The market, project, currency, and other information, views, and judgments mentioned in this report are for reference only and do not constitute any investment advice.

Written by 0xWeilan

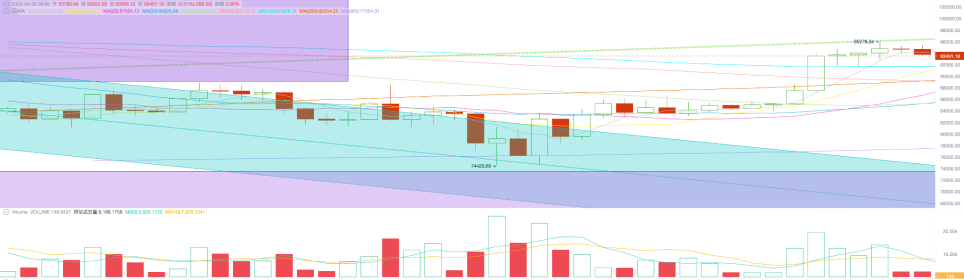

This week, BTC opened at $85,177.33 and closed at $93,780.57, rising 10.10% for the week with a volatility of 12.73%, achieving three consecutive rebounds with expanded volume. On Monday, it strongly broke through the key 120-day moving average and remained above it throughout the week, showing a strong long intention.

Trump's "reciprocal tariff war" is running in the second stage - "negotiation". The White House continues to release positive progress signals, while the other negotiating party remains vague, indicating that the negotiation results are not clear.

Trump clearly stated that he would not dismiss Powell, which has diluted the market's trading theme in recent weeks - the Fed's independence being damaged and the "triple kill" of stocks, bonds, and exchange rates causing greater chaos in the US economy and finance. Stocks, bonds, and exchange rates have stabilized and rebounded.

The Federal Reserve has released positive signals externally. Cleveland Fed President and 2026 FOMC voter Beth Hamark said the Fed is capable of acting quickly if the situation changes. Fed Governor Waller also stated that a severe decline in the job market might prompt the Fed to push for more and faster rate cuts.

The performance of global markets, especially the US financial trading market in recent weeks, fully proves the irrationality and arbitrariness of the "reciprocal tariff war" and its huge impact on the world economic system. The compromise taken by Trump and the Fed in response to the "triple kill" of stocks, bonds, and exchange rates indicates what we mentioned in last week's report - that politics, economy, and markets will first run along a rational path in the medium and long term.

However, it needs to be noted that the market rebound is a temporary elimination of concerns about a potential market crash and economic recession caused by the "reciprocal tariff war". The further market trend will depend on whether the "reciprocal tariff war" can end in time and whether the US economy will truly head towards recession. Based on this judgment, the ongoing Q1 financial report disclosure appears particularly important.

Policies, Macro Finance, and Economic Data

In statements by President Trump and his staff, the reciprocal tariff war is making good progress, especially negotiations with China, with Trump expressing confidence in reaching a mutually satisfactory agreement. However, the Chinese government directly points out that no negotiations have been conducted.

Countries actually in negotiations include Japan and South Korea, with a high probability of reaching conditions favorable to the US, and the degree of "conceding interests" will set an example for other countries.

The US-China negotiations, which are truly difficult, show no signs of entering actual consultation. Therefore, the second stage of the "reciprocal tariff war" has just begun and is far from achieving significant progress. This constrains the time and space of the market rebound, making it difficult to be optimistic in the short term.

Powell's speech this week focused on the inflation and economic uncertainty brought by Trump's tariff policy, setting the tone for the upcoming May monetary policy meeting and reaffirming the Fed's independence.

His tone remained consistent - policy driven by data, maintaining interest rate stability. He will not yield to political pressure for rate cuts but hints that policy might adjust if inflation or employment data significantly changes. Other Fed members' statements emphasized more of the "dovish" side, suggesting the possibility of a June rate cut.

As of the weekend, the CME FedWatch board shows a 62.7% probability of a June rate cut. With the market rebound, this probability has noticeably declined compared to the past two weeks.

On April 23, the Fed Beige Book revealed that 8 out of 12 Federal Reserve districts reported economic activity as "essentially unchanged", with overall economic growth slowing. Only a few districts (such as Atlanta and Dallas) reported slight growth, while districts like Boston and Chicago reflected deteriorating economic prospects. Businesses strongly reacted to tariff policies, with inflation expectations in 2025 rising to 3.5% in multiple districts, manufacturing activities further contracting, and manufacturing PMI dropping to 48.5. Consumer spending grew moderately, but high prices and tariff expectations began to weaken consumer confidence. Retailers reported inventory backlogs, especially for imported goods, with sales growth below expectations. Employment levels remained stable overall, but hiring activities weakened, with some districts reporting increased layoffs, particularly in retail and manufacturing. Wage growth slowed but remained above pre-pandemic levels, with labor shortages still existing in technology and high-skill positions.

The Beige Book content is one of the Fed's focus points. Its content indicates that the negative impacts of tariffs are emerging, but the extent remains unclear.

Accompanied by dovish statements from Trump and the Fed, extreme market panic has been alleviated. The US dollar index rebounded to 99.613 after falling to 97.991. The 2-year Treasury yield fell 1.42% to 3.7560%, and the 10-year Treasury yield dropped 2% to the neutral zone of 4.245%. Risk markets performed better, with Nasdaq, S&P 500, and Dow Jones achieving weekly rebounds of 6.73%, 4.59%, and 2.48% respectively.

Gold, with yield uncertainty, rose to $3,499.93/oz initially but then dropped significantly over two days, turning negative for the week.

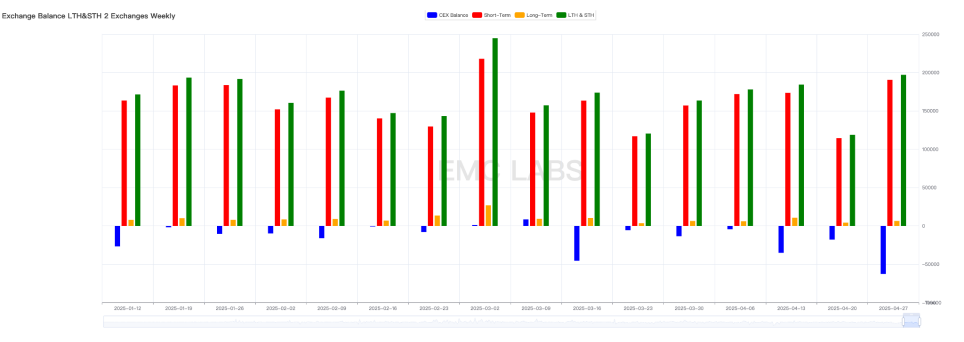

Selling Pressure

With significant price rebounds, on-chain selling scale increased this week, mainly from short-term holders. Total on-chain selling reached 197,040.26 coins, with 190,568.61 from short-term holders and 6,471.65 from long-term holders. Exchange outflows significantly increased to 62,696.12 coins, the largest net outflow week in this period, which not only relieved market selling pressure but also showed strong market buying enthusiasm.

Long and short-term selling scale statistics

Long-term holders increased positions by over 120,000 coins this week. Another noteworthy long group is the shark group (address clusters holding 100-1000 BTC), with a weekly increase of nearly 30,000 coins.

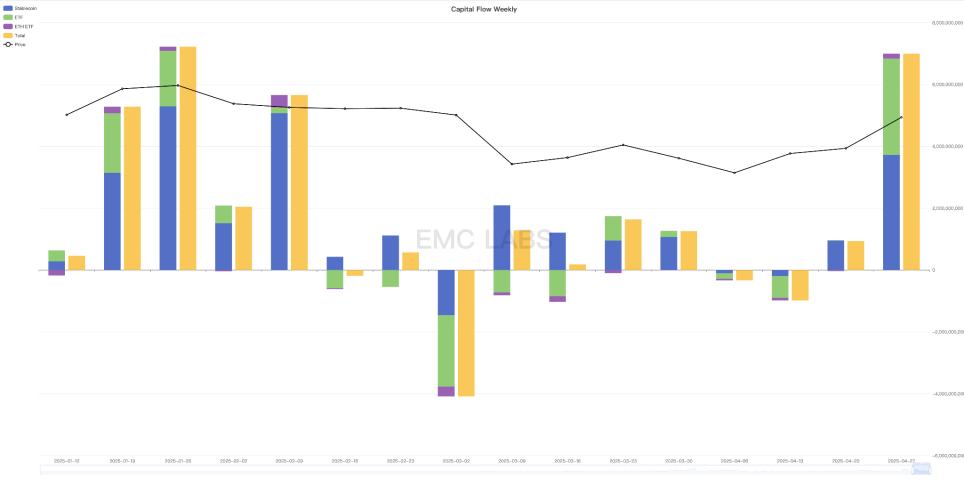

Capital Inflow and Outflow

With the Fed and Washington returning to rationality, stablecoin and ETF channel funds flowed in this week, totaling nearly $7 billion.

Crypto market capital inflow and outflow statistics (weekly)

Out of 7 trading days, 6 days recorded net inflows, showing very aggressive mid-to-long-term fund entry. However, it needs to be noted that as BTC price rebounds to the $95,000 line, with tariff war conflicts and economic recession concerns still present, and the most optimistic rate cut being at least a month away, market divergence remains, and short-term volatility is inevitable.

Cycle Indicators

According to eMerge Engine, the EMC BTC Cycle Metrics indicator is 0.50, indicating the market is in an upward continuation period.

EMC Labs was established in April 2023 by crypto asset investors and data scientists. Focusing on blockchain industry research and crypto secondary market investment, with industrial foresight, insights, and data mining as core competencies, committed to participating in the booming blockchain industry through research and investment, and promoting blockchain and crypto assets' benefits to humanity.

For more information, please visit: https://www.emc.fund