From a practical point of view, stablecoins are actually more than just a payment tool, but a new stage in the evolution of currency, which can be called " tokenized currency " .

1. The significance of stablecoins

1. Technical value as a distributed ledger

To truly understand stablecoins, we need to sort out their development background. Stablecoins are built on the basis of distributed ledger technology . Distributed ledger technology is the third iteration of human computing methods in thousands of years. The first was single- entry bookkeeping. Judging from the clay tablets in the Sumerian region that have been discovered so far, the single- entry bookkeeping method is used, which only records income and expenditure.

By around 1300 AD , Italy had developed double-entry bookkeeping, a method for recording not only income and expenses but also assets and liabilities. In the 700 years that followed, the calculation method was only refined, not rewritten.

It was not until the emergence of the Bitcoin blockchain in 2009 that a new method of calculation, namely distributed accounting, first appeared. The biggest difference between distributed accounting and previous accounting methods is that the previous accounting methods all recorded their own accounts, which belonged to private ledgers. For example, a remittance from Beijing to New York involves the participation of multiple institutions, and it is necessary to align all the information on the private ledgers of these institutions, which takes a certain amount of time and cost. However, a distributed ledger is a public ledger. Whether it is institutions or individuals around the world, they all record accounts on the same ledger. Therefore, there is no need for many institutions to align information. The two parties to the transaction can directly complete the payment in a point-to-point manner. This is the biggest difference between the two calculation methods.

After the emergence of Bitcoin blockchain, stablecoins began to appear in 2014. In the process of continuous engineering experiments, maturity and optimization of distributed ledger technology, two trends have emerged: on the one hand, since 2009, people have created Bitcoin, Ethereum and other currencies "out of thin air" on the blockchain, which are called "digital natives". On the other hand, since 2014, the emergence of stablecoins represented by USDT has marked the emergence of another trend, namely "digital twins". The so-called digital twins refer to the introduction of certain assets that already exist in the real world, such as the US dollar, into the blockchain and tokenize them, that is, mapping existing assets to the chain in a digital way.

At the same time, with the approval of the launch of Bitcoin ETFs by the United States and Hong Kong last year, a new phenomenon has emerged: digital native assets have moved from on-chain to off-chain. Bitcoin ETFs are listed on the New York Stock Exchange (NYSE) and the Hong Kong Stock Exchange (HKEX), and investors can invest and buy and sell them according to the mechanism of stock trading. Bitcoin itself exists on the chain, while Bitcoin ETFs exist off-chain. Therefore, in this process, the conversion between On-Chain and Off-Chain, as well as the interaction between digital twins and digital natives are involved.

In the practice of distributed ledger technology over the past decade, if we regard it as a social engineering experiment, we can see the changes and gradually prove the value of these technologies.

2. As a new financial market infrastructure

Based on distributed ledger technology, financial market infrastructure has also undergone significant changes since 2009. These changes are based on the transformation of distributed accounting. Financial market infrastructure mainly includes a series of mechanisms such as payment, trading, clearing and settlement. So what is new about the new mechanism compared with the old one? What are the characteristics of the old and new mechanisms?

The financial infrastructure assets we currently rely on adopt the central registration, central depository , central counterparty transaction and central settlement model, which requires at least three institutions to cooperate to complete the clearing and settlement of a transaction. However, on a distributed ledger, since all participants record accounts on the same ledger, the transaction model is transformed into a point-to-point transaction, and any two people can complete the transaction directly without the need for an intermediary.

The settlement model of the existing financial market infrastructure is net settlement, while the settlement model on the distributed ledger is transaction-by-transaction settlement. In other words, once the transaction is confirmed, the settlement is completed and the payment is made. From the perspective of the stock market, the New York Stock Exchange will launch a 5×23-hour trading model at the end of this year, reserving one hour for clearing after the end of trading hours; while Nasdaq will launch a 5×24-hour trading model in the future. However, Nasdaq cannot achieve this goal within this year because under the old financial infrastructure, the transaction process must be suspended for a period of time for clearing. In contrast, Hong Kong's virtual currency exchanges have achieved 7×24-hour trading without holidays, precisely because of the different types of ledgers, which leads to different financial market infrastructures. This is also one of the backgrounds of stablecoins, that is, they are built on new financial market infrastructures.

2. Asset Tokenization (RWA)

1. What is asset tokenization?

In my opinion, asset tokenization actually originated from USDT, which refers to putting real-world assets on the chain and tokenizing them through blockchain technology. Its development process has gone through three stages:

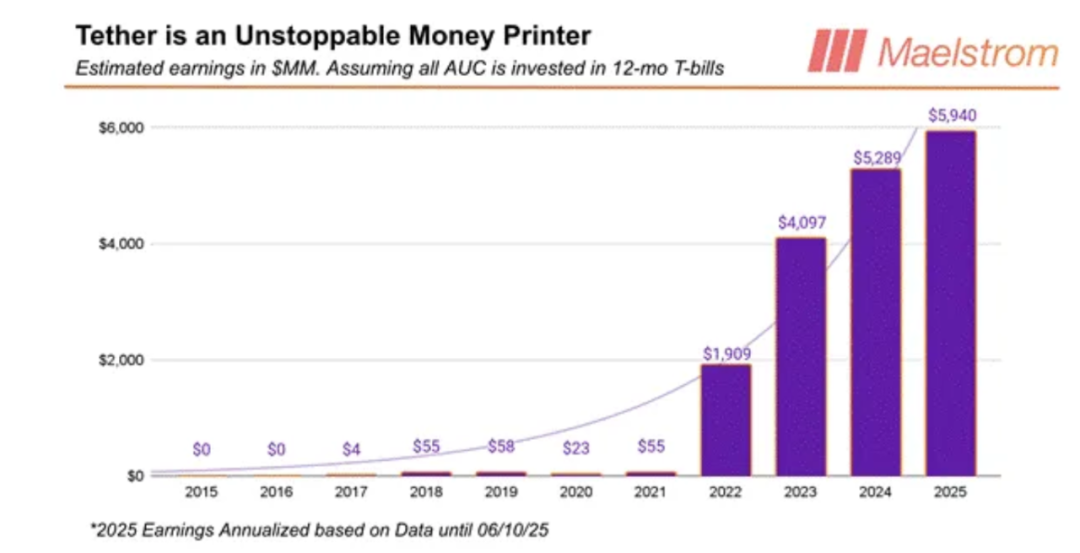

The first stage is the emergence of USDT, which was in 2015. The practice and social experiments of the past ten years from 2015 to now have shown that the tokenization of legal tender has great value, not only in the field of payment and settlement, but also in other aspects, which will be elaborated in detail later. In this context, countries have begun to legislate to regulate and further promote it under the license and regulatory framework. According to statistics of different calibers in 2024, the transaction volume based on US dollar stablecoins is as low as 16 trillion US dollars, while the higher statistics are 28 trillion US dollars. Whether it is 16 trillion US dollars or 28 trillion US dollars, it shows that the application of stablecoins based on distributed ledgers and blockchains has become a "killer application" and is widely used. Its largest user group is those who do not have bank accounts in Africa, using USDT and USDC to complete cross-border payments.

The second stage began last year, with the launch of tokenization of fund products in the United States by BlackRock, Fidelity, etc., such as U.S. Treasury bond funds, U.S. dollar currency asset funds, etc. These funds were tokenized and put on the chain, starting the process of tokenization of financial assets.

The third stage is the tokenization of physical assets, that is, the tokenization of physical assets such as real estate and hotel assets. This stage is still in the exploratory stage and may be gradually promoted from this year. At present, there are billions of dollars of physical asset tokenization practices.

These three stages are arranged in order from easy to difficult. The tokenization of legal tender is relatively easy because it does not need to rely on other means for credit endorsement. Legal tender such as the US dollar and the RMB are endorsed by national laws, so the market has a high degree of trust in them and the tokenization process is relatively simple. The tokenization of financial assets is relatively more complicated, but it is still easier than the tokenization of physical assets because its issuers and custodians are usually regulated licensed financial institutions, and the custody is mainly in banks. People trust these licensed financial institutions that are subject to strict financial supervision, so they are more likely to accept their tokenization.

The biggest difference before and after tokenization is that once an asset is minted into a token on the chain, it is separated from the banking system, leaving both the bank account system and the SWIFT system, and becomes decentralized. Therefore, whether the token exists on the chain and whether it exists permanently needs to be guaranteed by a strictly regulated financial institution (custodian bank). Tokens are generated based on instructions issued by the custodian bank. For example, after the custodian bank confirms that it has received $100,000 from the customer, it mints a $100,000 token (such as a US dollar stablecoin). This kind of instruction is only recognized by the custodian bank, so the process is relatively simple.

However, there is no mature solution for the tokenization of physical assets. The main problem is how to put information on the chain, confirm ownership, and ensure that the on-chain information is strongly bound to the physical assets off the chain, because the two can easily decouple. For example, for real estate, it is necessary to put real estate information on the chain, which requires cooperation from multiple parties, such as the Housing Authority and other relevant departments, but this problem has not yet been well solved.

In the blockchain industry, there is a potential solution, but it is not yet mature, called DePin (decentralized physical network). In theory, each block can collect data on the chain to ensure the real existence of assets and verify them on the chain. For example, charging piles can be equipped with blockchain communication modules, through which data such as the length of use, charging volume, and income of the charging piles can be directly uploaded to the chain. However, this path is currently not mature enough and the cost is high, so the tokenization of physical assets is relatively rare. It is expected to develop from 2025.

2. The significance of asset tokenization

Some people point out why tokenization is necessary and what is special about it compared to traditional currencies such as RMB or USD? The necessity of tokenization lies in:

1. Improve the liquidity of assets around the world

When an asset is minted as a token on a public chain, it is easily accessible to investors around the world, giving the asset global liquidity. This is equivalent to incorporating it into a global liquidity pool. For example, buying stocks on the Hong Kong Stock Exchange is a complicated process for Brazilian investors, who need to open an account in Hong Kong, convert their currency into Hong Kong dollars, and then trade. However, on the blockchain, these cumbersome procedures are omitted because it removes traditional mechanisms such as central registration and central depository, and enables peer-to-peer transactions. Investors can independently find information and decide whether to buy. This greatly improves the accessibility and trading convenience of assets.

2. New clearing and settlement model

Tokenization brings a peer-to-peer clearing and settlement model with fewer links, higher efficiency and lower costs. Preliminary statistics show that the turnover of funds of traditional banks is about 7 to 8 times a year, while the turnover of funds based on decentralized finance (DeFi) can reach 67 times a year, which is almost 10 times that of traditional banks. The fastest case of completing a loan on the blockchain is 10 seconds, including lending, recovery and interest settlement. This model is called "flash loan". "Flash loan" is achieved through excess asset mortgage rather than leveraged lending. The interest rate of USDT on-chain lending is 8%. This high interest comes from a significant increase in the frequency of fund turnover, rather than amplifying returns through leverage. Therefore, tokenization not only improves the efficiency of fund turnover, but also eliminates the need for leverage and reduces risks.

3. Programmability

Traditional currencies (such as RMB and USD) are not programmable, while tokenized currencies can be programmed through smart contracts. This feature has been widely used in clearing and settlement and default handling in smart contracts, greatly improving efficiency. For example, in on-chain lending, once the default condition is triggered, the smart contract will automatically execute the liquidation without the intervention of accountants, banks or courts. This process can be completed in just a few seconds, while handling defaults in traditional financial markets requires a large number of intermediaries and a long time.

4. The AGI Era

With the advent of the era of artificial general intelligence ( AGI), machines will create economic value independently of humans, and payments and settlements will also be required between machines. In this case, transactions between machines cannot rely on traditional payment methods, but need to be completed through smart contracts and programmable currencies. If legal tender hopes to maintain its importance and value in the AGI era, it must be programmable. Therefore, tokenization is not only a need for current financial innovation, but also an inevitable choice for future technological development.

3. Monetary properties of stablecoins

The attributes of currency have gone through three iterations: First, early currencies had natural attributes. Whether it was shells, gold, silver or copper, they all came from nature, and people gave them currency attributes. Second, with the emergence of sovereign states, legal currencies such as the RMB, US dollar, and British pound were born. At this stage, currency had legal attributes. Third, digital currencies such as Bitcoin were created. It is based on digital technologies such as cryptography, distributed ledgers, digital wallets, and smart contracts, which constitute the technical attributes of currency and enable it to gain global consensus. Based on this consensus, the total market value of Bitcoin has reached more than 2 trillion US dollars.

Stablecoins have dual attributes: on the one hand, legal tender is a currency that is given value by law and is used by people. On the other hand, when legal tender is converted into stablecoins, it has technical attributes. It runs on a distributed ledger, and is based on cryptography, distributed ledgers, digital wallets or smart contracts in the process of issuance, minting and operation. From this perspective, stablecoins can be regarded as the tokenization of legal tender and are the best currency created by humans.

From the perspective of currency attributes, stablecoins have functions such as payment and settlement. In addition, stablecoins not only have technical attributes such as programmability, but are also currencies that transcend time and space. Once the currency is converted into stablecoins and runs on the chain, it transcends spatial limitations and judicial area limitations. For example, in Africa, more than 60% of the population does not have bank accounts and cannot obtain currencies such as the US dollar through banks, but with the help of mobile wallets, US dollar stablecoins can be easily purchased on the chain. Third, it is a high-circulation currency, which is more efficient than the circulation of real currency by constraining circulation through smart contracts on the chain. Fourth, it is a democratized currency. Specifically:

1. Discussing Stablecoins from the Perspective of Reserve Assets

Stablecoins are similar to money funds in terms of asset reserve management. The issuer of stablecoins collects US dollars from customers and deposits them into a custodian bank. The custodian bank issues instructions to the issuer. For example, if a person receives $100,000, the issuer will then mint $100,000 in stablecoins for him on the chain. The underlying asset of stablecoins is legal tender, but legal tender is not circulated directly, but through tokens, and its management method is consistent with that of money funds. Some people worry whether this involves money creation, but in fact there is no money creation. Because legal tender is only deposited in the original place, there is no leverage in the issued currency, and there is no currency storage, so the disturbance to financial stability is relatively small. Stablecoins are only circulated at high speed across time and space in the form of tokens, replacing leverage. The reason why there is no currency storage is because it improves the efficiency of capital turnover. For example, "flash loan" can be lent and recovered within 10 seconds.

From the perspective of reserve assets, stablecoins actually solve the "last mile" problem of inclusive finance. Inclusive finance requires convenient access to financial services. Without financial accounts, inclusive finance is out of the question. Stablecoins are widely used in Africa, although the amount is not high. Take Kenya as an example. 60% of its people do not have bank accounts, so they developed a payment method based on mobile phone numbers, which has become a classic case of inclusive finance. Now Kenyans can not only send text messages to telecom operators to complete payments, collections or payments through mobile wallets, but also obtain US dollar stablecoins more conveniently on the chain through digital wallets, which is more convenient than the bank account system.

2. Analyzing Stablecoins from the Perspective of Cross-border Payment Facilitation

After obtaining the US dollar stablecoin, the holder will have the ability to make cross-border payments, which is a great progress for inclusive finance and greatly increases the access to financial services. As a result, those who do not have bank accounts in Africa have gained the possibility of global payments through mobile wallets, and Chinese cross-border e-commerce has become the biggest beneficiary. A survey in Yiwu found that local export merchants have begun to collect US dollar stablecoins. After receiving the US dollar stablecoins paid by customers, Chinese cross-border e-commerce merchants doing international trade need to return to settle the exchange, but they cannot directly use the US dollar stablecoins to settle the exchange. They can only exchange them for US dollars in the Hong Kong Stock Exchange and return them to the bank account for settlement. From a practical business perspective, it solves the problem of the "last mile" of inclusive finance.

At present, a new C To B model has emerged in China's cross-border trade and international trade , that is, global C-end users place orders directly on Chinese Internet e-commerce platforms. Chinese merchants no longer transport goods via containers, but in the form of parcels. After the C-end user places an order, the merchant will package the purchased goods such as shoes and clothing and send them directly to the user's residence through logistics. Compared with the traditional B To B To C container trade, C To B parcel trade urgently needs a faster payment method. If the payment takes 7 days to arrive, the merchant must wait until the payment is received before shipping. If the traditional payment method is used, the parcel trade cycle will be extended to two weeks or even three weeks. If the US dollar stablecoin is used, when the C-end customer pays the Chinese Internet platform, the payment will arrive quickly and the cost is extremely low. In this context, cross-border e-commerce has become the biggest beneficiary of stablecoins, and Chinese cross-border e-commerce has benefited a lot. Although China does not currently recognize this type of payment method, the Chinese people have actually benefited a lot from it, and it has provided a strong boost to the facilitation of cross-border trade.

4. US dollar stablecoin

Further focusing on the US dollar stablecoin, its fundamental goal is not to help the sale of US Treasury bonds or increase the number of US Treasury bond buyers, but to maintain the dominant position of the US dollar as the world's mainstream currency. It can be said to be the inheritance and development from the gold dollar, petrodollar to the token dollar or digital dollar. It is observed that last year, the transaction volume and payment volume of about 10 trillion to 20 trillion US dollars have been separated from the banking system. Once the stablecoin is minted, it has nothing to do with the bank . After holding the stablecoin, the customer no longer relies on the bank account system or SWIFT. At present, a transaction volume of nearly 20 trillion US dollars has been reached. From the perspective of payment alone, although it is less than 100 billion US dollars, the scale of transactions and payments combined is about 20 trillion US dollars.

Given that the US dollar stablecoin bypasses SWIFT, this is a major blow to the US financial power, but this trend is driven by technology and is unstoppable. The US may eventually have to accept a compromise, that is, to allow SWIFT to be bypassed, but to strive to maintain the status of the US dollar. In this case, 99.99% of the $20 trillion in stablecoin transactions last year were US dollar transactions, simply because other countries did not issue their own stablecoins, resulting in the US occupying the market.

Currently, the US government hopes to pass a stablecoin bill before Congress adjourns in August. At this stage, there are two types of US dollar stablecoins, divided into onshore and offshore categories. As of May 2025, the total minting amount is 250 billion US dollars. One is USDC, which is issued by the US financial technology company Circle and the mainstream cryptocurrency exchange Coinbase. It is an onshore US dollar stablecoin and is favored by US users. The second is USDT, which is issued by Tether, a company registered in El Salvador and has no branches in the United States. However, as a US dollar stablecoin, its reserve asset management is the same as that of a monetary asset fund. It needs to purchase a large amount of US short-term Treasury bonds, US dollar deposits and cash. The relevant operations are completed by US institutions, so it can be regarded as an offshore US dollar stablecoin.

The Hong Kong Stablecoin Ordinance also divides Hong Kong dollar stablecoins into onshore and offshore categories. Hong Kong dollar stablecoins approved by the Hong Kong Monetary Authority can be used by individual retail investors in Hong Kong, but Hong Kong dollar stablecoins issued outside Hong Kong, if recognized to a certain extent by Hong Kong regulators, can be used in Hong Kong, but only qualified investors, and retail investors are not eligible to use them. The same is true for relevant US regulations. As for why USDT chose El Salvador as its place of registration, the reason is that the legal currency of El Salvador is the US dollar. The country does not have its own legal currency. The US dollar has been designated as the legal currency during legislation, so there is no legal barrier to conducting US dollar stablecoin-related business in El Salvador.

5. The significance of stablecoins for China

1. Impact and Response

The impact of stablecoins on China is multi-dimensional at the monetary level. On the one hand, the form of currency continues to evolve over time. When technical attributes and legal attributes are integrated to empower currency, the competitiveness of currency will be significantly improved. In the pattern of currency competition between countries, better currencies will inevitably have a strong competitive advantage over other less competitive currencies.

On the other hand, the process of currency globalization is accelerating. In 2024, the global stablecoin transaction volume will reach 20 trillion US dollars, and most of the transactions will be denominated in US dollars. This currency circulation model based on public ledgers provides a more efficient and lower-cost way for currency internationalization.

In addition, the global monetary landscape is gradually moving towards multipolarization. In this process, countries need to actively think about how to enhance the competitiveness of their own currencies and explore the possibility of creating better currencies through technological empowerment and other means.

Monetary facilitation is also an important aspect that cannot be ignored. The key to the widespread use of stablecoins in Africa lies in their convenience in acquisition and payment. There is no need to meet the conditions for opening a bank account. Point-to-point payments can be made around the world with the help of mobile wallets, which greatly improves the accessibility and efficiency of payments.

In view of the many impacts brought by stablecoins, China is already at a stage where it must actively respond. Relevant work can be promoted in stages and levels. First, we can consider using Hong Kong as a "test field" to carry out relevant pilot projects for offshore RMB stablecoins. For example, we can support Hong Kong to join hands with mainland free trade zones, such as the Hainan Free Trade Zone, the Guangdong-Hong Kong-Macao Greater Bay Area, and the Shanghai Free Trade Zone. In particular, the FTN accounts in the Shanghai Free Trade Zone have unique advantages, and its financial policies are relatively more convenient and more complete. These policies can be combined with the stablecoin pilot, and exploration can be started from the offshore RMB stablecoin. Through the pilot, we can accumulate experience and lay the foundation for subsequent promotion on a larger scale in China.

2. Synergy with Central Bank Digital Currency (CBDC)

If the RMB stablecoin is officially launched in the future, it is necessary to consider its coordination mechanism with the central bank's CBDC. One possible solution is to build a two-tier architecture, that is, the central bank directly opens an account for the stablecoin issuer. The stablecoin issuer deposits the legal currency received from the customer into the account, and the central bank issues CBDC to the issuer accordingly. The issuer then uses CBDC to mint stablecoins on the blockchain for customers to use worldwide. Of course, this idea needs further discussion and improvement, but its core lies in exploring the organic combination path of the central bank's CBDC research results and the stablecoin architecture.

The positioning of the central bank's CBDC and commercial institutions' stablecoins has different focuses, and the two complement each other. The central bank's CBDC focuses more on centralized issuance to ensure monetary sovereignty and financial stability; while the stablecoins of commercial institutions, after leaving the banking system, rely on blockchain technology to achieve decentralized circulation, break through national borders and judicial regional restrictions, and achieve free circulation. In this model, the central bank leads the issuance in the first half, and commercial institutions promote market circulation in the second half, giving full play to their respective advantages and jointly promoting the innovative development of the monetary system.

3. Understanding of “decentralization”

The concept of decentralization can be understood from many perspectives: First, from an economic perspective, decentralization is actually a trade-off between fairness and efficiency. If fairness is emphasized, decentralization is needed to avoid excessive concentration of power in a single entity. On the contrary, if efficiency is pursued, centralized decision-making is preferred. Therefore, the degree of decentralization is closely related to the emphasis on fairness and efficiency. Ideally, a balance needs to be achieved between the two.

Second, from the perspective of technical protocols, decentralization is an inherent requirement of the underlying technology and cannot be achieved at the application layer. The application layer needs to take into account multiple factors such as user convenience and functional integrity, so it is difficult to achieve decentralization. However, the underlying protocol must be decentralized. Taking the blockchain protocol as an example, it has the characteristics of open source, no permission required, and free. This is similar to the IP protocol, UDP protocol, HTTP protocol, etc. in the Internet. These protocols do not require any entity's permission, are universally used, and have typical decentralized characteristics. It is this decentralized feature that enables the Internet and blockchain technology to achieve extensive interconnection and interoperability on a global scale.

Third, in the field of data privacy protection, decentralization means that individuals have sovereignty over their own data. From the perspective of data privacy protection, the underlying protocol is required to be decentralized to protect personal data rights. However, in the context of global interconnection, if there are multiple different underlying protocols on the Internet, it will cause problems in interconnection. The application layer must be regulated because it needs to generate huge social benefits, and through regulation, negative externalities are eliminated and positive externalities are enhanced. Therefore, it is an inevitable requirement that the application layer presents centralized characteristics.