The excitement over the US dollar stablecoin has not yet ended, and the craze for tokenization of US stocks has quietly emerged.

While you are still marveling at the fact that Apple stock can be bought on the blockchain, the U.S. financial system has already been quietly implanted into your wallet.

Tokenized U.S. stocks seem to be just a new technology trend: open 24 hours a day, low threshold, divisible and combinable. But what you really get is much more than these conveniences. You have obtained a complete set of "financial operating systems" led by the SEC, practiced by Wall Street, and polished over the years - regulatory logic, compliance standards, and information disclosure systems, all embedded in the back of these on-chain tokens through program code.

Stablecoins output U.S. dollar credit, while the tokenization of U.S. stocks outputs the U.S. regulatory system itself.

You no longer need a US ID or a Nasdaq account. You only need a wallet address and USDC to buy AAPLx and TSLAx at 3 a.m. However, while enjoying this "global liquidity dividend", it also means that global capital is increasingly operating on the track of rules set by the United States.

This is not a conspiracy, it is an open conspiracy.

The tokenization of U.S. stocks appears to be a technological innovation, but in essence it is an institutional output; it appears to be an open market, but in reality it is using "regulatory compliance" as a banner and "trust and transparency" as bait to siphon attention, asset flows, and the right to redistribute financial sovereignty on a global scale.

This is an expansion without war, a global credit conquest accomplished in the name of compliance.

1. Tokenized assets: turning US stocks into global "programmable assets"

What is the tokenization of US stocks? Simply put, it is to "package" the income rights, dividend rights, and even some governance rights of US stocks into tokens and issue them on the chain through blockchain technology through a special purpose vehicle (SPV) or custodian.

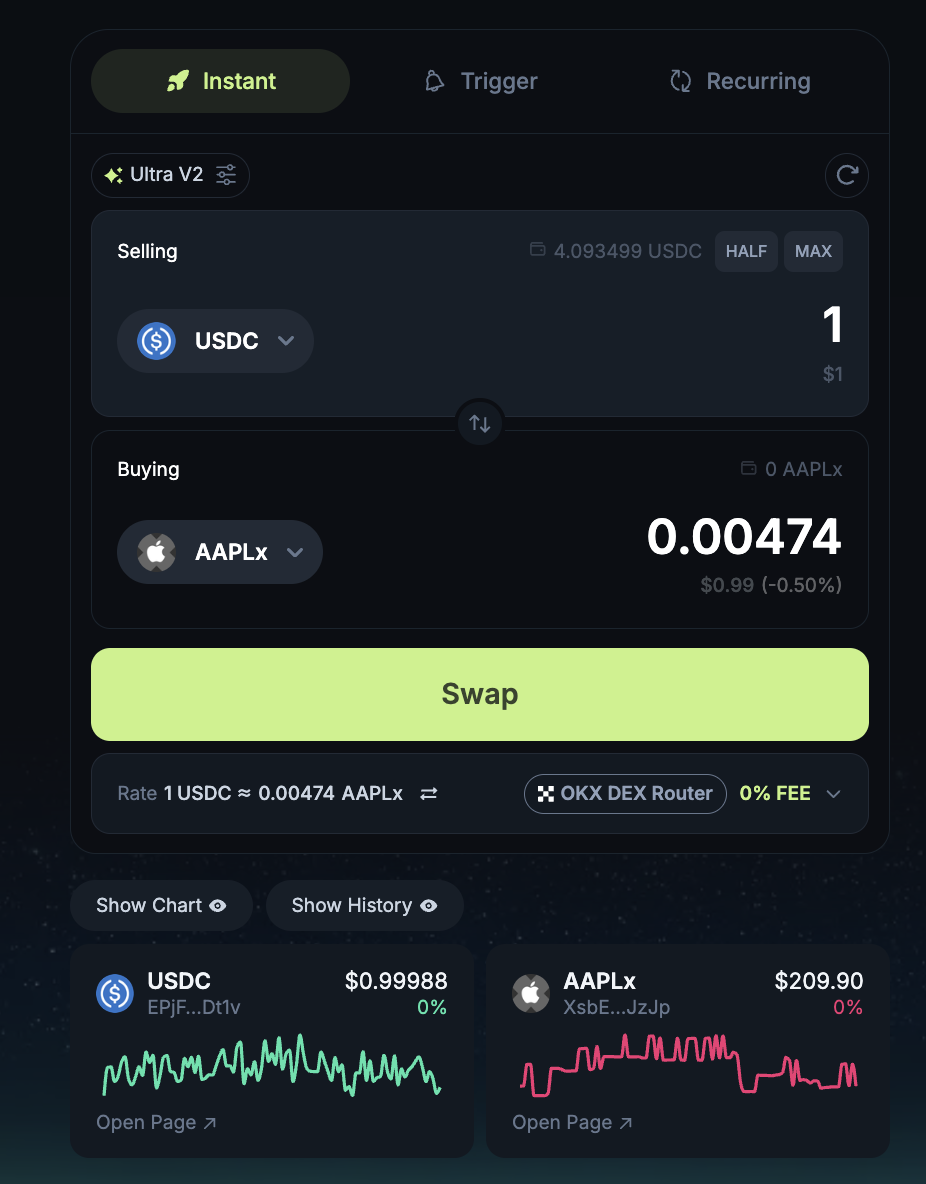

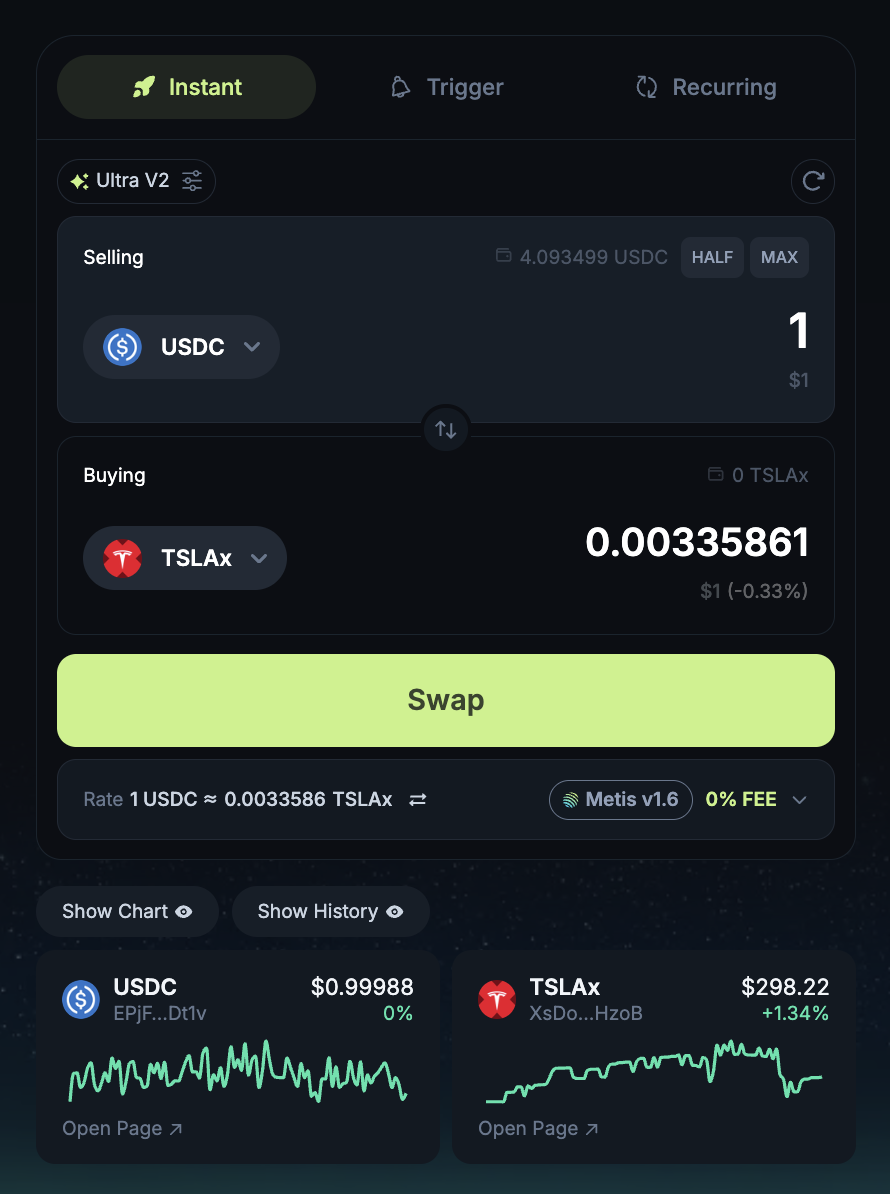

Specifically, you can now buy 0.0047 APPLx on Jupiter with 1 USDC. APPLx is a tokenized representation of Apple stock on the Solana chain, which corresponds to the real-world Apple stock held on your behalf by an SPV custodian.

The generation process of this APPLx (Tokenized Apple Stock) token is actually a combination of cross-border compliance + technology mapping, covering three links: traditional finance, digital asset custody, and blockchain issuance. The overall process is as follows:

- Real-World Share Acquisition First, Switzerland-based Backed Finance AG (a digital asset service provider registered by the Swiss Financial Market Supervisory Authority FINMA) purchases a certain number of Apple Inc. (AAPL) common shares on the Nasdaq open market through its partner brokers, such as Interactive Brokers LLC or other brokers licensed in the United States.

- Custody and SPV Structuring The purchased AAPL shares will not be held by Backed itself, but will be fully deposited in a regulated third-party financial institution (usually SIX Digital Exchange Custody or an equivalent custodian) and held by a specially established SPV (Special Purpose Vehicle) entity. This SPV entity is usually registered in Liechtenstein or Zug, Switzerland, with an independent legal status. Its only responsibility is to "hold and map" and not to carry out any other business activities to ensure asset isolation and legal clarity.

- Legal Disclosure (Legal Structuring & Claim Rights) Backed Finance will publish detailed legal disclosure instructions (eg ISIN mapping, token terms, prospectus under Liechtenstein TVTG/Blockchain Act) for each type of token to ensure that token holders have economic rights to the underlying assets, but do not directly have traditional shareholder rights such as voting rights. These instructions are generally publicly archived on the Backed official website or compliance disclosure platforms (such as DACS or Swiss Prospectus Register) for regulatory review and investor review.

- Token Minting on Solana Under the above compliance framework, Backed Finance will mint APPLx tokens on the Solana blockchain at a 1:1 ratio based on the number of managed assets, each representing 1 share of Apple stock actually held. These tokens are usually implemented by smart contract standards (such as SPL Token), and the initial distribution is controlled by Backed's on-chain multi-signature wallet. Coin holders receive APPLx through DeFi wallets (such as Phantom) without opening a Nasdaq account or US tax documents such as W-8BEN.

- On-chain Circulation & Redemption APPLx can be traded, split, pledged, and provide liquidity (LP) on Solana ecosystem platforms such as Jupiter Aggregator, Meteora, and Marinade Finance. If users want to redeem for real stocks (usually only for qualified investors), they need to submit KYC documents and go through Backed's redemption process, and the SPV will instruct the broker to transfer the real stocks.

This is a structure of "real stock → SPV custody → legal mapping → on-chain tokens", which emphasizes the authenticity, compliance and traceability of assets. Although the holder is not a "shareholder" in the traditional sense, through the trust structure and contractual agreement, the right to stock income is obtained, and the value of the traditional market is anchored and mapped to the blockchain world.

What does this mean?

Although you only buy a token on the blockchain, the governance logic behind it is actually defined by the US legal system.

In other words, on-chain tokens have become a "coded" expression of traditional U.S. stock governance rules.

2. Why US stocks?

Some people may ask, since tokenization is a global technological innovation, why are European stocks, Hong Kong stocks, or even Chinese A shares not leading the way?

The market has never prohibited the tokenization of stocks in other countries, not to mention that blockchain is decentralized. There is only one reason why U.S. stocks can become a pioneer in tokenization - U.S. stocks are attractive enough and many people want to buy them.

So, why are U.S. stocks so attractive?

It’s just two words: “transparent”.

Transparency is the most scarce resource in the modern financial system. The reason why U.S. stocks can form "high premium + strong consensus" among global investors is never based on sentiment, but on a complete set of extremely transparent regulatory systems.

Of course, the U.S. stock market is highly transparent. This transparency is not innate, but is guaranteed by a set of legal rules.

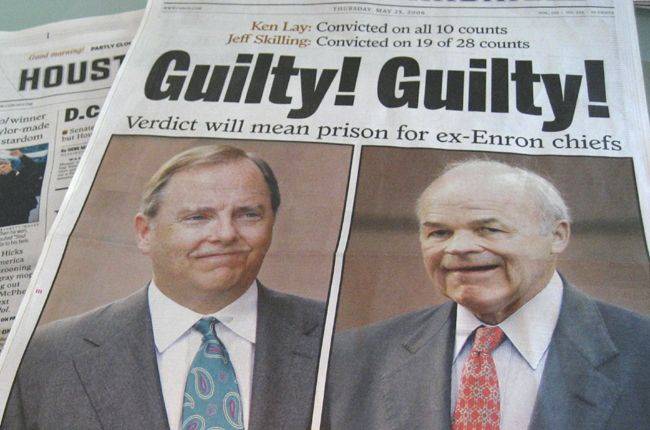

Take the Sarbanes-Oxley Act (SOX) in the United States as an example. It is an iron-blooded law introduced in 2002 after the Enron incident. It clearly stipulates:

- The CEO and CFO of a listed company must personally sign and endorse the financial figures in the annual report.

- Once financial fraud is discovered, management will face criminal liability or even imprisonment.

Such a system has greatly raised the threshold of corporate governance responsibility. Compared with the phenomenon of "high valuation + false financial reports + no consequences" in some Asian markets, the credibility of US stock financial reports has become its most hardcore selling point.

For example, the U.S. Securities and Exchange Commission (SEC) requires all listed companies to publish a 10-Q report every quarter and a 10-K report every year, covering core data such as revenue, cost, shareholder structure, and risk disclosure.

Let's briefly talk about the 10-Q and 10-K reports. These two report names sound like some kind of code names, but in fact they are indeed derived from the numbering method in US securities regulations.

What is a 10-K?

What is a 10-K?

The "10" in "10-K" refers to the form numbering system (Form 10 series) established by the U.S. Securities and Exchange Commission (SEC), while "K" is the classification code specifically used for annual reports.

The name first appeared in the implementing rules of the Securities Exchange Act of 1934. According to the rules, the SEC requires listed companies to submit a "Form 10-K" report every year to disclose the company's overall operating, financial and compliance status in the previous fiscal year.

Therefore, "10-K" actually means "Form 10 – Class K Purpose", and has become the official code for the annual report of US stocks.

What is a 10-Q?

What is a 10-Q?

Similarly, "10-Q" is the one in the "10 series of forms" that is specifically used for quarterly reports. "Q" is the abbreviation of "Quarterly". US listed companies must submit 10-Q three times a year, covering the first, second, and third quarters respectively (the fourth quarter is incorporated into the 10-K annual report for unified disclosure).

Compared with 10-K, the format of 10-Q is slightly lighter, but it still needs to follow the financial structure and disclosure elements clearly specified by the SEC to ensure that investors can make timely judgments on the company's short-term operating changes.

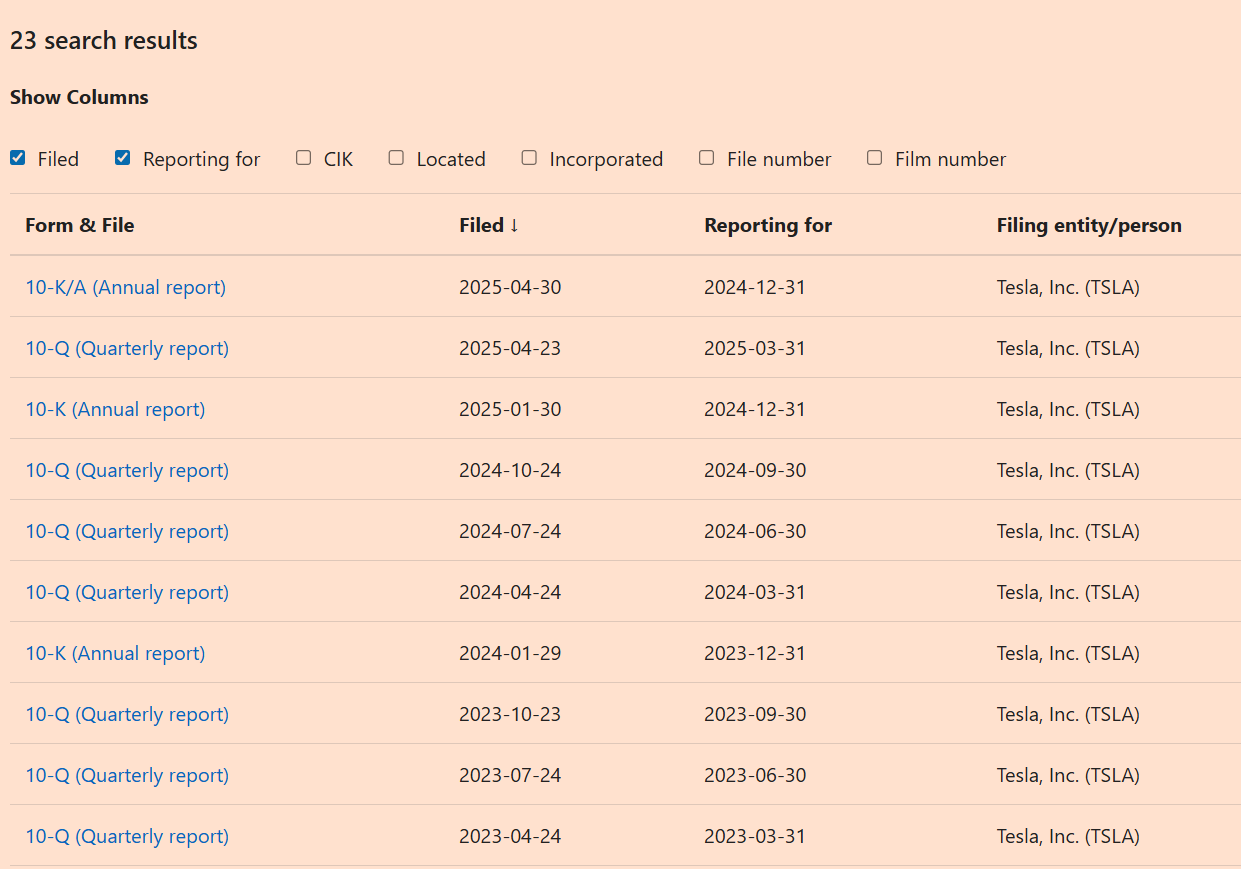

Therefore, the names of 10-K and 10-Q themselves reflect the rigor and standardization of the US securities regulatory system. Each report can be viewed in the SEC's EDGAR system ( https://www.sec.gov/edgar.shtml ), which has become one of the technical and institutional cornerstones for the US stock market to build the "highest transparency in the world".

For example, you can see all the latest 10-K and 10-Q reports of TSLA through this link.

The underlying trust built by this kind of information disclosure is exactly what the on-chain world desires.

Now, through tokenization, this "institutional transparency" of U.S. stocks is being packaged into the blockchain world in the form of "program code templates," allowing global users to enjoy the benefits of U.S.-style regulation without having a U.S. identity.

3. The “value engine” of US stock tokenization = regulatory dividend + liquidity dividend

If the global circulation of US dollar stablecoins is the output project of the US central bank to "anchor trust", then the rise of tokenization of US stocks is more like a self-fulfilling prophecy derived from market demand and feedback of regulatory trust.

The regulatory dividend of U.S. stocks is that it provides the "credibility" of assets; the liquidity dividend of the crypto market further releases the "accessibility" of U.S. stocks in the global market. The two are highly coupled through the tokenization of U.S. stocks - one is supported by compliance and the other is driven by technology. The two are mutually causal and are reshaping the basic logic of global asset allocation.

3.1 Liquidity dividend: Breaking the time and space constraints, US stocks are open 24 hours a day

In the traditional securities market, trading hours are always a natural limitation. The opening hours of US stocks are from 9:30 to 16:00 Eastern Time from Monday to Friday, which is exactly late at night when converted into Asian time. Ordinary Asian users who want to participate in the investment of popular targets such as Tesla, Nvidia, and Microsoft are often restricted by time differences, account thresholds, and even cross-border regulations.

After tokenization, everything changes.

Taking the Jupiter decentralized exchange on the Solana chain as an example, users can now use USDC to buy and sell tokenized US stocks such as TSLAx and AAPLx on the chain at any time, without any time, region or identity restrictions. The transactions of these tokens follow the AMM automatic market making logic and run 24 hours a day, without waiting for the opening, matching counterparties, or account review.

On the chain, "U.S. stocks are always open" is no longer a slogan, but a real experience.

3.2 Fragmented ownership: breaking down high barriers and increasing participation

The minimum trading unit of traditional stocks is "one share", which is particularly evident in high-priced targets. Taking the market at the end of 2024 as an example, the price of one Amazon (AMZN) share is more than $150, and the price of Berkshire Hathaway Class A shares is more than $500,000. For most small retail investors, this is almost an untouchable investment target.

Tokenization makes these assets “programmable” and “divisible”.

Tokenized U.S. stocks such as TSLAx and AAPLx can be traded with an accuracy of 0.0001 units. Users only need to hold $1 USDC to hold "0.001 Tesla stock token." This extremely fragmentable structure, combined with the global circulation capacity of stablecoins, opens up investment opportunities for billions of users around the world who have not yet been exposed to U.S. stocks.

This is not only about convenience, but also about universal participation rights. The distribution of assets no longer depends on intermediaries and account qualifications, but only on whether you have an on-chain wallet.

3.3 DeFi Integration: From “Investment Products” to “Callable Assets”

The significance of the tokenization of U.S. stocks is not only that they can be purchased on the chain, but also that it opens up the imagination boundary of real assets for DeFi.

On the chain, these stock tokens are no longer just an "underlying object", but a "callable asset component": they can be circulated, combined, and nested in various smart contracts, gradually integrating into the financial Lego system of the DeFi world.

Currently, US stock tokens such as AAPLx and TSLAx have received initial liquidity support on the Solana chain and can be traded 24/7 on DEXs such as Raydium. This also means that you can provide liquidity for TSLAx here and earn fees.

Although U.S. stock tokens have not yet been connected to lending protocols such as Kamino or interest rate protocols, there is a clear expectation in the industry: once the liquidity, custody structure and legal framework of these stock tokens are sufficiently solid, they will be able to be mortgaged, pledged, and even "split into PT (principal token) + YT (future cash flow token) structure, thereby introducing the "cash flow secondary market" of real-world assets.

For example, in the future on Rate-X, users may tokenize and package TSLAx dividend income and sell it in the form of YT, thereby exchanging for liquidity in advance - and this entire process will not require approval from the shareholders' meeting, nor will it require the signing of any offline contracts, and will be completely automatically executed and settled by smart contracts.

This is the greatest charm of the combination of tokenization and DeFi: it is not simply putting stocks "on the chain", but making stocks an asset module that can be combined, called, and nested, thereby releasing structural innovation capabilities that traditional finance does not have.

Of course, it’s still early days, but the direction is set. With platforms like Dinari and Backed Finance advancing compliance and asset custody transparency, we are witnessing an experiment on how traditional assets can be embedded in an open financial system gradually becoming a reality.

3.4 “Private Access” to the Primary Market: First Circulation of Unlisted Equity

Robinhood EU has further broken the monopoly of the primary market in its recently launched tokenized equity service in the EU. In addition to traditional US stocks such as Apple and Google, it has also launched tokenized equity of OpenAI and SpaceX. Users can get economic exposure to these star unlisted companies through USDC for only tens of dollars.

Although this practice is still subject to legal controversy (OpenAI has publicly stated that it is "unauthorized"), the trend it reflects is extremely clear: private equity will no longer be an area that only venture capital and family offices can access, but is becoming an "asset class that can be accessed on the chain."

This means that the on-chain “pre-IPO market” may be earlier, more transparent, and have a better pricing feedback mechanism than a real IPO.

3.5 Summary

The real value of U.S. stock tokenization lies not in “moving stocks onto the blockchain”, but in:

- U.S. securities regulation provides a credible “trust template”;

- Blockchain provides a "global interface" that can be infinitely replicated, fragmented, and combined.

The regulatory dividend makes people believe that this is a real, redeemable asset; and the liquidity dividend turns it into a sleepless, composable, and interest-bearing "new type of financial Lego."

This is why the world is embracing the tokenization of U.S. stocks. This is not a technological revolution, but an institutional evolution about "how to expand value trust."

The above are all good things about the tokenization of U.S. stocks. However, you must not forget that although this new path is dazzling, it is not without pitfalls.

4. Don’t forget the risks of centralization

You may think that the tokenization of U.S. stocks is a brand new thing. But in fact, this game has been quietly played in the chaos of the crypto three years ago.

In April 2021, the popular FTX launched a U.S. stock tokenization product called FTX-CM Equity. This product claims to be able to trade on the chain 24/7, and even offers a seemingly reliable promise of "redeemable for real stocks at any time."

However, when FTX collapsed in November 2022, people were shocked to find that behind these seemingly regular and redeemable tokens, there was not even a complete custody certificate. These "on-chain US stocks" held by investors instantly became "digital shells" that could not be exchanged for real stocks. In just one night, the on-chain assets of countless investors disappeared out of thin air.

What’s even more ironic is that FTX’s original promotional copy clearly stated “compliant custody” and “transparent settlement”. This is like you happily bought a luxury villa, but found out that the owner’s name on the property certificate is not yours at all.

FTX’s case is not an isolated one. The currently popular US stock tokenization platform xStocks has also fallen into a similar crisis of trust.

At the end of 2024, the tokenization of U.S. stocks became popular, and crypto trading platforms such as Kraken and Bybit chose xStocks' infrastructure and issued tokenized products for popular stocks including Apple (AAPL) and Tesla (TSLA).

But xStocks’ dark history makes people worry. In June 2024, xStocks was exposed by the media: its early team members had participated in the notorious DAOstack project, which had aroused widespread community doubts due to the opaque distribution of governance tokens and the “soft rug pull” of the founding team.

I’m not saying xStocks will necessarily go the way of FTX, but the point is: why should you trust it?

Centralized institutions inherently have trust loopholes.

History tells us that it is difficult for centralized institutions that are not subject to regulatory constraints to resist the temptation to "do evil." The reason why Nasdaq and the New York Stock Exchange are trustworthy is not because they are inherently noble, but because the SEC's strict and almost harsh supervision, quarterly financial audits, and frequent and public asset reserve verifications leave these centralized platforms "no chance to do evil."

However, the particularity of U.S. stock tokenization determines that it cannot be completely decentralized - the tokens on the chain must correspond to stocks or equity in the real world. Therefore, this model is destined to rely on centralized institutions to complete key links such as asset custody, liquidation, and redemption.

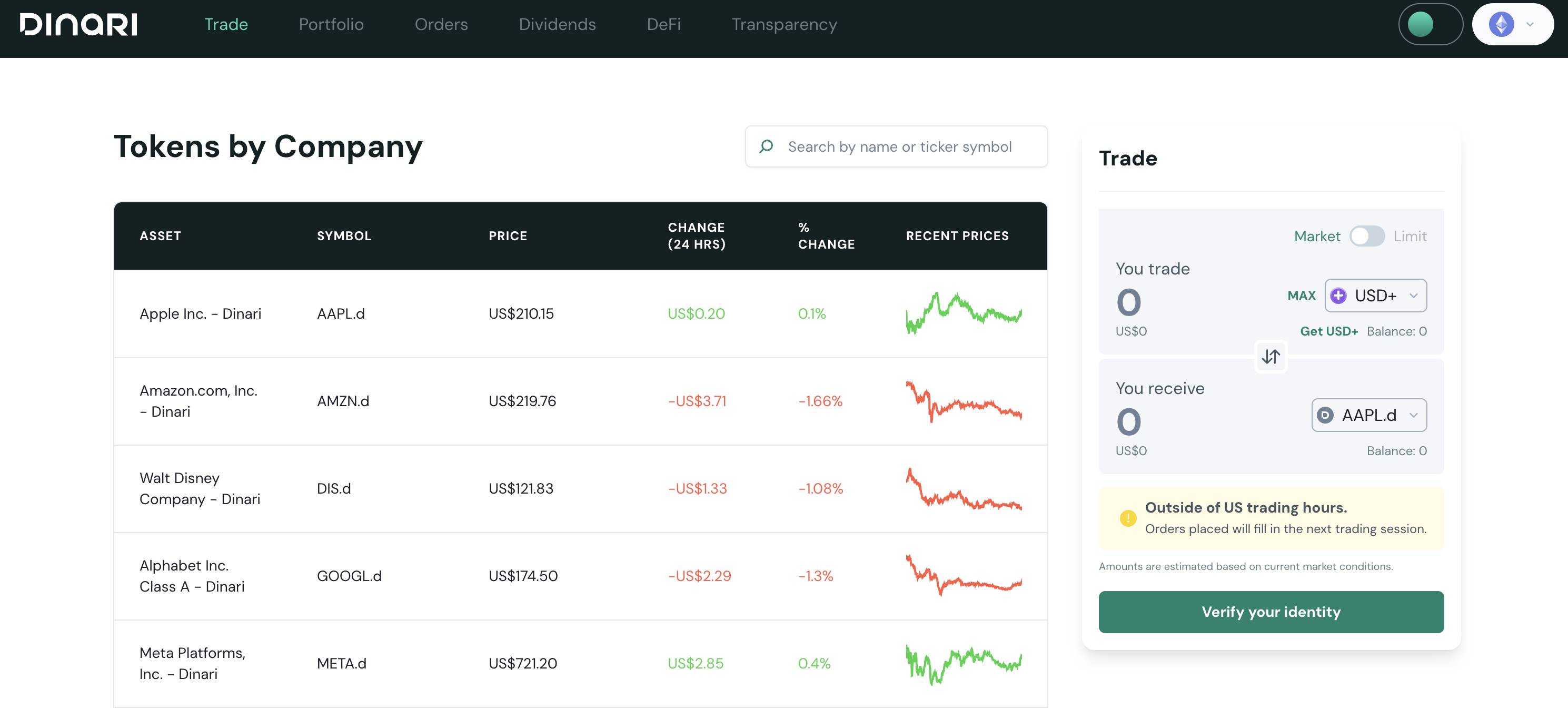

Since we cannot get rid of centralization, what we can do is to build a sufficiently transparent, strongly regulated, and verifiable trust system to ensure that the custodian cannot do evil or lose contact at will. This trust and auditable model is exactly the path Dinari is trying.

Just this June, San Francisco-based Dinari became the first U.S. stock tokenization platform to obtain a broker-dealer license in U.S. history. Obtaining this license means that Dinari must not only strictly comply with SEC trading rules (such as SEC Rule 15c3-3 asset custody and segregation requirements), but also must undergo public third-party financial audits and asset reserve verification every year.

Dinari CEO Gabriel Otte made it clear that the company's upcoming US stock tokenization business will be conducted entirely through "regulated intermediaries + blockchain real-time settlement", with asset custody and audit reports fully open and transparent. In addition, Dinari will also connect to traditional financial platforms such as Coinbase, Robinhood, and Cash App through APIs, and quickly spread the legal and compliant model reviewed by the SEC in a white-label manner.

Almost at the same time, crypto giant Coinbase is also actively promoting similar businesses and has formally submitted a compliance license application for stock tokenization services to the SEC. Coinbase's General Counsel Paul Grewal publicly stated that "the future of tokenization must be driven by regulation rather than technology. Only in this way can U.S. stocks on the chain truly be worthy of investors' trust."

The actions of Dinari and Coinbase send a clear signal: the real competition in the tokenization of U.S. stocks is not about whose blockchain technology is more advanced, but about whose compliance supervision is more transparent and stricter.

After all, the problem of centralization risk is not something that blockchain can solve by nature, and only supervision that is strong enough to be awe-inspiring is the ultimate answer.

Conclusion: Tokenization of US stocks is not about “moving it to the blockchain”, but about “implanting it in the heart”

In this era where capital and code are integrated, regulation and protocols are quietly merging. The tokenization of U.S. stocks is not only an evolution of asset forms, but also an expedition of the trust system.

This expedition does not require a fleet or rely on military force, but uses code as a boat and the system as a sail to engrave "verifiable transparency", "enforceable rules" and "inheritable trust" into the on-chain world.

What we see is not a simple "on-chain" but a silent institutional expansion - the American financial logic, with governance as its banner and compliance as its justification, has spread digital estates on the borderless land of DeFi.

Here, the SEC number is transformed into the consensus instruction of the smart contract, and the KYC process is embedded in the signature authority of the wallet. The trust that originally belonged only to Wall Street can now take root in any decentralized wallet.

This is the true face of the tokenization of US stocks:

It does not turn stocks into program codes, but transforms institutions into consensus, casts trust into liquidity, and compresses financial governance into a series of portable civilization modules.

When the control of assets is no longer determined by brokers, but by code; when the boundary of trust is no longer the national border, but the thickness of compliance standards——

We can finally say:

The tokenization of U.S. stocks is not the end, but the prelude to the reconstruction of the global financial structure and the silent expansion of "code civilization."