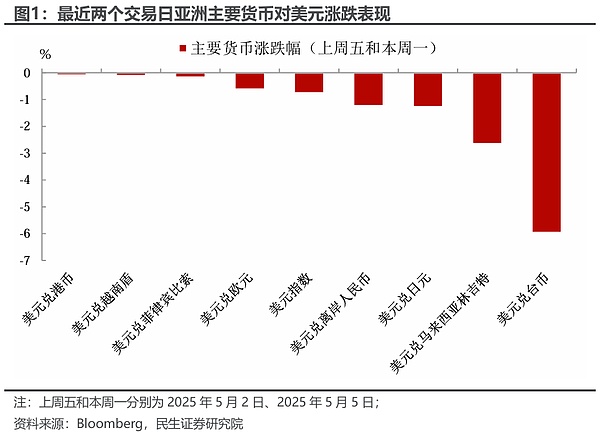

In recent days, the Asian foreign exchange market has experienced intense volatility, with onshore RMB surging nearly 600 points, offshore RMB breaking through 7.20 at one point, Hong Kong dollar continuously touching strong exchange guarantee, and Taiwan dollar experiencing a "historic-level" surge, accumulating over 9% in just two days, which is extremely rare in the forex market.

Behind the significant surge, in addition to the most direct catalyst of positive signals from US tariff negotiations, the market is hotly discussing a behind-the-scenes "Mar-a-Lago Agreement" in the making.

According to Wind Trading Desk, despite market rumors, JPMorgan Chase believes in its latest forex strategy weekly report that the US dollar's weakness is not derived from any coordinated agreement, but driven by multiple fundamental changes.

For instance, US economic growth expectations have been downgraded, stagflation concerns from trade conflicts have intensified; the Federal Reserve's independence is controversial; US term premium rises simultaneously with the Federal Reserve's declining terminal rate; Germany's fiscal policy shifting towards easing, providing support for European capital markets.

In this context, the attractiveness of US dollar assets has declined, naturally causing funds to flow to other markets.

Additionally, JPMorgan Chase stated that the market generally believes another powerful driver behind Asia's strong currencies is the massive US dollar assets accumulated through years of trade surplus beginning to flow back, creating strong forex hedging pressure.

Goldman Sachs analyst Teresa Alves believes that the US dollar is overvalued by 16%, and may quickly adjust or even overshoot if there are "significant" macroeconomic changes.

Why does the market firmly believe in an agreement?

The "Mar-a-Lago Agreement" originally referred to Trump's concept of lowering the US dollar and boosting export countries' currencies through multilateral methods. Although this concept was never formally implemented, recent unusual Asian currency fluctuations have reignited this topic.

For example, South Korea's Finance Minister recently acknowledged "working-level consultations" with the US Treasury on exchange rate issues; Taiwan's "Central Bank" unusually issued a statement after the New Taiwan dollar's appreciation, claiming it was "not under US pressure". These ambiguous responses have instead expanded market speculation.

More critically, the market generally believes this round of exchange rate movement is "extraordinary". JPMorgan Chase points out that such a surge in currencies like the New Taiwan dollar could hardly occur without policy tacit consent. Since Asian foreign exchange markets are long dominated by regulatory bodies, the saying "no wind, no waves" is not groundless in this context.

Unlike the 1985 Plaza Accord, Asian countries (especially export-oriented economies) currently hold massive US dollar assets. In this situation, governments don't need to directly sell US dollars; they can promote currency appreciation by "window guidance", increasing corporate hedging ratios or requiring conversion of part of US dollar income into local currency.

BNP Paribas experts stated:

While no economy will officially admit currency valuation is the negotiation focus, market expectations suggest otherwise. This is especially noteworthy given the Mar-a-Lago Agreement's emphasis on high US dollar valuation as the fundamental cause of US trade imbalance.

Although the "Mar-a-Lago Agreement" remains unofficially confirmed, Asian currencies' rise has already created ripples in capital markets. Amid the intertwined influences of geopolitics, macroeconomic policies, and market expectations, an invisible "currency storm" might be forming.

Asia's Massive US Dollar Assets Become Key Variable

The market generally believes that another powerful driver behind Asia's strong currencies is the massive US dollar assets accumulated through years of trade surplus beginning to flow back.

JPMorgan Chase estimates that Chinese exporters alone hold $400-700 billion in assets, and combined with other Asian export countries' net international investment position surplus, this creates enormous potential reflux and forex hedging pressure.

UBS research on the 5th also pointed out that besides stock inflows, this round of New Taiwan dollar's rise is mainly driven by forex hedging by insurance companies and enterprises, and the stop-loss of previous Taiwan dollar financing arbitrage trades.

China's recent adjustment of the USD/RMB fixed exchange rate is also viewed as an important policy signal, removing obstacles for widespread Asian currency appreciation.

Goldman Sachs Calculates: US Dollar Overvalued by 16%

Could US dollar depreciation be far from over?

Goldman Sachs analyst Teresa Alves stated in the May 1st report that the US dollar is currently overvalued by about 16%, with this valuation mismatch primarily driven by global funds chasing the US's superior return prospects. As the US's return advantages gradually diminish, the dollar's overvaluation may be progressively corrected.

Goldman Sachs research indicates that the degree of US dollar overvaluation is highly dependent on assumptions about the "standard level" of current account.

Currently, the US actual current account deficit is about 4%. If the current account deficit narrows to 2.6%, it would correspond to a 16.5% dollar adjustment; if further reduced to 2% (close to IMF's 2023 standard), it might lead to a 22% dollar depreciation; if it drops to 1%, a 31% dollar depreciation might be needed to achieve balance.

Investors should pay attention to changes in the US current account status and global fund flow trends, preparing for potential dollar adjustments.