Source: MiaoTou APP

U.S. Treasury yields fell, U.S. Treasury prices rebounded, are U.S. Treasury bonds safe?

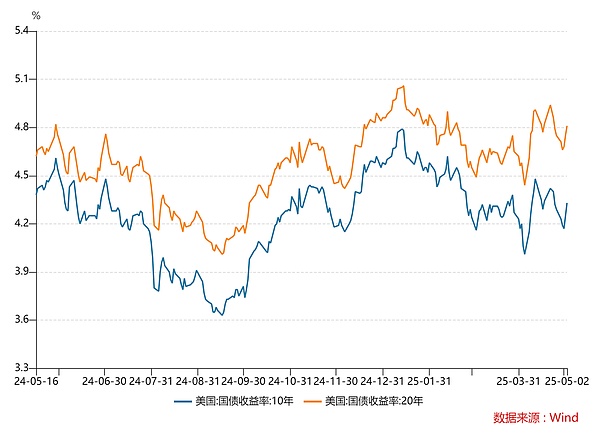

After the tariff policy was implemented, U.S. Treasury yields continued to rise. The 30-year U.S. Treasury yield once exceeded 5%, and the 10-year yield also reached 4.50%.

Rising U.S. Treasury yields mean falling U.S. Treasury prices. The two are inversely related, and the logic is simple:

Suppose you buy a 1-year US bond with a coupon rate of 5% and a face value of $100. You can cash it out for $105 at maturity. But if the stock market rises at this time, investors sell the original $100 US bonds, the supply in the market increases, and the demand remains unchanged, the price of the US bonds in your hands will fall, for example, to $98, and the corresponding yield will become 7.14% (7/98) ; vice versa.

The key behind the rise and fall of bond prices is actually the change in supply and demand . When the market demand for government bonds increases sharply and there is a situation where supply exceeds demand, bond prices will rise and the yield to maturity will fall; conversely, when the market supply increases and supply exceeds demand, bond prices will fall and the yield to maturity will rise.

The rise in U.S. bond yields actually reflects the sell-off of U.S. bonds . In theory, U.S. bonds should be the safest "safe haven" amid global tariff uncertainty, rising risk aversion, and rising expectations of a Fed rate cut, but now they are being sold off.

One of the reasons is that the fund basis trading was blown up, forcing them to close their positions and sell US bonds in exchange for liquidity, which resulted in a price stampede . Basis trading is actually arbitrage through the price difference between spot and futures Treasury bonds. Hedge funds use high leverage, and once market fluctuations lead to losses, it will trigger a wave of selling, forming a vicious cycle of "selling-yield increase-selling again";

Another reason is that the market's confidence in the United States is weakening . Whether it is the worry that the escalation of the trade war will increase the risk of stagflation in the United States, or Trump's public pressure on Federal Reserve Chairman Powell to cut interest rates and even threaten to fire him, the Fed's independence crisis has weakened the market's confidence in US dollar assets.

However, the selling pressure on US bonds was soon relieved. Since April 21, US bond yields have fallen and US bond prices have rebounded. Has the US bond alarm been lifted?

# 01 US debt holds Trump in its grip

According to conventional logic, rising U.S. bond yields (i.e. falling U.S. bond prices) usually means rising U.S. interest rates or strong economic data, which in turn attracts global funds to flow into the United States and pushes up the U.S. dollar exchange rate. But this time the situation is very different - U.S. bonds and the dollar actually fell simultaneously, and U.S. stocks were not "spared."

The collapse of the U.S. stock market and the dollar may be exactly what Trump wants to see . After all, his core consideration has always been to consolidate political power, and his usual method is to "first create a crisis and then solve it in a high-profile manner."

The plunge in U.S. stocks has become a tool for him to play against the Federal Reserve. Once the market trades that the U.S. economy is in recession and panic is rising, the Federal Reserve is forced to initiate a large-scale interest rate cut, followed by economic recovery and stock market recovery. Trump can then take advantage of the situation to attribute the "credit" to his wise decision and pave the way for his 2026 mid-term elections.

As for the depreciation of the US dollar, it is a two-pronged approach for Trump: on the one hand, it improves export competitiveness; on the other hand, it can dilute the huge government debt. It can be said that "there is a calculation in the suppression."

However, the decline in US debt has put Trump under tremendous pressure. As the yield of US debt in the market rises, the interest rate of newly issued US bonds also needs to be increased accordingly, otherwise investors will be unwilling to buy. Once the interest rate of new treasury bonds increases, the payment pressure of the United States will also increase. In this way, the US's practice of "taking money from Peter to pay Paul" will only make the debt gap bigger and bigger, forming a vicious cycle .

So after the sharp drop in U.S. debt, the Trump team began to "save the market":

On April 9, Trump announced that he would suspend the implementation of "reciprocal tariffs" for 75 countries around the world that have not taken retaliatory tariff measures against the United States for 90 days, and reduce the tariffs of these countries to 10%;

On the 12th, the United States implemented tariff exemptions for some Chinese high-tech products (such as smartphones, semiconductors, etc.);

On the 22nd, Trump expressed his willingness to negotiate with China in a "very friendly" manner, and that tariffs on Chinese goods may be significantly reduced in the future, but not to zero. On the same day, he also said that he had "no intention of firing" Federal Reserve Chairman Powell, giving the market a "reassurance";

On the 28th, U.S. Treasury Secretary Benson declared that he did not want the Sino-U.S. trade situation to escalate further, trying to calm the panic in the financial market. At the same time, the Federal Reserve also began to calm market sentiment;

On the 24th, Cleveland Fed President Hammack said that although a rate cut in May is almost impossible, if the economic data by June can provide clear and convincing signals, a rate cut may be taken as early as June - in any case, market expectations have been ignited.

Although the Trump team's "compromise" temporarily eased the selling pressure on U.S. debt, the U.S. debt alarm has not been lifted.

# 02 U.S. debt is no longer a “safe haven”

The risk premium of U.S. Treasuries is increasing, and the market is beginning to price U.S. Treasuries as "risky assets" rather than "risk-free assets ."

U.S. debt has always been regarded as a safe haven asset, mainly relying on the credit of the U.S. dollar . But now, the market no longer regards U.S. debt as a "refuge", and the reason behind this is simple - the credit of the U.S. dollar has been overdrawn.

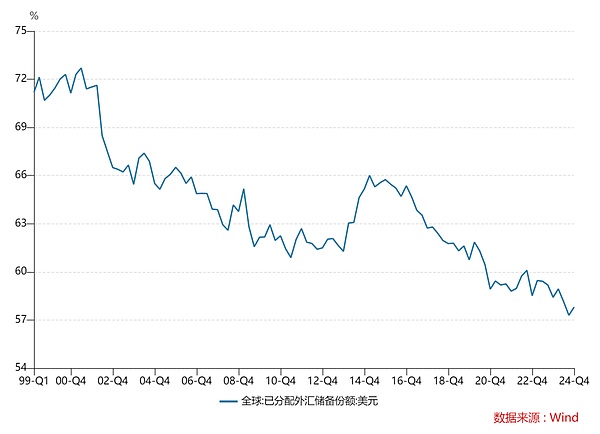

As soon as the Bretton Woods system was established in 1944, the US dollar became the only currency in the world pegged to gold. All currencies had to be pegged to the US dollar, and global trade and reserves revolved around the US dollar. By 2001, the US dollar accounted for 72.7% of global foreign exchange reserves, which was the peak period of the US dollar's credit. However, with the rise of the euro and global multipolarization, the US dollar's share in global foreign exchange reserves began to slowly decline, which means that the US dollar's credit has also begun to decline.

The United States frequently uses the dollar hegemony as a weapon to attack the economies of other countries through sanctions, asset freezes, etc. Especially during the Russia-Ukraine conflict, the United States froze Russia's foreign exchange reserves, which directly aggravated the global crisis of confidence in the dollar and caused many countries with trade surpluses with the United States to begin to "abandon" U.S. debt.

Then there is the US debt problem, which has now reached the "dangerous edge". The US national debt has already exceeded 36 trillion US dollars, and the debt accounts for more than 120% of GDP. Analyst Larry McDonald pointed out that if the interest rate remains at 4.5%, the US debt interest expenditure may reach 1.2 trillion to 1.3 trillion US dollars by 2026, exceeding the defense expenditure, and the US fiscal deficit will be overwhelmed.

The pressure on the United States' short-term debt is even more pressing. In 2025, 9.2 trillion U.S. Treasury bonds will mature, with 6 trillion U.S. Treasury bonds maturing in June alone.

The credit of the US dollar is now like an overdraft on a credit card. Global capital has begun to shift to non-US assets such as gold. The share of the US dollar in global foreign exchange reserves has continued to decline, falling to a low of 57.3% in 2024.

Another logic supporting US debt is that countries with trade surpluses with the US have to return US dollars to the US after receiving them, mainly because they can earn interest by investing in US debt, forming a closed loop of "commodities-dollars-US debt" . However, Trump's "reciprocal tariff" policy will break this closed loop. If the global trade war does not ease, the scale of the US trade deficit will decrease, which will directly affect the ability of surplus countries to accumulate US dollars.

When U.S. debt is no longer a "safe haven", traditional safe-haven funds will turn to alternative assets such as gold and non-U.S. currencies. The International Monetary Fund predicts that the share of U.S. dollar reserves may fall below 50% in 2026.

# 03Will the U.S. debt default?

This issue has always attracted much attention. The market’s trust in U.S. assets has encountered a systemic crisis. How great is the risk of U.S. debt default?

The possibility of a direct short-term default of US debt is very low . MiaoTou has said many times that if the United States faces a debt crisis, the status of the US dollar as the world's reserve currency will be greatly threatened, and it may even trigger a new round of global financial crisis, which is undoubtedly an unbearable disaster for the United States.

The US government has many means to avoid default and will never easily go to the brink of default . For example, Trump once used tariffs as a bargaining chip to ask other countries to promise to buy more US debt . The tariff plan issued on April 2 is a typical "extreme pressure" method. In addition, Trump may also adopt a "debt swap" strategy . For example, the "Mar-a-Lago Agreement" rumored recently, one of the items is that the Trump administration plans to replace part of the US debt with 100-year non-tradable zero-interest bonds.

Another means is to replace high-interest bonds with low-interest bonds. Trump has publicly criticized the Federal Reserve many times and pushed the Federal Reserve to cut interest rates as soon as possible through policy pressure, which can directly lower the face interest rate of short-term newly issued bonds.

However , the impact of interest rate cuts on long-term government bonds is not direct . In fact, long-term US bond yields may rise instead of fall in the context of interest rate cuts, especially when US inflation expectations rise and deficits remain high. As Nobel economist Paul Krugman said: "When the debt scale exceeds the critical point, monetary policy will become a vassal of fiscal policy." Today, the US bond market is entering a new normal of "diminishing effectiveness of interest rate cuts."

If the market loses confidence in U.S. debt and is unwilling to buy new debt, it will eventually have to rely on the Federal Reserve to "take over", which is a typical "balance sheet expansion" behavior. Although this approach can ease debt pressure in the short term, it is not a sustainable solution.

The Fed's core goal is to maintain price stability and promote full employment, not to fund fiscal deficits. Direct bond purchases through balance sheet expansion may be seen as fiscal monetization, which will undermine the central bank's independence. If the Fed "takes over" for a long time, it may make the Treasury Department more bold in issuing bonds.

In extreme cases, the Fed may have to start the "printing press" and directly purchase government debt, which is the last "trump card" . Although this can avoid default in the short term, it also brings another hidden risk - as these new dollars eventually flow back to the United States, they will significantly increase the domestic money supply, thereby pushing up inflation. This situation is essentially equivalent to a "hidden default", that is, the actual interests of creditors will be damaged through currency depreciation, and the risks and losses will be "shared" among investors holding dollars and U.S. bonds around the world .

In fact, most countries and institutions do not want to see a US debt default, because once a default occurs, it will bring immeasurable consequences. As the cornerstone of the global financial system, the default of US debt will not only directly impact the global market, but also bring huge losses to investors, institutions and even countries.

In summary, although the probability of direct default of US Treasury bonds in the short term is extremely low, the risk of its price falling still exists.

# 04Written at the end

For us investors, we need to pay special attention to the following points:

(1) If you invest in U.S. bonds through QDII funds or related wealth management products (domestic accounts + RMB) , you do not need to exchange currency or open an overseas account, but you need to be alert to the risk of a sharp drop in U.S. bond prices. For example, if tariffs are further escalated, the Federal Reserve loses its independence, and market confidence in the U.S. economy declines, the attractiveness of U.S. bonds will drop significantly ; on the contrary, if the tariff war eases, U.S. inflation falls, and the economy achieves a soft landing, then U.S. bond yields are expected to fall and U.S. bond prices may continue to rebound.

In particular, the short-term volatility of U.S. Treasuries is large, like a "swinging ball" with violent emotional fluctuations. At present, the U.S. bond market is extremely sensitive to Trump's policies and the "pivot" of the Federal Reserve, and any signal may bring about short-term sharp fluctuations . When Trump insists on high tariffs or the Federal Reserve is hawkish, U.S. bond prices may fall sharply; on the contrary, if the Trump team makes remarks to ease trade conflicts, releases signals to control deficits, or shows signs of policy easing, U.S. bonds may rebound quickly;

(2) If you purchase U.S. bonds directly through an overseas brokerage or bank (overseas account + U.S. dollars) , you need to pay special attention to the risk of exchange rate fluctuations. If the RMB appreciates, you may face exchange losses, resulting in the "wiping out" of interest rate differentials, and even the possibility of negative returns .

Note: From the perspective of debt structure, domestic institutions and individuals in the United States are the main holders of U.S. debt. According to the latest International Capital Flows Report (TIC) released by the U.S. Treasury Department, as of the end of February 2025, domestic institutions and individuals in the United States held about 76% of U.S. debt, while the total amount of U.S. debt held by foreign investors was $8.8 trillion, accounting for 24.2% of the total size of U.S. debt.

Among them, Japan is still the largest creditor of U.S. debt. As of the end of February, the amount of U.S. debt held reached US$1,125.9 billion, an increase of US$46.6 billion in a single month; mainland China ranked second with US$784.3 billion, an increase of US$23.5 billion; the United Kingdom ranked third with US$750.3 billion, a month-on-month increase of US$10.1 billion.