Author: OxCousin, IOBC Capital

Original Title: Macro Outlook for the Crypto Market in the Second Half of 2025

In the first half of 2025, the Crypto market was significantly influenced by several macro factors, with three key aspects being: Trump administration's tariff policy, the Federal Reserve's interest rate policy, and geopolitical conflicts in the Russia-Ukraine and Middle East regions.

Looking ahead to the second half of the year, the Crypto market will continue to navigate a complex and changing macro environment, with the following macro factors playing crucial roles:

I. Derivative Impact of Trump's Tariff Policy: Inflation Expectations

Tariffs are an important policy tool for Trump's administration, with the government hoping to achieve a series of economic goals through tariff negotiations: first, expanding US exports and reducing trade barriers in other countries; second, maintaining a 10%+ base tariff to increase US fiscal revenue; third, enhancing the competitiveness of specific industries and stimulating the return of high-end manufacturing.

As of July 25th, tariff negotiations with major global economies have made varying degrees of progress:

Japan: An agreement has been reached. US tariffs on Japanese goods have been reduced from 25% to 15% (including automotive tariffs), with Japan promising to invest $55 billion in the US (covering semiconductors and AI), opening automotive and agricultural markets, and increasing US rice import quotas.

European Union: The deadline is August 1st. EU negotiation representatives arrived in the US on July 23rd for final consultations, but the negotiation results have not been publicly disclosed.

China: The third round of trade negotiations will be held in Sweden from July 27th to 30th. After the previous two rounds, US tariffs on China have been reduced from 145% to 30%, and Chinese tariffs on the US from 125% to 10%. There are reports that the US-China tariff negotiation period may be extended by 90 days, with potential tariff rollback if no new agreement is reached in the third round.

Additionally, the US has reached tariff agreements with the Philippines and Indonesia. The third round of US-China tariff negotiations is currently the most watched. While tariff policy uncertainty is gradually decreasing, the possibility of failing to make substantial progress in negotiations with key economic entities cannot be ruled out, which could lead to greater impacts on financial markets.

From an economic theory perspective, tariffs are a negative supply shock with a "stagflation" effect. In international trade, while enterprises are the tax subjects, they often transfer this tax burden to US domestic consumers through price transmission mechanisms. Therefore, it is expected that the US may experience a round of inflation in the second half of the year, which could significantly impact the Federal Reserve's interest rate reduction pace.

In summary, the impact of Trump's tariff policy on the US economy in the second half of the year may manifest as a periodic rise in inflation. Unless data indicates low inflation pressure, it will likely slow down the interest rate reduction pace.

II. Weak Dollar Cycle Favorable to the Crypto Market

The dollar tide cycle refers to the systematic outflow and inflow of the US dollar globally. Although the Federal Reserve did not cut interest rates in the first half of the year, the dollar index has weakened: falling from a high of 110 at the beginning of the year to 96.37, showing a clear "weak dollar" state.

The dollar's weakness may have multiple reasons: first, the Trump administration's tariff policy suppressed trade deficits, disrupting the dollar's circulation mechanism, while tariff barriers weakened the attractiveness of dollar assets, raising market concerns about the dollar system's stability; second, fiscal deficits drag down credit, with continuous increases in US debt scale and repeated rises in US debt rates deepening market doubts about fiscal sustainability; third, the petrodollar agreement expired without renewal, with global central banks' dollar reserves dropping from 71% in 2000 to 57.7%, and gold reserve proportions increasing, triggering "de-dollarization" attempts. Additionally, the policy orientation reflected in the rumored "Mar-a-Lago Agreement" may have played a supporting role.

Based on previous dollar tide cycles, the dollar index's strength almost dictates global liquidity trends. Global liquidity typically follows a complete 4-5 year dollar tide cycle with cyclical fluctuations. The weak dollar cycle generally lasts 2-2.5 years, and if calculated from June 2024, this weak dollar cycle might continue until mid-2026.

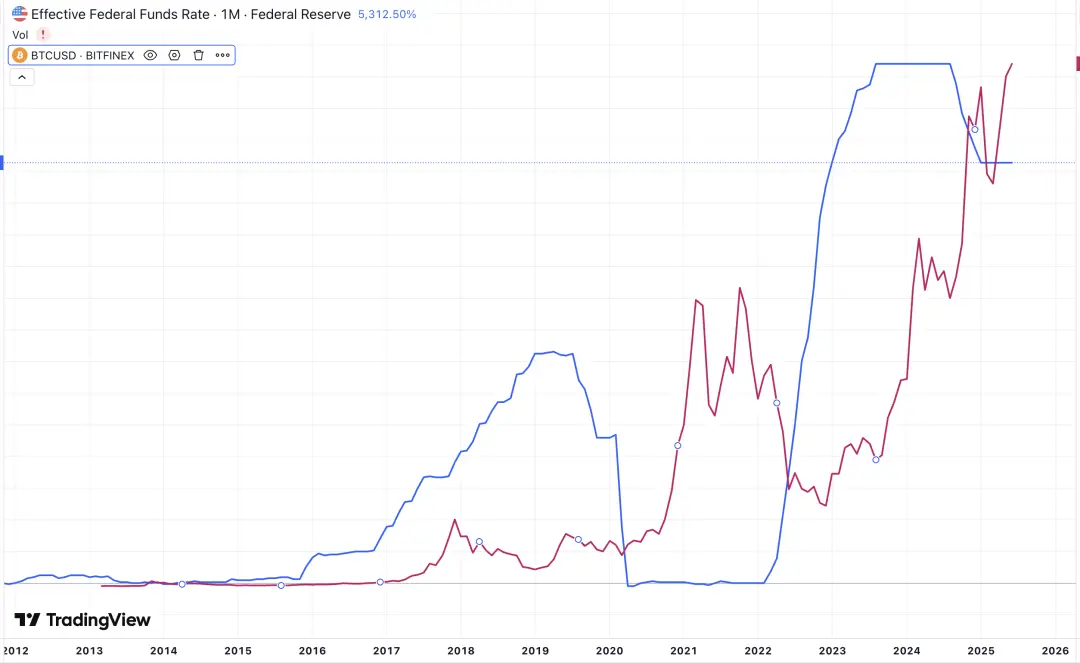

Graphic: IOBC Capital

As the image shows, Bitcoin's trend often shows a negative correlation with the dollar index. When the dollar weakens, Bitcoin typically performs strongly. If the "weak dollar" cycle continues in the second half of the year, global liquidity will shift from tight to loose, continuing to benefit the crypto market.

III. Federal Reserve Monetary Policy Likely to Remain Cautious

There are four monetary policy meetings in the second half of 2025. According to the CME "Fed Watch" tool, there is a high probability of 1-2 interest rate cuts. Specifically, there's a 95.7% chance of maintaining the current rate in July, and a 60.3% chance of a 25 basis point cut in September.

Since Trump took office, he has repeatedly criticized the Federal Reserve's slow interest rate reduction pace on X platform, even directly blaming Fed Chair Powell and threatening to fire him, which has subjected the Federal Reserve to certain political intervention pressures. However, the Federal Reserve withstood the pressure and did not cut rates in the first half of the year.

According to normal term arrangements, Fed Chair Powell will officially step down in May 2026, with the Trump administration planning to announce a new chair nominee in December 2025 or January 2026. In this context, market attention is gradually focusing on the main dovish committee members within the Federal Reserve, viewed as potential "shadow chair" influences. Nevertheless, the market generally believes that the July 30th monetary policy meeting will continue to maintain the current rate level.

Predictions for delayed rate cuts are primarily based on three core reasons:

1️⃣ Persistent inflation pressure - Influenced by Trump's tariff policy, US CPI rose 0.3% month-on-month in June, with core PCE inflation rising 2.8% year-on-year. The tariff transmission effect is expected to further push up prices in the coming months, and the Federal Reserve believes that the path to reducing inflation to the 2% target is obstructed and requires more data confirmation;

2️⃣ Slowing economic growth - The 2025 growth rate is estimated at only 1.5%, but short-term data like retail sales and consumer confidence exceed expectations, alleviating the urgency for immediate rate cuts;

3️⃣ Persistent job market resilience - Unemployment remains low at 4.1%, but corporate hiring is slowing. The market predicts a gradual unemployment rate increase in the second half of the year, with Q3 and Q4 unemployment rate forecasts at 4.3% and 4.4% respectively.

In summary, the probability of a rate cut on July 30th, 2025, is extremely low.

Graphic: IOBC Capital

Overall, the Federal Reserve's monetary policy is expected to remain cautious, with potentially 1-2 rate cuts for the year. However, by observing historical Bitcoin and Federal Reserve rate trends, there is actually no significant correlation between the two. The global liquidity under the weak dollar state might have a more substantial impact on Bitcoin than Federal Reserve rate changes.

IV. Geopolitical Conflicts May Temporarily Affect the Crypto Market

The Russia-Ukraine war is currently in a stalemate, with dim prospects for a diplomatic solution. On July 14, Trump proposed a "50-day ceasefire deadline", stating that if Russia does not reach a peace agreement with Ukraine within 50 days, the United States will impose 100% tariffs and secondary tariffs, and provide military assistance to Ukraine through NATO, including "Patriot" air defense missiles. However, Russia has already assembled 160,000 elite troops, planning to focus on key fortresses on the Donbas front. Meanwhile, Ukraine has not been idle, conducting a large-scale drone attack on Moscow airport on July 21. Additionally, Russia announced its withdrawal from a military cooperation agreement with Germany that lasted thirty years, completely rupturing Russo-European relations.

From the current situation, achieving a ceasefire by September 2 seems difficult. If a ceasefire is not reached, Trump's sanctions could potentially trigger market turbulence.

V. Crypto Regulatory Framework Takes Shape, Industry Enters Policy Honeymoon Period

The US GENIUS Act has been implemented in July 2025, stipulating that "no interest shall be paid to token holders, but reserve interest belongs to the issuer and its purpose must be disclosed". However, it does not prohibit issuers from sharing interest earnings with users, such as Coinbase's USDC with 12% annual yield. The restriction on paying interest to token holders limits the development of "yield-bearing stablecoins", originally intended to protect US banks and prevent trillions of dollars from flowing out of traditional bank deposits that support loans to businesses and consumers.

The US CLARITY Act clearly defines SEC regulation of security tokens and CFTC regulation of commodity tokens (such as BTC, ETH). It introduces the concept of a "mature blockchain system", enabling regulatory conversion through certification - decentralized, open-source blockchain projects that run automatically based on preset rules can be certified (by submitting proof of no centralized control) and transition from "securities" to "commodities" regulation, with CFTC gaining full regulatory authority. Additionally, it provides partial exemptions for DeFi - activities like code writing, node operation, frontend interface provision, and non-custodial wallets are typically not considered financial services and are exempt from SEC regulation, only needing to comply with basic anti-fraud and anti-manipulation provisions.

Overall, the accelerated advancement of the GENIUS Act, CLARITY Act, and Anti-CBDC Surveillance State Act marks the US crypto regulation moving from a "regulatory gray area" to a "sunshine regulation" era. It also reflects the policy intent of "maintaining the US dollar's global trade currency status". As the regulatory framework gradually improves, the stablecoin market scale is expected to expand further, with compliant stablecoin projects and DeFi protocols benefiting.

VI. "Coin-Stock Strategy" Activates Market Enthusiasm, Sustainability Remains to be Observed

As MicroStrategy completes an epic transformation with its "Bitcoin strategy", a crypto asset reserve revolution led by listed companies is sweeping the capital market. From ETH to BNB, SOL, XRP, DOGE, HPYE, TRX, LTC, TAO, FET, and over a dozen mainstream Altcoins are becoming new anchors for corporate treasuries, with this "coin-stock strategy" becoming this year's market trend.

Analyzing this capital alchemy using MicroStrategy's "triple flywheel":

Stock-Coin Resonance Flywheel: Stock price is long-term premium relative to net asset value (currently 1.61x), creating a low-cost financing channel; fundraising → BTC accumulation → pushing up coin price → amplifying per-share gold content → feeding back valuation, forming a spiral upward closed loop.

Stock-Debt Synergy Flywheel: Zero-interest convertible bonds cleverly transform debt pressure, with no principal repayment burden and conversion rights in the company's hands; attracting hedge fund arbitrage capital and injecting low-cost liquidity.

Coin-Debt Arbitrage Flywheel: Replacing depreciating fiat debt with appreciating crypto assets, completing long-cycle arbitrage layout.

Moreover, using a tiered sales strategy precisely captures three types of capital: preferred stocks lock in fixed-income investors, convertible bonds attract arbitrage funds, stocks carry risk gaming. Specific logic can be referenced in 《Understanding MSTR MicroStrategy's Bitcoin Strategy in One Article》.

This year, more listed companies are adopting the "coin-stock strategy" (configuring crypto assets as reserve assets on their balance sheets), with continuously expanding reserve scale and increasingly diversified asset allocation. According to incomplete statistics: 35 listed companies collectively reserve over 920,000 BTC; 13 listed companies collectively reserve over 1.48 million ETH; 5 listed companies collectively reserve over 2.91 million SOL. Other details will be elaborated in the next article.

The integration of traditional finance and the crypto world is a unique market variable in this cycle. When listed companies transform their balance sheets into crypto asset platforms, we must also be wary of risks when the tide recedes.

Summary

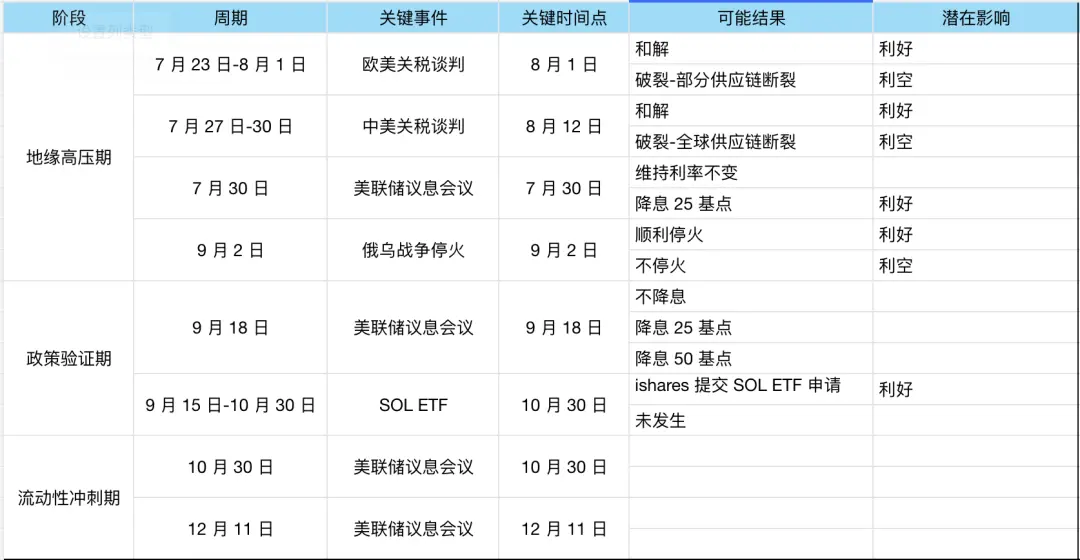

If these foreseeable macro events are projected chronologically, the second half of the year can be divided into the following stages:

Graphic: IOBC Capital

The market is like a vast ocean; we cannot predict storms, we can only adjust our sails in the storm.