Pendle is the most successful DeFi protocol that has emerged in this cycle, without even needing the qualifier "one of". While many articles have explained Pendle, this piece aims to analyze the protocol's unique mechanism and value capture design from a new perspective, combining the latest developments. Readers familiar with Pendle's mechanism can skip the initial explanatory section and focus on the subsequent analysis.

What is Pendle

Pendle is a Yield Trading protocol. To explain how yield is traded, we'll use two assets from the synthetic stablecoin protocol Ethena: USDe and sUSDe.

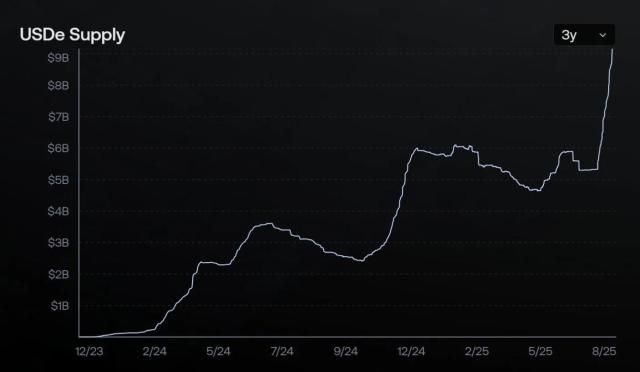

USDe is a stablecoin pegged 1:1 to the US dollar. Simply holding USDe does not generate interest but earns Ethena airdrop points, which can be used to allocate sENA tokens after each quarterly airdrop. sUSDe is the staked version of USDe, a yield-generating stablecoin with interest rates fluctuating between 5% and 15% based on market sentiment and funding rates. Holding sUSDe earns fewer Ethena points compared to USDe.

For these two assets, the yield for USDe is Ethena points, while sUSDe's yield consists of both interest and Ethena points.

Both interest and points are highly "time-sensitive". Interest rates can dramatically fluctuate with market conditions, and point values are closely tied to snapshot dates and token real-time prices. Therefore, the "yield" being traded requires a specific timeframe - it could be the yield for the next 3 months, but not for the next 300 years.

Yield is generated by the underlying asset. We call the current value of an asset that will generate yield at a future point "principal", thus completing the three key elements: principal, yield, and timeframe.

Pendle wraps yield-generating assets into Standardized Yield (SY) tokens, then splits them into Principal Tokens (PT) and Yield Tokens (YT) with a set timeframe, enabling the trading of "yield" within a specific period.

Before expiration, holding YT generates yield from the underlying token. At expiration, PT's value will equal SY, while YT's value will become zero. (For example, with 10 days left, YT represents 10 days of underlying asset yield and has value; after expiration, it represents 0 days of yield and becomes worthless.)

[The translation continues in the same manner for the rest of the text, maintaining the structure and translating all non-HTML content to English.]This is similar to the government bond model, where I buy a 1-year government bond with a face value of 110 for 100 yuan, and when redeemed at maturity, I receive 110 yuan, thus locking in a 10% annual yield. Similarly, as government bonds approach their redemption period, they get closer to their face value and can be redeemed at par.

As the seller of yield, PT holders have sold the "uncertainty" of yield and locked in a "fixed rate".

Becoming a Pendle LP (Liquidity Provider) is equivalent to simultaneously holding SY and PT, while selling part of the YT. In addition to the fixed income generated from the PT portion, LPs can also earn PENDLE token emission rewards (liquidity mining).

It's not difficult to see that Pendle offers choices for users who want to reduce risk and increase stable returns, those willing to take risks for potential uncertain returns, and those simply wanting to engage in DeFi mining. By addressing user needs, adoption comes naturally.

Pendle's Data

Pendle's success is evident from the data. Despite last week's market downturn and experiencing its largest asset maturity in history (meaning some users pursuing stable returns realized "profit settlement"), Pendle's TVL (Total Value Locked) still reached a new high of $700 million.

Over 48% of Ethena's assets were packaged as Pendle assets, reaching $460 million. More than $4 billion in Pendle PT assets were deposited as collateral in lending protocols like Aave, Morpho, Euler, and Silo. The recently launched HyperEVM-related assets attracted over $80 million in funds within 4 days. Despite over $1.5 billion in assets maturing mid-week, this caused less than a 3% TVL decline in a single day, with many assets choosing to remain and continue participating in the protocol, demonstrating trust.

PT assets deposited in various lending protocols

Crypto Profit Models

There are two most profitable business models: first, like a casino taking a cut, corresponding to exchanges in the crypto world; second, like a bank earning from loan interest spreads, corresponding to lending protocols in the crypto world.

Pendle is the 5th largest DEX (decentralized exchange) on Ethereum, following the "rake" model of collecting transaction fees. For traders, the "rake" model is often a zero-sum game - like perpetual contracts on CEX where one side's profit means the other side's loss, with the exchange being the only long-term winner.

However, Pendle presents scenarios where all participants can profit, which the author believes is its unique "positive externality".

(Translation continues in the same manner for the rest of the text)Pendle completed a private fundraising round in April 2021, raising $3.7 million with investors including Hashkey Capital, Mechanism Capital, and others. It also raised $11.83 million through an IDO at a price of $0.797 per token.

Pendle Founder TN Lee

After the market peaked in 2021 and quickly entered a bear market, the Pendle team, with their keen insight and forward-thinking, worked hard to build and quickly transform, ultimately launching the highly successful Pendle V2 version in 2022, successfully revitalizing the project across market cycles.

In July 2023, Pendle was listed on Binance Spot via Launchpool. One month later, Binance Labs (now Yzi Labs) announced investment in Pendle.

Simple Future Outlook

Pendle currently has no comparable competitors. Whether Spectra on EVM or RateX on Solana, similar products are far behind in liquidity, capital volume, and protocol integration. As Pendle establishes more ecosystem interactions and DeFi strategies with top protocols like Ethena and Aave, its track dominance will become increasingly unshakable.

Contract safety verified over time, accumulated brand effect, and user trust give us reason to believe that traditional capital (TradFi) would likely choose to collaborate with Pendle when entering the yield trading track.

Additionally, Pendle's latest funding rate trading protocol Boros, launched yesterday, is considered the next major growth point. The funding rate market is believed to have $200 billion in open interest and over $300 billion in daily trading volume potential. Within 24 hours of launch, Boros achieved an impressive $15 million in open interest and $36 million in nominal trading volume.

When I first introduced Pendle in March 2024 (when PENDLE was $1.2), I wrote that yield and risk are the core factors of finance, and balancing their transfer is an eternal strategy. Through decentralized magic, Pendle makes this happen on-chain, continuously bringing potential yields from outside the ecosystem into it, achieving a win-win game and gradually becoming an indispensable DeFi infrastructure with unlimited potential.

Now, 1.5 years later, Pendle has become an indispensable DeFi infrastructure, with its token price exceeding many "ghost chains". In the foreseeable future, Pendle will continue to grow rapidly, leading the DeFi track.

Disclaimer: The author holds PENDLE tokens that meet disclosure standards.