Original Author: Simon Taylor

Original Translation: Block unicorn

Preface

Every fintech company will become a stablecoin company.

Although stablecoins have sparked various emotions such as hype, suspicion, hope, and concern, I believe we have crossed an important watershed. We are transitioning from the "Banking as a Service" (BaaS) era to an era where stablecoins serve as infrastructure. B2C, B2B, and infrastructure companies centered around stablecoins will shape the industry in the next decade.

This transformation will be ten times more intense than the fintech boom of the past decade.

Because we are moving towards a new infrastructure layer. People still view stablecoins as a new payment channel, but when they see it as a platform that sits above all other layers, we will finally fully transition to a stablecoin-native approach. Stablecoins are a platform.

Key points of this article:

Previous era: Banking as a Service (BaaS) and its insights into stablecoins

Why stablecoins are an infrastructure layer (not just a new channel)

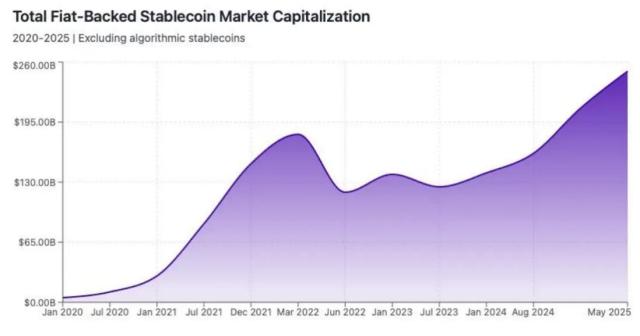

Stablecoin gold rush and regulatory unlocking

Full-stack use cases

Strategic positioning and future outlook

Enterprises unable to adapt to the new platform layer will be commoditized.

The impact of stablecoins on payments is like the internet's impact on telecommunications - creating a platform layer that commoditizes the underlying infrastructure pipeline.

We can see this infrastructure layer gradually emerging in every payment process and business model. Here's how it works.

4. How Stablecoins Play a Role in the Entire System

Yes, stablecoins operate as alternative payment channels today. But this is just the foundation. Most people view them as payment channels in the diagram below, rather than a platform:

Stablecoins as payment channels - they are more than that and have more functions.

The real opportunity lies in the capabilities enabled by their infrastructure.

4.1 Stablecoins for International Payments - Starting Point

Undoubtedly, the primary use case for stablecoins is cross-border payments. The main currency routes are Asian countries, followed by the US to Latin American countries (Mexico, Brazil, Argentina).

G20 leads payment activities to the Global South through TRON and Tether

Cross-border payments come in various types. Let's delve into each payment process.

Early B2B use cases:

Scale-expanding enterprises for market expansion (e.g., SpaceX): Used for financial management, supplier payments, and inter-company payments.

International payroll and payments (e.g., Deel, Remote): Contractors and employers will pay to stablecoin wallets.

Artemis surveyed over 30 companies in the stablecoin business and found that B2B, as a category, grew year-on-year by 400% (and accelerating), making it the fastest-growing category. (Note: The transaction volume shown in the chart represents only a part of the overall market)

As the growth curve shows, this is significant growth.

Currently, the last-mile liquidity and forex spreads are bottlenecks, but new companies like Stablesea, OpenFX, and Velocity are entering the market to change this.

Consumer cross-border stablecoin use cases include:

Remittances and P2P (e.g., Sling Money): Customers use stablecoins for cross-border remittances, faster and often at lower costs.

Stablecoin-linked cards: Also known as "dollar cards", allowing consumers in Southern Hemisphere countries to purchase services from Netflix, ChatGPT, or Amazon.

Artemis's survey also showed that P2P and stablecoin-linked cards grew year-on-year by over 100%, with at least $1 billion in transaction processing volume (TPV) in their sample.

Stablecoins are becoming a feature of new banks (like Revolut and Nubank), though their current use cases remain narrow but may expand in the future. Apps like Revolut, which initially started with remittances and P2P, can fully leverage this new channel due to their unique positioning.

Currently, forex spreads for local currency transactions are typically high, with low liquidity. But this is changing.

The landscape of domestic payments is still forming, but it's fascinating.

4.2 Stablecoins for Domestic Payments (Future Direction)

(Translation continues in the same manner for the rest of the text)The reality is that opportunities vary by use case. Startups are exploring new payment processes, while payment service providers (PSPs) are expanding market access through existing processes. In the future, asset management companies and banks will find their positioning in the market, likely closer to their existing core business.

5. Criticisms, Concerns, and Why Most Are Exaggerated

I will summarize the criticisms as follows:

Criticism: Stablecoins will trigger bank runs. Rebuttal: This assumes Terra-style algorithmic stablecoins, not Treasury-backed permissioned payment stablecoin issuers (PPSIs) under the GENIUS Act.

Criticism: Large tech companies will form a monetary oligopoly. Rebuttal: This is a reasonable concern, but the framework makes it unlikely for large tech companies to directly issue stablecoins—they will use stablecoins, not issue them. Becoming a PPSI presents high regulatory barriers.

Criticism: Will lead to community bank deposit outflows. Rebuttal: Money market funds are already causing this. Community banks that adapt to provide stablecoin services will thrive.

Criticism: "This is crypto," implying it's full of crime and scams. Rebuttal: It's time to abandon this view. The future of finance is on-chain, and institutional capital is building infrastructure. There are genuine, novel risks such as key management, custody, liquidity, integration, and credit risk that should be focused on.

Criticism: Stablecoins are just regulatory arbitrage because "holding USDC should be as hard as holding USD". Rebuttal: Fintech itself achieved regulatory arbitrage through the Durbin Amendment. It's easier to develop on stablecoins, but there's also a comprehensive licensing system.

I believe this debate will continue.

Stablecoins will drive the next era of finance, and our vision of the future has only just begun.

6. Finally, Why Every Company Needs a Stablecoin Strategy

Everything we do today can be stablecoin-native, at which point finance will gain superpowers. We can build instant, global, 24/7 finance. We can recombine financial Lego blocks, and it will be more developer-friendly.

The BaaS era tells us that new infrastructure creates massive opportunities and risks. Companies that learn from the successes and failures of that era will win in the stablecoin-centric era.

Every company needs a stablecoin strategy. Every fintech company, every bank, every finance team needs one. Because this is not just a new payment channel. It is the platform layer upon which everything else will be built.

I implore every reader to build based on lessons from the past.

Collapses are inevitable, and things will go wrong, which is also inevitable.

This includes how you will protect yourself when things inevitably collapse.

Build cool things.

And stay safe.