Author: Haotian

Recently, compared to ETH's steady upward trend, SOL's performance seems slightly lackluster. $4,300 vs $175, what mystery lies behind this price difference? In my personal understanding, at a deeper level, this is a covert battle about "who is the institutional darling":

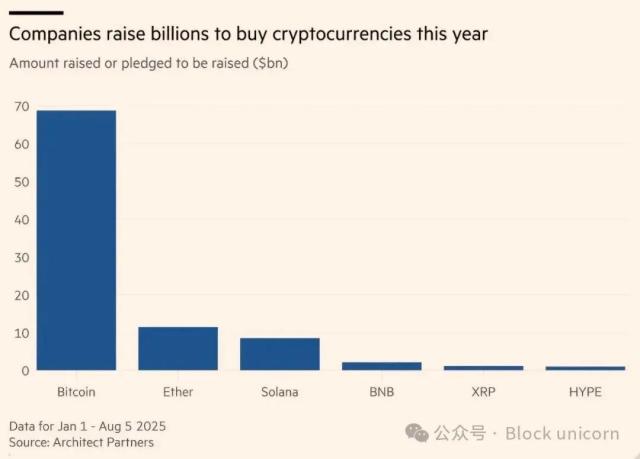

1)ETH has already obtained the "pass" to enter the traditional financial world——After ETF approval, cumulative net inflow has exceeded 10 B USD, allowing off-market funds to enter compliantly, which is equivalent to opening a formal door for institutions.

SOL's ETF application remains uncertain, and the current reality is that it lacks funding channels, directly impacting price performance. Of course, this can also be interpreted as SOL still having room for catch-up, as SOL's ETF is not entirely impossible, just requiring more time to go through compliance procedures.

Critically, under the purchasing power of companies like SharpLink and BitMine in US stocks, ETH's MicroStrategy has already demonstrated a certain institutional FOMO effect, which will drive more enterprise Treasury fund allocations, creating massive Wall Street off-market funding momentum for ETH;

2)Currently, the stablecoin scale difference between ETH and SOL is still quite significant, with data showing 137 B VS 11 B. Everyone must be wondering, with both having American blue-blood genes and on-chain NASDAQ, why has SOL fallen so far behind in this wave of US stablecoin policy-guided stablecoin war?

Actually, it's not SOL's fault. Behind this is the ultimate test of chain infrastructure's decentralization, security, and liquidity depth. On Ethereum, USDC (65.5 billion), USDT, and DAI firmly control the stablecoin market, which reflects absolute trust from institutions like Circle and Tether in the Ethereum network;

Although SOL's VCs are all American capital, Wall Street's new institutional buyers might not consider too much, just looking at the realistic data gap, which might be a short-term insurmountable difference for SOL. However, objectively speaking, SOL's stablecoin growth is actually quite good. Including PayPal's PYUSD choosing to focus on Solana provides considerable imagination space, just requiring patience;

3)Once upon a time, SOL's on-chain economic vitality was explosive, with PumpFun's daily trading volume breaking millions of dollars, and various MEME on-chain memes flying everywhere. However, the problem is that we're currently in an institutional chip accumulation period. Large funds care more about compliance channels, liquidity depth, and safety records—these "hard indicators"—rather than how many MEMEs are in PVP on the chain.

In other words, it's not yet the narrative cycle dominated by retail investors. Conversely, this on-chain vitality is precisely SOL's differentiated advantage. When the market cycle shifts and retail investor FOMO reignites, SOL's accumulated innovative gameplay and user base might become the trigger for the next market wave;

4)As SBF's "biological son", SOL might still be affected by the FTX collapse, with the tragic fall from $260 to $8 still vivid in memory. Although technically SOL has completely separated, in institutional memory, this association is like a scar, occasionally brought up.

Moreover, rising from $8 to $175 itself proves SOL's ecosystem's resilience. Those teams building during the darkest times have become new forces reconstructing SOL's public chain fortress, and this rebirth experience might be beneficial in the long term;

5)ETH follows a layer 2 stratification route, though criticized for liquidity fragmentation, which precisely meets institutional risk isolation needs. SOL's integrated high-performance route, with everything running on a single chain, appears as concentrated risk in institutional eyes.

So you see, Robinhood partnering with Arbitrum is a prime example. From an institutional perspective, ETH's high gas drawback actually becomes an advantage for filtering high-value transactions, though contrary to Mass Adoption, the current main theme isn't about Mass Adoption, but who can win institutional Wall Street favor;

6)Lastly, time consensus accumulation differs. ETH has 9 years of history, while SOL is only 4 years old. Although native projects like Jupiter and Jito have demonstrated world-class product capabilities, compared to DeFi giants like Uniswap, Aave, and MakerDAO, there's a gap in market education, ecosystem sedimentation, and trust accumulation.

In summary, the E guard's painful memories might breed an S guard wave under a new market FOMO, but this contest is essentially a periodic mismatch between institutional and retail investor narratives. After all, ETH wasn't built in a day, and SOL's growth speed is actually already quite remarkable.