Written by: TechFlow

The sentiment of the crypto market is once again focused on regulatory actions.

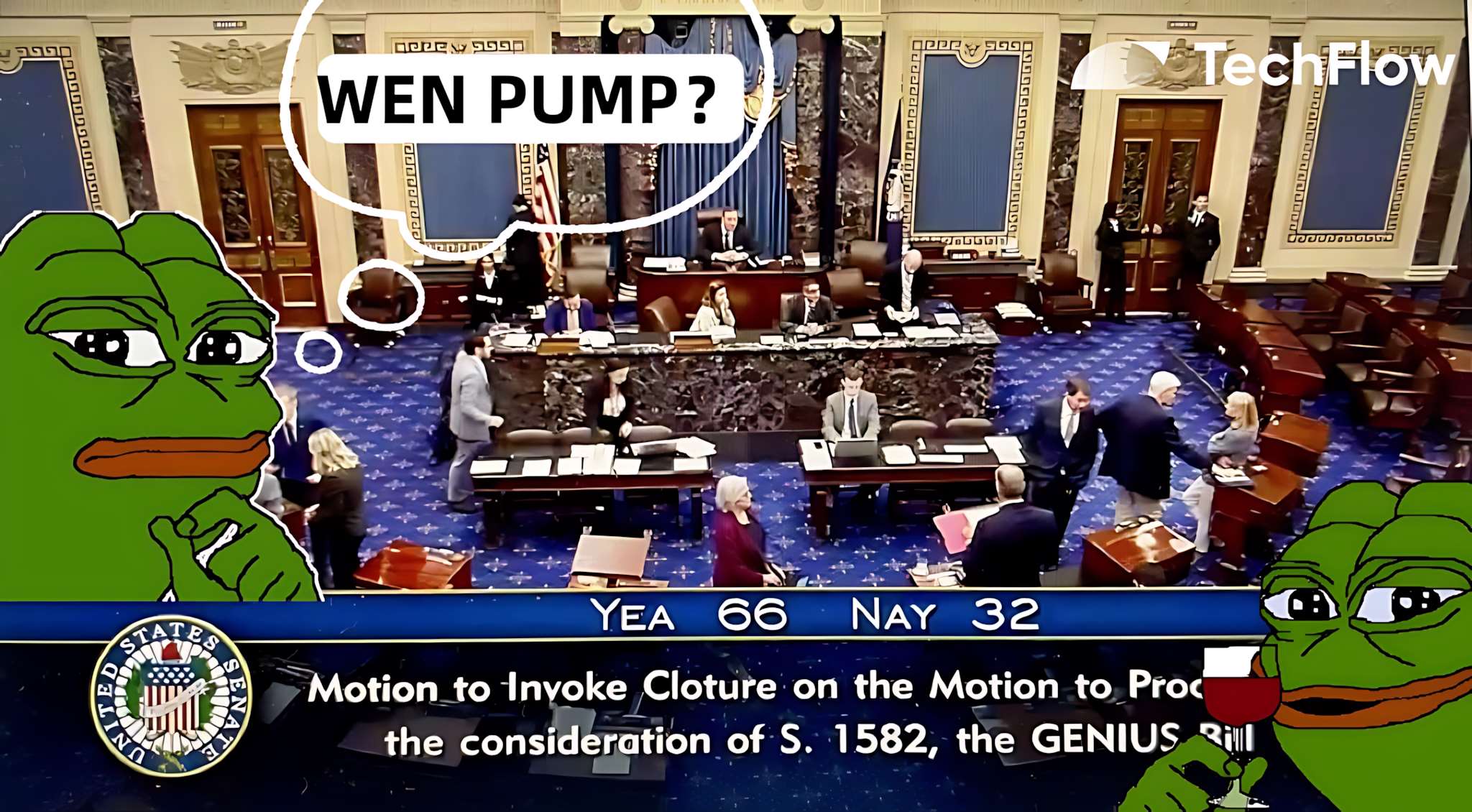

On May 19, the U.S. Senate passed the procedural vote for the GENIUS Act with a vote of 66-32, marking a milestone in the imminent implementation of the U.S. stablecoin regulatory framework.

As the first comprehensive federal stablecoin regulatory bill in the United States, the rapid advancement of the GENIUS Act has sparked heated responses in the crypto market, with DeFi and RWA sectors related to stablecoins leading today's market.

Will the GENIUS Act become a catalyst for the next bull market?

According to Citibank's forecast, the global stablecoin market size is expected to reach $1.6 to $3.7 trillion by 2030. The passage of the bill provides more "compliance" qualifications and development space for stablecoins, giving traditional companies a more reasonable reason to enter.

The market is also expecting incremental funds to bring a "flood of liquidity" and inject new liquidity into related crypto assets.

But before that, you should first understand the contents of this bill and its legislative motivation to provide a more convincing reason for selecting related crypto assets.

From "Wild Growth" to Standardization

The GENIUS Act, literally translated as the "Genius Act," is actually an abbreviation for the Guiding and Establishing National Innovation for U.S. Stablecoins Act of 2025.

In simpler terms, it is a national legislative document of the United States.

The market's attention is due to it being the first comprehensive federal regulatory bill for stablecoins in U.S. history. Before this, stablecoins and cryptocurrencies had been in a subtle gray area:

If not explicitly prohibited, it could be done, but there were no clear rules on "how to do it".

The goal of the GENIUS Act is to provide legitimacy and safety to the stablecoin market through a clear regulatory framework, while consolidating the dollar's dominance in digital finance.

In summary, the key contents of the bill include:

Reserve Requirements: Stablecoin issuers must have 100% reserve support, with reserve assets being U.S. dollars, short-term U.S. Treasury bonds, and other highly liquid assets, with monthly public disclosure of reserve composition.

Regulatory Tiering: Large issuers with a market cap over $10 billion (such as Tether, Circle) must be directly regulated by the Federal Reserve System or the Office of the Comptroller of the Currency (OCC), while smaller issuers can be regulated by states.

Transparency and Compliance: Prohibiting misleading marketing (such as claiming stablecoins are guaranteed by the U.S. government), and requiring issuers to comply with Anti-Money Laundering (AML) and Know Your Customer (KYC) regulations. Issuers with a market cap over $50 billion need annual audits of financial statements to ensure transparency.

This means that the U.S. attitude towards stablecoins is actually friendly, but with the premise that stablecoins must have U.S. dollars as reserves and meet open and transparent requirements.

[... rest of the translation continues in the same manner]$FXS (Frax Finance, issuing FRAX): FRAX has a market cap of about $2 billion, using a partial algorithmic mechanism (50% collateralized, 50% algorithmic), with about 15% of collateral assets in US Treasuries (approximately $300 million). If Frax adjusts to a fully collateralized mode and increases the proportion of US Treasuries, it could benefit from market expansion, but its algorithmic mechanism may face regulatory pressure, as the bill does not protect algorithmic stablecoins.

$ENA (Ethena Labs, issuing USDe): USDe has a market cap of about $1.4 billion, issued through ETH hedging and yield strategies, with only 5% of reserves in US Treasuries (approximately $70 million).

Its strategy may need significant adjustments to comply with the bill requirements. If successful, it could benefit from market growth, but risks remain.

DeFi Trading/Lending

$CRV (Curve Finance): Curve focuses on stablecoin trading (TVL of about $2 billion in 2025), with 70% of its liquidity pools being stablecoin trading pairs (such as USDT/USDC).

The increase in stablecoin usage driven by the GENIUS Act will directly boost Curve's trading volume (currently around $300 million daily), with $CRV holders benefiting from trading fees (approximately 5% annual yield) and governance rights. If the stablecoin market grows as predicted by Citigroup, Curve's TVL could increase by another 20%.

$UNI (Uniswap): Uniswap is a universal DEX (TVL of about $5 billion in 2025), with stablecoin trading pairs (such as USDC/ETH) accounting for 30% of its liquidity. The increased stablecoin trading activity brought by the bill will indirectly benefit Uniswap, but to a lesser extent than Curve (due to more diversified business), with $UNI holders benefiting from trading fees (approximately 3% annually).

$AAVE (Aave): Aave is the largest lending protocol (TVL of about $10 billion in 2025), with stablecoins (such as USDC, DAI) accounting for about 40% of its lending pool.

The bill's passage will attract more users to use stablecoins for lending (such as collateralizing USDC to borrow ETH), potentially further increasing Aave's deposits and borrowings (based on current trends). $AAVE holders will benefit from protocol revenue (approximately $150 million in annual revenue in 2025) and token value appreciation.

$COMP (Compound): Compound's TVL is about $3 billion, with stablecoin lending accounting for about 35%. Similar to Aave, increased stablecoin lending will benefit Compound, but its market share and innovation speed are lower than Aave, with $COMP's potential appreciation potentially being relatively smaller.

Yield Protocols

$PENDLE (Pendle): Pendle focuses on yield tokenization (TVL of about $500 million in 2025), with stablecoins commonly used in its yield strategies (such as USDC yield pool, currently with an annual yield of about 3%). The stablecoin market growth driven by the bill will increase Pendle's yield opportunities (with yields potentially rising to 5%), with $PENDLE holders potentially benefiting from increased protocol revenue (approximately $30 million in annual revenue in 2025).

Layer 1

$ETH (Ethereum): Ethereum carries 90% of stablecoin and DeFi activities (DeFi TVL exceeding $100 billion in 2025). The increase in stablecoin usage driven by the bill will boost Ethereum's on-chain transaction volume (current gas fee annual revenue of about $2 billion), with $ETH value potentially rising due to increased demand.

$TRX (Tron): Tron is an important network for stablecoin circulation, with public data showing USDT circulation of about $60 billion on the Tron chain in 2025, accounting for 46% of total USDT. The increase in stablecoin usage may enhance Tron's on-chain activity.

$SOL (Solana): Solana has become an important platform for stablecoins and DeFi due to its high throughput and low cost (TVL of about $8 billion in 2025, with on-chain USDC circulation of about $5 billion). Increased stablecoin usage will drive Solana's DeFi activity (current daily average transaction volume of about $1 billion), with $SOL potentially benefiting from increased on-chain activity.

$SUI (Sui): Sui is an emerging Layer 1 (TVL of about $1 billion in 2025), supporting stablecoin-related applications (such as Thala's stablecoin and DEX). The growth of the stablecoin ecosystem driven by the bill will attract more projects to deploy on Sui, with $SUI potentially benefiting from increased ecosystem activity (current daily active users of about 500,000).

$APT (Aptos): Aptos is also an emerging Layer 1 (TVL of about $800 million in 2025), with its ecosystem supporting stablecoin payments. Increased stablecoin circulation will drive Aptos' payment and DeFi applications, with $APT potentially benefiting from user growth.

Payment Track

$XRP (Ripple): XRP focuses on cross-border payments (daily average transaction volume of about $2 billion in 2025), with its low cost and high efficiency complementing stablecoins. The increased demand for stablecoin cross-border payments driven by the bill (such as using USDC for international settlement) will indirectly enhance XRP's use cases (such as serving as a bridge currency), with $XRP potentially benefiting from increased payment demand.

$XLM (Stellar): Stellar also focuses on cross-border payments (daily average transaction volume of about $500 million in 2025), having previously collaborated with IBM to launch the World Wire project, using stablecoins as bridge assets.

Oracles

$LINK + $PYTH: Oracles provide price data for stablecoins and DeFi. The expansion of the stablecoin market driven by the bill will increase the demand for real-time price data in DeFi, potentially increasing on-chain data call volume.

However, this is more like an extension of sector-wide benefits, rather than a completely strong correlation.

RWA

$ONDO (Ondo Finance): Focusing on tokenizing fixed-income assets like US Treasuries, its flagship product USDY (a US Treasury-backed stable yield token) has been issued on chains like Solana and Ethereum (USDY circulation of about $500 million in 2025). The GENIUS Act's requirement for stablecoin reserves to hold US Treasuries directly benefits Ondo's US Treasury tokenization business, with USDY potentially becoming a preferred reserve asset for stablecoin issuers. Additionally, increased stablecoin circulation will drive retail and institutional purchases of USDY through USDC, potentially increasing demand for Ondo's asset tokenization, with $ONDO holders benefiting.

The Dollar: A Larger Yangmou (Overt Strategy)

The United States' push for stablecoin legislation can be considered a "yangmou".

On one hand, the US wants a weak dollar policy to increase exports, while on the other hand, it doesn't want to give up the global monetary status of the dollar.

By supporting stablecoin development, the US has extended the global influence of the dollar in a digital manner without increasing the Federal Reserve's liabilities - currently, 99% of stablecoins are pegged to the US dollar.

Simultaneously, the regulatory requirement for stablecoins to hold US short-term Treasury bonds as reserves cleverly finds new buyers for US debt, as the scale of US Treasuries held by Tether has already exceeded that of many developed countries.

This policy maintains the global dominance of the dollar while finding reliable buyers for the US's massive debt, truly killing two birds with one stone.

The passage of the GENIUS Act is undoubtedly a milestone in the crypto market, providing a new path for the continuation of US dollar hegemony through the binding of stablecoins and US Treasuries, while simultaneously driving the comprehensive prosperity of the crypto ecosystem.

However, this "yangmou" is a double-edged sword - while bringing opportunities, its high dependence on US Treasuries, potential suppression of DeFi innovation, and uncertainties in global competition could become future hidden dangers.

Yet, uncertainty has always been a stepping stone for the crypto market's progress.

Risks may be uncertain, but participants are waiting for a definitive bull market to arrive.