What are the future incremental opportunities?

Jeremy Allaire: Recent growth reflects more of a global market "green light" signal for stablecoins. This is not only due to the digital asset market's activity but also indicates that stablecoins are now seen as usable digital cash tools. With a 90% year-on-year growth and a 49% increase year-to-date, the future growth potential is enormous.

Stablecoin growth is largely an output of economic activity. The digital asset market is the starting point, but interest in financial services' various sub-sectors is accelerating, with potential lasting decades. Third-party predictions range from 25% to 90% CAGR, and our internal model baseline is 40%, which can still bring considerable returns in an uncertain environment.

3. How to view the adoption of USDC in cross-border remittances?

Jeremy Allaire: Cross-border remittance demand is growing, including both C2C (personal transfers) and B2B enterprise treasury liquidity. This quarter, we expanded cooperation with Remitly, MoneyGram, ZEPS, and CPN's primary application scenario is cross-border remittances.

USDC's advantage lies in its globally built liquidity network and deposit/withdrawal system, covering key nodes such as banks and payment service providers, enabling low-cost settlement between different fiat currencies, electronic currencies, and bank accounts. This network effect and delivery capability are difficult to replicate, and simply "issuing a coin" cannot solve the end-to-end cross-border settlement problem.

(The translation continues in the same manner for the rest of the text, maintaining the specified translations for specific terms)Jeremy Allaire: We view banks as important potential partners and have collaborated with regional banks, globally systemically important banks, and community bank networks. This quarter, we also announced partnerships with core banking infrastructure providers like Fiserv, FIS, and Matera, which serve tens of thousands of banks. Banks of all sizes can benefit, and we are willing to promote cooperation.

4. Will Circle apply for a stablecoin license in Hong Kong?

Jeremy Allaire: Asia is our key market. USDC institutional-grade direct liquidity is already available in Hong Kong, and we are collaborating with a global systemically important bank. Hong Kong is one of the earliest CPN corridors, crucial for cross-border trade. We are familiar with the local regulatory framework and will consider this within our broader growth strategy.

Launching Arc Chain, Circle Builds Its Own Technology Stack

1. Circle today announced its self-developed blockchain Arc. With many public chains already existing in the market, why create another one?

Jeremy Allaire: Circle is a market-neutral company. USDC protocol operates on 24 public chains, CCTP enables seamless cross-chain mobility, and developer tools support multi-chain applications. However, we found that mainstream institutional adoption of stablecoins still faces barriers.

Arc is an open blockchain designed specifically for stablecoin finance, focusing on payment, foreign exchange, and capital market scenarios, not a general-purpose platform.

All transactions and gas fees on Arc will be settled in USDC, and future stablecoins issued on Arc can also be used for payment. These predictable, cash-equivalent fees are more easily accepted by financial institutions and listed companies. Arc also provides instant settlement finality, meeting bank regulatory requirements and offering optional privacy features.

2. Will Arc's gas fees become a new revenue source for USDC?

Jeremy Allaire: Yes. Arc aims to carry the core transaction flow of stablecoin finance, and gas fees are one of the new revenue models.

We already have multiple transaction fee sources, including CPN's scaled transactions, Circle Mint advanced features, USYC yield-generating tokens, etc. Arc's fee model will complement these revenues.

4. How will Arc maintain low fees and ensure validator distribution?

Jeremy Allaire: Arc uses a completely new fee mechanism to ensure low and predictable transaction costs, paid in USDC. Validators will be operated by audited professional nodes, meeting security and compliance requirements, and achieving global distribution among major institutions. We are developing market expansion plans, with initial designs outlined in the white paper.

5. What will be the future development relationship between Arc and CPN (Circle Payments Network)?

Jeremy Allaire: CPN is currently in the pilot stage, with cross-border payment corridors opened in Hong Kong, Brazil, Nigeria, and Mexico. By year-end, it will significantly expand to major developed markets and more emerging markets, enhancing liquidity guarantees.

Arc will become an important underlying support for CPN, with built-in foreign exchange engines, configurable privacy and confidential transfers, directly serving inter-institutional fund flows. We anticipate that many financial institutions already integrated with CPN will use Arc as a payment and settlement infrastructure in the future.