Written by: Saurabh Deshpande

Compiled by: TechFlow

Hello,

I hinted at the beginning of the year that we would be building a liquidity position from our balance sheet and over the past few weeks we have been steadily building our Hyperliquid position.

This is in sync with our ongoing exploration of speed , margins , revenues and business models . Saurabh’s post today explains why we invested in Hyperliquid.

For the sake of disclosure, we have not contacted anyone at Hyperliquid at the time of writing. No marketing managers were harmed at the time of writing. We will continue to invest, co-build, and research the future of the on-chain development market. Our thesis is that given Hyperliquid's ability to attract venture capital, it will become the dominant way to build applications in the coming months.

Long before the word “blockchain” was coined, merchants used a shared infrastructure called the Silk Road. Although the route had existed for centuries, it was considered dangerous and inefficient. Local warlords collected tolls, bandits attacked caravans, and merchants had to deal with dozens of different legal systems and currencies. Each trading post operated independently, hoarded information, and charged fees based on what the market would bear.

During the Mongol Peace, Genghis Khan improved the business environment by unifying the fragmented TechFlow Road. An Eastern European merchant could now travel to China without fear for his life. Moreover, he could do so under a unified legal framework, using standardized weights and measures and protected by the same security forces. The Mongols established a system called "Yam " , a TechFlow network of post stations, horses and sealed imperial plaques. This enabled merchants to cover greater distances and improved the transportation of goods.

Yams act like nodes that are easily replicated. It creates a network effect, making the entire system stronger with each new participant. The more merchants that use the routes, the greater the security, the more reliable the service, and the lower the cost for everyone. The Mongol trade network lasted for centuries, enabling one of the greatest transfers of knowledge, technology, and culture the medieval world has ever seen.

This is how humans have always solved the problem of scaling commerce: by building shared infrastructure that gets stronger with each new participant. Later great inventions, like spinoffs of the Silk Road, helped us do business more efficiently. With the advent of steamships, telegraphs, and container ships, we reduced the cost of shipping goods by a few basis points, bringing it closer to zero. Today, even in digital finance, the transfer of value relies on networks whose fundamentals remain unchanged.

There is a simple truth in financial markets: money needs to flow, and it needs to flow efficiently. Joel has already explored this in the book "Money Flows" . The blockchain world has been building technology stacks for years, but has largely ignored this basic principle. Most DeFi protocols are launched with great fanfare, attract some initial liquidity during the incentive period, and then watch users and trading volume move to the next hot project that offers higher returns. This is a predictable pattern in the DeFi space.

Traditional finance is not accessible to the masses. But those with access can gain leverage, thereby increasing profits. Behind the gated glass doors of banks and prime brokers, dollars are rehypothecated across different trades. The same collateral is used for different positions. As a result, the utilization of the entire engine is close to 100%. But only a few institutions have access to these controls.

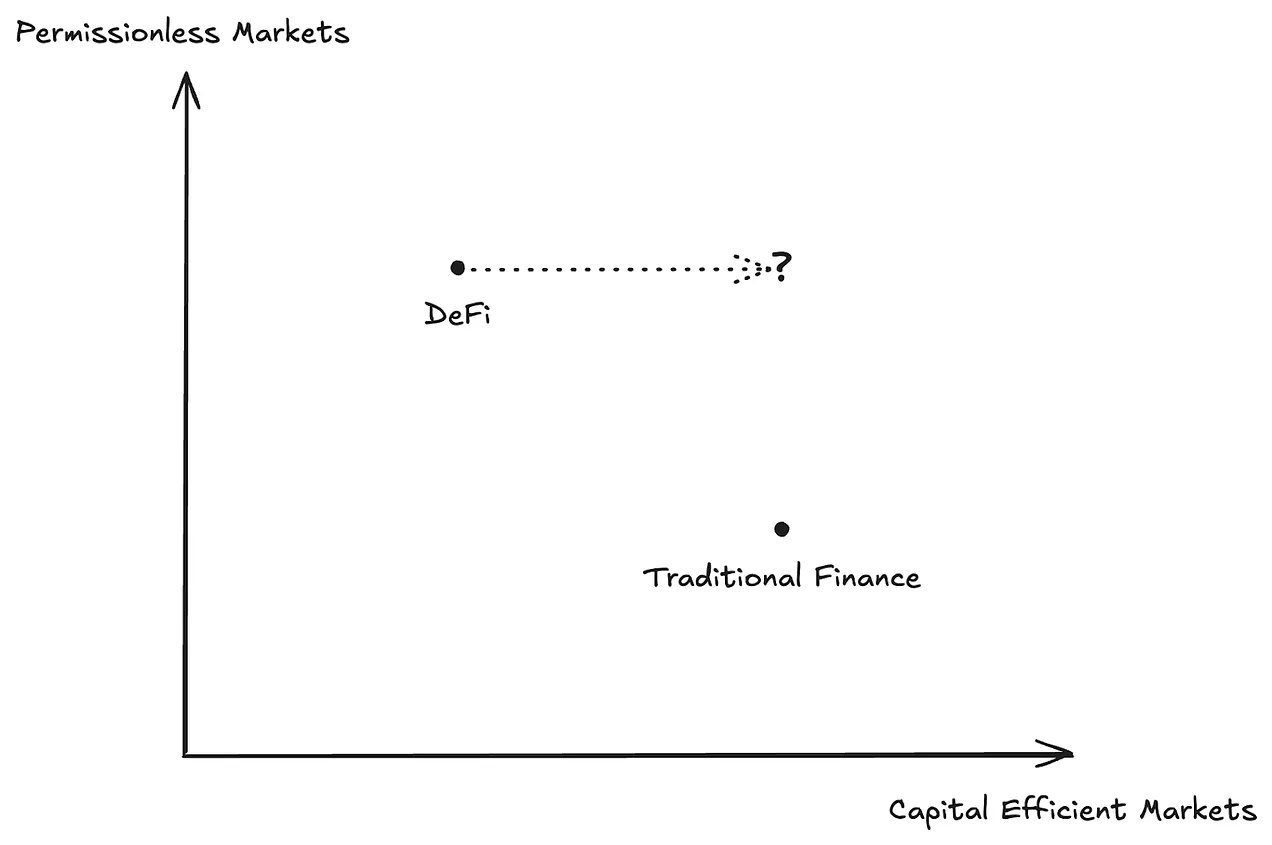

DeFi opens these doors wide: anyone with a browser can borrow, swap, or hedge. But the price of openness is stranded collateral. Siloed margin accounts, overcollateralized loans, and liquidity pools that can’t communicate with each other. In the “Permissionless Markets vs. Capital Efficient Markets” chart below, traditional markets are squatting in the bottom right, DeFi is hovering in the top left, and the top right is still empty. Hyperliquid’s bet is to plant a flag in this void. This is important because if financial institutions are going to use blockchain infrastructure, they won’t use it because it provides permissionless access. They want a system that is as efficient as the one they already have. Without institutional adoption, crypto won’t be able to start its next phase of growth.

Our previous article on Hyperliquid focused primarily on exchanges. This article will explore the Hyperliquid ecosystem and how it attempts to change DeFi’s funding efficiency and liquidity.

Hyperliquid’s bet is that “less is more”, that by reducing distractions and unnecessary actions, wealth can be better accumulated and grown. And, crucially, it will bring its friends along. Hyperliquid isn’t trying to be a general-purpose computer or a metaverse theme park. It’s trying to be Manhattan’s financial district, crammed into a single matching engine.

The question is, can Hyperliquid turn an exchange into a gravity sink so dense that capital can’t escape? The answer lies in two intertwined ideas: how quickly value can circulate, and how hard it is for value to escape.

Fund transfer

First, blockchain is about money. This may sound obvious, but it’s worth examining what “moving money” actually means in practice. The Silk Road was successful because it made trade easier, faster, and more secure than it would have been otherwise. But it was not unique. Many people throughout history have accumulated wealth by controlling integrated infrastructure networks.

The Rothschilds made their name in financial services, but their business was built on the powerful information networks of 19th-century Europe. While other financiers had to wait days for news via horses and ships, the Rothschilds used carrier pigeons, private couriers, and strategic telegraph investments to deliver market intelligence within hours. The family later invested in railroads across Europe, not for the transportation revenue, but because railroads were the arteries of 19th-century commerce. Whoever controlled the railroads controlled the economy.

J.P. Morgan Chase in the United States took a similar approach. He financed railroad construction and organized industry around it. He consolidated competing rail lines into an integrated network, standardized track gauges so trains could actually connect, and eliminated redundant lines. When Andrew Carnegie needed steel shipped from Pittsburgh, he chose to ship it through Morgan's railroads. When John D. Rockefeller needed oil shipped from Pennsylvania to a refinery, he chose to make a deal with Morgan's railroad empire.

Morgan’s real innovation was the vertical integration of the infrastructure itself. He controlled the steel companies that built the railroads, the banks that financed the expansion, and the railroads that moved the goods. It became almost a circulatory system for American capitalism. By the time he had it all done, you couldn’t move money, materials, or information within the United States without paying Morgan a fee somewhere in the chain.

Any chain that enables capital to flow smoothly between its parts has inherent advantages.

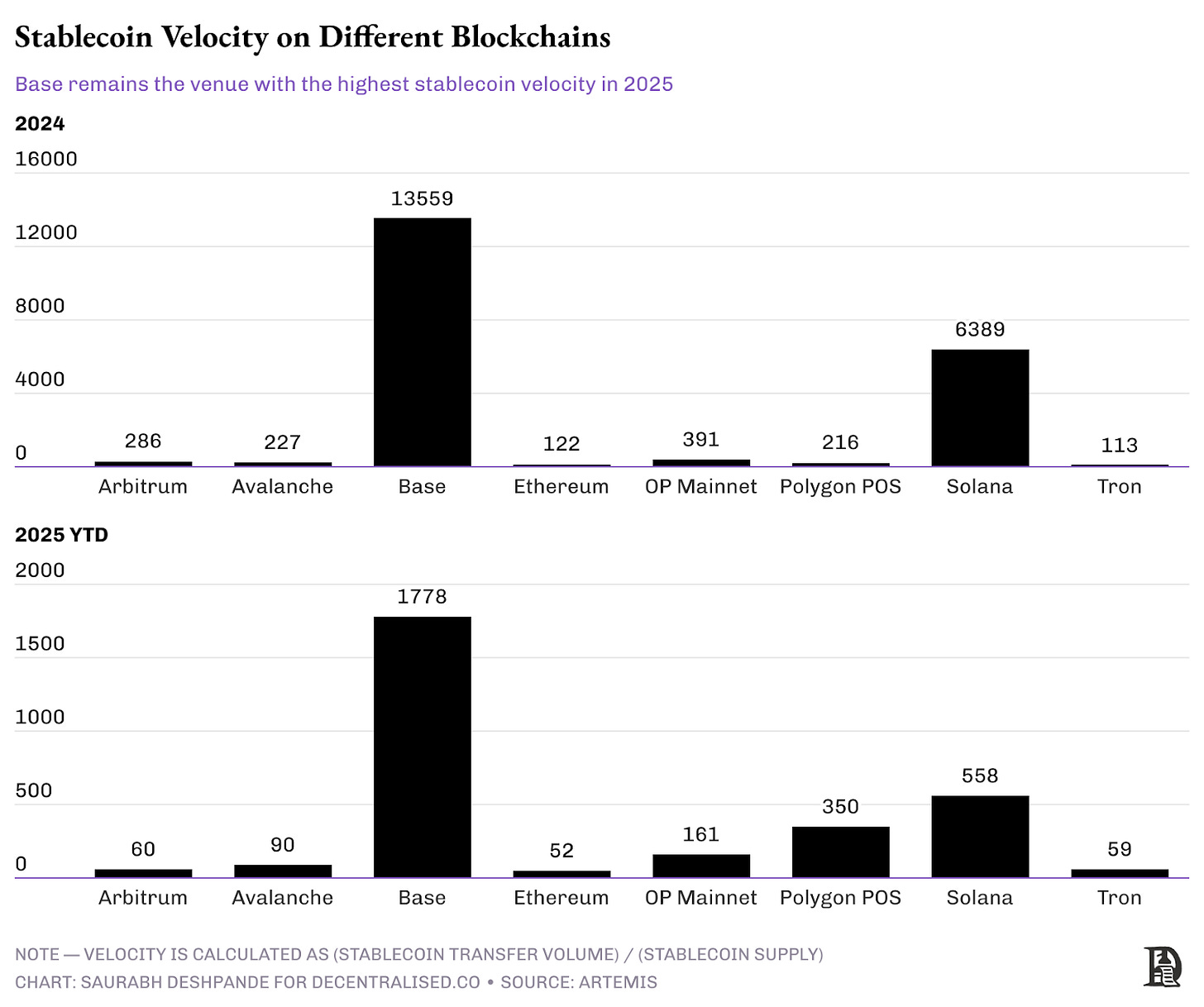

Stablecoins have become the killer app for cryptocurrencies. As of June 22, Ethereum, Solana, and Tron have moved $12.2 trillion worth of stablecoins in 2025. Each major blockchain has found its niche in how stablecoins are moved. Tron has become the dominant network for payments in emerging markets, while Ethereum handles larger institutional transfers and Solana excels at high-frequency, small transactions.

Solana became the go-to platform for memecoin trading in 2024. This is reflected in Solana’s stablecoin transaction velocity. With a stablecoin supply of only $1.8 billion, Solana settled $11.5 trillion worth of stablecoins. In other words, each stablecoin was traded over 6,300 times. With the rise of AI agents, trading activity on Base has also risen. Stablecoin transaction velocity in 2024 was too high due to the low supply. But Base was the only chain that settled more stablecoins among the choices. In 2025, the number of stablecoin transactions on Base exceeded 1,700.

These numbers show that money behaves differently when fees are close to zero. On Ethereum, when a transaction costs $10, it’s unlikely that small traders will regularly put in $50 or $100. But on Solana, we see this regularly, with fees under a penny. Exchanges, liquidity providers, and MEV extractors make money from fees and slippage. Validators make money from bribes from MEV extractors. Instead of making high profits on a small number of trades, you make small profits on huge volumes. When friction disappears, speed is everything.

On-chain activity can be divided into two parts - high-value activity (such as Ethereum, due to its high liquidity) and low-value but high-frequency activity (such as Base and Solana). Is it possible to have both activities on the same chain? Hyperliquid's approach is interesting. Its ecosystem is not optimized for a certain type of capital flow, but provides infrastructure for all types of capital flows.

The Hyperliquid ecosystem consists of two parts.

Hyperliquid DEX is powered by HyperCore, a native L1 order book system, and

HyperEVM is a high-performance EVM-based blockchain built by the Hyperliquid team.

While both are building blocks, precompiled and builder code are the distribution mechanism.

Precompiled smart contracts are specialized smart contracts that connect HyperEVM and HyperCore to enable smooth data access and execution across environments. These contracts enable developers to directly access trading data such as perpetual contract positions, spot balances, value equity, oracle prices, and pledge delegation.

A builder code on Hyperliquid is a referral-like identifier that developers can use when building applications or tools on the platform. When users interact with Hyperliquid through their application, such as a trading bot or interface, the developer's builder code is rewarded. This enables them to earn a share of the trading fees generated by users. This creates a direct path to profitability for developers who build valuable tools and applications in the Hyperliquid ecosystem.

Improve capital efficiency

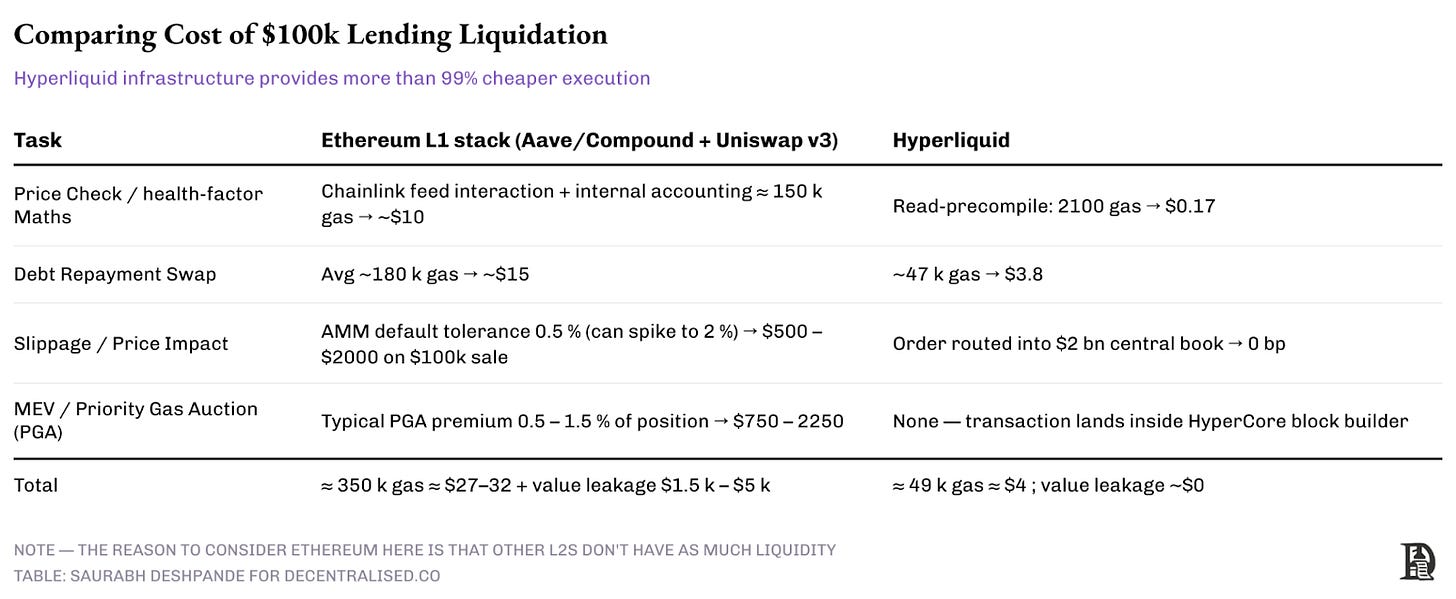

Traditional DeFi lending protocols are extremely inefficient when managing collateral positions. On Ethereum-based platforms like Compound or Aave, liquidating a $100,000 USDC loan backed by $150,000 worth of ETH requires performing multiple expensive operations:

Oracle price calls consume 80,000 gas ($10-30),

External DEX swap costs 150,000 gas ($15-50 USD), and

Slippage loss due to AMM mechanism is 0.5-2% ($500-2000)

Front-runners extracting MEV add another ~1% value loss, typically resulting in a total inefficiency of $500-3,000 per liquidation.

Hyperliquid’s precompile functionality eliminates these inefficiencies by directly integrating the order book. Lending smart contracts can read prices directly from the HyperCore order book using the read precompile function and send liquidation orders directly by writing to the system contract HyperEVM. The same $100,000 liquidation scenario only requires 2,100 Gas to obtain price data and 47,000 Gas to execute. This significantly reduces costs compared to traditional Ethereum-based protocols while eliminating slippage by accessing over $2 billion in order book liquidity.

The result is that while clearing $100,000 through lending applications on Ethereum costs about $27, plus value leakage through MEV (about $15,000), it costs less than $5 on Hyperliquid.

Agreement-based clearing

Precompilation supports protocol-based liquidation, where the lending protocol implements an automatic liquidation mechanism similar to the perpetual contract system on HyperCore.

In traditional finance, when you can’t afford the margin, your broker will immediately sell your shares at the market price. This is convenient and does not cause any value loss because they have direct access to the deep market.

In most DeFi protocols, the situation is more complicated. When your loan goes bad, the protocol has to find someone willing to liquidate you, and then hope that they can sell your collateral on multiple different exchanges without losing too much due to slippage. It's like having to sell your house through a series of middlemen instead of directly on the market.

Hyperliquid operates more like traditional finance. When your collateral drops too low, the smart contract sells it directly into a deep order book that processes billions of daily trades. Your position is closed at a fair market price without having to find anyone to assume your loan and leak the value.

This architecture improves capital efficiency at the protocol level. Traditional DeFi protocols maintain separate liquidity reserves and typically offer 75% loan-to-value (LTV) ratios due to execution risk. Ultra-liquidity-based lending protocols can eliminate the buffer and offer LTV ratios of over 90% because liquidations are executed with deep liquidity guaranteed. This allows users to deploy capital 20-25% more efficiently while maintaining the same risk profile. The result is a unified liquidity layer where every DeFi protocol has access to institutional-grade execution capabilities with full transparency and composability.

Liquidity as a moat

Liquidity is the soul of financial applications. If your product is great but lacks liquidity, it is not a product. In traditional DeFi applications, liquidity is mostly a zero-sum game. DeFi is composable to a certain extent, but we have not really unified liquidity yet. When one platform has liquidity, other platforms lack liquidity.

There is a problem with blockchains like Ethereum: when Aave needs to liquidate a large position, it must split it into multiple blocks (which makes Gas less efficient) in order to obtain liquidity from different platforms, or risk slippage. As mentioned earlier, for a $100,000 liquidation, Ethereum typically ends up paying $1,000 to different intermediaries. Because of this, projects are forced to integrate with multiple external DEXs, which increases complexity, Gas costs, and execution risk, while still not guaranteeing optimal pricing.

On the surface, this is just a liquidity problem. But it can spill over and take up scarce resources from the team. Ultimately, poor execution is bad for the protocol. As a result, founders end up spending their valuable time on activities that are not core to their business. If you are a lending protocol, one of your core goals is to grow loan size. Of course, how to liquidate bad debts is also important. But if there is a better way to access large liquidity pools, it means you don’t have to bother finding the optimal way to liquidate risky positions; you can spend your time on development, not maintenance.

New protocols often launch with minimal liquidity, creating a “chicken and egg” problem where traders avoid the platform due to poor execution, which in turn prevents liquidity providers from earning the fees they deserve.

It often makes sense to look back at how our traditional financial system solved these problems. Stock exchanges like London, New York, and Mumbai ultimately won out because everyone traded there. There was no L2 to segment users, nor the liquidity that L2 brings . Network effects in finance are particularly powerful because they have a compounding effect: more participants mean better prices, which attracts more participants, ultimately creating better prices.

Hyperliquid is addressing this by increasing liquidity collaboration. Do you think your application can bring liquidity and want to benefit from it?

Hyperliquid's builder code is a permissionless fee-sharing mechanism that enables DeFi developers to earn revenue from transactions performed by their applications. They are trying to solve this problem by giving all applications access to the same unified liquidity pool of over $2 billion, avoiding fragmentation. Hyperliquid is one of the most liquid exchanges not only in the DeFi space, but also in the cryptocurrency space. All projects built on HyperEVM can easily tap into this liquidity.

Applications built with builder code do not compete for liquidity, but instead contribute to and benefit from a shared liquidity layer. When users trade through any builder code application, they access the same deep order book as the Hyperliquid core exchange. This applies to mobile wallets, trading bots, and complex DeFi protocols.

This architecture means that newly launched lending protocols do not need to build their own liquidity or integrate with multiple external decentralized exchanges (DEX). Lending smart contracts can use pre-compiled mechanisms to read prices directly from the HyperCore order book and send liquidation orders directly by writing to the system contract , thereby gaining instant access to institutional-grade liquidity depth. The protocol benefits from the same liquidity that serves billions of daily transactions, ensuring efficient liquidation regardless of the establishment time or scale of the protocol.

Builder Code Network Effect

In most DeFi ecosystems, new applications are like new restaurants opening on the same street. They compete for the same customer base and carve up the existing pie. On Ethereum or Solana, when a new DEX comes online, it must convince users and liquidity providers to leave Uniswap or Raydium. It’s a zero-sum game: one application’s gain is another application’s loss.

The builder code turns this on its head. Every new app on Hyperliquid actually strengthens the entire ecosystem, like adding a store to a shopping mall. When a new trading bot comes online and brings 1,000 active users, those users add volume to HyperCore’s liquidity pool (which all other apps use). More volume means better prices for everyone. Lending protocols get stronger execution, derivatives platforms get tighter spreads, and even competitor trading bots benefit from deeper liquidity.

This is a positive-sum game because when shared infrastructure becomes more powerful, everyone wins. Rather than competing for a fixed share, each new participant contributes to a larger pie for everyone else.

Since liquidity can now be achieved with just a few lines of code, the quality of the application becomes even more important.

This dynamic reverses the status quo of traditional DeFi liquidity fragmentation. Instead of launching with empty order books or extremely low AMM liquidity, these protocols immediately inherit the execution quality of the entire Hyperliquid ecosystem. Derivatives trading applications launched today can provide the same low spreads and deep liquidity as mature protocols, eliminating the typical entry barriers faced by existing platforms.

The unified liquidity model also enables complex cross-protocol interactions that were previously impossible. Decentralized hedge funds can execute complex multi-asset strategies across different builder code applications while maintaining consistent execution quality because all trades are ultimately settled based on the same order book.

This reminds me that every factory was once half a power plant. Since electricity could not be transported, it had to be produced inside the factory. The factory had to install steam engines, add coal to the boilers day and night, and pull intricate belts to the huge overhead drive shafts. A large part of the workers were adding coal, tightening pulleys, and oiling bearings all day long. This work could only keep the lights on in the factory, but it could not improve the quality of the products on the production line.

Then came the advent of the public AC grid and small electric motors. Factories could now buy kilowatt-hours of electricity like they bought water. Maintenance staffs were reduced; plant layouts became flexible; and management's focus shifted from "maintaining boiler pressure" to "how do we double production?"

Builder codes do the same thing. They free developers from the constraints of acquiring and managing liquidity. They can prioritize user experience and focus on building applications with great experiences.

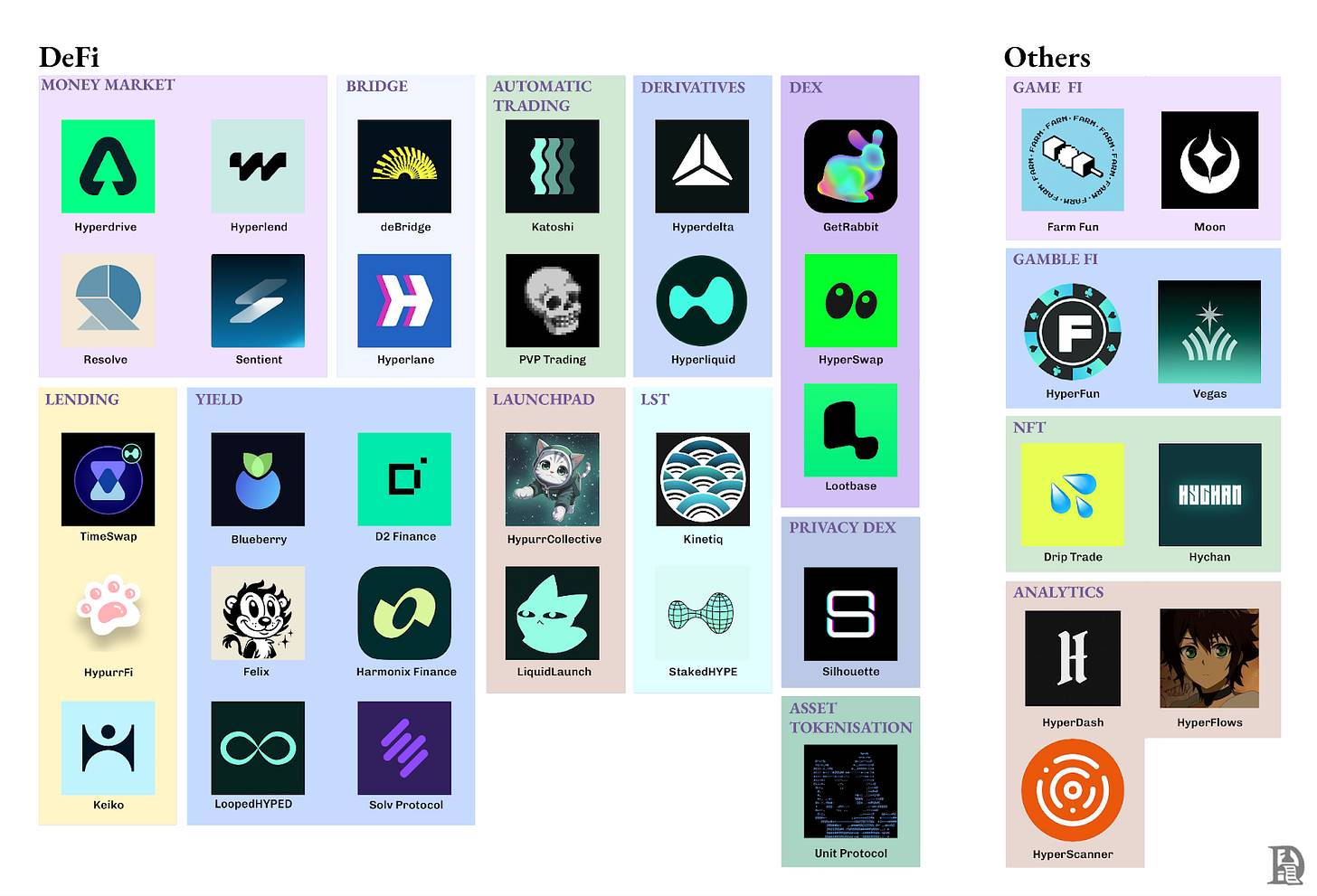

HyperEVM Ecosystem

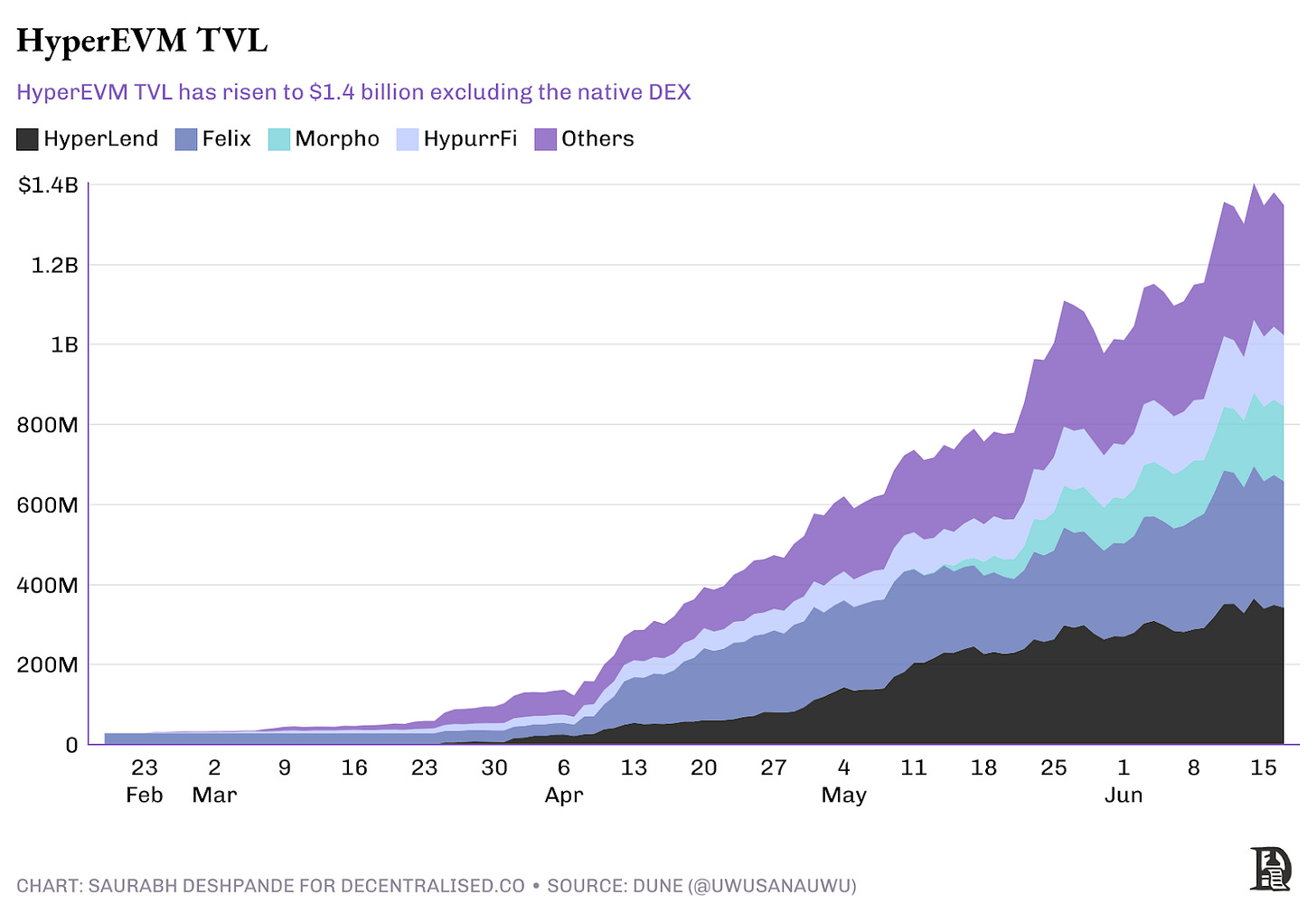

The HyperEVM ecosystem has rapidly grown into a comprehensive DeFi infrastructure with a total value of over $1.5 billion and covering more than 100 projects. HyperEVM uses the same HyperBFT consensus mechanism as HyperCore, allowing direct interaction with spot and perpetual contracts through precompiled and system contracts. HyperEVM | Hyperliquid Documentation . This unique architecture enables the protocol to build complex financial applications that leverage the liquidity of the native order book while maintaining full compatibility with the EVM.

NOTE – This market map is not exhaustive.

Projects range from lending markets to liquidity staking to synthetic assets. But they all benefit from the same unified liquidity layer. Applications in different industries are being built on Hyperliquid.

Loans and Money Markets:

HyperLend ($470M TVL) — The leading lending protocol with direct access to order book liquidity for instant and efficient liquidations.

HypurrFi ($319M TVL) — Home to the leveraged lending marketplace and the USDXL stablecoin, backed by U.S. Treasuries.

Unit Protocol - A bridge layer that introduces BTC, ETH, and SOL into Hyperliquid as uBTC, uETH, etc.

Felix Protocol - Multi-collateral stablecoin (feUSD), reducing dependence on external stablecoins.

Exchange:

HyperSwap and KittenSwap — AMM-based DEXs process $75 million in volume per day, and unlike major exchanges, they still need to bootstrap their own liquidity.

Liquidity Staking:

StakedHYPE - Simple liquidity staking, stHYPE automatic compounding rewards

Kinetiq - Smart validator selection system that automatically delegates to the highest performing validators

LoopedHYPE - Automatic leveraged cyclic staking income, with a potential annualized rate of return of more than 10% through 3x to 15x leverage.

The rapid growth of the ecosystem demonstrates the significant benefits of removing friction to onboarding liquidity. With the launch of the protocol and the convenience of instant access to deep liquidity, the total locked value (TVL) of HyperEVM has steadily climbed to $1.5 billion.

What does all this mean?

I think Hyperliquid has four distinct advantages.

First, of course, is instant access to deep liquidity while reducing execution risk. Listing on Hyperliquid means immediate access to a powerful liquidity pool that serves billions of transactions per day. This eliminates the typical cold start liquidity challenges that plague new protocols. In addition, direct access to unified liquidity can significantly reduce execution risks such as slippage and MEV extraction, ensuring that trading is smoother and safer from the start.

The second is perpetual fee sharing. The builder code provides a sustainable economic model by embedding a perpetual fee sharing mechanism into every transaction. This ensures that the protocol can continue to receive revenue proportional to the actual value it creates, rather than relying on temporary incentives or unsustainable liquidity mining programs.

The third is to focus on development. Developers are free to devote their energy and resources to building better products and optimizing user experience. They no longer need to invest a lot of time, money or energy to maintain liquidity incentives, fund pool management or negotiate with partners to maintain liquidity.

BasedApp embodies this. Instead of spending months building a trading infrastructure from scratch, they focused on what users really wanted: "holding cryptocurrencies, trading, and using cryptocurrencies in the real world." Once their mobile app is live, they can fully access Hyperliquid's liquidity for perpetual contract trading and combine it with its mature Visa card infrastructure for real-world consumption. As founder Edison Lim said, they can focus on creating an "operating system for on-chain finance" instead of solving the liquidity bootstrapping problem.

Finally, cross-protocol synergies. Each new protocol strengthens the shared liquidity ecosystem, forming a virtuous cycle, where increased activity attracts more participants and further deepens the liquidity pool. This interconnected approach can create lasting network effects that benefit all participants and ensure the continued growth of the entire ecosystem.

Most ecosystem construction follows a similar strategy: provide grants to developers and organize hackathons. These methods are valuable, but they ignore the fundamental problem. The real resistance lies in the constant competition for liquidity, not the lack of funds or ideas. Every new protocol must obtain its own liquidity through dot-com, and then compete with profit-seeking capital when the incentive mechanism fails. The builder code completely subverts this burden. After access, inherit a $2 billion order book and earn a certain percentage of fees based on the proportion of traffic you generate. Teams like Lootbase can devote their energy to products without worrying about fragmented liquidity provider (LP) incentive mechanisms.

For developers, this creates a fundamentally different value proposition. On other chains, you might get a $50,000 grant to build a DEX, but then spend six months convincing market makers to provide liquidity and a lot of time on incentives. On Hyperliquid, you have immediate access to over $2 billion in order book liquidity from day one. Your success depends on building a great product, not your ability to convince VCs to fund liquidity mining.

Hyperliquid doesn’t offer traditional grants and accelerator programs. You don’t get full guidance during the development process, nor do you get guaranteed market support. Instead, you get the infrastructure you need to build applications that work from the day they are released. If you can create real value for users, the builder code will ensure that you get a fair share of economic gains.

Hyperliquid will face competition from new chains like MegaETH and Monad that are coming to market soon and have impressive technical specifications. It will be interesting to see whether these new chains can match Hyperliquid's shared liquidity and capital efficiency approach. Technical performance is the key point at the moment, but economic design is the fundamental factor in creating lasting value.