Welcome back to our blog series for founders building at the frontier of AI and Web3. From stablecoins to smart wallets, OpenFi is the final piece of the agentic internet puzzle. Learn how founders are shaping the next financial stack.

Authors: Jasper De Maere | X | LinkedIn | Greysen Cacciatore | X | LinkedIn

As agents take on real financial workflows, we need systems designed to support autonomy at scale. OpenFi marks the next stage: a composable, intelligent layer for value coordination across the Post Web. Think of it as DeFi, rebuilt for AI agents.

Open Finance represents the consumer-facing layer of The Post Web financial stack. It’s where intuitive, cost-efficient financial apps meet users and agents, directly. Beneath it, DeFi serves as the peer-to-peer orchestration layer, enabling the permissionless exchange of value between agents and economic actors.

As AI agents begin managing financial activity on behalf of users, this dual stack becomes essential. OpenFi abstracts complexity at the front, while DeFi powers intelligent, modular, and programmable value flows in the back. Together, they form the foundation for intent-driven financial experiences in a decentralized, agent-operated economy. (Also read: OpenFi, fintech’s endgame)

Missed earlier posts in the series?

- Blog 1: What Founders Need to Know – A thesis-level view of The Post Web and why this cycle is different

- Blog 2: The Agentic Internet – Why agents are the new users of the internet

- Blog 3: DePIN Infrastructure – How decentralized infra brings agents into the real world

- Blog 4: Real World Assets – Why tokenization is becoming the bedrock of agentic commerce

TL;DR – Why OpenFi Is Emerging Now

OpenFi is reaching a tipping point as several foundational components converge. Four key trends are driving the shift:

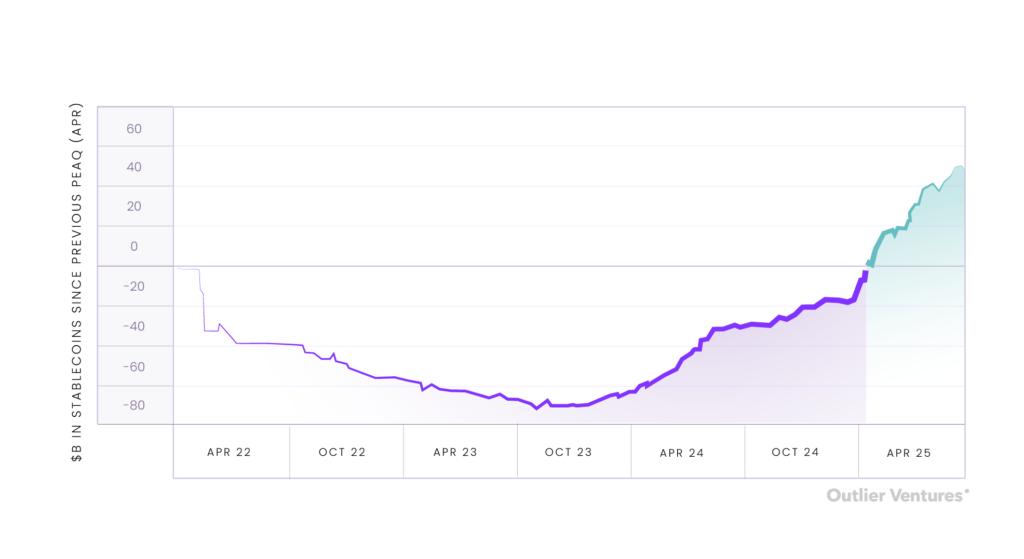

- Mechanisms of Exchange: Stablecoins are gaining regulatory clarity and adoption, becoming the default medium of exchange for on-chain activity.

Exhibit 1: Change in stablecoin circulation since previous peak in April 2022. Since late 2023, we’ve seen a continued strong momentum in stablecoins ($b) in circulation

- Scaling: With L2s and rollups maturing, transaction costs are dropping exponentially, enabling everyday (low value) financial transactions like payments, remittances & wage streaming.

Exhibit 2: Daily average User Operations Per Second (UOPS) on Ethereum and its Roll Ups over time. It’s showing the stepchange is scalability and usage of ETH based RUs which accelerated ~4x since the start of 2024.

- Consumer Finance Inflection: Consumer finance is reaching an inflection point, and blockchain-powered OpenFi is perfectly positioned to meet rising demand for transparent, user-centric financial services.

Exhibit 3: Below is the total addressable market (TAM) in Billions (USD) for Neobanks from 2024 to 2034. Precedence Research estimates a 40% CAGR, with TAM reaching roughly 4.4 Trillion USD by 2034.

- Smart Wallets: Smart wallets and AI-powered interfaces are making DeFi and OpenFi more accessible by simplifying account management, transactions and decision-making.

Open Finance is reaching a tipping point as several foundational components fall into place. Stablecoins have emerged as the default mechanism of exchange on-chain, with growing regulatory clarity and widespread adoption creating a solid foundation for day-to-day financial activity. At the same time, scaling solutions have matured, reducing transaction costs to the point where low-value use cases like payments, remittances, and savings are economically viable, especially in emerging markets where traditional financial infrastructure is either broken or inaccessible. Neobanks are also entering the picture, adopting crypto rails and semi-custodial models that make them natural aggregation layers for bringing OpenFi to the masses.

In the context of The Post Web, OpenFi becomes more than a decentralized financial system, it becomes the financial coordination layer for agents. AI-powered agents and smart wallets are beginning to abstract the complexity of DeFi, making it possible for users to delegate financial tasks to autonomous systems that can transact, earn, lend, and manage capital on their behalf. OpenFi protocols, when designed to be modular, composable, and machine-readable, are primed to become the backend infrastructure for intelligent financial automation. As the Post Web shifts economic activity from manual interfaces to autonomous intent execution, OpenFi will be a critical enabler of financial inclusion, precision, and programmability at global scale.

Key Trends Shaping OpenFi

Here’s where founders should pay attention next.

Emerging Markets

OpenFi offers a faster, cheaper, and more inclusive alternative to legacy financial systems, making it especially compelling in underbanked regions like LatAm and Africa, where consumer finance dominates and dApps are well-suited to meet growing demand for accessible, user-driven financial services.

Exhibit 4: Distribution of financial application in Latam across consumer, enterprise & specialized. Latam is an example of emerging markets with a heavy skew towards consumer-facing financial applications.

Neobanks Go Crypto

Neobanks adopt crypto-native rails and semi-custodial solutions, they are positioned to become onboarding layers for Openfi at scale.

AI & Security

AI is helping DeFi and OpenFi applications smarter through stronger risk management and fraud detection systems.

Novel Models

Novel models of DeFi are emerging at the application (DEXs) and governance levels (treasury management), further strengthening the ecosystem.

Design Space for Founders

The opportunity isn’t just theoretical. Builders are already pushing the boundaries of OpenFi across three major vectors:

1. Fat Wallets: The New Neobanks

A modular financial operating system where the wallet is the user’s gateway to compliant, composable, and cross-chain finance.

Wallets are quickly evolving from basic crypto storage tools into comprehensive financial hubs, functioning much like the neobanks of Web3. Powered by trends such as account abstraction, stablecoin adoption, and growing demand for seamless DeFi access, wallets are becoming true control centers for decentralized finance. They allow users to complete KYC, manage assets, grant consent to dApps, and execute transactions across multiple chains, all from a single interface.

As the ecosystem matures, new features are emerging around cross-chain abstraction, FX-denominated stablecoins for emerging markets, and integrated KYC solutions that combine compliance with composability. Wallets are now positioned to become the primary interface for interacting with decentralized applications and financial infrastructure, offering users a modular, secure, and highly personalized experience.

2. Agentic Finance

Projects building agentic finance infrastructure enabling autonomous, composable financial agents that can operate on behalf of users, protocols, or institutions.

Agentic finance is an emerging area where builders are creating intelligent agents that can reason, execute, and manage financial workflows autonomously. These agents can be programmed to optimize yield, rebalance portfolios, manage liquidity positions, and offer research insights. While the idea is compelling, the infrastructure is still nascent. Today’s implementations are mostly experimental, with limited applications that optimize for performance, transparency, and effective coordination of agents. If done right, agentic finance could unlock a new layer of intelligence within finance, allowing users to leverage agents to make informed investment decisions and manage their portfolios.

3. Privacy-Enhanced Transactions

Projects embedding privacy into open finance to ensure user control, regulatory compliance, and scalable trust in a transparent-by-default system.

While blockchains are built for transparency, that very strength can become a liability, especially in consumer-facing financial applications. Privacy plays a critical role in open finance. It protects sensitive financial information, reinforcing individual autonomy and control. It also helps meet compliance standards and builds the trust needed for broader adoption. To make open finance viable at scale, users must be empowered with tools that allow for baseline transactional privacy. This could involve a mix of privacy-preserving technologies, from zero-knowledge proofs to privacy pools and mixers. We believe the most effective solutions will thoughtfully combine these approaches to balance transparency with discretion.

Founder Implications

OpenFi is no longer just a DeFi upgrade, it’s the new coordination layer for financial autonomy in The Post Web. If you’re building:

- Financial agents

- Smart wallets

- Modular fintech rails

You’re already part of the OpenFi movement. Now’s the time to lead it.

Ready to Build the Financial Layer of the Future?

If you’re designing financial systems for an agent-driven internet, you’re already building OpenFi. Now join the teams leading it.

Post Web Base Camp is the only accelerator built for founders shaping the autonomous, decentralized future. We offer:

- Capital to accelerate your roadmap

- Hands-on support from DeFi and infra specialists

- A strategic network of investors, protocols, and distribution partners

Founders from previous cohorts have gone on to raise multi-million dollar rounds, ship across chains, and become category leaders.

Want to get the rest of this series in your inbox? Subscribe to our newsletter and stay ahead of the curve.

The post OpenFi: The Financial Stack for Agentic Automation appeared first on Outlier Ventures.