Author | @Web3_Mario

Abstract: As Trump's policies are being gradually implemented, attracting manufacturing back through tariffs, actively bursting the stock market bubble to force the Federal Reserve to lower interest rates, and promoting financial innovation through deregulation to accelerate industrial development, this combination of strategies is substantially changing the market. The RWA track under the favorable deregulation policy is increasingly attracting attention in the crypto industry. This article mainly introduces the opportunities and challenges of tokenized stocks.

Overview of Tokenized Stocks Development History

In fact, tokenized stocks are not a new concept. Since 2017, attempts at Security Token Offering (STO) have begun. STO is a financing method in the cryptocurrency field, essentially digitizing and chaining the equity of traditional financial securities through blockchain technology to tokenize assets. It combines the compliance of traditional securities with the efficiency of blockchain technology. As an important securities category, tokenized stocks are the most notable application scenario in the STO field.

Before STO, the mainstream financing method in the blockchain field was ICO (Initial Coin Offering). The rapid rise of ICO mainly relied on the convenience of Ethereum smart contracts, but most tokens issued did not represent real asset rights and lacked regulation, leading to frequent fraud and project abandonment.

In 2017, the US SEC issued a statement regarding the DAO incident, indicating that certain tokens might be securities and should be regulated under the 1933 Securities Act. This marked the formal emergence of the STO concept. In 2018, STO began to be recognized as a "compliant ICO" and gained industry attention. However, due to lack of unified standards, poor secondary market liquidity, and high compliance costs, market development was slow.

With the arrival of DeFi Summer in 2020, some projects began attempting decentralized solutions, creating derivatives linked to stock prices through smart contracts, allowing on-chain investors to directly invest in traditional stock markets without complex KYC processes. This paradigm is usually called the synthetic asset model, which does not directly hold US stocks and requires no trust in centralized institutions, thus avoiding expensive regulatory and legal costs. Representative projects include Synthetix and Mirror Protocol in the Terra ecosystem.

In these projects, market makers could mint on-chain synthetic US stocks by providing over-collateralized crypto assets and provide market liquidity, while traders could directly trade these assets on DEX secondary markets to gain exposure to the anchored stock prices. At that time, Tesla was the most prominent stock in the market, not NVIDIA from the previous cycle. Therefore, most projects' slogans emphasized direct on-chain TSLA trading.

However, the trading volume of on-chain synthetic US stocks has always been unsatisfactory. Taking sTSLA on Synthetix as an example, including primary market minting and redemption, its total cumulative on-chain transactions were only 798. Most projects subsequently claimed to delist US stock synthetic assets due to regulatory considerations and shifted to other business scenarios, but the essential reason was likely the failure to find product-market fit and establish a sustainable business model.

Besides the synthetic asset model, some well-known CEXs have been attempting to provide US stock trading capabilities for crypto traders through centralized custody models. This model involves third-party financial institutions or exchanges custodying actual stocks and creating tradable assets directly on CEX. Notable examples include FTX and Binance. FTX launched tokenized stock trading services on October 29, 2020, collaborating with German financial company CM-Equity AG and Swiss Digital Assets AG, allowing non-US users to trade tokens linked to US-listed company stocks. In April 2021, Binance also began offering tokenized stock trading services, with Tesla (TSLA) being the first listed stock.

However, the regulatory environment was not particularly friendly at the time, and since the core initiators were CEXs, they directly competed with traditional stock trading platforms like Nasdaq, facing significant pressure. FTX's tokenized stock trading volume reached its historical peak in the fourth quarter of 2021, with October 2021 trading volume at $94 million. However, after its bankruptcy in November 2022, its tokenized stock trading service stopped. Binance also ceased its tokenized stock trading service in July 2021, just three months after launching, due to regulatory pressure.

Subsequently, as the market entered a bear market phase, the track's development stagnated. Until Trump's election and his deregulatory financial policies brought a change in the regulatory environment, reigniting market interest in tokenized stocks, now known as RWA. This paradigm emphasizes creating tokens backed 1:1 by real-world assets through a compliant architectural design, with approved issuers launching tokens on-chain, and token creation, trading, redemption, and underlying asset management strictly following regulatory requirements.

Current Market Status of Stock RWA

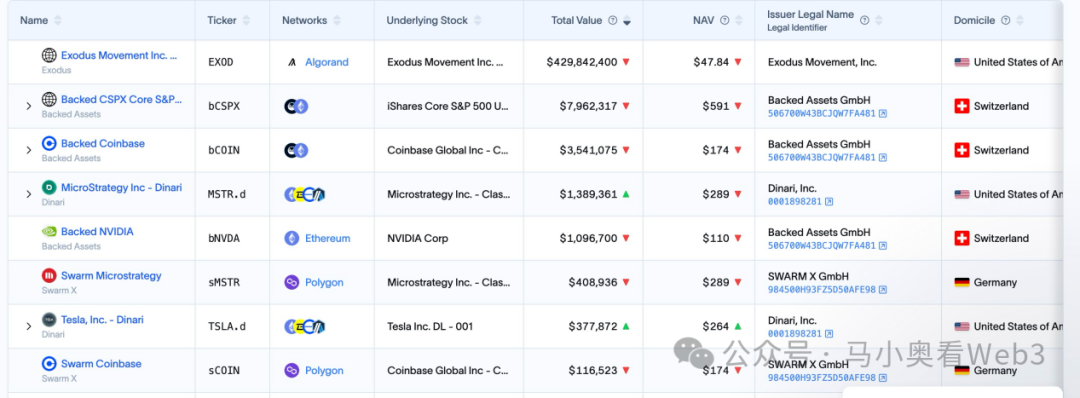

Let's introduce the current market status of stock RWA. Overall, the market is still in its early stages and primarily focused on US stocks. According to RWA.xyz data, the current stock RWA total issuance reaches $445.40M, but notably, $429.84M is attributed to one asset, EXOD, issued by Exodus Movement, Inc., a software company focusing on self-custodial crypto wallets, founded in 2015 and headquartered in Nebraska, USA. The company's stock is listed on NYSE America and allows users to migrate its common A-class shares to the Algorand blockchain, with users able to view on-chain asset prices directly in the Exodus Wallet. The company's total market value is $1.5B.

The company has become the only US company to tokenize its common stocks on the blockchain. However, it's worth noting that the on-chain EXOD is merely a digital identifier of its stock and does not include voting, governance, economic, or other rights, and the Token cannot be directly traded or circulated on-chain.

This event is significant, indicating a clear shift in the SEC's attitude towards on-chain stock assets. In fact, Exodus's attempt to issue on-chain stocks was not smooth. In May 2024, Exodus first submitted an application for common stock tokenization, but due to the SEC's previous regulatory policy, the on-chain plan was initially rejected. However, in December 2024, after continuously improving the technical solution, compliance measures, and information disclosure, Exodus finally received SEC approval and successfully completed the tokenization of common stocks. This event also drove the company's stock price to a historical high.