Author: Alex, Mint Ventures

Introduction: The necessity of paying attention to the RWA track at this moment

In this round of crypto cycle with little innovation, we did not see new tracks like Defi, NFT and even Gamefi in the previous round. Meme speculation has become the main hot spot of market transactions. However, with the mass production of projects, the continuous acceleration of liquidity extraction rhythm and the exhaustion of themes, the Meme market has also entered a doomed depression cycle. As many AI projects, which are new themes in this round, have not yet found the right product fit between Crypto and AI, the business logic of the track is fragile, and it is difficult to attract long-term industrial investment and long-term funds.

The complete failure of commercial exploration in the Web3 track and the lack of investment narratives with solid industrial logic are the main reasons why most crypto assets other than BTC have entered the "bear market" ahead of schedule. The depression of the application track has also directly led to the continuous decline in the valuation of public chain platforms that carry applications, causing the exchange rate of public chain assets represented by ETH against BTC to continue to fall.

At the same time, BTC has benefited from multi-dimensional improvements in fundamentals (opening of compliant investment channels, government reserves, inclusion in the balance sheets of listed companies and sovereign funds, friendly regulation...). After experiencing a mid-term correction for several months, it has now returned to near new highs and accumulated relatively generous unrealized profits.

However, the need to cash in part of the profits of this part of funds and find more flexible copycat assets for layout still exists.

The question is, what to buy?

Compared with other encryption tracks horizontally, RWA may be one of the key categories that deserves more attention.

In the article "U.S. Stocks on the Blockchain and STO: A Hidden Narrative", the author explained the thinking behind this: From a business logic perspective, the value proposition of tokenization of U.S. stocks and more RWA assets is clear, and the needs of both supply and demand are relatively clear; in addition, the improvement of the regulatory environment represented by the United States has provided an opportunity for the outbreak of this track, and influential traditional financial institutions are eager to try it.

Based on this, the author has recently conducted research on many RWA projects, and Ondo, as a representative project among them, deserves special analysis.

In the report, I will analyze Ondo’s business status, team background, competition, challenges and risks, and compare its current valuation level with other projects in the same track.

PS: This article is the author’s interim thinking up to the time of publication. It may change in the future, and the views are highly subjective. There may also be errors in facts, data, and reasoning logic. All views in this article are not investment advice. Criticism and further discussion from colleagues and readers are welcome.

1. Business status

1.1 Product Matrix

Ondo Finance is an institutional-level platform that focuses on tokenizing traditional financial assets (Real-World Assets, RWA) and introducing them into blockchain. It is also the representative project with the highest brand awareness and the most complete product line among the RWA projects that have issued tokens.

Ondo's products include tokenized funds, interest-bearing stablecoins, lending platforms, tokenized asset issuance protocols, tokenized asset trading platforms and its own compliant blockchain, covering all aspects of RWA from issuance, custody to trading circulation.

We can also divide its products into asset, protocol and infrastructure categories.

Next, let’s take a look at Ondo’s current main products.

1.1.1 Asset products

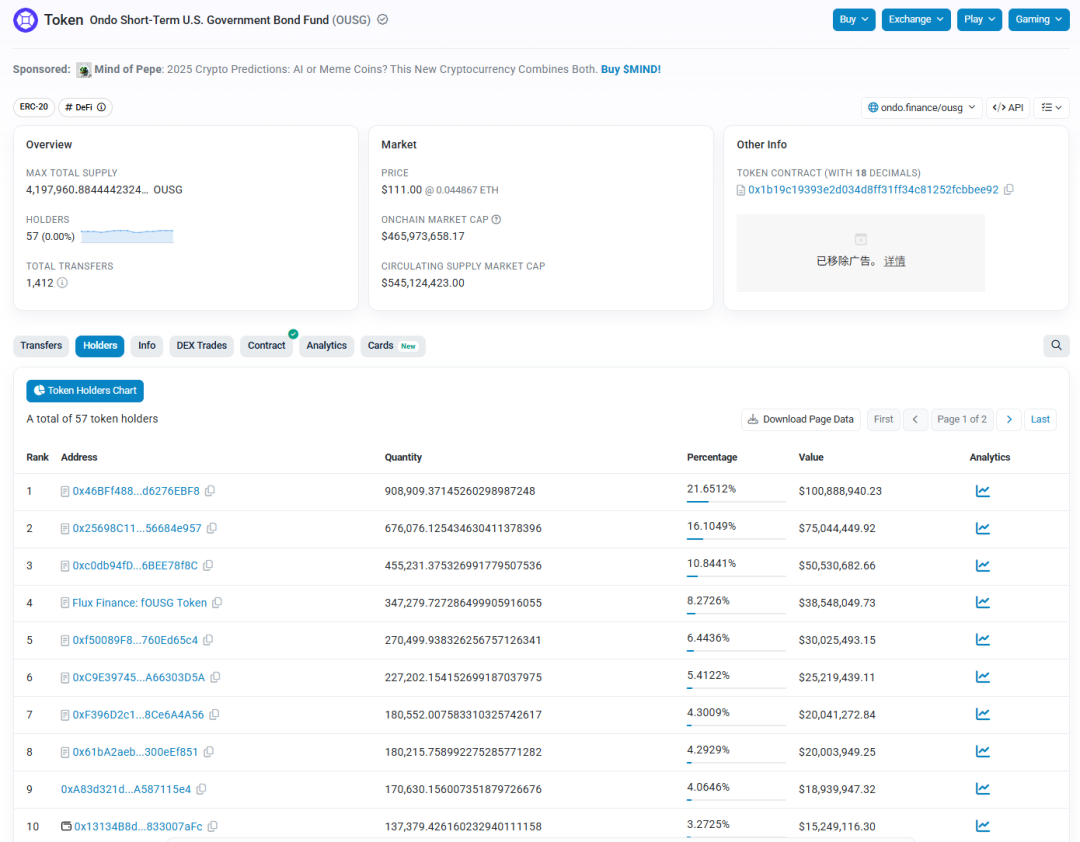

OUSG (Ondo Short-Term US Government Bond Fund )

A token backed by U.S. Treasury bonds, issued to qualified purchasers, requiring strict KYC/qualified investor certification. When investors purchase OUSG, it is equivalent to holding a share of a portfolio of short-term U.S. Treasury assets invested by professional fund managers. The intrinsic value of OUSG tokens will increase with the increase in the net value of the fund, which is equivalent to automatically rolling in interest income every day. In addition to BlackRock BUIDL U.S. Treasury Fund, OUSG's underlying assets also include U.S. Treasury shares issued by Franklin Templeton (FOBXX), Wellington, WisdomTree, Fidelity, etc. as reserve assets.

OUSG’s profit model

OUSG charges institutional clients a management fee of 0.15% (currently not levied, levied starting July 1, 25) and fund expenses (also 0.15%, levied in progress). Its actual income is generated by deducting these fees from the underlying U.S. Treasury interest.

USDY (US Dollar Yield)

Yield-generating USD stablecoin. USDY is issued to non-US individuals and institutional users, and its income is supported by short-term US Treasury bonds and bank deposit interest. The base price of USDY is $1, but the interest is included in the token value in a daily settlement, allowing holders to automatically obtain income . Therefore, users do not need to pledge or lock USDY, and holding USDY can automatically accumulate income every day. The income calculation of USDY is usually based on the risk-free interest rate (SOFR) minus a fee of 0.5%.

USDY’s profit model

Ondo sets the annualized yield of USDY every month (such as 4.25% in a certain month), distributes most of the basic income to coin holders, and retains about 0.5 percentage points as management fees.

In addition, both OUSG and USDY can be converted into stable value tokens with rebase functions, namely rOUSG and rUSDY. Their value will remain unchanged, but the number of tokens will increase as the income increases, similar to Lido's stETH mechanism.

Differentiated positioning of OUSG and USDY

Although OUSG and USDY are very similar products in terms of definition, both of them invest funds in high-quality cash equivalents such as short-term U.S. Treasury bonds, they actually differ in several aspects and have different positioning:

Difference in asset composition : OUSG indirectly invests in U.S. Treasuries by holding shares of multiple regulated government bond funds (such as the Buidl Fund issued by BlackRock and WTGXX issued by WisdomTree). Its portfolio is diversified and entirely composed of government-related securities. In contrast, USDY adopts a direct holding strategy, with most of its assets being a combination of bank deposits + short-term government bonds. USDY does not invest in any fund products, and the proportion of bank demand deposits is significantly higher.

Return and risk : The return levels of both closely follow the risk-free rate (about 4-5% annualized), with little difference. However, because USDY holds some bank deposits, its return stability is slightly higher, and its net value is almost unaffected by interest rate fluctuations. At the same time, the 3% excess collateral increases the risk resistance cushion. Accordingly, USDY introduces a certain amount of bank credit risk (although it has been mitigated as much as possible), while OUSG basically completely corresponds to the US government credit (credit quality is purer). Therefore, while USDY bears a small bank risk, it achieves stable returns and risk isolation through asset structure design. Correspondingly, OUSG more directly reflects the Treasury market interest rate, and the risk comes entirely from Treasury interest rate fluctuations.

Liquidity and redemption mechanism : OUSG is aimed at qualified investors, providing instant redemption and on-chain settlement convenience, but the transfer in the secondary market is restricted and needs to be circulated in a restricted environment. Only institutional addresses that have passed the KYC application can hold it. USDY can become a freely tradable interest-based stablecoin after the initial lock-up period (40 days) and can circulate freely on the chain, which improves its liquidity and wide availability. However, it is precisely because of the 40-day waiting period that the initial liquidity of USDY is not as instant as OUSG. In terms of redemption, OUSG supports direct exchange for USDC. The official redemption of USDY requires fiat currency withdrawal and has a minimum amount requirement, so in general, USDY holders will cash out through secondary market transactions.

Denomination: The base par value of OUSG is USD 100 and the base par value of USDY is USD 1.

We can also simply understand it as follows: USDY focuses more on open circulation and tends to retail demand, and is positioned as a stablecoin; while OUSG emphasizes instant liquidity in a closed environment, tends to institutional demand, and is positioned as a fund share.

1.1.2 Protocol products

Flux Lending Platform

Flux Finance is a decentralized lending protocol developed based on the Compound V2 asset pool model. It supports users to use high-quality RWA assets (currently only OUSG is supported) as collateral, lend stablecoins, and lend idle stablecoins to earn interest. Flux currently supports depositing and lending stablecoins such as USDC, DAI, USDT, FRAX, etc. At the same time, it implements permission control for restricted assets such as OUSG (whitelisted addresses are required to be used as collateral) to take compliance into account. Flux is governed by Ondo DAO, that is, ONDO token holders control parameters and asset lists through governance. The emergence of Flux allows users holding OUSG to pledge liquidity.

When the only available collateral asset type is OUSG, Flux is not very eye-catching, and the business volume of tens of millions of US dollars in deposits and loans is not large. However, when more and more RWA assets are introduced to the chain in the future, Flux will become a key component of the Ondo ecosystem, providing lending liquidity for RWA assets within the ecosystem.

Ondo Global Markets (GM)

Ondo officially unveiled the design of the GM platform at the first Ondo Summit held in New York in February 2025. This is Ondo's planned traditional asset tokenization platform, which aims to put thousands of publicly traded securities (stocks, bonds, ETFs, etc.) on the chain. Ondo also calls the vision of this product "Wall Street 2.0". Ondo GM is expected to be open to investors outside the United States. All issued GM tokens are backed by real securities 1:1, and can be freely transferred like stablecoins and can be used in Defi, but with built-in compliance authority control at the issuance and redemption level. Ondo pointed out that the current traditional investment environment has disadvantages such as high fees, limited channels, and fragmented liquidity. GM hopes to achieve lower costs, 24/7/365 trading and instant settlement through blockchain. For example, investors will be able to obtain tokenized versions of US stocks/funds such as Apple, Tesla, and S&P 500 ETFs as easily as buying stablecoins, and can trade freely in non-US markets or participate in on-chain financial services. The GM platform will also support token holders to choose to participate in securities lending to earn additional income.

However, Ondo Global Markets has not yet been officially launched. On its official website, it only vaguely states that it is "expected to be released later this year". The business should still be preparing for products, compliance and other aspects. The clear compliance guidance of US regulators on asset tokenization and the clarification of relevant legislation will be important prerequisites for the smooth operation of the product. In addition, Ondo Global Markets will run on Ondo Chain, which will be introduced in detail below.

Nexus Asset Issuance Protocol

Ondo Nexus is a new technology solution launched in February 2025, which aims to provide instant liquidity for US Treasury tokens issued by third parties. In simple terms, Nexus uses the instant minting and selling capabilities of OUSG to act as a common liquidity layer between different issuers. Ondo expands the scope of eligible collateral for OUSG to US Treasury tokens of companies such as Franklin Templeton, WisdomTree, and Wellington. The income certificates issued by these partner institutions (such as Franklin's FOBXX fund tokens, etc.) can be accepted by Ondo and exchanged for OUSG, thereby achieving shared liquidity between various products and stablecoins. Through Nexus, an investor holding US Treasury tokens of third-party institutions can sell them to Ondo at any time 24/7 in exchange for USDC or other stablecoins, and Ondo will include the token in its own asset pool as support and mint the equivalent OUSG. This provides an "instant redemption" mechanism for the entire market, breaking the limitation that traditional funds can only be redeemed within a limited time window on weekdays. The launch of Nexus also strengthens Ondo’s partnership with asset management giants such as BlackRock and Franklin.

1.1.3 Infrastructure Products

Ondo Chain: A licensed L1 with a focus on compliance

In February 2025, Ondo announced that it will launch its own semi-permissioned blockchain, Ondo Chain, which is specially designed for institutional-level RWA issuance and trading. Ondo Chain adopts Proof of Stake (PoS) consensus, but the assets that validators can stake are not limited to crypto assets, but can also be real-world assets with sufficient liquidity to reduce the impact of crypto market volatility on network security. Validation nodes will be served by well-known licensed financial institutions (intended consultants include Franklin Templeton, Wellington, WisdomTree, Google Cloud, ABN AMRO, Aon, McKinsey and other large traditional institutions).

The chain is characterized by combining the transparency of the public chain and the compliance security of the permissioned chain: the chain is open for access and development, but the verification layer is controlled to prevent MEV attacks and meet regulatory requirements. In addition, Ondo Chain natively supports key financial functions (such as dividend distribution, stock splits, etc.), provides proof of reserves on the chain, and verifiers regularly audit to ensure that each token is backed by sufficient physical assets. Ondo Chain will also have a built-in cross-chain bridge based on a decentralized verification network. The so-called "open" means allowing anyone to issue tokens, develop applications, or access the network as a user or investor. At the same time, user identification and permissions will be the core functions of Ondo Chain, allowing asset issuers and application developers to implement permission management and transfer restrictions at the appropriate contract level. That is to say: although users can freely access the network, developers can agree at the contract level which users on the network can access the protocols and assets it deploys.

The goal of the chain is to serve as the underlying architecture of the future "Wall Street 2.0", allowing institutions to conduct operations including prime brokerage and cross-collateralized lending on the chain, and achieve seamless integration of traditional finance and DeFi. Ondo Chain is expected to be tested and launched in 2025, and is said to be working with PayPal, Morgan Stanley, BlackRock and other institutions to design network details.

In summary, Ondo Finance has initially built a comprehensive matrix covering asset issuance, liquidity management, and infrastructure. Its product lines, from underlying assets (U.S. bonds, bank deposits, public securities) to on-chain protocols and infrastructure (lending, cross-chain bridges, and dedicated chains), work together to deliver business to each other.

1.2 Business Data

Although Ondo Finance has a wide range of products, there are not many products that have actually been launched. The asset products are OUSG and USDY, and the protocol products are the lending product Flux.

OUSG business data

Data source: Ondo official website

Currently, the total asset size of OUSG is US$545 million. Since its issuance in 2023, its size has experienced three waves of rapid growth. The fastest growth was from February this year to date, from less than 200 million to more than 500 million.

OUSG is available on three blockchains: Ethereum, Polygon, and Solana, but the vast majority of issuance is actually on Ethereum, and the scale on the other two chains is very small.

Looking at the address data on Ethereum, OUSG holds only 57 addresses, and the top 10 addresses account for more than 90% of the total asset issuance. This data is consistent with the fact that OUSG is only open to compliant institutions.

Data source: etherscan

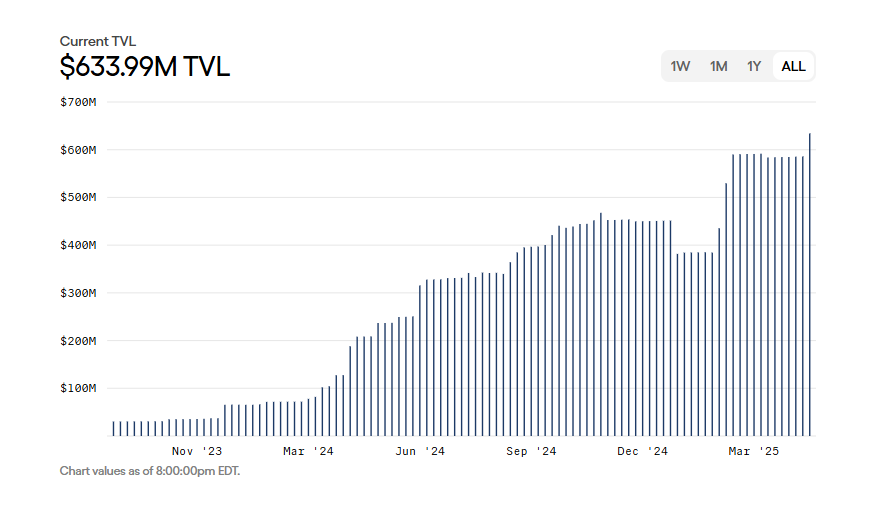

USDY business data

Data source: Ondo official website

Currently, the total asset size of USDY is 634 million US dollars, and it currently supports 8 blockchains including Ethereum, Mantle, Solana, Sui, Aptos, Noble, Arbitrum, and Plume.

Ethereum is also the main battlefield for USDY issuance, with more than half of its issuance on Ethereum, a market value of approximately US$330 million, and the number of coin holding addresses is also not large, only 316; Solana follows closely behind, with an issuance market value of approximately US$177 million and a number of coin holding addresses as high as 6,329, showing a higher retail user adoption rate.

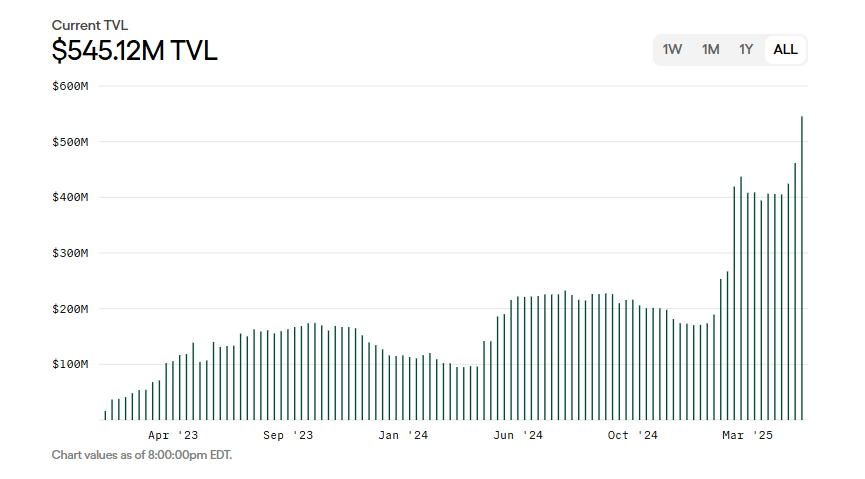

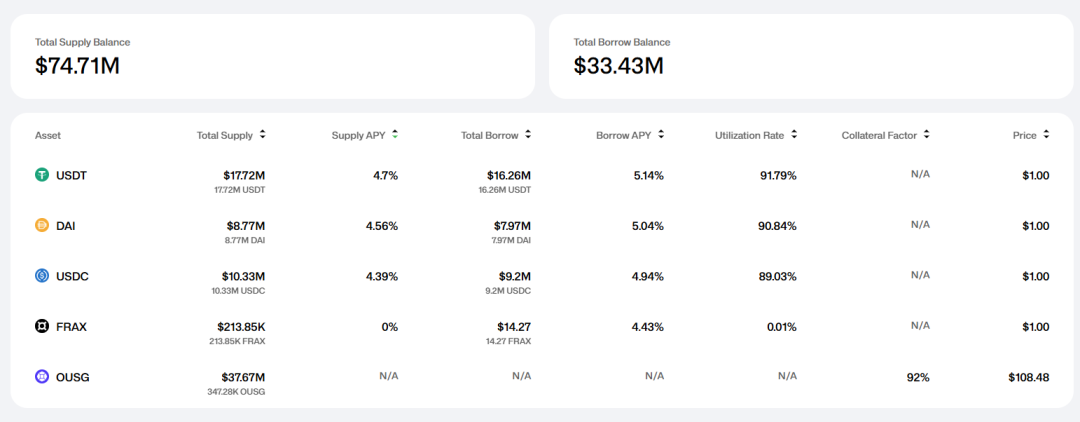

Flux business data

Data source: Flux official website

Since Flux currently only supports OUSG as collateral assets, its business scale is not high, with a total deposit size of US$74 million and loan funds of US$33.43 million. The subsequent growth of Flux still depends on the Ondo ecosystem to introduce more RWA assets.

1.3 Team Background

As a track that integrates strong compliance, Defi and traditional finance, whether the project party has rich business resources of traditional financial institutions, whether it has established smooth communication channels with government regulatory authorities, and whether it has deep industry experience in financial compliance are important references for us to judge whether the project can develop smoothly in the future.

Professional background of key team members

Source: Ondo official website

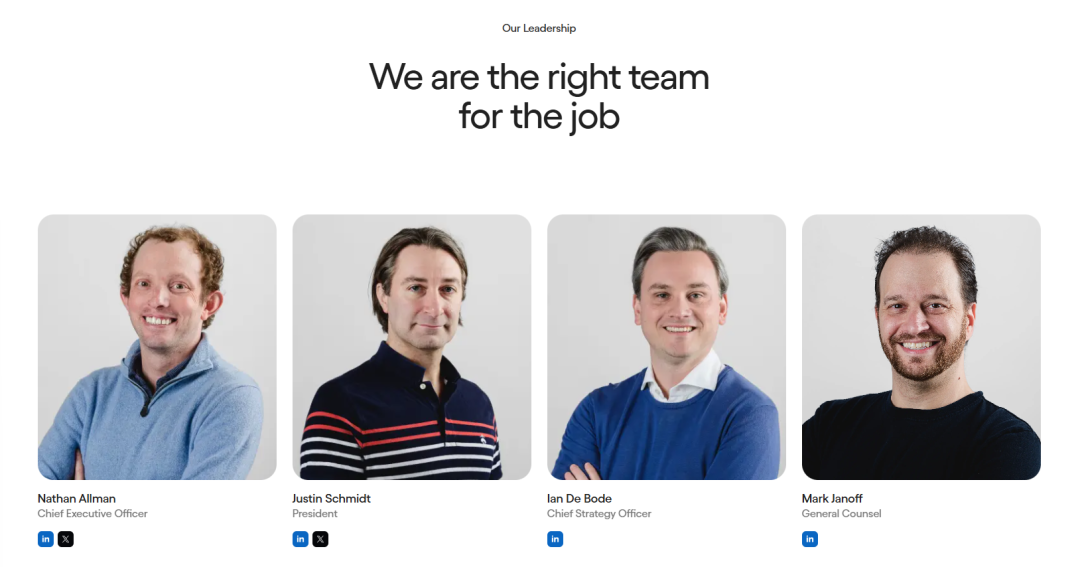

Ondo Finance's founding and senior management team mainly come from large financial institutions and well-known consulting firms on Wall Street. Many of them are from Goldman Sachs' digital asset business department. All core team members are real-name registered.

Among them, co-founder Nathan Allman worked in the digital asset department of Goldman Sachs. President and COO Justin Schmidt previously served as the head of Goldman Sachs' digital asset market department and was also one of the founding members of Goldman Sachs' digital asset team. Chief Strategy Officer Ian De Bode was a partner at McKinsey before joining Ondo, responsible for consulting in the field of digital assets, and has nearly ten years of experience in providing strategic consulting to senior executives of financial institutions. General Counsel Mark Janoff has a degree from Stanford Law School and has worked in legal affairs for technology companies. The core members of the team have luxurious resumes, and their past resumes are well adapted to the development needs of Ondo's track.

Government relations: Actively participate in policy development and industry associations/public initiatives

In April 2025, the Ondo team and its legal advisors met with the US SEC Crypto Asset Working Group and submitted a proposal to the regulator on the compliance framework for tokenized securities. According to the minutes of the meeting, Ondo proposed to the SEC a plan to issue and sell on-chain tokenized US securities under current financial laws. The discussion covered key issues such as the structural model of securities tokenization, registration and broker-dealer regulatory requirements, market architecture regulations, anti-financial crime compliance, and state corporate laws. Ondo even suggested that regulators consider adopting a "regulatory sandbox" or temporary exemption measures (to facilitate giving companies space for innovation and exploration before formal regulations are implemented) to promote innovation while ensuring investor protection.

Ondo Finance's interactions with government officials and regulators are not limited to private meetings, but also occur in public. In February of this year, Ondo hosted the first Ondo Summit in New York, inviting many important figures in traditional finance and blockchain to attend. It is worth noting that the summit guests included former and current officials from the U.S. Congress and regulators: Patrick McHenry, former chairman of the U.S. House Financial Services Committee, attended and delivered a speech on the future regulation of digital assets; Caroline Pham, member and acting chairman of the Commodity Futures Trading Commission (CFTC), also held a fireside chat at the meeting to share regulatory trends. During the meeting discussion, McHenry called on the crypto industry to actively engage with Washington policymakers and emphasized the lengthy and complex legislative process. Caroline Pham introduced the recent progress of regulators in implementing federal policies.

Furthermore, in early 2025, Ondo announced that Patrick McHenry would join the company as an advisor and serve as vice chairman of the Ondo Finance Advisory Board. McHenry had long served as a member of Congress and participated in the formulation of financial regulatory policies. His joining was seen as an important move for Ondo to strengthen its government relations.

"Friendship" with the Trump family

In early February 2025, at the "Ondo Summit" held in New York, Donald Trump Jr., the eldest son of the US President, unexpectedly appeared and delivered a speech. After that, Ondo Finance officially announced in February 2025 that it had established a strategic partnership with World Liberty Financial (WLFI), a crypto platform supported by the Trump family, to jointly promote the adoption of RWA and introduce traditional financial assets to the blockchain. According to the announcement, WLFI plans to integrate the tokenized assets (OUSG, USDY) provided by Ondo into its network as reserve assets. After that, an Ethereum address marked as belonging to WLFI exchanged approximately 342,000 ONDO tokens for $470,000 in USDC. As early as two months ago, the address had first bought $245,000 worth of ONDO and deposited the tokens in Coinbase Prime custody.

Of course, there are many crypto projects that have reached verbal cooperation with WLFI and obtained WLFI addresses for purchase. This kind of cooperation and purchase has a strong advertising nature and is more like a business cooperation.

1.4 Business Summary

Based on the above information, I think Ondo's business situation can be summarized in a few sentences:

From asset issuance to trading, Ondo has a complete product matrix around RWA, and the ceiling of the business story is very high.

The core team has excellent backgrounds, has a good layout in traditional financial enterprises and government relations, and can speak to regulatory authorities

The core products (Global Markets and Ondo Chain) have not yet been launched, and are still waiting for the regulatory approval signal. The current business development is still quite "left-side"

In general, facing the RWA crypto blue ocean that is far from being fully developed, Ondo is currently one of the most well-prepared crypto companies, with various endowment resources that are very good, and now it only needs the approval of regulators and legislatures.

2. Competition

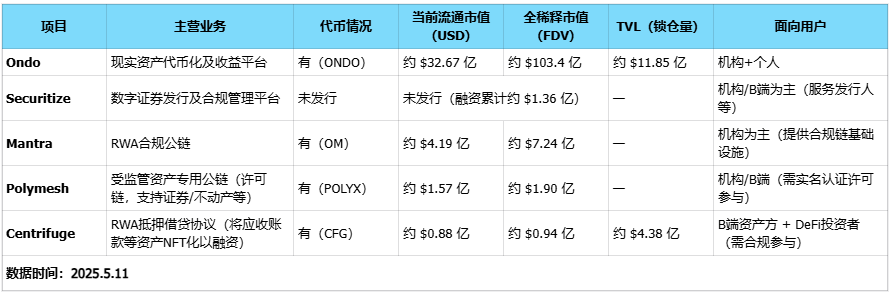

As the RWA concept heats up, Ondo faces competition from multiple projects at multiple business levels, including Securitize (no token issued), Centrifuge, Polymesh (listed on Binance), etc.

The following is a comparison of Ondo’s competition with several competitors in terms of market share, product differences, compliance progress, and ecological cooperation:

2.1 Market Position and Scale

Data source: https://app.rwa.xyz/treasuries

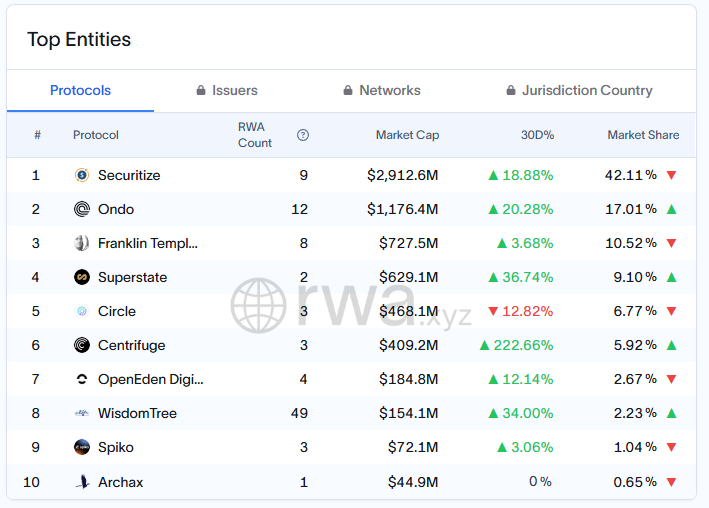

According to statistics from RWA data platform RWA.xyz, as of May 2025, Ondo ranks second in the US debt RWA market in terms of locked assets, with a market share of approximately 17.01% and a locked asset size of approximately US$1.17 billion. The first place is the Securitize platform supported by BlackRock, with locked assets of approximately US$2.912 billion and a market share of 42.11%. The third place is Franklin Templeton's Benji platform (727 million, 10.52%).

In the Treasury yield token market segment, Securitize and Ondo remain in the lead, with Securitize having a larger asset size and Ondo growing faster (up 20.3% in the past 30 days). Centrifuge focuses on private credit RWAs such as SME loans, with approximately $409 million in locked assets, accounting for 5.96%, and a business growth rate of 222.66% in just one month.

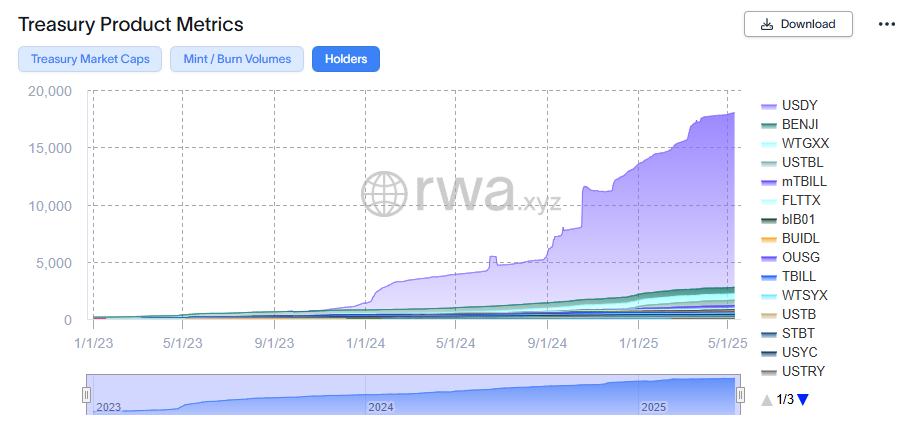

The number of holders of various national debt tokenized assets, data source: https://app.rwa.xyz/treasuries

It is worth noting that Ondo is far ahead of other projects in terms of the number of holders - its US Treasury token holders account for more than 90% of the entire market (because USDY is open to non-US ordinary investors and has a wide user base), while Securitize and other projects prefer to serve institutional investors, and their holders are mainly a few large customers.

2.2 Product positioning and mechanism differences

Ondo focuses on highly liquid, stable-yield U.S. dollar assets (short-term government bonds, money market funds) and strives to integrate them into DeFi applications. The USDY launched by Ondo is positioned as a "yield stablecoin" that can be used for payment and mortgage. In contrast, Securitize, as a digital securities issuance platform, has a wider range of services, including private equity, tokenization of fund shares, etc. However, in terms of U.S. Treasury yield products, Securitize has cooperated with BlackRock to issue the BUIDL fund token (custodied by Coinbase), which is mainly aimed at institutions and wealthy customers. BUIDL is similar to OUSG in that it is a cumulative-yield fund token, but the liquidity mechanism is different: BUIDL is usually only allowed to be redeemed during specific hours on U.S. working days, while Ondo OUSG provides instant minting and sales services all year round. In terms of DeFi integration, Ondo is clearly superior - its USDY and OUSG are available in more than 80 multi-chain applications and support on-chain collateral lending (Flux). In contrast, Securitize focuses on matching transactions through its own licensed trading system (ATS license) and has not yet been deeply integrated into public DeFi protocols. However, it is used as an important underlying income asset by many projects, including Ondo and Ethena.

Centrifuge's products are completely different: its core is the Tinlake loan pool, which packages real-world assets such as factoring receivables and real estate mortgages into coupon rights for sale, and investors bear higher risks in exchange for higher returns (often 5-10%+ annualized). This type of asset has a long term and poor liquidity, and needs to rely on large institutions such as MakerDao to provide exit liquidity (starting in 2021, MakerDAO will list the senior bond tokens of the Tinlake pool as RWA collateral, open the Maker Vault to the asset party, and lock the corresponding debt into it to lend DAI at the agreed interest rate). Correspondingly, Centrifuge's governance token CFG is more used for on-chain staking and security, rather than being positioned in daily retail and payment scenarios. It is considered a more segmented track in RWA.

Polymesh is positioned as a dedicated securities chain. With built-in identity authentication and permission control, it is convenient for institutions to issue various compliant tokens (stocks, bonds, fund shares, etc.) on it. Polymesh was transformed from the original Polymath project. Its POLYX tokens are used to pay on-chain fees and governance, but there are still not many actual asset issuance activities on the Polymesh network, and the scale is far smaller than the RWA activities of mainstream public chains such as Ethereum. However, some heavyweight traditional institutions (such as WisdomTree) now choose to cooperate with Ondo (issuing assets through Nexus and serving as a design consultant for Ondo Chain, etc.) instead of building their own chains. In the long run, Ondo has more prospects for business implementation.

2.3 Compliance and Regulatory Progress

When it comes to compliance, different platforms have adopted different strategies.

Ondo cooperates with regulated financial entities and follows the model of "registration exemption + overseas issuance". The so-called registration exemption means that the securities issued by the institution meet specific exemption terms, such as: not open to all American public, and therefore exempt from public sale registration with the SEC, in order to reduce compliance costs and improve issuance efficiency. OUSG is a private securities in the United States that is only open to qualified investors, while USDY is issued overseas through overseas entities. Ondo's compliance team has a rich background. Its chief compliance officer and many senior executives are from Wall Street institutions such as Goldman Sachs and are familiar with regulatory rules.

Securitize directly holds multiple US financial licenses, including Broker-Dealer and SEC registered transfer agent, so it has more direct compliance authority when issuing digital securities. This enables it to legally provide services for large asset management programs, such as tokenized KKR fund shares. At the same time, Securitize also cooperates with many large banks to explore blockchain applications. In contrast, Ondo has not yet held an SEC license on its own, but relies on a partner structure to operate legally (such as collaborating with Clear Street brokers, Coinbase custody, etc.). Globally, Ondo uses regulatory arbitrage (not providing USDY to Americans) to expand the market, while Polymesh integrates compliance from the bottom up (requiring each address to bind an identity). Centrifuge holds the underlying assets by setting up an offshore special purpose vehicle (SPV) and provides legal advice to ensure that its tokenized debt does not violate securities laws.

Regulatory policy risk is a common challenge faced by all RWA platforms. If the United States requires such tokens to be recognized as public securities in the future, Ondo and Securitize will need to obtain more comprehensive licenses or change their issuance methods.

However, at present, Ondo maintains good communication with regulators. For example, Ondo chose to establish a regulated subsidiary in the United States (Ondo I LP, etc.) and operate in accordance with existing rules. Its products such as USDY also emphasize daily reporting transparency by independent third parties. This reduces the risk of enforcement to a certain extent. In contrast, some attempts at decentralized RWA projects (such as selling RWA tokens to US users without registration) are more likely to become the focus of regulatory crackdowns.

2.4 Ondo’s Phased Advantages

Ondo's current leading position lies in the brand awareness brought by its extensive traditional financial ecological support. Through various product cooperation and public relations publicity, Ondo "cleverly" obtained the indirect endorsement effect of financial giants such as BlackRock, Morgan Stanley, and Fidelity. For example, Buidl issued by BlackRock is one of the underlying assets of OUSG. Although the two parties have no direct cooperation, under the hype, the market once regarded Ondo as the main "BlackRock concept currency"; top asset management companies such as Franklin and Wellington directly participated in the Ondo Nexus plan and contributed their US debt products as part of the Ondo ecosystem. Even payment giants PayPal and card organization Mastercard have cooperated with Ondo - PayPal's PYUSD stablecoin will be used for OUSG redemption, and Mastercard invited Ondo to join its multi-token network (MTN) pilot to graft bank payment interfaces to on-chain settlement.

Although the level of cooperation with many large organizations mentioned above cannot be said to be very deep, compared with other RWA projects, these cooperation cases not only bring good advertising effects and brand accumulation to Ondo, but also provide demonstration cases for it to carry out more commercial cooperation in the future.

In general, Ondo achieves market entry faster than other projects by connecting at both ends: upstream, it connects with traditional asset management giants to acquire assets and brand reputation, and downstream, it connects with the crypto market to acquire users and liquidity.

3. Main challenges and risks

Although Ondo has made good progress, its business still faces many challenges and risks:

3.1 Intensified competition

Ondo's phased advantages are more relative to other Web3 projects. Compared with projects that are truly backed by large platform-based institutions (such as Securitize invested by BlackRock), Ondo's advantages are not obvious. At present, due to unclear regulatory rules, many large financial institutions have not yet fully joined the battle. The source assets of RWA are still the strengths of Tradfi giants. With such a large financial pie, they have full motivation to build their own ecosystem to digest it, rather than giving it all to emerging Web3 projects like Ondo.

3.2 Product delivery and implementation capabilities

Ondo's core protocols such as Global Markets and Ondo Chain have not yet been officially delivered. Its current products are mainly asset-based, and its lending protocol is a fork from Compound V2, which is relatively simple. In the future, after the delivery of core products, whether Ondo can withstand the test of multiple dimensions such as products, operations, and compliance remains in doubt.

3.3 Uncertainty of regulatory compliance

Although the current US government is the most crypto-friendly, no formal crypto regulatory legislation has been passed so far (the recent rejection of the stablecoin GENIUS Act is a microcosm), and the mid-term elections for both houses will be held in 2026. It is still unknown whether the Republican advantage in both houses can be maintained after the election. If the compliance bill for asset tokenization cannot be passed before the mid-term elections, subsequent promotion will be more difficult and the uncertainty will be greatly increased.

3.4 Token Risks

1. The current circulation rate of Ondo tokens is only about 34%, and it faces an inflation rate of up to 64% in the next year, with great potential selling pressure; 2. The value capture of tokens is vague. Currently, ONDO tokens mainly grant governance rights, and there is no clear fee dividend or repurchase and destruction mechanism.

4. Valuation reference

The total supply of ONDO is 10 billion, and currently about 3.16 billion are in circulation, accounting for about 31.6% of the total.

Based on today's price (25.5.11), Ondo's market capitalization is approximately US$3.27 billion and its fully diluted market capitalization is approximately US$10.3 billion.

Among similar asset tokens, ONDO far exceeds other projects in terms of both circulating market value and FDV.

From the perspective of relative valuation, the market capitalization ratio of ONDO/CFG is about 40x, while the ratio of Ondo TVL/CFG TVL is about 2.7x, which shows that the price of ONDO has fully priced in optimistic expectations for future expansion, which has largely overdrawn the future growth rate and made this market value very vulnerable when facing various risk factors.

From a fundamental analysis perspective, the current valuation of ONDO tokens is still clearly high.

Starting from Ondo's static status quo: based on a market value of 3.27 billion, assuming that the annual income of the Ondo platform mainly comes from the management fees and spreads of USDY and OUSG (estimated based on an asset size of $1 billion, an average return of 5%, and an expense ratio of 0.3-0.5%), it is approximately US$3-5 million per year, plus miscellaneous income such as Flux, the total annual income is estimated to be less than US$10 million.

The static price-to-earnings ratio (P/E) of the circulating market value calculated in this way is far more than 300 times, and the FDV is more than 1,000 times. It can be seen that it is very expensive according to traditional valuation, and this is based on the fact that ONDO tokens do not have a clear token value capture.

The current high valuation of ONDO tokens reflects the market's extremely optimistic growth premium for Ondo in the next few years: if Ondo can expand to $10B+ TVL within 2-3 years (as the official "Next Stop: $10B" goal proposed), and successfully extend its business to areas such as stocks, the revenue scale may increase by an order of magnitude, and the current valuation will be digested to a certain extent.

Ondo’s high valuation also comes from its grand narrative of “Wall Street 2.0 on the chain”. If Ondo Chain develops smoothly, Ondo will be able to enjoy the valuation level of the public chain. The MC of several billion US dollars and the FDV of more than 10 billion will not seem so exaggerated.

Of course, considering the many issues I mentioned in the "Challenges and Risks" section, it takes a lot of effort and luck for a project to get to this point, as well as a good market atmosphere, and there is great uncertainty.

Events that require attention in the future

The following events and data will directly affect the expectations of the project and have a direct impact on the token price, so they need to be paid special attention to:

1. Project progress:

Ondo Chain mainnet and testnet deployment and launch

Testing and Launch of Ondo Global Markets

Whether to introduce and issue more new categories of RWA assets

Can we bring in more institutional partners and deepen our relatively shallow partnership with large financial institutions?

Is the asset size growing continuously?

2. Changes in the external environment:

Legislative progress of the US asset tokenization bill

The SEC’s regulatory attitude towards asset tokenization, whether it is clear that “sandbox regulation” means that business can be explored in advance before legislation

Will traditional tradfi giants build their own products and platforms? Will the blue ocean quickly turn red?