Introduction: When Traditional Finance Collides with DeFi Native Forces

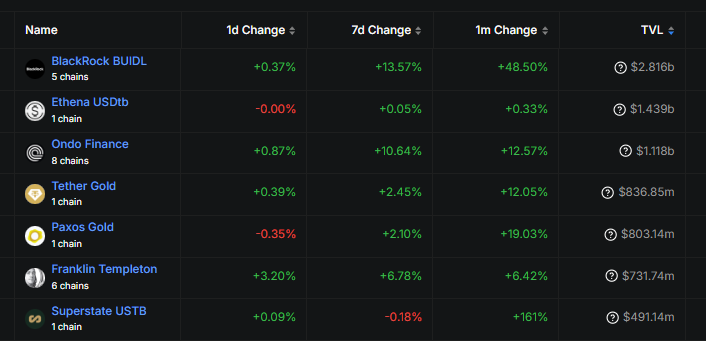

On May 7, 2025, defillama data shows that the RWA (Real World Asset Tokenization) track TVL broke through $11.886 billion, growing 46% from the beginning of the year. Among them, BlackRock's BUIDL fund surged to $2.816 billion with a 48.8% monthly growth rate, while Ethena USDtb and Ondo Finance followed closely with over $1 billion in TVL.

This asset revolution, driven jointly by traditional financial institutions and DeFi protocols, is pushing the competition of token economic models to new heights. This article focuses on two leading projects, ONDO and ENA, revealing the deep value logic of the crypto market from dimensions such as token design, revenue capture, and liquidity gaming.

I. Token Economic Model: The Route Conflict between Deflationary Gaming and Point Systems

1.1 ONDO: Deflationary Experiment under Institutional Narrative

As the leader in the RWA track, ONDO adopts a fixed total supply of 10 billion tokens + a deflationary mechanism, repurchasing and burning tokens through transaction fees. Its core design is:

- Institutional Priority Strategy: Staking revenue comes from 0.15% management fees of OUSG (tokenized US Treasury) and 0.17% transaction fees of USDY (stable yield product), expected to capture $176 million in protocol revenue in 2025;

- Unlock Pressure Test: From January 2025, team and investor tokens will be gradually released (accounting for 45.9% of total supply), but through cooperation with BlackRock and other institutions, part of the liquidity is hedged by compliant capital pools;

- Governance Premium: Holders can participate in voting on RWA asset issuance rules, such as deciding whether to introduce corporate bonds or real estate assets.

The advantage of this model is being linked to traditional financial returns, but the weakness is over-dependence on the speed of institutional capital entry. As the lesson from Maple Finance in the 2022 bear market showed - when a wave of institutional redemptions occurs, the token may face a spiral decline.

1.2 ENA: Stablecoin Empire's Point Economics

ENA builds a DeFi native incentive system:

- Burning Flywheel: The protocol uses 20% of USDe (algorithmic stablecoin) revenue to burn ENA, combined with Shard/Sats point system to lock liquidity. For example, users can obtain sENA by staking ETH and participate in future token distribution of Ethereal DEX;

- Revenue Bundling: USDe holders get 4% ETH staking revenue + 10%-18% derivative hedging revenue, forming an "internet bond" effect. Currently, USDe issuance reaches $8 billion, directly supporting ENA market value;

- No Deflationary Trap: Although the total supply is fixed at 15 billion, by cross-chain re-staking (such as Converge L1), tokens are embedded in multiple revenue scenarios, reducing selling pressure.

This design gives ENA an advantage in high-frequency trading scenarios, but caution is needed against derivative risks like negative funding rates. As a certain institutional report in March 2025 pointed out: "ENA's valuation is essentially an on-chain mapping of hedge fund performance."

II. Revenue Source Dissection: Traditional Asset Securitization vs Algorithmic Stablecoin Alchemy

2.1 ONDO: The "On-chain BlackRock" Gnawing at the Trillion-Dollar Fixed Income Market

ONDO's value capture is directly linked to the traditional financial market:

- US Treasury Arbitrage: Through tokenized short-term government bonds (like OUSG), investors can obtain 5% annualized returns, far higher than Coinbase's 2.3% current rate;

- Institutional Pipeline: Cooperating with Fidelity to issue OMMF money market fund, allowing qualified investors to participate in private credit markets with a $100,000 threshold, management fee rate of 0.25%;

- Compliance Premium: Achieving bankruptcy isolation through Ankura Trust, meeting SEC requirements for securitized asset custody, attracting long-term funds like family offices.

However, this model faces a double ceiling: the overall RWA track TVL only accounts for 0.2% of traditional mutual fund scale, and many competitors are sharing the corporate credit market.

2.2 ENA: The "On-chain Bridgewater" of Derivative Revenue

ENA builds a more aggressive revenue engine:

- Funding Rate Arbitrage: By shorting ETH perpetual contracts to hedge staked asset volatility, with historical annual average returns of 15.7%. When ETH staking rate progresses from 26% to 50%, this strategy's returns may double;

- Liquidity Black Hole: USDe has been integrated into over 50 protocols like Aave and Curve, with daily DEX trading volume exceeding $1.2 billion, with fees rebated to ENA stakers;

- Regulatory Arbitrage: By setting headquarters in the Cayman Islands, avoiding strict US scrutiny of derivative protocols, rapidly expanding market scale.

The risk of this model lies in cascading liquidations during extreme market conditions. For example, in February 2025, when ETH price dropped 23% in a single day, USDe's collateralization ratio once touched the 105% warning line.

III. Liquidity War: Unlock Tide vs Ecological Bundling

3.1 ONDO: Combating Token Selling Pressure with Compliance Narrative

Despite facing 45.9% token unlock pressure, ONDO stabilizes the market through a triple strategy:

- Institutional OTC Channel: Cooperating with GSR and Genesis Trading to establish a block trading platform, directing unlocked tokens to sovereign funds to reduce market impact;

- Cross-chain Liquidity Pool: Deploying BUIDL fund on Solana, utilizing its 50,000 TPS feature for second-level redemption, capturing $120 million in institutional deposits in a single day;

- Governance Rights Premium: Holding over 100,000 ONDO allows participation in BlackRock RWA asset allocation meetings, pushing the token towards "on-chain investment bank equity".

3.2 ENA: Building Liquidity Moat with Point System

ENA's liquidity defense is more ingenious:

- Staking Nesting: Users staking ENA can obtain sENA points, which can be exchanged for Ethereal DEX governance tokens. This "Russian doll" model locks 80% of tokens in smart contracts;

- Exchange Alliance: Launching Shard point products on CEXs like Binance and OKX, binding trading volume with ENA price. For example, in Binance Launchpool, ENA staking volume occupies 63% of the pool;

- Stablecoin Hard Demand: As a payment tool, USDe is integrated into Amazon and Shopify's crypto payment interfaces, forming a cash flow closed loop.

IV. Track Ceiling: Divergent Paths in Trillion-Dollar Market

4.1 RWA Track: Long March of Compliance and Asset Diversification

Although RWA TVL breaks through $11.8 billion, sub-markets show structural differentiation:

- Government Bond Dominance: BlackRock BUIDL, Ondo OUSG and other US Treasury products occupy 78% of the share, with corporate credit and real estate long-tail assets progressing slowly;

- Regulatory Chasm: EU MiCA law requires RWA issuers to hold financial institution licenses, causing 85% of projects to concentrate in offshore jurisdictions like Cayman Islands and Singapore;

- Technical Bottleneck: Protocols like Centrifuge still rely on Chainlink oracles manually inputting asset data, leading to liquidation disputes in AP Hotel REIT tokenization project due to data delay.

4.2 Stablecoin Track: Bidirectional Expansion of Derivatives and Payments

The stablecoin track where ENA is located shows a more savage growth state:

- Earnings War: USDe's 15% comprehensive yield far exceeds USDC's 2.3%, driving its market share from 3% to 18%;

- Payment Revolution: PayPal integrates USDe into Solana network, reducing cross-border remittance fees from 3% to 0.1%, with monthly transaction volume exceeding $4 billion;

- Regulatory Arbitrage: By setting reserve assets as ETH staking certificates, avoiding the US regulatory framework for fiat stablecoins.

V. Risk Factors

- ONDO: Regulatory policy changes, RWA product compliance controversies, token economic model income singularization.

- ENA: Stablecoin de-pegging risk, extreme derivatives market volatility (such as negative funding rates), staked asset liquidation risk.

Conclusion: The Ultimate Battlefield of Token Economics

When ONDO moves trillions of dollars of government bonds onto the blockchain, and ENA reconstructs US dollar hegemony through algorithms, this contest of token economic models has long transcended price fluctuations. It is essentially a confrontation between two routes: traditional financial compliance transformation vs. DeFi's native institutional subversion. For investors, ONDO represents an on-chain replication of Wall Street order, while ENA is an open challenge to central bank monetary sovereignty.

In the short term, ENA may continue to lead market sentiment with its stablecoin's rigid demand and high-yield gimmicks; but in the long term, if ONDO can connect trillion-level RWA assets such as real estate and carbon credits in 2025-2026, it may open a true financial empowerment revolution. As BlackRock CEO Larry Fink said: "Tokenization is not an option, but a must-answer question for global capital markets."

In this process, every parameter adjustment in token economics could trigger a trillion-dollar capital reallocation.