Vintage originally referred to the "year" of wine, where a good year is a gift from nature, and a poor year is marred by weather and soil limitations. In funds, the "establishment year" is often called Vintage, just as the wine's vintage reflects its terroir, and the fund's year is a snapshot of the economic cycle, directly affecting returns.

For crypto funds established during the pandemic's massive liquidity injection period, they are currently experiencing painful backlash from a "bad year".

Rise and Fall by Bubble

Recently, crypto fund investors have been sharing their grievances on social media. The trigger was Web3 fund ABCDE announcing that their $400 million fund will no longer invest in new projects or raise funds for a second phase. The fund's founder, Du Juan, stated that over the past three years, ABCDE has invested over $40 million in more than 30 projects, and despite the current challenging market environment, their internal rate of return (IRR) remains globally leading.

ABCDE's investment pause reflects the current dilemma of crypto VCs: institutional fundraising and project investment enthusiasm are both declining, token listing lock-up models are increasingly questioned, and flexible investors are even hedging their portfolios through secondary market and hedging operations. Amid high macro interest rates, unclear regulations, and internal industry challenges, crypto VCs are experiencing their most severe adjustment period. Especially for crypto funds established around 2021, the current environment has intensified the difficulty of exit strategies.

Cypher Capital's co-founder Bill Qian disclosed the performance of their invested funds, "We invested in 10+ VC funds this cycle, with excellent GPs who captured top projects. But for our VC fund investments (as LPs), we've already done a 60% accounting write-down, hoping to recover 40% of the principal. Can't help it, the investment vintage of 2022/23 caught us, so we must accept it. Sometimes, you've done nothing wrong, just defeated by time and the vintage." However, he is optimistic about the next crypto VC cycle, believing in the principle of reversal. Just like the Web2 VCs in Silicon Valley were wiped out in 2000, subsequent years became fertile ground for innovation and investment.

The "capital carnival" of 2021 to 2022 was not only driven by internal industry creativity and market sentiment boosted by DeFi, NFT, and chain games but also related to the special era's background. Affected by the COVID-19 pandemic, many central banks implemented massive quantitative easing and zero interest rates, leading to global liquidity flooding, with "hot money" seeking high-return assets—an environment academia and industry termed "Everything Bubble". The emerging crypto industry became one of the significant beneficiaries.

Facing such a trend, crypto venture capital firms that easily obtained funds began "lifting" investments, betting on conceptual tracks with large-scale investments, with less rational analysis of projects' intrinsic value. Similar to the tech stock bubble, this crazy investment and short-term surge detached from fundamentals essentially represented "expectation pricing" under ultra-low capital costs. Crypto VCs invested heavily in overvalued projects, thus planting hidden dangers.

Borrowing from traditional equity incentive mechanisms, token lock-up mechanisms aim to prevent project parties and early investors from concentrated short-term selling by long-term phased token release, thus protecting ecosystem stability and retail investor interests. Common design mechanisms include "1-year cliff + 3-year linear release", or even longer 5-10 year lock-ups to ensure teams and VCs cannot cash out before project maturity. This design itself isn't problematic, especially for an industry that has grown wildly for years. To dispel concerns about project parties and VCs "misbehaving", token lock-up constraints are an effective method to enhance investor confidence.

However, when the Federal Reserve began quantitative tightening and raising rates in 2022, liquidity quickly tightened, and the crypto industry's bubble burst. As these inflated valuations rapidly fell, the market entered a "value restoration" painful stage. Crypto VCs, having reaped what they sowed, gradually fell into their "darkest moment"—many institutions not only lost significantly in early investments but were also questioned by retail investors who mistakenly believed they had gained substantial returns.

According to data recently released by STIX founder Taran Sabharwal, almost all tracked projects experienced significant valuation drops, with SCR and BLAST showing year-on-year declines of 85% and 88% respectively. Multiple data indicate that many crypto VCs who promised locked positions might have missed better secondary market exit opportunities last year. This forced them to seek alternative strategies—Bloomberg reported that many venture capitals secretly collaborated with market makers, hedging lock-up risks through derivatives and short positions to profit during market declines.

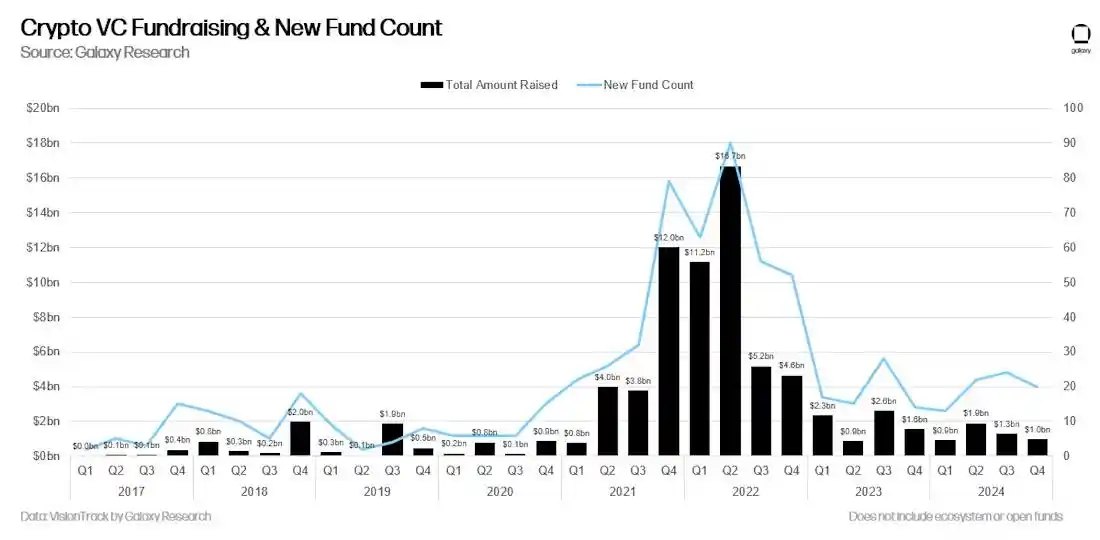

In a weak market, fundraising for new crypto funds is equally challenging. Galaxy Digital's report shows that although the number of new funds increased in 2024, it remains the weakest year for crypto venture capital financing since 2020, with 79 new funds raising $5.1 billion, far below the frenzy levels during the 2021-2022 bull market.

According to a previous research article by PANews, an incomplete statistic showed that Web3-related investment funds launched in the first half of 2022 reached 107, with a total amount of $39.9 billion.

Meme and Bitcoin ETF's Fund Diversion

In an industry lacking clear product narratives and practical use cases, communities began leveraging Meme hot topics to generate discussion and traffic. Meme tokens repeatedly triggered trading frenzies, attracting massive short-term speculative funds through the "instant wealth myth".

These Meme projects often experience rapid one-time hype but lack sustained support. As on-chain "casino" narratives continue spreading, Meme tokens began dominating market liquidity, occupying user attention and capital allocation focus. This caused some truly promising Web3 projects to be squeezed and obscured, with limited exposure and resource acquisition capabilities.

Simultaneously, some hedge funds started exploring the Memecoin market to capture excess returns from high volatility. This includes the venture capital firm Stratos, supported by a16z co-founder Marc Andreessen. The hedge fund launched a liquidity fund holding the Solana-based meme coin WIF, generating an impressive 137% return in the first quarter of 2024.

Besides memes, another milestone event in the crypto industry—the launch of Bitcoin spot ETF—might also be a potential reason for the Altcoin market's stagnation and VC challenges.

Since the first Bitcoin spot ETFs were approved in January 2024, institutions and retail investors can directly invest in Bitcoin through regulated channels, with traditional Wall Street asset management giants entering the market. The ETF attracted nearly $2 billion in fund inflows within its first three days, significantly enhancing Bitcoin's market position and liquidity. This further strengthened Bitcoin's "digital gold" asset attributes, attracting broader traditional financial participants.

However, with Bitcoin ETF's emergence providing a more convenient, lower-cost compliant investment path, the industry's original fund circulation logic began changing. Large amounts of funds that might have flowed to early venture capital funds or Altcoins chose to remain in ETF products as passive holdings. This not only interrupted the previous fund rotation rhythm of Altcoins rising after Bitcoin but also increasingly decoupled Bitcoin from other tokens in price trends and market narratives.

Under the continuous siphon effect, Bitcoin's dominance in the entire crypto market continues to rise. According to TradingView data, as of April 22, Bitcoin's market dominance (BTC.D) has increased to 64.61%, reaching a new high since February 2021. This indicates that Bitcoin's position as an "institutional entry point" is becoming increasingly consolidated.

The impact of this trend is multi-layered: traditional capital is increasingly concentrated on Bitcoin, making it difficult for Web3 startup projects to obtain sufficient financing attention; for early VCs, token exit channels are limited, secondary market liquidity is weak, leading to extended payback cycles and difficult profit realization, forcing them to slow down or even suspend investments.

Moreover, the external environment is equally severe: high interest rates and increasingly tight liquidity make LPs hesitant to allocate high-risk investments, while regulatory policies continue to evolve but remain incomplete.

As Rui from Hashkey Capital wrote on Twitter: Will there be a desperate counterattack like in 2020? Many friends are pessimistic, so they are leaving the market. Their logic is simple and effective. On one hand, all users who should have entered have already entered, everyone is accustomed to the Casino-style gameplay, accustomed to defining project quality by pumping and dumping, just likeated shorting ETH, user attributes have been stereotyped. On the other hand, it's difficult to see the emergence of large-scale on-chain applications, Social, Gaming, ID, and other fields have been "attempted to be reconstructed" by Crypto, but ultimately everyone found it to be a mess, making it hard to find new Infra opportunities and new infinite imagination.

Under multiple pressures, the "dark moment" of crypto VCs may continue for quite some time.