The May non-farm employment report was robust, with 139,000 new jobs added, higher than Wall Street's expected 126,000, but new positions were mainly concentrated in leisure, entertainment, and healthcare sectors, while government departments and manufacturing experienced net job losses. The data details appear slightly weak, with unemployment rate rising from 4.19% to 4.24%. If not for the decline in labor participation rate, unemployment rate could have been close to 4.6%.

The non-farm employment data performed better than recent unemployment benefit application data, with stock markets and US Treasury yields rising simultaneously, despite hard data finally beginning to align with soft survey data. Additionally, with geopolitical risks cooling since "Liberation Day" and tensions within the Trump camp, the market has once again entered a "bad news = good news" mode, continuously seeking reasons for further Federal Reserve rate cuts.

Although the passage of the "Big Beautiful Bill" still carries risks, market sentiment has rebounded to peak levels, with volatility index and credit spreads both falling to historical lows. The VIX's crash speed is among the fastest in history, even surpassing the pandemic period, with the US dollar being the primary victim, significantly weakening due to policy reversals after Liberation Day.

Regarding the US dollar, we are entering a new correlation mechanism where stock prices begin to positively correlate with the dollar, a rare occurrence and the first sustained structural change since the pandemic. This reflects market concerns about potential implications of Trump's policy reversals on US assets, making current US stock performance more influenced by international capital flows rather than Federal Reserve rate change expectations.

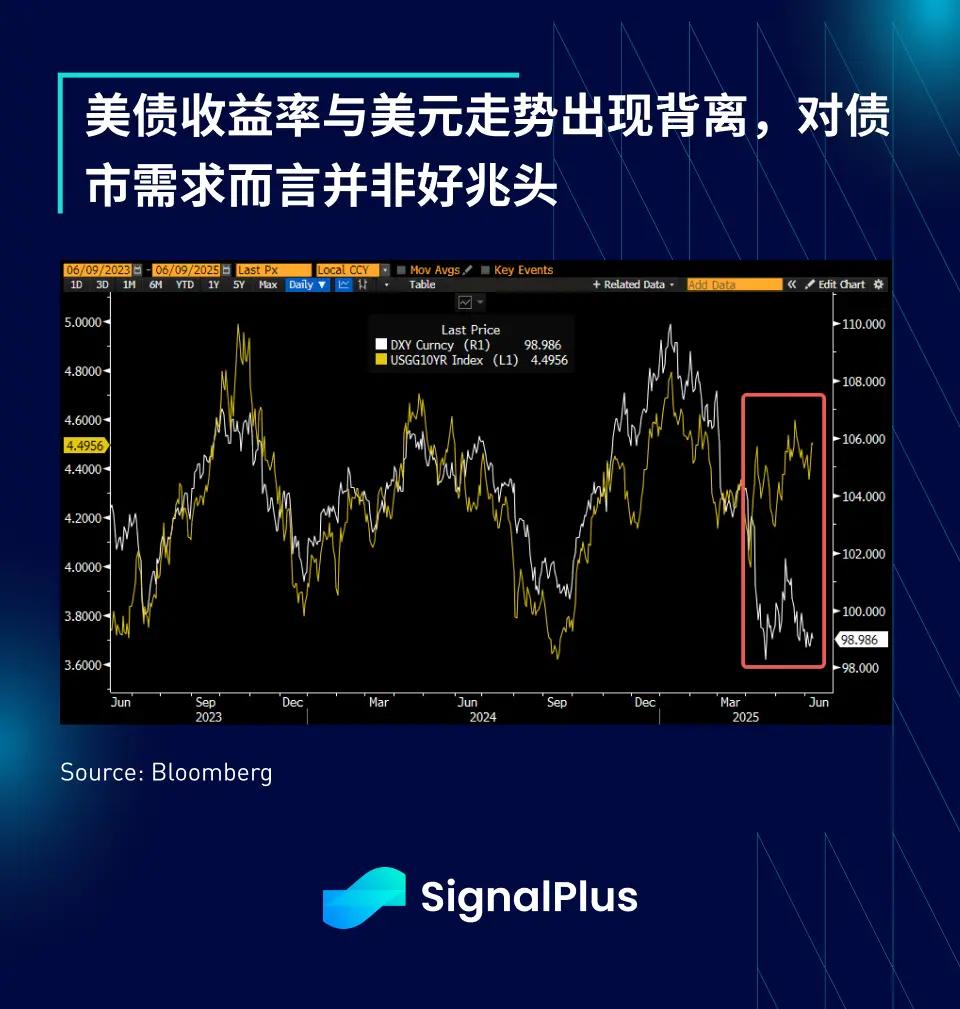

In the bond market, yields typically move in sync with the dollar under non-crisis conditions. However, since "Liberation Day", this correlation has been broken, with yields continuing to rise despite a weakening dollar, which traditionally signals potential future Federal Reserve rate cuts. This divergence may persist until there are more definitive results on budget expenditure bills and whether the Trump administration can reach trade agreements in the coming months.

This week will be a crucial litmus test for market risks. Mid-week will see long-term US Treasury bond auctions, accompanied by US-China trade negotiations restarting after recent escalations. Any trade negotiation progress is expected to focus on breakthroughs in rare earth supply, while the bond market must simultaneously handle the upcoming CPI data and supply pressure from 10-year and 30-year bond issuances.

The market currently expects core CPI to grow by 0.25% month-on-month, with cost-push effects from tariffs likely to manifest only in late summer, providing a basis for the Federal Reserve to restart rate cuts in the third or fourth quarter.

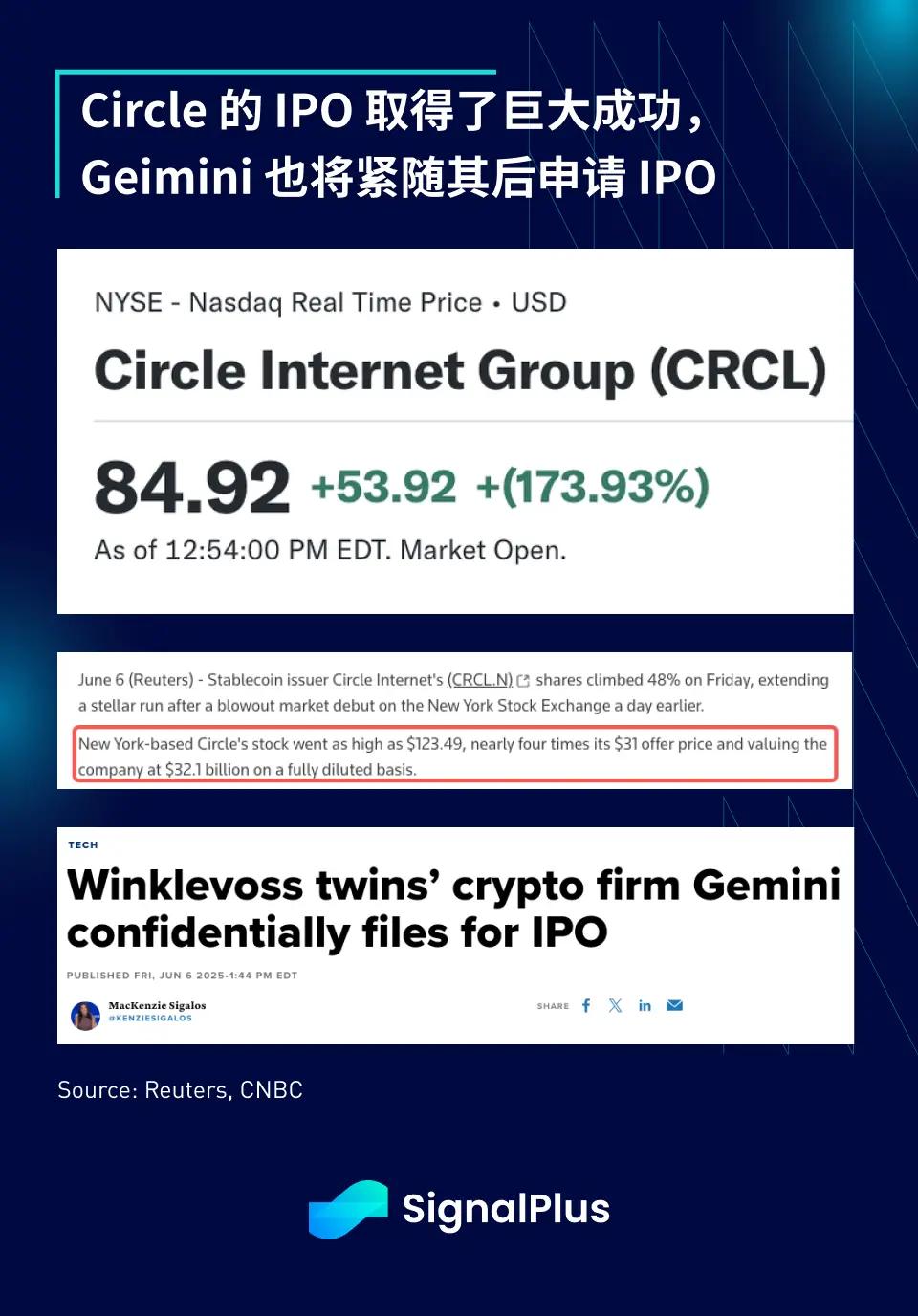

In the cryptocurrency sector, last week saw significant volatility, with few highlights in the blockchain native domain. The main focus was on traditional financial areas, including Circle's IPO and banking business dynamics. ETF fund flows for BTC showed mixed performance, while ETH performed more positively, recording net inflows for 14 consecutive days, totaling over $800 million, with CME's ETH futures open interest also reaching a historical high.

Circle's IPO was hugely successful, with stock prices surging nearly 4-fold post-listing, reaching a market value of around $32 billion. Cryptocurrency banking was also active, with Robinhood completing a $200 million acquisition of Bitstamp, and Gemini filing an IPO application in the hot public market atmosphere.

It's worth noting that we don't believe this provides a unilateral bullish reason for assets like BTC or ETH, as general investors now have more ways to access cryptocurrency assets, whether through ETFs, MSTR, or other BTC proxy tools. Compliant exchanges and regulated stablecoin issuers are also about to emerge. As cryptocurrency assets gradually mature and become an investable macro asset class, the current cycle will only become more complex and diverse.

Wishing everyone a successful and lucky trading week!