In recent months, a specific pattern has repeatedly played out: US President Donald Trump would take measures objectively harmful to the US economy, after which the market would collapse. Upon seeing this situation, Trump would then pressure Federal Reserve Chairman Powell, demanding he lower the federal funds rate - the rate at which the Fed lends to banks. However, the stern Powell would flatly refuse, responding: "No."

Trump hopes to lower rates because this would effectively inject funds into the US economy, stimulating economic activity and boosting the market. He believes this would make his achievements appear remarkable. Powell, meanwhile, wants to follow rigorous economic standards in setting rates, carefully balancing the Fed's dual mission of maximizing employment and maintaining price stability.

Moreover, Powell is committed to maintaining the Fed's independence from political pressure, especially preserving this independence in the public eye. If the market believes the US central bank's independence has been lost, issuing US government bonds could become more difficult. Fundamentally, this means the US would have to pay higher costs to borrow funds, thereby damaging national strength - a particularly serious issue now, as the US carries a massive debt of $30 trillion and needs periodic refinancing.

If the US is forced to refinance at higher rates due to market distrust of the government, interest costs would consume a larger proportion of GDP. In current parlance, the US would be in trouble.

This confrontation has continued until now. Last week, Trump repeatedly suggested intending to fire Powell, and the market reacted poorly. On Monday, Trump attacked Powell on the Truth Social platform as a "complete failure", causing a market collapse. In response, reportedly, US Treasury Secretary Scott Besent has expressed concerns about the risk of firing Powell to Trump. Currently, Trump seems to have compromised, stating on Tuesday that he will not fire the Fed chairman.

However, this process seems more like a continuously deteriorating spiral, with many market observers waiting for the next crisis to erupt. This inevitably raises a question: What consequences would arise if Trump truly cannot restrain his impulse and insists on removing Powell? Especially, what impact would this have on the cryptocurrency industry?

Challenging Fed Authority

It should be noted that the president should not have the right to arbitrarily dismiss the Fed chairman. Section 10 of the 1913 Federal Reserve Act states: "Each Fed board member's term is fourteen years, starting from the end of their predecessor's term, unless the president removes them early for reasonable cause."

While this wording seems ambiguous, in the 1935 "Humphrey's Executor v. United States" case, the Supreme Court ruled that the Constitution does not grant the president "unrestricted dismissal rights", thus the president's dismissal power is limited by legal provisions.

This ruling established the concept of "independent institutions" - organizations belonging to the executive branch but possessing independent powers. While many agencies like the SEC, CFTC, and FTC share this characteristic, the Fed's importance is incomparable.

Economists rarely focus on central bank political control. Politicians' incentives typically focus on the short term, with decision cycles usually measured in years or election cycles. This tendency makes them more inclined to implement short-term effective policies, with directly injecting funds into the economy being the purest form of short-termism. However, fiscal and monetary policies are a delicate art, often involving difficult policy choices.

A typical case is Richard Nixon pressuring Fed Chairman Arthur Burns before the 1972 election to implement expansionary monetary policy to enhance his re-election chances. Nixon indeed won the election overwhelmingly, but what followed was a disastrous "stagflation" - economic stagnation and inflation coexisting, severely damaging the US economy for a decade, with effects still continuing in some hollowed-out industries.

In stark contrast, Paul Volcker implemented a series of radical interest rate hikes from 1979 to 1987 after the stagflation crisis, triggering the "Volcker Shock" and causing multiple painful economic recessions. However, this policy ultimately successfully suppressed inflation, laying the foundation for the economic prosperity of the 1990s and achieving Bill Clinton's outstanding fiscal policy.

These choices are beyond what politicians can or dare to make. This is the crux - economists and critically important market participants firmly believe the Fed must remain independent, or the entire economic structure of American society will face a collapse risk. This is no exaggeration - central banks controlled by politics in Weimar Germany, Peronist Argentina, and Venezuela have all experienced hyperinflation, leading to generational geopolitical decline, even situations where citizens couldn't find food and resorted to eating rats, further facilitating the rise of dictators like Adolf Hitler.

If Trump wants to fire Powell, he must first overturn the precedent of the "Humphrey's Executor" case. Considering the current Supreme Court composition, many legal scholars believe this is not impossible. However, once crossing this "Rubicon", it would mean the president would have comprehensive legal power to arbitrarily command all administrative officials, including the Fed chairman. Most believe this would lead to catastrophic consequences.

But regardless of the outcome, this will be a test for cryptocurrency. Bitcoin's original white paper aimed to eliminate intermediary financial institutions as "trusted third parties" in financial transactions. If the Fed fails and US monetary policy deviates from rational judgment, the "decentralization" principle advocated early by cryptocurrencies will face a severe test.

Trump has recently triggered capital flight, with investors seeking safe-haven assets. Traditionally, during crises, savvy investors would convert risky assets to US Treasury bonds, viewing them as risk-free assets. However, this notion might be outdated. During the tariff crisis's peak, 10-year bond yields approached 5%, and have not fully returned to previous low levels. If Trump truly destroys the Fed, the current capital outflow would seem minor compared to potential massive fund inflows into the cryptocurrency domain.

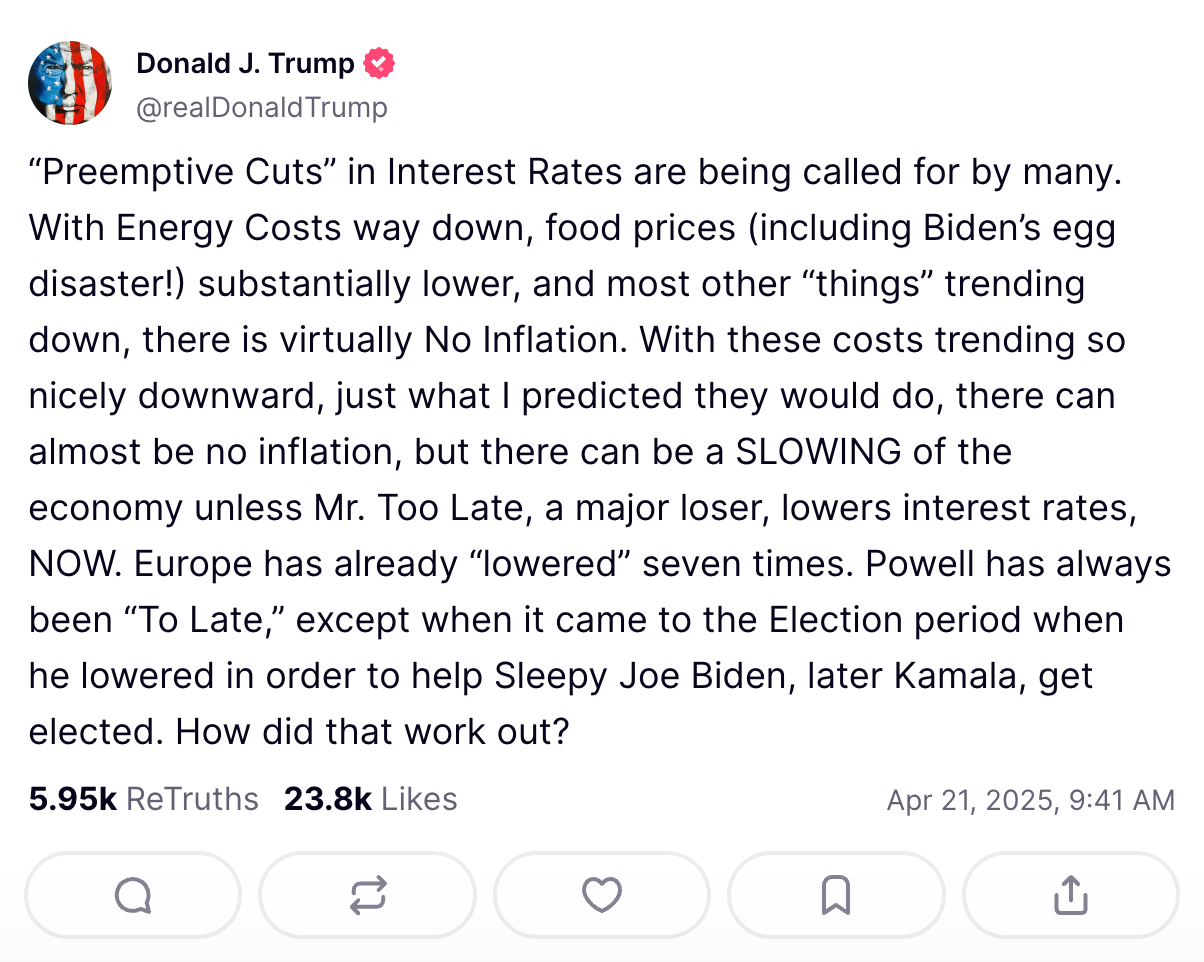

Note: Trump attacks Powell, directly calling him "Mr. Slow"

Historically, Bitcoin prices were highly correlated with the Nasdaq index (though with greater volatility). However, since the tariff crisis began, despite continuously low US securities prices, Bitcoin prices have miraculously begun to surge. This raises speculation: Are we witnessing the long-predicted "decoupling" - where crypto assets achieve their original mission of breaking away from centralized assets and operating independently?

We cannot assert whether this trend will continue, but if Trump truly removes Powell, the answer will soon be revealed.

Out of the Frying Pan, Into the Fire

Of course, from a macro-historical perspective, a global collapse is not entirely beneficial for cryptocurrency, and this crisis will bring significant impacts to multiple domains. Stablecoins would almost immediately face severe consequences.

Over the past decade, two dollar-denominated stablecoins—USDC and Tether's USDT—have dominated the market. Their issuers, Circle and Tether, are not only important systemic institutions but also major buyers of U.S. Treasury bonds, which form the core of their stablecoin reserve assets.

If the Federal Reserve falls into crisis, one of the most direct consequences would be a sharp increase in the risk of U.S. Treasury bond default. Economist Noah Smith once speculated that Trump might try to address the U.S. sovereign debt issue through "debt restructuring":

"I suspect Trump will use the method he typically employs in the business world—when debt cannot be repaid, he will seek a low-cost bailout; if bailout is hopeless, he will directly declare bankruptcy."

In fact, Trump himself hinted at this possibility in February this year, claiming he could potentially reduce debt through some "technical manipulation":

"There is indeed a risk with U.S. national debt, which could become an interesting issue... Perhaps many of these debts simply 'don't count'. In other words, some debts might be fraudulent, so the actual debt scale could be lower than we imagine."

If the U.S. experiences a sovereign debt default, the Treasury bond reserves held by Circle and Tether would directly shrink in value, leading to insufficient stablecoin collateral and potentially triggering a bank run. Although the market might ultimately stabilize, if the situation deteriorates, the collapse of mainstream stablecoins could become unavoidable.

This impact would create a domino effect: smart contracts collateralized by stablecoins would be forced to liquidate positions, and panic would spread throughout the entire cryptocurrency market.

However, these technical consequences might be more "mild" compared to the political costs triggered by a Federal Reserve crisis. After all, for the cryptocurrency market, Treasury bonds are not the only systemic risk assets. The U.S. dollar has maintained its status as a global reserve currency for decades, backed by solid logical support—the dollar's relative strength and stability make it the preferred choice for international trade settlement. However, if the U.S. government credit supporting the dollar becomes unstable, this pattern might fundamentally change.

As more international trade is denominated in euros or renminbi, regulatory bodies in the EU and China will gain greater authority to monitor fiat currency flows through cryptocurrency channels. An unnamed prominent cryptocurrency industry lawyer stated directly:

"I believe China will fill part of the market gap, and the EU will occupy most of the remaining share. But whether it's the Chinese Communist Party's strict regulation or the EU's excessive intervention based on different objectives, neither is favorable for the cryptocurrency industry. This situation is concerning."

In this context, market funds might shift towards uncolateralized native crypto assets, but such assets have almost no precedent for large-scale transactions in the real world. More likely, the stablecoin crisis will push the currently ascending cryptocurrency industry into long-term stagnation.

Ultimately, no one can predict whether Trump will fire Powell, or even confirm if he has such authority. Similarly, no one can anticipate what chain reaction his decisions might trigger. But just as a butterfly's wings in Argentina might cause a tornado in Prague, every "whisper" from Trump in the West Wing of the White House could permanently alter the fate of the Block chain industry—either vindicating or causing its collapse.

Whether we want to or not, this storm can no longer be avoided.

We can only embark on this unknown journey together.