Previously a tool dedicated to cryptocurrency, stablecoin is gradually becoming part of mainstream finance. Circle and Tether now have larger US debt portfolios than some sovereign countries.

The recent passage of the GENIUS Act has legalized stablecoin use, driving interest from banks, payment processors, and Fortune 500 companies.

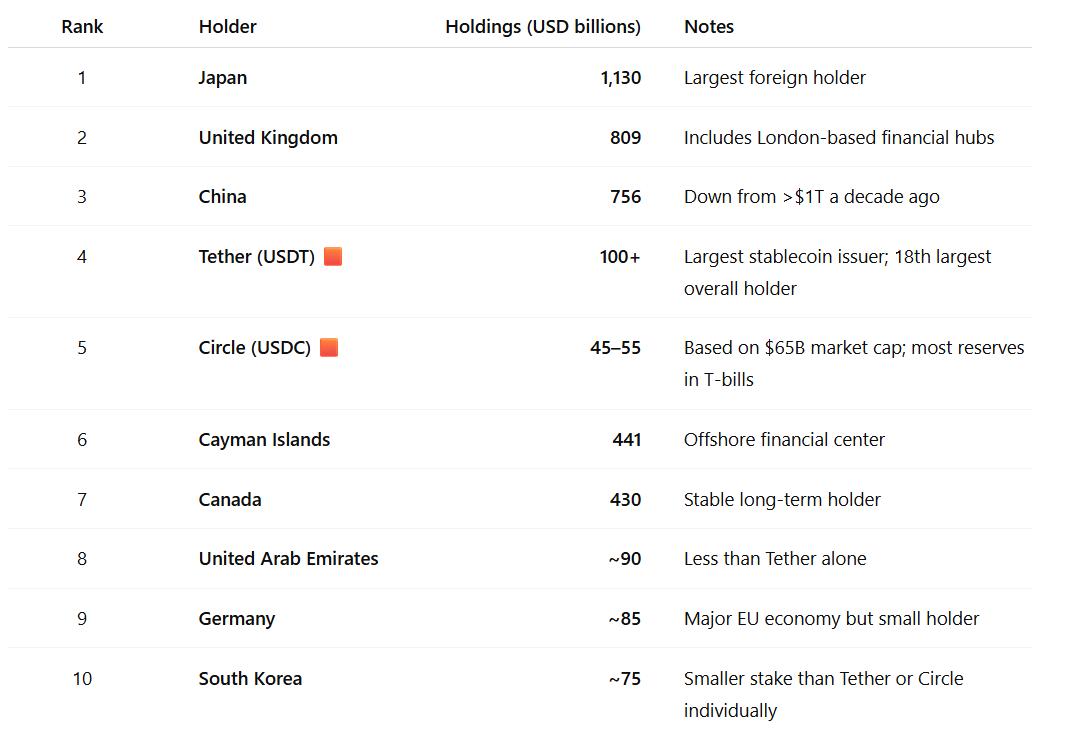

Circle and Tether quietly accumulate more US debt than Germany, South Korea, and UAE

Stablecoin is a digital token pegged to the USD and backed by reserves, typically in US Treasury bills (T-bills). This structure ensures that a token can be reliably exchanged for one dollar.

This stability makes them attractive for cross-border payments and as a payment layer for the cryptocurrency ecosystem.

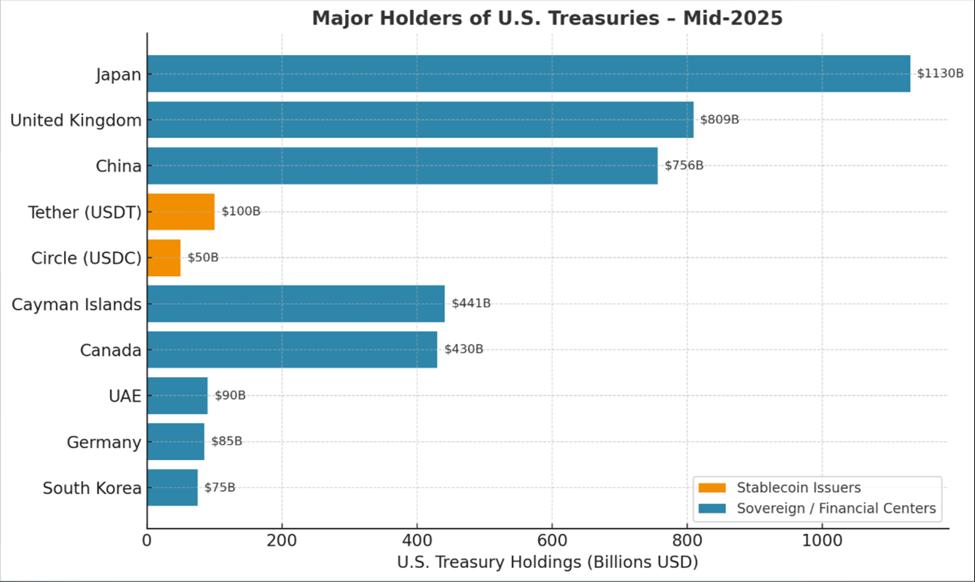

The two leading stablecoin issuers, Tether (USDT) and Circle (USDC), hold more US government debt than some large national economies. This includes Germany, South Korea, and the United Arab Emirates.

Tether, the largest stablecoin issuer, currently holds over 100 billion USD in T-bills. According to Treasury data, it ranks as the 18th largest US debt holder, above the UAE (85 billion USD).

Circle, the USDC issuer, holds between 45 and 55 billion USD in T-bills, surpassing South Korea (around 75 billion USD) if considered individually.

Combined, these two companies exceed all three countries, with a recent Apollo report highlighting the industry's rapid growth.

"Nearly 90% of stablecoin use is cryptocurrency transactions, which is likely to continue growing. The big breakthrough would be if USD stablecoins are used for global retail payments. If the USD stablecoin market grows to trillions, US T-bill demand will increase significantly. There are financial stability risks as money will move quickly if depositors lose trust in a stablecoin issuer," reads a quote from the Apollo report.

Top Foreign and Private Holders of US Treasuries as of Mid-2025

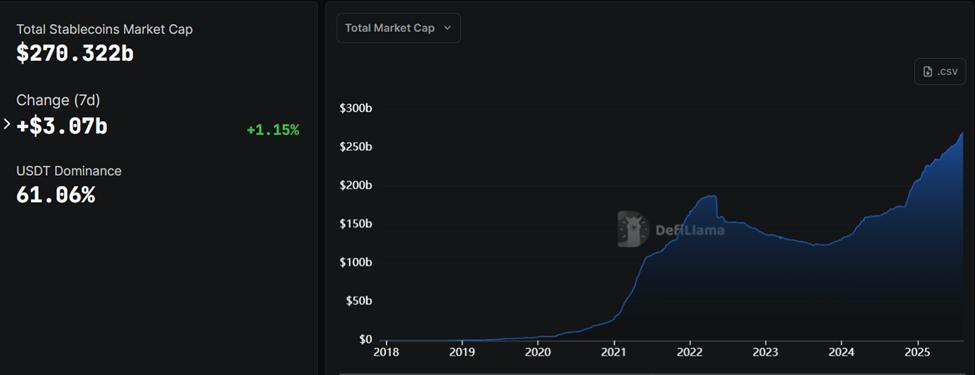

Top Foreign and Private Holders of US Treasuries as of Mid-2025The stablecoin industry is currently the 18th largest Treasury bill holder from outside, with forecasts showing it could grow from the current market capitalization of 270 billion USD to 2 trillion USD by 2028.

Stablecoin Market Cap. Source: defillama

Stablecoin Market Cap. Source: defillamaUSDC's market capitalization alone has increased 90% in the past year to 65 billion USD. This was driven by institutional acceptance and Circle's prominent IPO in June.

Trading Volume Competing with Traditional Payment Giants

Meanwhile, the acceptance story doesn't stop at reserves. Early 2024 saw stablecoin trading volume surpass Visa, mainly due to cryptocurrency transaction use. Increasing global remittance usage also contributes to growth, with a BeInCrypto report indicating that 49% of institutions use stablecoins.

With near-instant payments and low fees, stablecoins are being marketed as a faster, cheaper alternative to SWIFT and legacy payment systems. Stripe acquired the stablecoin startup Bridge for 1.1 billion USD in October, marking one of fintech's first major bets on this technology.

The rise of stablecoin issuers as large T-bill buyers occurs as traditional foreign holders are reducing. China's holdings have dropped from over 1 trillion USD a decade ago to 756 billion USD.

Although still the largest foreign holder with 1.13 trillion USD, Japan has also signaled a more cautious approach. This creates an opportunity for stablecoin issuers to become a stable source of demand for US debt.

Top Foreign and Private Holders of US Treasuries as of Mid-2025

Top Foreign and Private Holders of US Treasuries as of Mid-2025"The constant presence of stablecoin issuers is a major boost in confidence for the Treasury about where to place debt," Fortune reports, quoting Yesha Yadav, a professor at Vanderbilt Law School who studies the intersection of cryptocurrency and bond markets.

Supporters argue that stablecoins could help reinforce dollar dominance globally, similar to how the offshore "Eurodollar" market did in the 20th century.

They also suggest that increasing T-bill demand from stablecoin companies could help reduce long-term interest rates and strengthen US sanctions enforcement abroad.

However, skeptics warn against overstating the numbers, citing the US money market fund (MMF) sector, which is much larger than stablecoin holdings at around 7 trillion USD.

Meanwhile, bank lobby advocates warn that stablecoins could draw deposits from banks, potentially reducing lending capacity.

"Citi forecasts stablecoins will be among the largest US T-Bills holders. If US debt increases and T-Bills fluctuate, trust in digital dollars will also be affected. This creates a temporary shift towards other currencies," a user writes, citing Citibank.

Industry leaders counter that similar concerns about money market funds (MMF) decades ago were proven unfounded.

However, if stablecoins continue to absorb large amounts of short-term bonds, this could disrupt how Wall Street manages liquidity and risk.

However, the development of Circle and Tether shows that the US debt market has a new large class of investors, originating from the volatile cryptocurrency field rather than from traditional banks.