Written by: Tanay Ved, Victor Ramirez, Coin Metrics

Compiled by: AididiaoJP, Foresight News

Key Points:

- Under favorable regulatory environments and clear investor interest in publicly traded crypto assets, Kraken, Gemini, and Bullish are planning initial public offerings (IPOs).

- Coinbase's 2021 IPO set an industry benchmark. At the time of listing, Coinbase was valued at $65 billion, with 96% of its revenue coming from trading fees, while subscription and service revenue now accounts for 44% in Q2 2025.

- Among IPO candidate exchanges, Coinbase still leads with 49% of spot trading volume. Bullish and Kraken each hold 22% and are rapidly expanding new services.

- Not all reported trading volumes are of equal value. Round-trip trading analysis reveals artificial activity on some platforms and emphasizes the need to assess exchange quality and transparency.

Introduction

In the history of the cryptocurrency industry, the US government has often been cold, even hostile. But last week, things changed positively.

The Presidential Digital Assets Working Group released a 166-page report outlining the current state of digital assets and proposing policy recommendations for establishing a comprehensive market structure. Meanwhile, SEC Chairman Paul Atkins announced a "Crypto Project" in a public speech, aimed at making the US the "global crypto capital" by on-chain financialization of markets, simplifying complex crypto business licensing, and supporting the creation of financial "super apps" offering multiple services.

The main beneficiaries of this new regulatory framework are centralized exchanges. Several private centralized exchanges like Kraken, Bullish, and Gemini are leveraging this relatively favorable environment to seek initial public offerings (IPOs). As these companies open up to public investment, investors need to understand their fundamental drivers. In this article, we will deeply evaluate key metrics of these exchanges and highlight some considerations when using exchange-reported data.

Crypto Exchange IPO Boom

Since Coinbase's IPO in April 2021, crypto-related IPOs have been scarce over the past four years, mainly due to the adversarial relationship between crypto companies and the former SEC. Thus, private companies couldn't obtain liquidity from public markets, and unqualified investors couldn't profit by investing in these companies. With the Trump administration promising a more friendly regulatory system, a batch of new private crypto companies announced listing plans.

This environment, coupled with renewed investor interest in public market crypto exposure, has spawned some of the most explosive IPOs, such as Circle's recent public IPO. Gemini, Bullish, and Kraken plan to list in the US, hoping to seize this opportunity and position themselves as full-stack digital asset service providers.

(Translation continues in the same manner for the entire text)Trading on the Order Book: Analyzing Exchange Economic Activity

As mentioned, trading volume is one of the most predictive indicators for estimating valuation. However, reported trading volume may vary between exchanges and can be a misleading data point.

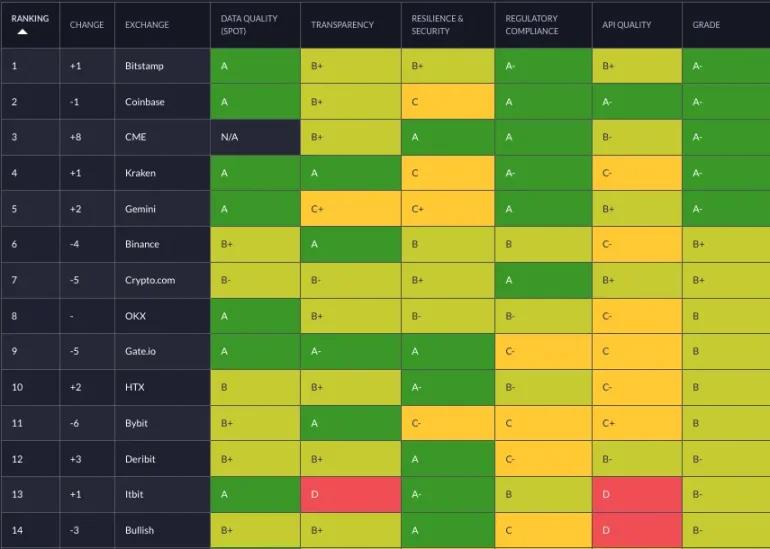

Although most major cryptocurrency exchanges have cracked down on wash trading, some irregular practices still exist. Our Trusted Exchange Framework method details how to detect abnormal trading activities and evaluates qualitative factors such as regulatory compliance.

Source: Trusted Exchange Framework

We developed a more powerful signal for detecting buy and sell trades by calculating the frequency of repeated trades. Our test method is as follows:

- We randomly selected 144 5-minute periods from January to June 2025, generating nearly 20 million trades.

- For each exchange and period, select one trade.

- If another trade occurs within 10 trades or 5 seconds, with an opposite direction, and almost identical amount and price (<1%), mark these two trades as repeated trades.

- Repeat this operation for each trade. Skip if the trade has already been marked as a repeated trade.

- Calculate the volume of trades marked as repeated trades and divide by the total volume.

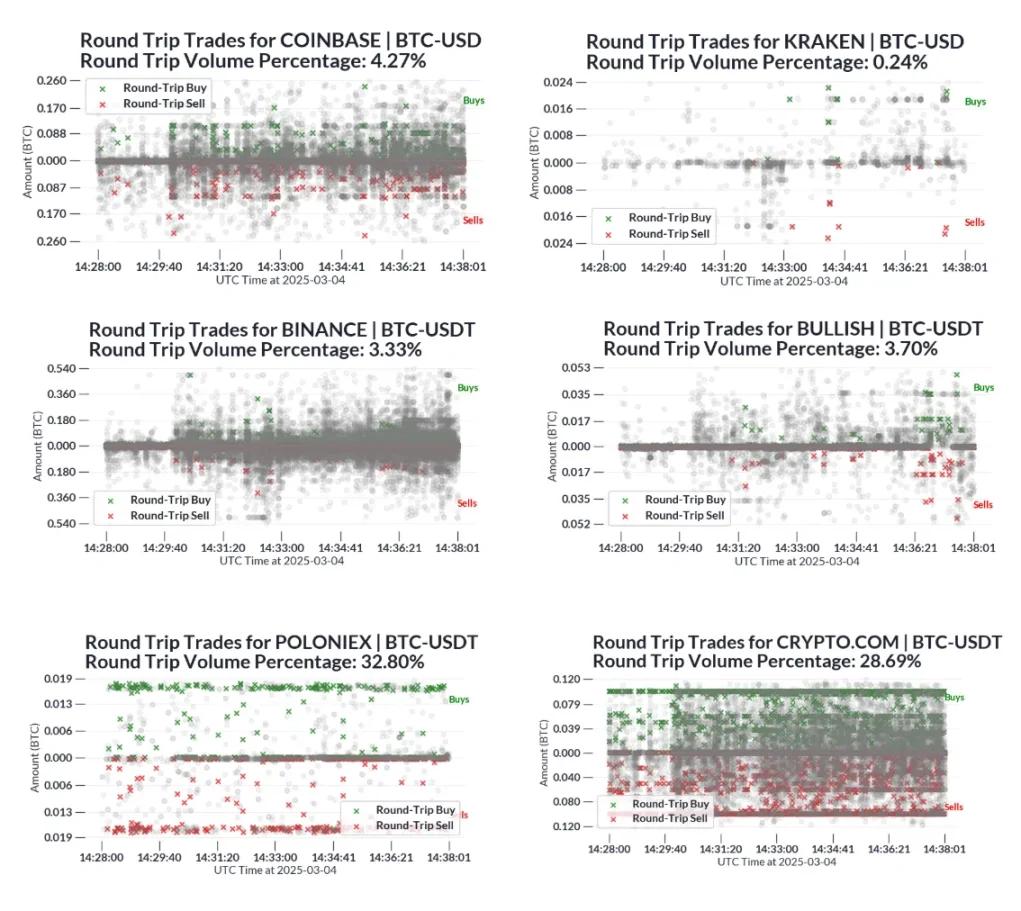

In the following diagram, we plot a sample of trades from a few exchanges in one period and mark suspected round-trip trades. Each gray point represents a normal trade, while green and red marks represent round-trip trades.

Source: Trusted Exchange Framework

Due to the approximation of this method, we expect some false positives, such as repeated trades caused by normal market activities (e.g., market makers providing liquidity on both sides of the order book). However, compared to industry baselines like Crypto.com and Poloniex, the proportion of repeated trades is high, raising concerns about the reliability of their reported trading volume data.

For example: In the first and second quarters of 2025, we estimate Crypto.com's trading volume to be around $720 billion, including BTC-USD ($201 billion), BTC-USDT ($192 billion), ETH-USD ($165 billion), and ETH-USDT ($160 billion). According to the estimated proportion, approximately $160 billion of trades in these trading pairs come from repeated trades.

Conclusion

As multiple cryptocurrency exchanges are about to go public, investors need to understand the relative trading volumes of these platforms. While trading volume helps estimate trading revenue (currently still the majority of income), qualitative factors such as business diversification, the existence of repeated trades, and regulatory compliance are also important considerations for assessing exchange quality. This information can help market participants determine whether valuations are reasonable.

Coinbase remains at the forefront four years after its IPO, mainly due to its diversification in revenue sources such as custody, stablecoins, and Layer-2 fees. However, competition in the exchange market is intensifying. Other exchanges must diversify their revenue sources away from trade-related fees that heavily depend on market sentiment to compete. As the market structure gradually becomes clear, exchanges are allowed to evolve from trading venues to comprehensive super-apps. How these exchanges seize this opportunity, whether they can realize their vision and replicate the success of past breakthrough IPOs, will be an important development to watch in the coming year.