Written by: KarenZ, Foresight News

After spending $1.1 billion to acquire the stablecoin payment platform Bridge in October 2024, Stripe officially announced the launch of stablecoin financial accounts on May 8th, aiming to provide more efficient and convenient cross-border payment and fund management solutions for global enterprises, further solidifying its position as a global fintech leader.

So, what stablecoins does Stripe's stablecoin financial account support? What is its underlying asset composition? Which countries or regions does the business cover? From early Bitcoin payment exploration to today's stablecoin strategy, what is Stripe's layout in the cryptocurrency field? This article will take you through a detailed exploration.

Stripe Stablecoin Financial Accounts: Defining Borderless Finance

According to Stripe's official documentation, stablecoin financial accounts allow users to hold USDC and USDB stablecoin balances and send and receive funds through stablecoins and traditional financial channels (such as ACH, SEPA, and wire transfers). This means that funds from stablecoin balances can be transferred to external bank accounts or crypto wallets. If the recipient is an external bank account, the received amount will be automatically converted based on the current exchange rate, greatly enhancing the convenience and flexibility of fund circulation.

Stripe also revealed that it will gradually support more types of stablecoins in this account. The technical support for this service comes from the Bridge platform acquired by Stripe last year. Bridge focuses on stablecoin infrastructure construction and can help enterprises seamlessly integrate cryptocurrency technology, providing guarantees for the operation of Stripe's stablecoin financial accounts.

In terms of stablecoin custody, Bridge plays a key role. Currently, Stripe's stablecoin account supports USDC (issued by Circle) and USDB, a closed-loop stablecoin issued by Bridge. It is worth noting that USDB is not publicly offered and is pegged 1:1 to the US dollar. Its underlying assets consist of US dollars and BlackRock short-term money market funds.

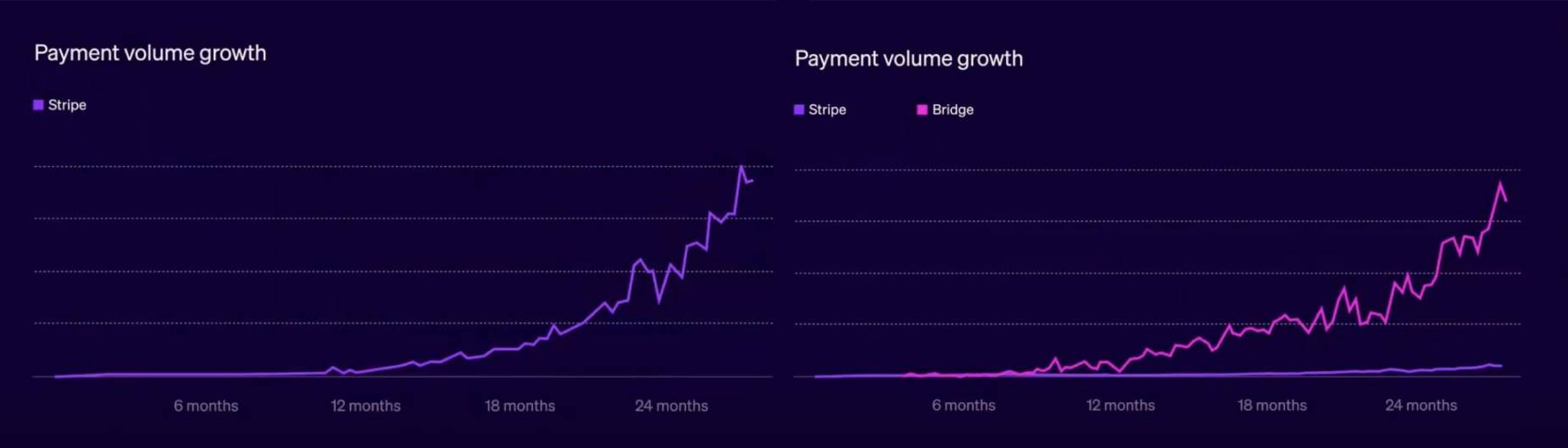

As Stripe executives stated at Stripe Sessions 2025, stablecoins can truly achieve borderless finance. By comparing the payment transaction growth of Stripe and Bridge in their first two years, we can see that Bridge shows a more significant exponential growth trend, which also indirectly confirms the huge potential of stablecoins.

In the API call information of the Bridge USDB document, the author observed that USDB is on the Solana blockchain, with Bridge responsible for minting, destroying, and holding stablecoin reserves.

It is worth mentioning that Bridge also supports creating custom stablecoins, including chain selection, token name, and reserve strategy. Bridge will distribute a portion of earnings to USDB and Bridge custom stablecoin holders at the end of each month. Rewards will be minted in the form of new tokens.

However, in information updated a month ago, Bridge stated that Bridge stablecoins (USDB and custom stablecoins) currently support Solana and Base networks, and will soon be launched on Polygon, Ethereum, Optimism, and Arbitrum. At the same time, Bridge stablecoins are always backed by a 1:1 US dollar value. The underlying assets include short-term US Treasury bonds, overnight US Treasury repo agreements, money market funds, and cash. This investment portfolio is stored in a separate account to protect token holders' interests and is managed by BlackRock, Fidelity, and Apex partners.

In terms of service coverage, Stripe's stablecoin financial accounts are currently open to enterprise users in 101 countries or regions, mainly concentrated in Latin America, Africa, Asian countries focusing on Central/South Asia and Southeast Asia, the Middle East (such as Saudi Arabia and Qatar), Oceania, and European countries mainly consisting of non-EU small economies or offshore financial centers. These regions are primarily developing countries, emerging markets, and small economies, typically characterized by high dollarization needs, strong cross-border payment demands, relatively loose regulatory environments, insufficient traditional financial infrastructure, or high inflation. Stripe's stablecoin accounts can precisely provide low-cost, high-efficiency payment and fund management solutions for these regions.

Countries or regions such as China, Hong Kong, the United States, core EU countries, the United Kingdom, India, Russia, Japan, Canada, and Australia are temporarily not included in the support list due to strict regulatory requirements, mature financial markets, or geopolitical factors.

Stripe's Crypto Layout: From Payments to Ecosystem Building

Stripe's layout in the cryptocurrency field is not a sudden development but the result of long-term exploration and deep cultivation.

2014-2018: Brief Attempt at Bitcoin Payments

In 2014, Stripe became the first major payment company to support Bitcoin payments, hoping that Bitcoin would become a globalized decentralized transaction medium to solve issues of low credit card penetration or high transaction fees.

In 2018, due to Bitcoin's long transaction confirmation times, high fees, excessive volatility, and decreased customer willingness to accept Bitcoin, Stripe announced the termination of Bitcoin payment support. Stripe believed that Bitcoin had evolved to be more suitable as an asset rather than an exchange medium.

Despite terminating Bitcoin support, Stripe remained optimistic about cryptocurrencies, stating that it would pay attention to the development of emerging technologies and faster payment methods such as the Lightning Network, Stellar (in which Stripe had seed investment), and Ethereum.

2019-2021: Cautious Exploration

In 2019, Stripe briefly participated in Facebook's Libra (later renamed Diem) project but withdrew due to regulatory pressure, demonstrating its cautious attitude towards the crypto field.

In 2021, Stripe formed a new crypto team aimed at developing Stripe's crypto strategy and promoting the integration of payments and Web3.

In November 2021, Matt Huang, co-founder and managing partner of Paradigm, joined Stripe's board of directors. Stripe co-founder and CEO Patrick Collison stated at the time: "Few people understand cryptocurrencies better than Matt, especially their potential for global internet enterprises."

2022: Full Return to the Crypto Market

In March 2022, Stripe launched a series of products aimed at providing tools and APIs for customers to more easily buy and store crypto tokens, convert to cash, trade NFTs, and handle KYC compliance workflows. Stripe's support page indicated that the company's products would support users purchasing over 135 cryptocurrencies using fiat currency in 180 countries/regions.

In April 2022, Stripe added cryptocurrency support to its programmatic (API-based) payment platform Connect, with Twitter set to become the first platform allowing users to pay with cryptocurrency through this platform.

2024-2025: Accelerating Stablecoin Strategy

Stripe's crypto ambitions significantly accelerated in 2024, focusing on stablecoins and consolidating its position in Web3 payments through acquisitions and product innovations.

In April 2024, Stripe allowed clients to accept cryptocurrency payments, initially supporting only USDC stablecoin, covering Solana, Ethereum, and Polygon.

In October 2024, Paxos launched its new stablecoin payment platform, with Stripe being the first customer to use the new solution. Stripe's Pay with Crypto product is supported by Paxos's stablecoin payment infrastructure, making it easier for merchants to accept stablecoin payments.

In October 2024, Stripe acquired the stablecoin payment platform Bridge for $1.1 billion. Bridge is known as the Web3 version of Stripe.

On April 30, 2025, Bridge partnered with Visa to launch a stablecoin card issuance product, allowing Bridge developers to programmatically issue Visa cards related to stablecoins across multiple countries/regions through a single API integration. Enterprises and individuals can use their stablecoin balances for daily shopping anywhere Visa is accepted. When a cardholder shops, Bridge deducts funds from their stablecoin balance and converts them to local currency, enabling merchants to receive payment in their local currency like other transactions.

On May 7, 2025, at Stripe Sessions 2025, Stripe launched a stablecoin financial account. Stripe also announced an expanded partnership with Ramp, an integrated financial operations platform, introducing an enterprise card based on stablecoins and integrated with expense management software, providing businesses with faster settlement speeds, lower costs, built-in currency fluctuation protection, and seamless card issuance. Specifically, businesses can fund their Ramp wallet with local currency and then convert it to stablecoins, or directly deposit stablecoins. Cardholders only need to pay with local fiat currency, and merchants can receive fiat currency. Funds are held at US dollar equivalent, avoiding local currency depreciation.

Future Outlook

From early attempts with Bitcoin to today's comprehensive layout centered on stablecoin financial accounts, Stripe's development in the crypto field has accelerated the integration of traditional finance and crypto economy, and is driving the mainstreaming of stablecoins.

By acquiring Bridge for $1.1 billion and launching stablecoin financial accounts covering 101 countries, Stripe has not only effectively addressed many pain points in cross-border payments but also provided an important US dollar tool for emerging markets. Its strategy focuses on the low-cost and high-efficiency characteristics of stablecoins, combined with Bridge's technological advantages and Stripe's global payment network, laying a solid leadership position in crypto payment.

As global financial regulators gradually improve the regulatory framework for stablecoins and traditional financial giants like Visa become increasingly open to stablecoins, stablecoins are moving from the margins to the mainstream. The stablecoin financial account launched by Stripe provides businesses with a low-friction, high-efficiency global payment solution, promoting the global financial system towards a more efficient, convenient, and inclusive direction.