Just a few years ago, the word 'cryptocurrency' typically evoked images of extreme volatility, such as Bitcoin's dramatic price fluctuations. However, in the past year, we have witnessed another meaningful wave of change in the cryptocurrency market. This is the explosive growth and spread of stablecoins across the financial market. Unlike digital assets like Bitcoin or Ethereum, whose prices change by the minute, stablecoins essentially maintain stability by pegging their value to a specific fiat currency like the US dollar or physical assets.

The global liquidity increase and accelerated digital transformation after the pandemic have raised interest and usage of stablecoins to unprecedented levels. Beyond being a simple cryptocurrency investment tool, stablecoins have now firmly established their presence as a key intermediary for cross-border remittances, digital payments, and the DeFi ecosystem. Can stablecoins go beyond being a 'safe asset' in the highly volatile cryptocurrency market and become a key player in a 'new horizon' that resolves the inefficiencies of traditional financial systems and drives financial innovation?

In this first installment of a series to be published over 2-3 parts, we will closely analyze through on-chain data why and how stablecoin usage has surged in the past year, and explore specific cases of how stablecoins are being utilized in actual financial environments. We will comprehensively illuminate the phenomenon of stablecoins emerging as a core element of financial infrastructure through data and cases.

Stablecoin Usage Analysis: A Breakthrough Revealed by Data

The growth of stablecoins in the past year can be clearly confirmed through on-chain data, not mere speculation. The total issuance, daily transfer volume, and number of active addresses of major stablecoins have consistently increased, demonstrating their role as a core liquidity source in the digital economy.

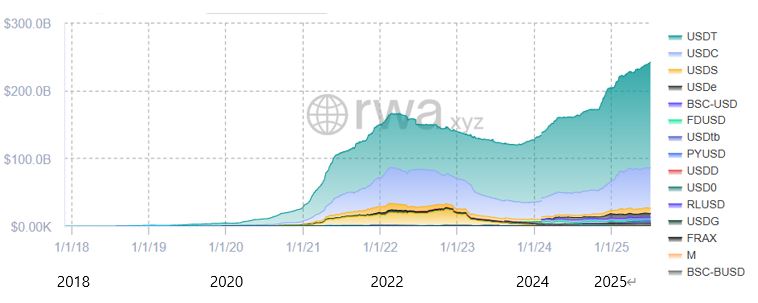

As of the end of June 2025, the market capitalization of stablecoins recorded $241.7 billion, a surge of over 50% compared to the same period last year. This clearly shows the explosive increase in stablecoin demand, exceeding 1% of the US M2 money supply of $21.4 trillion in 2024.

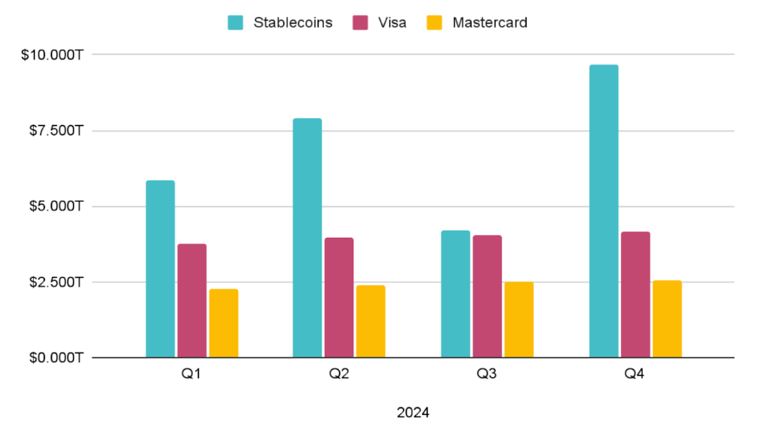

Moreover, stablecoin transaction volume reached $2.6 trillion in June this year alone, proving the potential for fast and efficient cross-border fund transfers. Furthermore, according to a Cointelegraph report citing CEX.io data, stablecoins recorded an overwhelming transaction volume surpassing the combined transaction volume of Visa and Mastercard in 2024. This suggests that stablecoins are firmly establishing themselves as a core payment method in the global financial market.

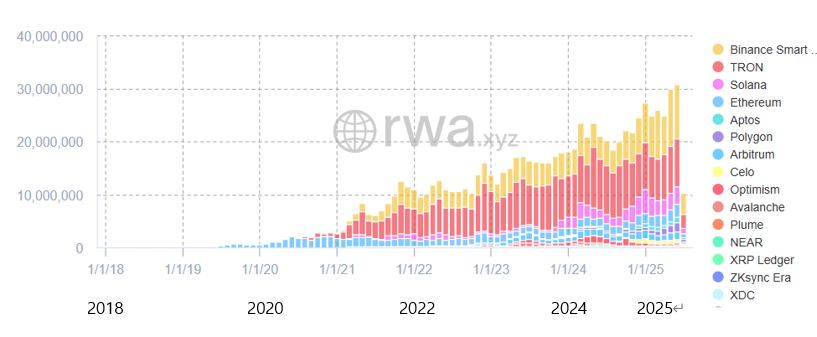

The continuous increase in active addresses for stablecoin usage also shows that more users are using stablecoins in everyday transactions.

Major stablecoins like USDT (Tether), USDC (USD Coin), and Dai (DAI) are leading the market with different growth drivers and market shares.

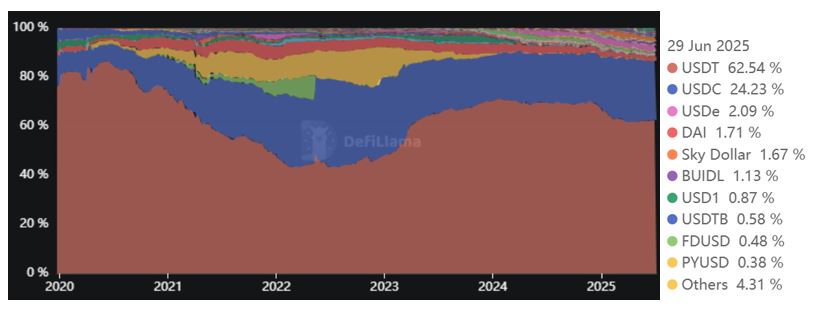

- USDT (Tether) has maintained the top market share for the past five years, boasting the largest issuance with a 62.5% market share as of the end of June, maintaining an overwhelming presence in Asian markets and cross-border remittances.

- USDC (USD Coin) maintains a 24.2% market share, emphasizing transparency and regulatory compliance, and has established its position in institutional and Western DeFi markets.

- Dai (DAI) is recognized for its unique value within the DeFi ecosystem as a decentralized, collateral-based stablecoin.

These stablecoins are creating practical use cases, especially in cross-border remittances and digital payments. Stablecoin transfers using blockchain technology provide much lower fees and faster processing speeds compared to traditional banking systems, bringing innovation particularly to small-scale international remittance markets in financially underserved Asian and African developing countries.

Utilization in DeFi Ecosystem: Stablecoins Penetrating the Heart of Finance

The DeFi ecosystem has been another key driver of stablecoin growth. In the highly volatile cryptocurrency market, stablecoins play a crucial, indispensable role as both a 'value storage mechanism' and a 'transaction intermediary'. Investors utilize stablecoins in various ways: storing assets without price volatility risks, taking out loans using them as collateral, depositing to earn returns, or supplying liquidity pools to receive transaction fees.

The proportion of stablecoins in DeFi protocols is overwhelming. For instance, a significant portion of assets deposited in major DeFi lending and liquidity protocols like Aave, Curve, and Compound consists of stablecoins. Decentralized exchanges like Curve Finance, in particular, support low-slippage trading between stablecoins and attract large liquidity. While stablecoin deposit yields (APY) fluctuate depending on market conditions, they provide higher return opportunities compared to traditional financial products, serving as an incentive to draw more liquidity into DeFi. Stablecoins enable stable operation of the DeFi ecosystem and function as essential infrastructure for financial innovation.

Where Reality Meets Stablecoins: Opening a New Horizon in Digital Finance

The influence of stablecoins is no longer limited to the virtual asset market, but is creating practical use cases in various real-world sectors, opening a new horizon in digital finance.

The most representative area is payment and remittance. For example, in some countries like Turkey, dollar-linked stablecoins are practically used as a key currency due to high inflation and exchange rate volatility. In developing countries like the Philippines, there is an increasing number of cases where overseas workers use stablecoins for remittances to their home countries, with much lower fees and faster speeds compared to traditional banking systems. This not only reduces fees but also demonstrates the potential of inclusive finance by improving financial service accessibility for those without bank accounts.

Card companies' entry into the coin payment market is acting as an important variable that could shake up the payment market. With the emergence of stablecoin-based payment cards, there are predictions that traditional payment systems like card companies, PG companies, and VAN companies could undergo changes. Particularly, if P2P (Peer-to-Peer) payment methods that directly transfer stablecoins from consumer wallets to merchant wallets spread, it is expected to reduce intermediary fees and improve transaction speeds.

These real-world application cases have drawn the attention of governments and regulatory authorities to stablecoins. In fact, the US Senate passed the GENIUS Act, which requires stablecoins to fully maintain reserves by 2025, conduct monthly audits, and comply with anti-money laundering (AML) regulations. This demonstrates a strong will to ensure transparency and stability in the stablecoin market.

In this way, stablecoins are evolving from a mere cryptocurrency variant to a partner in real-world finance. What innovations will the 'revenue beyond stability' structure of stablecoins bring in the future? In the next column, we will look into the financial operating principles hidden within fixed prices through the US Treasury-based RWA model and Tether's revenue structure.

News in real-time...Go to TokenPost Telegram

<Copyright ⓒ TokenPost, Unauthorized Reproduction and Redistribution Prohibited>