#Case 1

A, a 30-something office worker residing in Busan and in charge of overseas trade at a small and medium-sized manufacturing company, went on a business trip this month to meet with a Singapore buyer. In the past, he would have had to process all expenses such as airline tickets and local accommodation costs through complicated bank transfer procedures. However, this time was different, thanks to the public chain-based Korean won stablecoin payment system that the company has pilot-introduced. Before departing, he charged Korean won stablecoin to the company's dedicated wallet. He was then able to complete real-time payment in local currency by linking with the payment system 'Straits X' used by the local partner company.

#Case 2

B, a 20-something college student from California, USA, embarked on his first trip to Korea to see the BTS concert in Seoul. Before boarding the flight to Korea, he came across information about easy payment with Korean won stablecoin on social media. He installed a mobile wallet app and charged Korean won stablecoin with dollars. Upon arriving at Incheon Airport, he paid for the airport bus using the wallet app without going through an exchange, and checked into his accommodation with just one app. He could also pay at nearby restaurants simply by scanning a QR code.

These cases assume usage scenarios when Korean won stablecoin is actually issued. Discussions continue about whether the Korean won stablecoin promised by the Lee Jae-myung government can establish itself as a payment method in daily life. Various issues coexist, including differentiation from existing easy payment systems, expanded private sector participation, and value as an investment asset.

■Ongoing Controversy over Utility

The 'Digital Asset Basic Law' proposed by Democratic Party lawmaker Min Byung-deok on the 10th allows private issuance of Korean won stablecoin. The capital requirement was initially lowered from 5 billion won to 50 billion won, then adjusted to 10 billion won in the draft 'Digital Asset Innovation Act' disclosed on the 17th. In any case, the bill is being organized to enable private participation.

Korean won stablecoin can be used in various payment systems such as domestic online shopping malls, coffee shops, and food delivery services. Payments can be made quickly and cheaply without intermediary payment agents. In fact, in the United States, retail giants Amazon and Walmart are considering issuing their own stablecoins. An advantage is the ability to hedge exchange rate fluctuation risks in real-time. Additionally, foreign tourists can charge Korean won stablecoin to their digital wallet and pay, while Koreans traveling abroad can link with foreign payment systems for real-time payments.

On the other hand, there are strong counterarguments that if Korean won stablecoin fails to secure differentiation from existing easy payment methods, it will be ignored. Without special incentives, it will be difficult to gain consumer choice. Moreover, the difference from the Bank of Korea's experimental 'Central Bank Digital Currency' (CBDC) is unclear. Some suggest activating Korean won stablecoin in specific areas such as medical tourism.

■Infrastructure is Still Necessary

Some argue that considering global trends, there is a need to establish Korean won stablecoin infrastructure domestically, regardless of these practical controversies. If not participating in this trend, it could mean not just missing one payment method, but potentially having financial sovereignty and national industrial ecosystem subordinated to overseas platforms. It was proposed that the effectiveness of stablecoins should be verified through private experiments and consumer choices, while the government should focus on providing flexible policy environments like regulatory sandboxes.

Professor Lee Jong-seop of Seoul National University Business School stated, "If a company issues Korean won stablecoin and there is no demand, it will naturally exit, and if needed, the market will keep it alive," adding, "We can't be riding horses when others are running steam locomotives." He further explained that "Just as it's difficult for a latecomer like Tving to catch up where Netflix has already established itself, platform competition is an industry where early positioning is absolutely crucial."

The professor also noted, "While CBDC remains in a closed structure, stablecoins have superiority in openness and global interoperability," comparing it to "the difference between intranet and internet."

■Investment Value? 'Well...'

On the morning of the 13th, when Israel attacked Iran, the price of Tether (USDT), a dollar-based stablecoin, temporarily rose to $1.0008. The 24-hour trading volume reached approximately $9.766 billion, recording the highest level that week. Analysis suggests this resulted from investors moving assets en masse to stablecoins after withdrawing funds from high-volatility cryptocurrencies like Bitcoin and Ethereum due to Middle East geopolitical instability.

Such geopolitical conflicts stimulated demand for 'digital safe assets'. This also led to a surge in Circle (USDC), another dollar-based stablecoin. On the 4th, Circle Internet Group conducted an IPO with an initial public offering price of $31 per share. It soared 168% in its first trading, drawing global attention. Currently, Circle Internet is trading at $235 per share on the New York Stock Exchange.

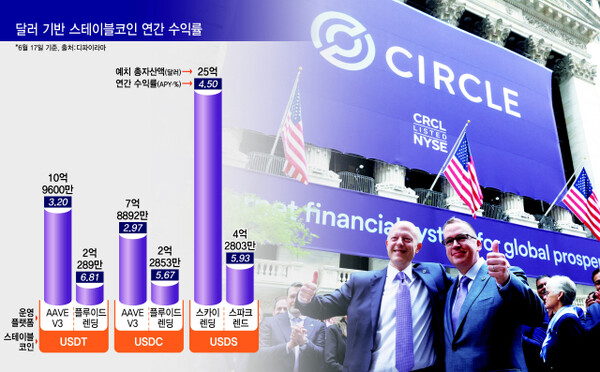

Dollar-based stablecoins are attracting attention as investment assets providing 4-10% annual percentage yield (APY) through deposit alone. Cryptocurrency exchange Kraken offers 5.5% on USDT, while Coinbase provides 4.1% on USDC. Decentralized (DeFi) platforms offer higher returns than bank interest rates through 'yield farming'. However, yields vary significantly across operating platforms.

What about Korean won stablecoin? The industry is skeptical about its investment value. Lee Hyun-ho, CEO of Busan blockchain company Global Top Net which issued 'Camel Coin', said, "It's questionable whether an unlisted Korean won stablecoin can be recognized for its exchange value with the won," emphasizing that "to expect deposit or interest income, exchange listing must precede it."