The long-anticipated collision between cryptocurrency and traditional banking systems has officially begun with the passage of the GENIUS Act. The impact of this legislation is already clearly emerging, with retailers like Amazon and Walmart considering launching their own stablecoins within two weeks.

Hank Hwang, CEO of Chronos Research, told BeInCrypto, "As more companies adopt this trend, the banking system will need to adapt quickly, especially when funds move away from traditional deposits. However, consumers switching to retailer-backed stablecoins will not receive the same protections offered by traditional banks."

A New Era of Cryptocurrency Integration

The GENIUS Act represents a historic change in the integration of cryptocurrency, especially stablecoins, into the US financial market. The act ensures that stablecoins are backed by tangible assets and subject to strong oversight, recognizing the potential for payment innovation.

One of the most critical provisions of the act is a clear regulation that only insured deposit institutions, including banks and credit unions, and certain approved non-bank entities can be authorized to issue stablecoins. It also strictly prohibits algorithmic-based or unsupported stablecoins to ensure stability and consumer confidence.

For far too long, certain industries and American consumers have been left in the dark.

— U.S. Senate Banking Committee GOP (@BankingGOP) March 13, 2025

That changes today with the GENIUS Act – a bipartisan step forward that will provide regulatory clarity for payment stablecoins. pic.twitter.com/H44W25dJzh

Following the act's passage, several prominent retailers are considering launching company stablecoins. Reports suggest that major corporations like Amazon and Walmart are seriously contemplating this step.

Multiple motivations will likely drive their reasons.

Retail Giants' Stablecoin Motivations

Retailers like Amazon and Walmart boast massive customer bases, generating billions of dollars in revenue daily through purchases. Many customers pay using traditional credit card networks like Visa and Mastercard.

These networks typically charge 2-3% exchange fees per transaction. However, for companies with such large transaction volumes, these fees can amount to billions of dollars annually.

Powerful companies can significantly reduce or eliminate these costs by issuing their own stablecoins and bypassing these networks.

Simultaneously, removing payment network intermediaries like banks drastically reduces payment times. Stablecoins, built on blockchain technology, enable near-instantaneous settlements, significantly improving companies' and suppliers' cash flow and efficiency.

In the context of international transactions, retailer-backed stablecoins offer a lower-cost alternative to traditional cross-border payment methods, streamlining global payments. These moves will essentially expand the retailers' customer base.

Their own stablecoins can be integrated into loyalty and rewards programs, providing unique incentives or discounts to customers. They can also open doors to offering new financial services.

"Frictionless rewards, cost savings, and consumer-centric benefits will drive change. Stablecoins will gain attention with preferred benefits and practical utility, seeking returns over idle deposits," Hwang told BeInCrypto.

These numerous advantages raise questions about how this new payment traffic will impact traditional banking services.

Stablecoins' Impact on Traditional Banks

Widespread adoption of retailer-backed stablecoins could significantly disrupt traditional banks, primarily by withdrawing funds from traditional deposits.

If Amazon or Walmart issue stablecoins, consumers can hold purchasing power in these stablecoins instead of traditional bank accounts. Instead of keeping money for groceries or online shopping, consumers can transfer those funds to Amazon or Walmart stablecoin wallets.

This change will directly reduce money held as deposits in traditional banks. Since these deposits are the lifeline of banks, substantial outflows will shrink their funding base, affecting their ability to lend to existing customers and businesses.

"Consumers will seamlessly transition from traditional finance to chains, finding familiar, fast, and flexible rails. Retail coins will absorb liquidity from banks to branded crypto networks," Hwang said.

Simply put, their overall economic activity will significantly decrease.

"The GENIUS Act levels the playing field with strict standards for reserves, regulation, and issuer qualifications. Banks will establish their position with a trustworthy framework, while non-bank entrants face rigorous rules. Ultimately, this is a liquidity war where the strongest survive," Hwang added.

How will traditional banks adjust their strategies to maintain competitiveness in light of these risks?

How Banks Will Adapt to Digital Transformation

To some extent, banks are already experiencing general deposit migrations. Stablecoins could accelerate this trend. Traditional banks have been actively working in recent years to meet the growing demand for digital banking.

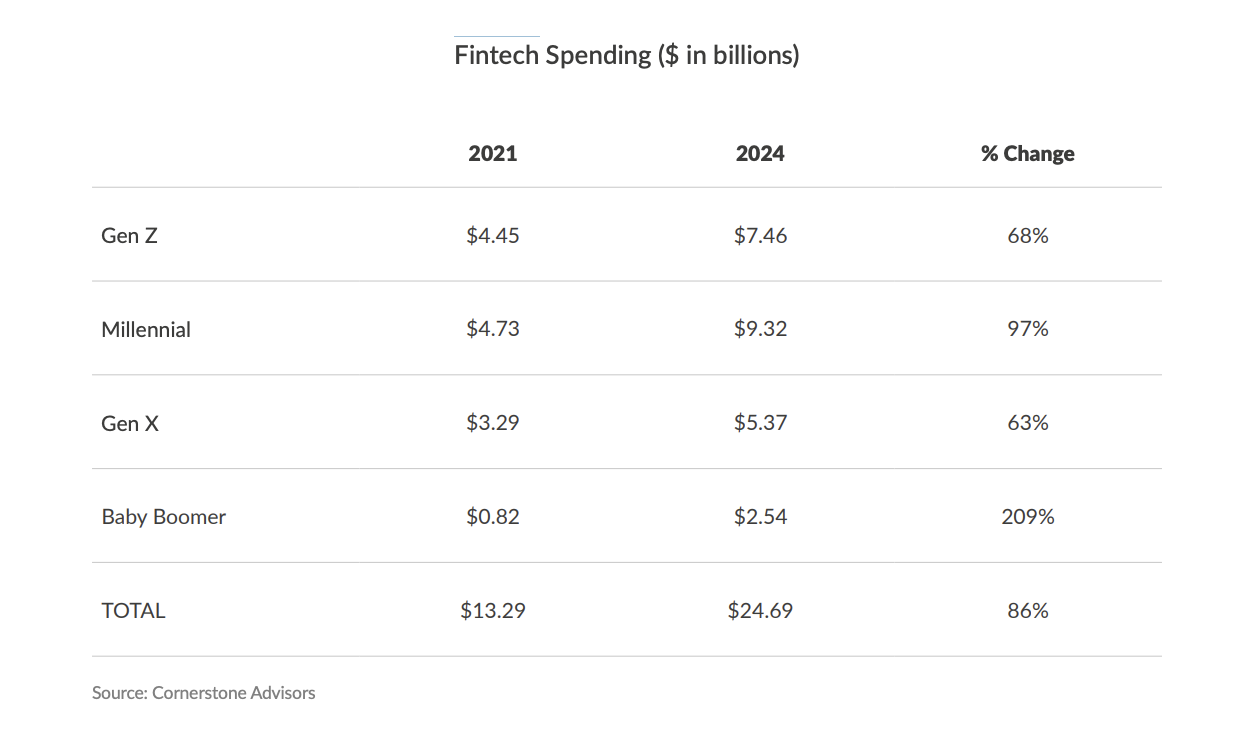

Cornerstone Advisors' recent report emphasizes that fintech spending has significantly increased across all generations. From 2021 to 2024, fintech spending for Generation Z, Millennials, Generation X, and Baby Boomers increased by 86%, jumping from $13.29 billion to $24.69 billion.

Some banks have already made significant progress in preparing for the expected widespread adoption of retail-supported stablecoins. For example, JP Morgan Chase has been preparing for this change for years.

"Banks like JP Morgan will not only defend deposits but also leverage trusted infrastructure to create fast and secure digital dollars, generating new revenue and enhancing customer benefits," said Mr. Huang.

With the launch of the JPM Coin in 2019, JP Morgan pioneered the concept of bank-issued digital currency for wholesale payments. They utilized private Blockchain technology within the Kinaxis division to increase efficiency and accelerate inter-bank payments.

After the passage of the GENIUS Act, JP Morgan announced the introduction of the JP Morgan Deposit Token (JPMD) as its latest strategic step. This will be piloted on Coinbase's public Base Blockchain.

This move is particularly significant. The JPMD is positioning itself as a fully insured digital representation of bank deposits, especially those paying interest.

This directly contrasts with the GENIUS Act, which prohibits non-bank payment stablecoins from paying interest to holders. Critics argue this is a concession to existing banks.

David Sacks just said the quiet part out loud

— Pledditor (@Pledditor) June 21, 2025

The GENIUS Act was written by the banking industry to keep stablecoin issuers uncompetitive with legacy system products pic.twitter.com/nqZeWDISgT

The JPMD's ability to generate returns aligns with new regulatory clarity. It provides institutional clients with a compliant and highly integrated alternative to traditional stablecoins for on-chain payments and cross-border B2B transfers.

It also clearly demonstrates how banks can leverage their existing strengths to maintain a strategic advantage against new competition.

The Critical Role of FDIC Insurance

Thanks to existing infrastructure, resources, and unique regulatory protections, banks have a robust foundation to adapt to changes in the financial sector.

"Traditional financial banks must build bridges between legacy and digital. They must deploy deposit tokens, enhance Blockchain-based benefits, and combine security with seamless convenience. To secure liquidity, banks must combine innovation with insurance," Mr. Huang told BeInCrypto.

This possibility is particularly important considering the consumer protection gap between traditional banks and non-bank stablecoin issuers. Traditional banks provide Federal Deposit Insurance Corporation (FDIC) protection, guaranteeing deposits up to $250,000 per depositor. This insurance is backed by the US government and is the most robust guarantee in the financial world.

FDIC insurance does not apply to stablecoin issuers outside the banking industry. While the GENIUS Act aims to ensure strong reserves and audits for stablecoins, a "run" on issuers could still lead to operational issues, liquidity problems, or situations where the stablecoin loses its dollar peg. In such cases, recovery depends on the issuer's solvency and operational integrity.

In contrast, if an FDIC-insured bank fails, insured deposits remain safe. The FDIC intervenes to prevent principal loss, which is the core purpose of deposit insurance: protecting consumers from bank failures.

"Without deposit insurance, consumers face security risks and liquidity loss, with unclear transparency about actual reserves. During large redemptions, stablecoins may struggle to maintain stability under pressure," Mr. Huang added.

By leveraging these critical advantages, banks can maintain a strong appeal to consumers who prioritize guaranteed deposits.

The Future of Finance: A Hybrid System

The emergence of stablecoins issued by large retailers or non-bank institutions represents a significant change in the financial industry. This development could impact the future of traditional banking models and potentially alter existing capital flows.

Each player has unique advantages, making competition increasingly fierce. As a result, a hybrid financial system is likely, with both non-bank and banking institutions either securing their place or gradually disappearing.

Ultimately, the winners will be those who best combine technological innovation with trust, security, and regulatory compliance.