Get the best data-driven crypto insights and analysis every week:

Diving into dYdX

By: Tanay Ved

Key Takeaways:

dYdX v4 migrated from the Ethereum ecosystem to a standalone Cosmos app-chain, decentralizing its exchange infrastructure while improving performance and sovereignty.

Trading volume on dYdX v4 has recently averaged around $200M daily, with open interest steadily climbing to $175M, showing healthy traction in a highly competitive landscape.

Perpetual futures trading volume on dYdX still lags behind major centralized exchanges but has significant room to grow as demand for on-chain derivatives platforms accelerates.

Recent market data shows BTC and ETH continuing to dominate activity, with open interest, funding rates and liquidations offering a granular lens into shifting trader positioning and sentiment.

Introduction

Exchanges are a core pillar of crypto infrastructure. They enable participants to access liquidity, gain exposure to crypto-assets, and engage in spot and derivatives markets. Centralized exchanges (CEXs) like the CME and Binance handle trillions in volume annually, with derivatives capturing an even larger addressable market. But with improvements in blockchain scalability, decentralized exchanges (DEXs) are aiming to close the gap, leveraging on-chain infrastructure to deliver a more CEX-like trading experience at similar scale.

As part of a grant from the dYdX Grants Program, Coin Metrics is onboarding dYdX market data and diving deeper into its ecosystem. We previously released a demo walking through how to access a suite of dYdX data. In this issue of State of the Network, continue our coverage with an overview of dYdX v4: its role as an orderbook-based perpetual futures exchange, its transition to a Cosmos app-chain, and key exchange metrics like trading volume, open interest, and market activity.

dYdX Overview & Background

What is dYdX?

dYdX is a decentralized exchange (DEX) that enables users to trade perpetual futures contracts in a non-custodial manner. Perpetual futures contracts, often referred to as “perps”, are a type of derivatives contract that allow traders to speculate on crypto-asset prices, without directly owning the underlying assets. Unlike their traditional counterpart, these contracts have no expiration date, with positions being held as long as margin requirements are met. Perpetual futures are offered by a number of major exchanges, like Binance, Deribit and Coinbase International.

In contrast to DEXs like Uniswap, dYdX distinguishes itself by not relying on an automated market maker (AMM) to facilitate trading. Instead, it uses a traditional orderbook and matching model to cater to the needs of sophisticated traders and institutions.

dYdX v4: From an Ethereum App to a Cosmos App-Chain

dYdX has had a unique journey as an exchange, continually adapting to shifting user demands and trade-offs in blockchain scalability. It initially launched in 2017 as a decentralized application on Ethereum mainnet, offering margin trading, lending, and borrowing services. This period, often referred to as “DeFi Summer,” saw a boom in DeFi protocols, with the emergence of Uniswap, Compound, Aave, and others creating a competitive environment.

By 2021, dYdX transitioned to a StarkWare Layer-2 solution, becoming one of the earliest major applications to migrate from Ethereum mainnet to a Layer-2 network. Unsustainably high gas fees during periods of congestion, and limited throughput on Ethereum Layer-1 became a bottleneck for user experience and scalability, prompting the launch of dYdX v3, built on StarkWare's StarkEx (a ZK-rollup based L2).

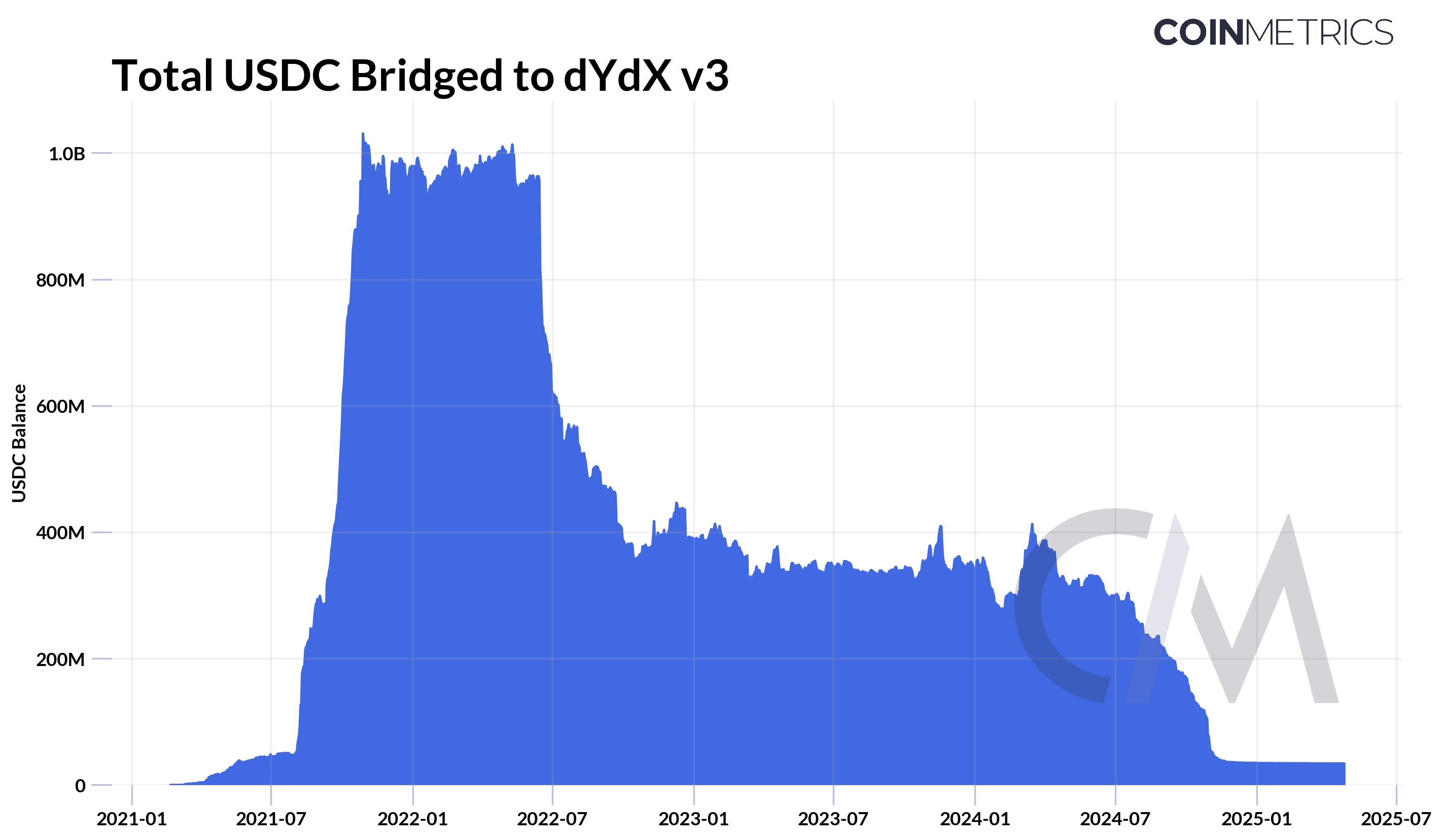

This move significantly improved dYdX’s competitiveness and made high-frequency trading use-cases more feasible. By 2022, the balance of USDC (the primary margin and collateral asset on dYdX) locked in the protocol reached 1B USDC, making it one of the top DeFi protocols by TVL and derivatives volume.

While v3 was a major step forward, dYdX still faced limitations: the orderbook and matching engine remained centrally operated. This led to dYdX’s second major transition in late 2023, becoming a standalone application-specific Layer-1 chain (app-chain), built using the Cosmos SDK and proof-of-stake (PoS) consensus. Trades were now settled on the dYdX Chain, with margin collateral (USDC) natively minted on Cosmos.

The shift to a Cosmos app-chain was intended to bring the following key improvements:

Full Decentralization: Moving to its own chain allowed dYdX to decentralize core components like the orderbook & matching engine among validators. It also enabled a shift towards community based governance, adding staking & governance utility to the DYDX token.

Improved Throughput: Cosmos’ architecture offered significantly higher throughput (10,000 transactions per second) which is crucial for delivering better trade execution to compete with the likes of centralized exchanges, but at the expense of leaving Ethereum’s large liquidity base.

Full-stack & Customizability & Control: Building with Cosmos SDK gave dYdX to gain full sovereignty over its infrastructure. This includes customizing parts of the stack (such as off-chain, in-memory orderbooks) to optimize performance, validator operations, fee structures, and addressing maximal extractable value (MEV) risks, albeit with reduced compatibility to EVM based tooling.

Overview of Architecture

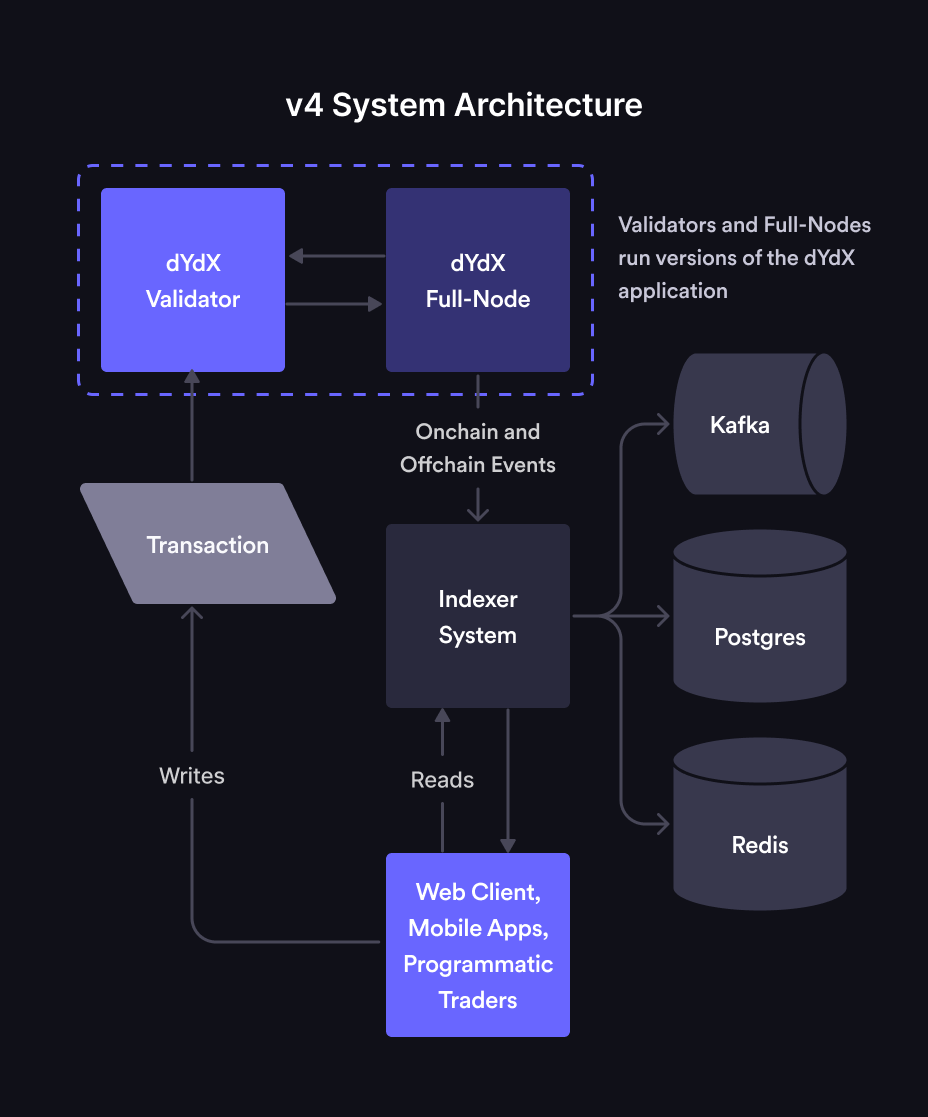

Ultimately, dYdX v4 (or dYdX Chain) is made up of 3 main components: the protocol, the indexer and the front-end. Parts of these components function fully on-chain, while others are off-chain, aiming to achieve a balance between decentralization and performance.

Protocol (Application): The protocol or open-source application is dYdX Chain, an L1 blockchain built on the Cosmos SDK and CometBFT consensus.

Validators: Validators store orders off-chain in an in-memory orderbook, gossip transactions to other validators, and produce new blocks for dYdX Chain through the consensus process (based on DYDX stake-weight).

Full-nodes: Full nodes run the open-source dYdX Chain but do not participate in consensus (zero stake-weight). They connect to validators, gossip transactions, process committed blocks, and maintain a full history of the chain to support the indexer.

Indexer: The Indexer is a read-only service that indexes real-time data from dYdX Chain and serves it via websocket and REST APIs. Much of the market data analyzed in the next section is sourced from the Indexer.

Front-end: dYdX provides open-source front-ends via a web app, iOS app, and Android app to access the exchange.

The lifecycle of an order on dYdX involves all these components. Orders and matching occur off-chain, propagated across validators and full nodes, before final settlement on-chain. This structure optimizes blockspace usage while maintaining decentralization.

Several other decentralized exchanges, like Hyperliquid (a standalone Layer-1) are also pursuing high-performance orderbook models, reflecting industry momentum toward replicating the trading experience of centralized platforms using decentralized infrastructure.

Diving into dYdX Market Data

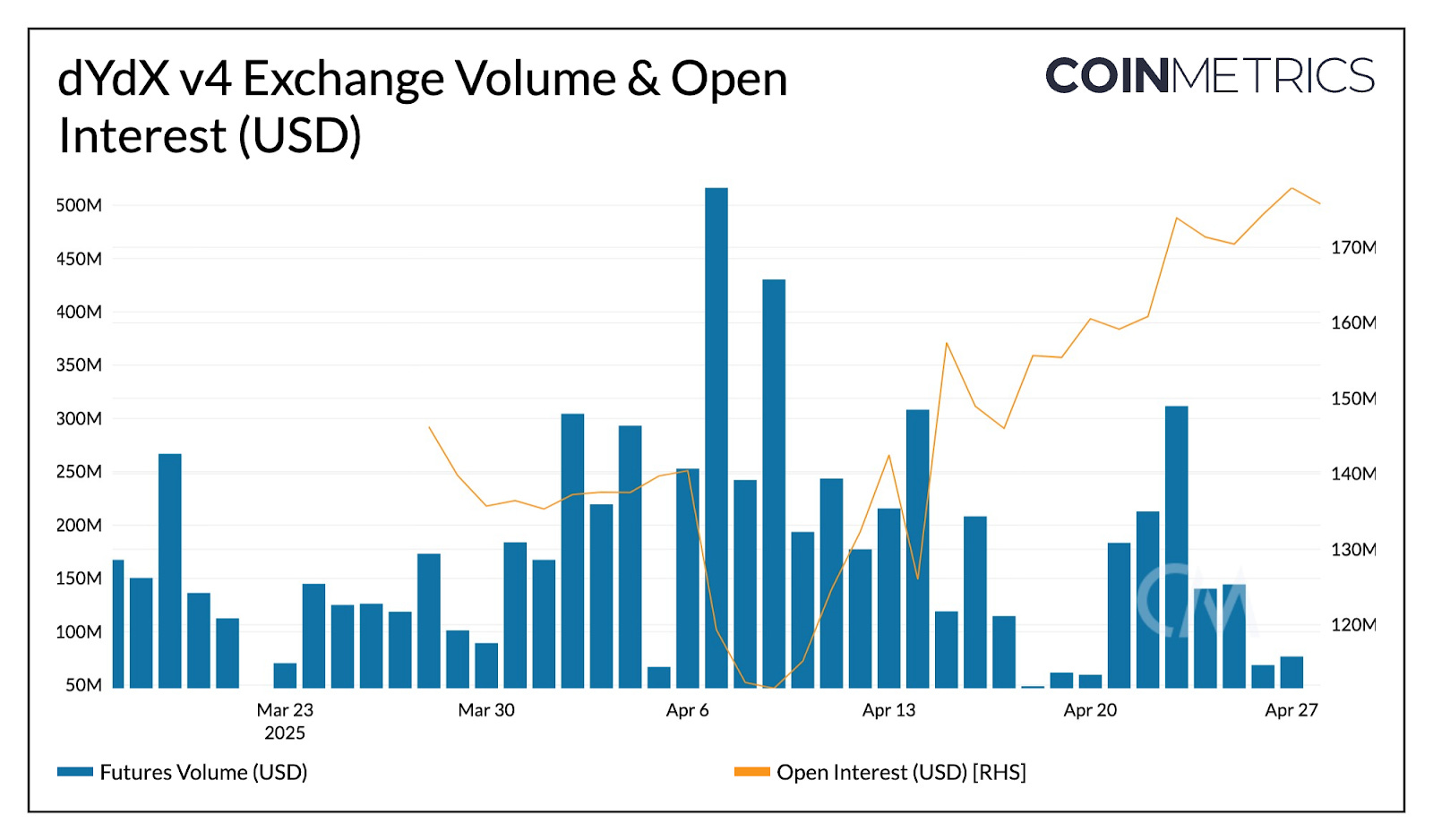

Having understood dYdX’s background and architecture, we can dive into market data for dYdX v4 to examine usage and activity on the exchange. The past two months offer an interesting window into the market amid heightened volatility and macroeconomic uncertainty. Trading volume on dYdX v4 has averaged $200M, peaking at $500M on April 6th, with open interest steadily rising to $175M as market conditions and sentiment reverse.

Source: Coin Metrics Market Data Feed

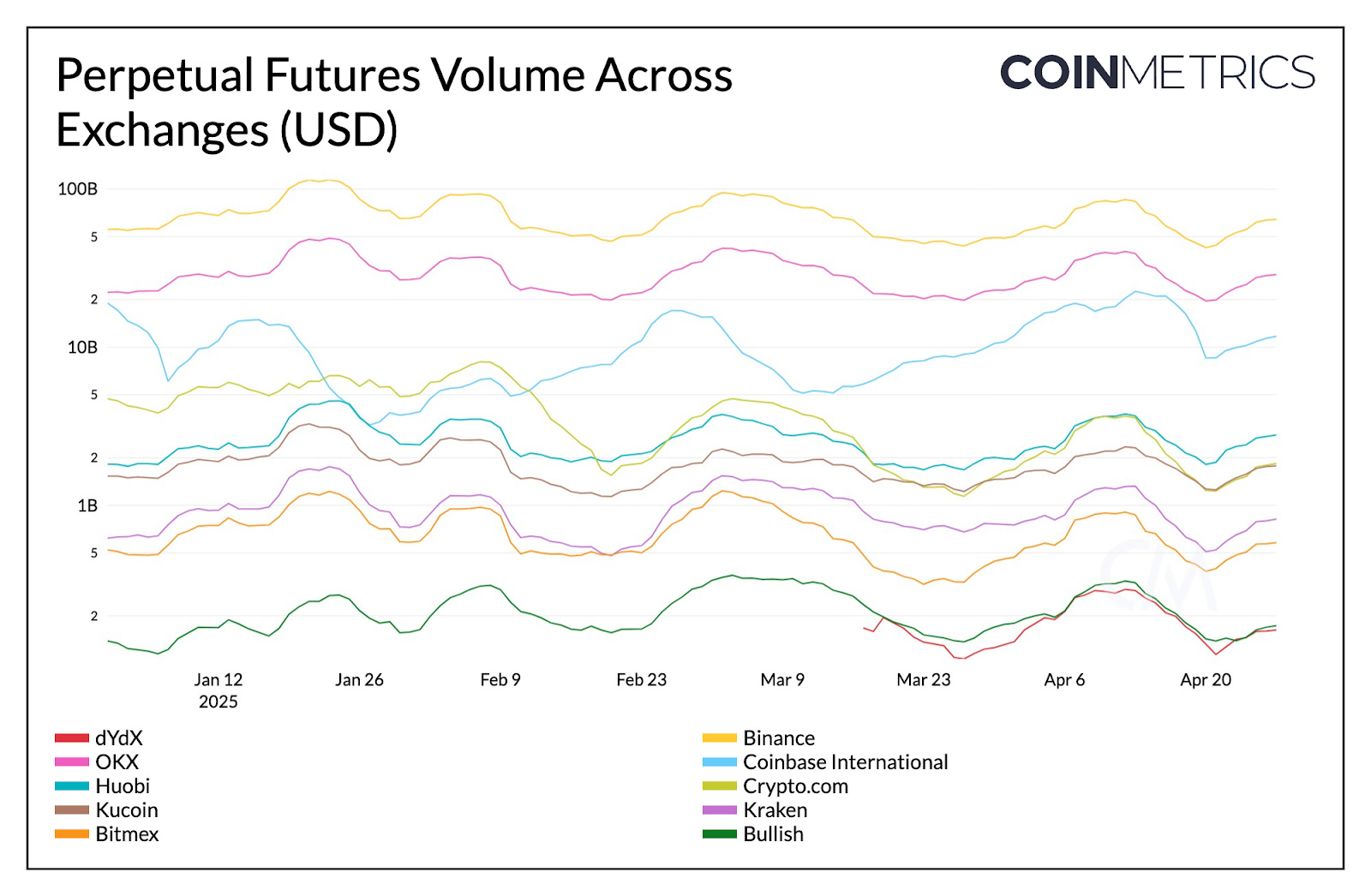

Derivatives exchanges like dYdX remain smaller than centralized exchanges like Binance and others in terms of volume. As demand for on-chain trading infrastructure grows, dYdX has significant room to grow and narrow the gap with prominent exchanges. The chart below shows how perpetual futures trading volume on dYdX compares to other major exchanges.

Source: Coin Metrics Market Data Pro

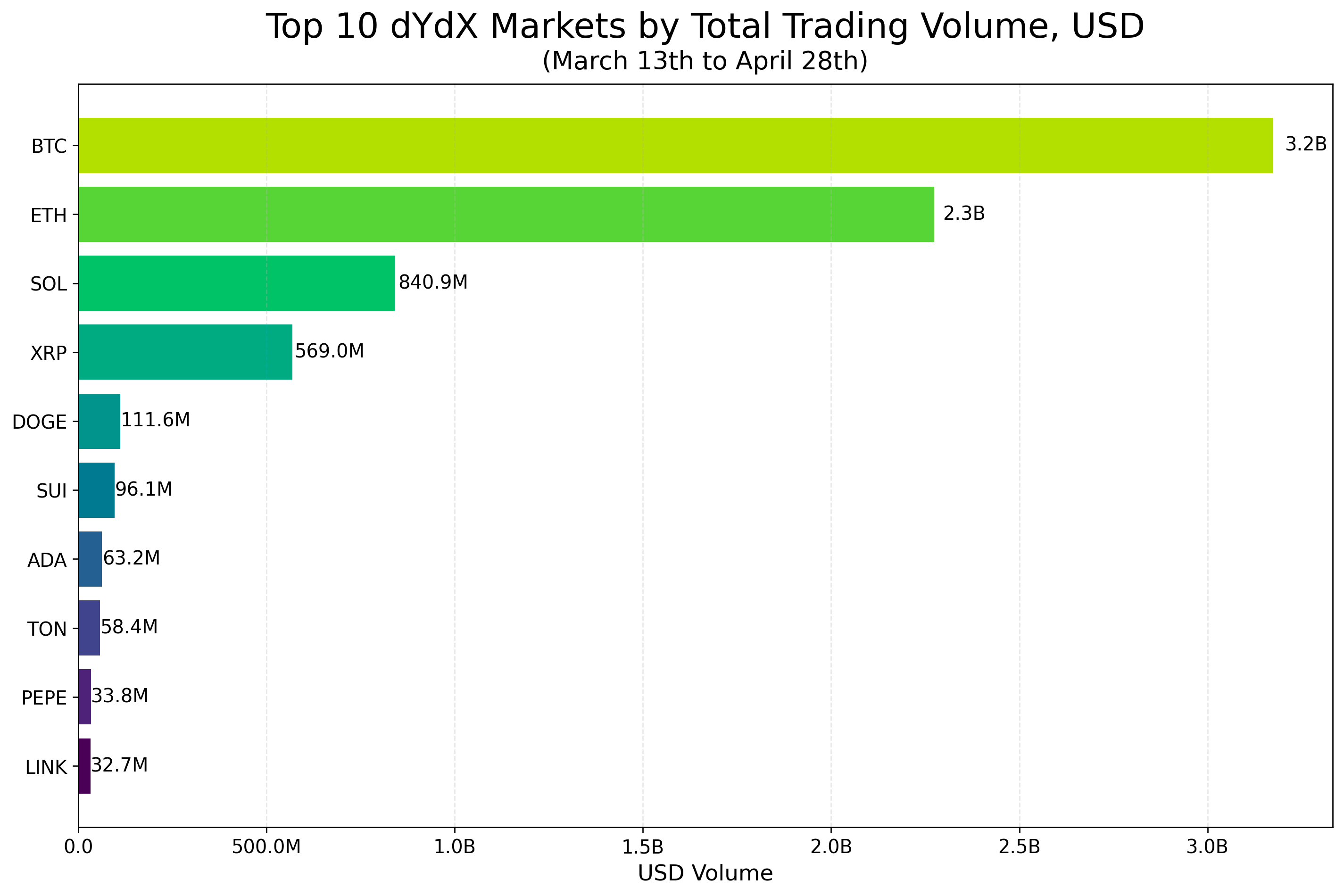

The chart below displays the top 10 markets by trading volume on dYdX (over the period of March 13th to April 28th). Trading activity is concentrated towards large cap and liquid assets, with BTC ($3.2B), ETH ($2.3B) and SOL ($840M) recording the highest total trading volume over the period, followed by major altcoins and meme coins.

Source: Coin Metrics Market Data Feed

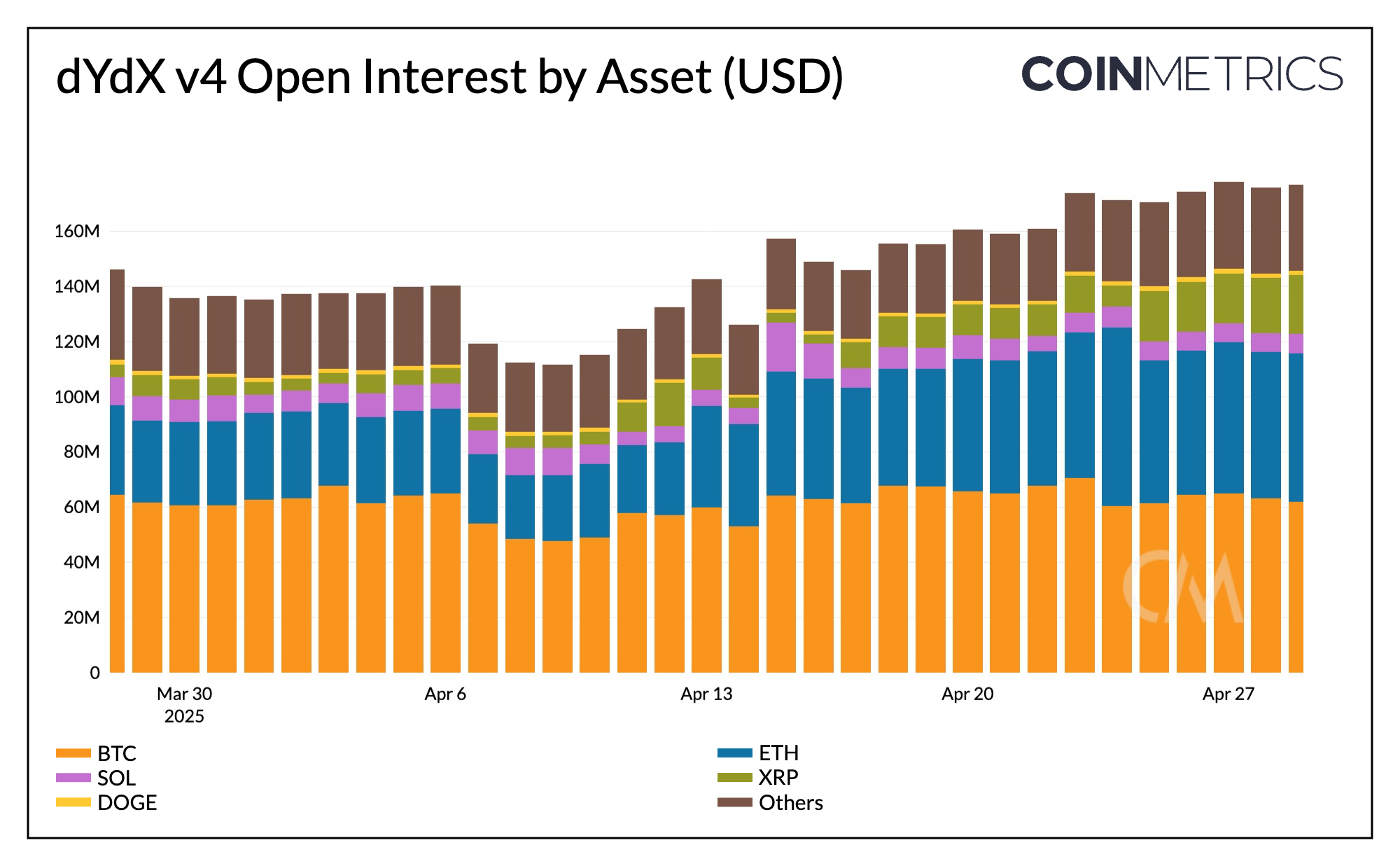

When segmented by asset, 35% (or ~$65M) of open interest is concentrated in BTC, followed by 30% (or ~$53M) in ETH. XRP ranks third, with its share steadily growing toward 11% of total open interest.

Source: Coin Metrics Market Data Feed

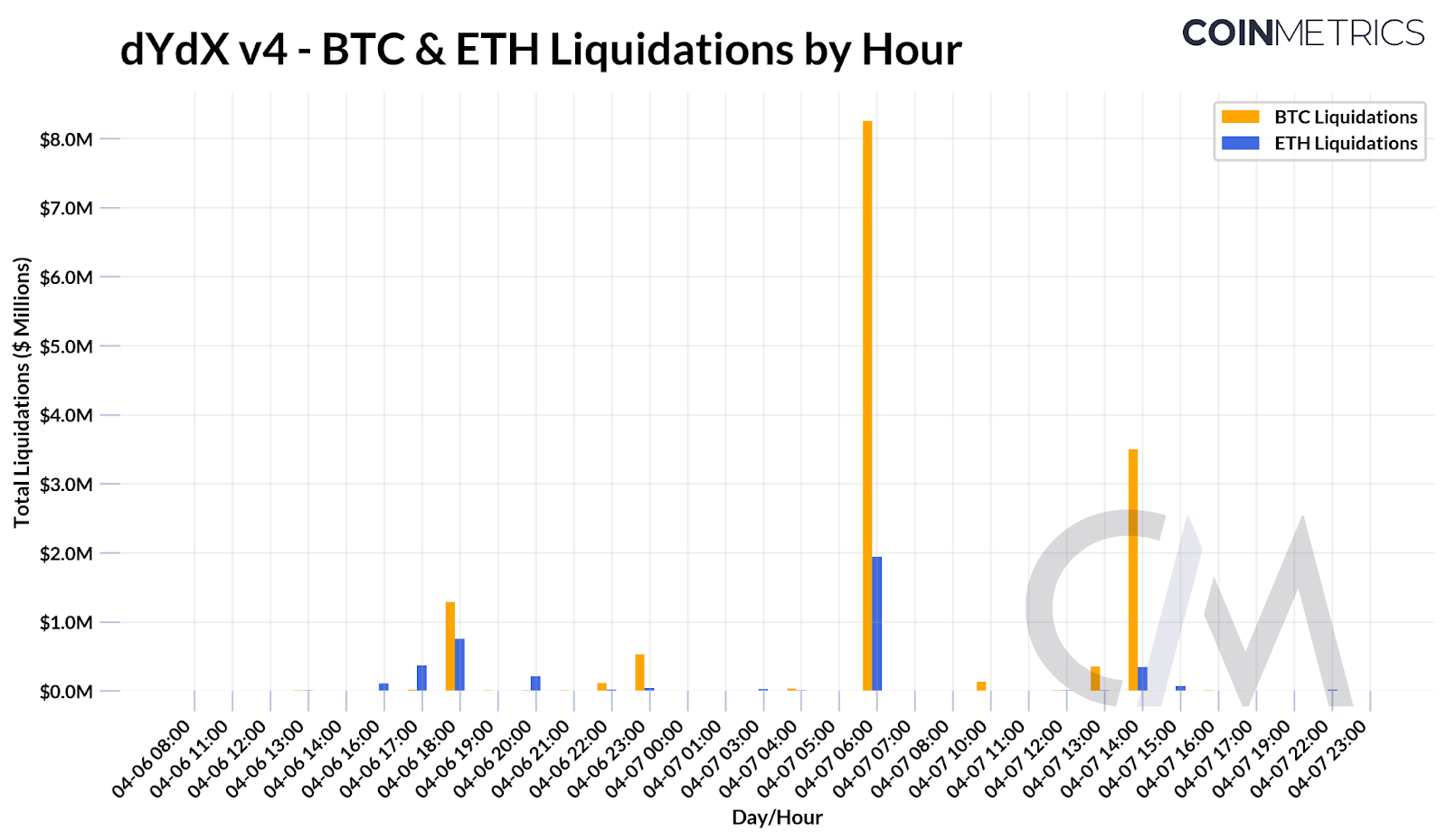

Hourly Liquidations & Funding Rates

For more granular insights on how traders are positioning around key market events, we can explore dYdX market data at a 1-hour frequency. As the effects of Donald Trump’s “Liberation Day” tariffs reverberated across markets, long and short positions in BTC & ETH were liquidated on April 6th, reaching $8M for BTC and $2M for ETH, respectively.

Source: Coin Metrics Market Data Pro

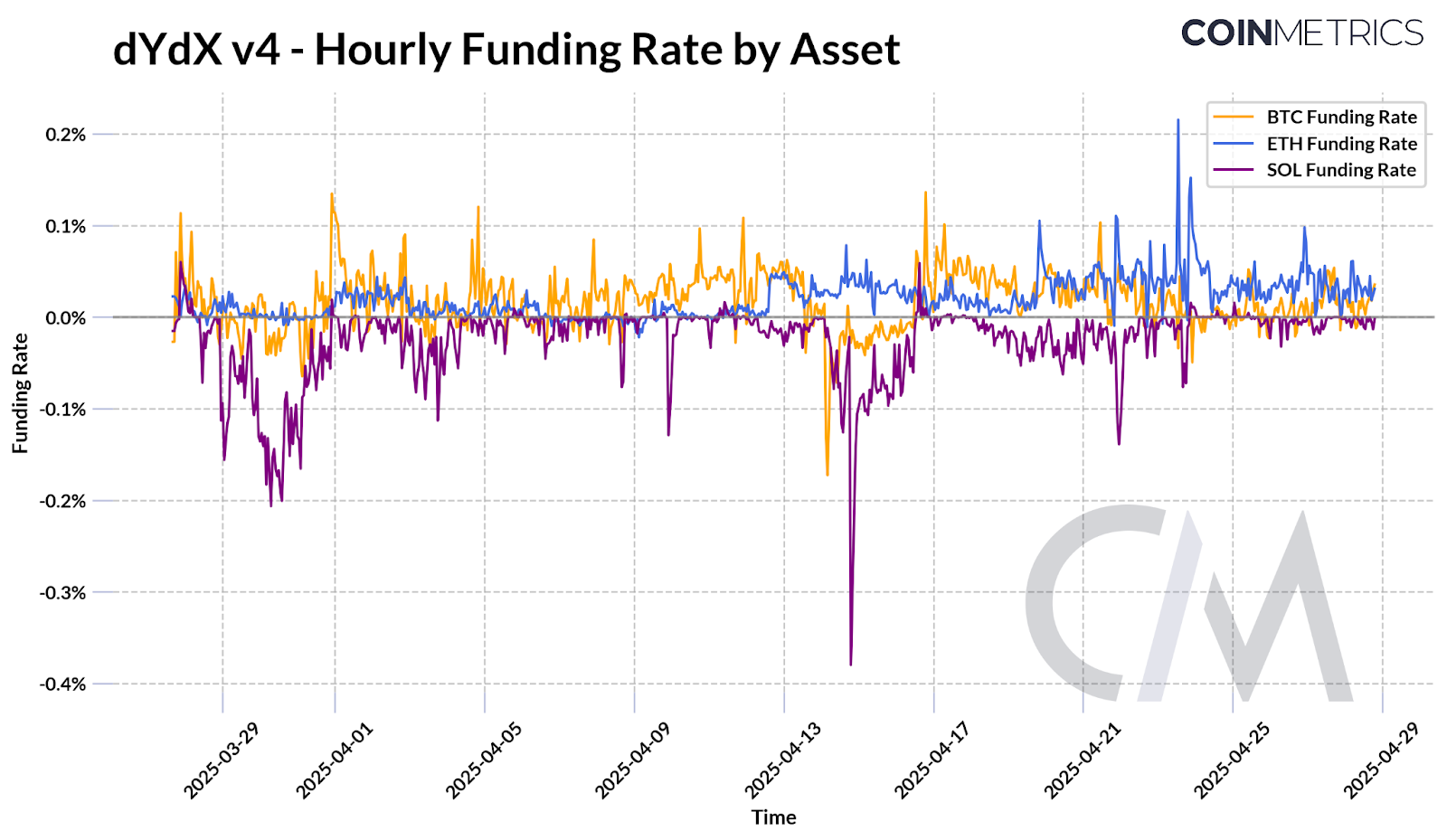

Beyond liquidations, funding rates provide a useful lens into trader sentiment on perpetual futures exchanges like dYdX. They are an important mechanism in perpetual futures markets, helping align the price of the perpetual contract with the spot market price. When funding rates are positive, indicating bullish sentiment, traders holding long positions pay those holding shorts. When funding rates are negative, reflecting bearish sentiment, shorts pay longs, effectively keeping the contract price close to the spot price.

Source: Coin Metrics Market Data Pro

Tracking funding rates can signal the prevailing market bias and conditions for traders to lean long or short. The chart below shows the 1-hour funding rates for major assets on dYdX v4. BTC funding remained largely neutral, while SOL saw a sharp drop around April 13–14, reflecting heavy shorting. ETH funding, by contrast, rose notably on April 23rd, suggesting increased long positioning as ETH briefly overtook BTC as the dominant asset by open interest on dYdX.

Conclusion

dYdX’s transition to an app-chain architecture marked a bold step toward delivering a more decentralized, high-performance exchange experience. While perpetuals trading on dYdX remains smaller in scale compared to leading centralized venues, its model positions it well to capitalize on growing demand for on-chain derivatives infrastructure. Market data suggests healthy activity across major assets, with trends in trading volumes, open interest, liquidations, and funding rates offering signs of maturing usage.

Coin Metrics Updates

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.