Author: Zhang Yaqi

The market is shifting from "American exceptionalism" to "American negation". Bank of America global strategist Michael Hartnett suggests that investors should sell US stocks on rallies and buy international stocks and gold on dips.

Hartnett noted in his research report released on the 24th that recent capital flows show US stocks experienced an outflow of $800 million, while gold saw an inflow of $3.3 billion, indicating an increasing market preference for gold.

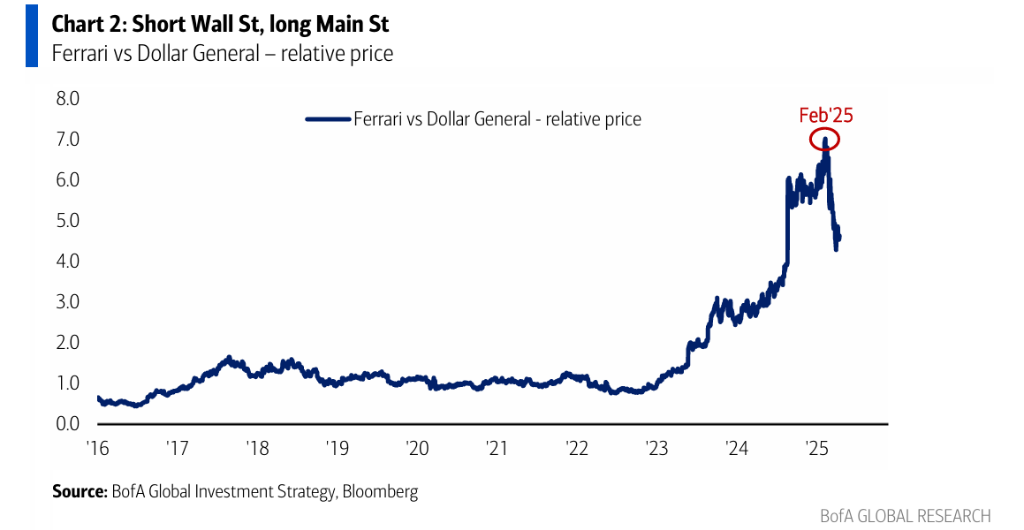

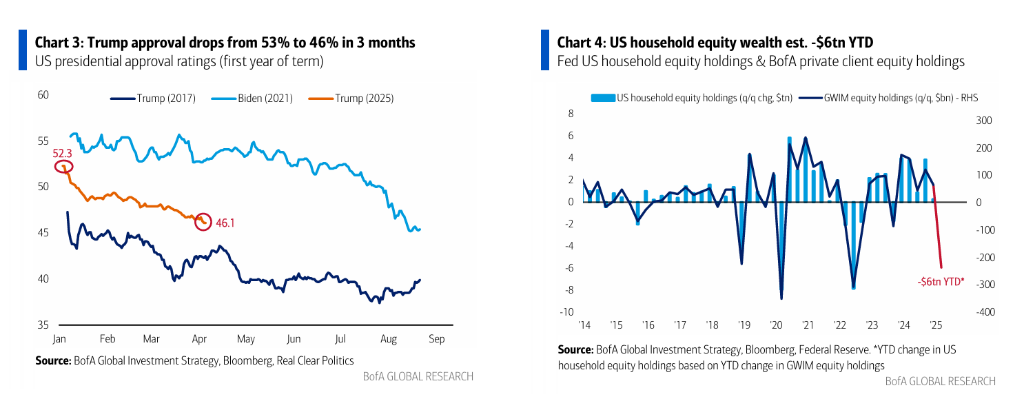

As global economic rebalancing occurs, capital is flowing from the US market to other regions, especially emerging markets and Europe. This capital flow trend supports gold prices. Year-to-date, gold has performed best (+26.2%), followed by government bonds (+5.6%) and investment-grade bonds (+3.9%), while US stocks have declined by 3.3%. US household stock wealth has shrunk by approximately $6 trillion this year.

Hartnett recommends "Stay BIG, sell rips", which means going long on Bonds, International Stocks, and Gold. Investors should sell US stocks during market rallies rather than blindly chasing gains.

Hartnett: Market is at a Historic Turning Point

Hartnett stated that from the beginning of the year to now, financial asset performance shows a clear trend: gold leads (+26.2%), bonds perform well (government bonds +5.6%, investment-grade bonds +3.9%), while US stocks (-3.3%) and the US dollar (-8.5%) have significantly declined.

Recent capital flows show that stock markets in all regions have seen inflows (Europe $3.4 billion, emerging markets $1 billion, Japan $1 billion), with only US stocks experiencing an outflow of $800 million; gold saw an inflow of $3.3 billion.

The current trend indicates a rebalancing of the relationship between Wall Street and Main Street. Bank of America's data shows that US household stock wealth has shrunk by approximately $6 trillion this year, with the ratio of US private sector financial assets to GDP falling from over 6 times to 5.4 times.

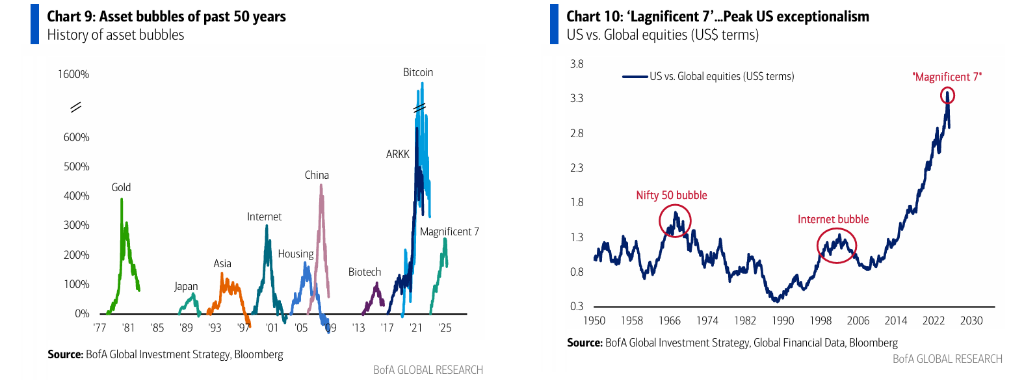

Hartnett believes this change marks the end of an era of "never been so prosperous" - characterized by low interest rates, over $30 trillion in global policy stimulus, 9% US government deficit, and AI boom.

Three Key Driving Factors of Transformation

Hartnett believes the current market correction is triggered by "3B" factors:

Bonds: US Treasury yields have risen 50 basis points fastest since May 2009

Base: Trump's support rate has dropped from 53% to 46%

Billionaires: Tech giants' market value has evaporated by over $5 trillion

To reverse the "sell on rallies" trend, the market needs three factors:

Rate cuts: Fed rate cut expectations (market expects 65% chance of rate cut on June 18 FOMC, 100% for July 30 meeting)

Tariffs: Easing of Trump's tariff policies

Consumers: Maintaining resilience in US consumer spending

Global Revaluation and Dollar Weakness

Hartnett states that the major trend in 2025 is reaching peak valuations for stocks and credit. Historically, S&P 500 P/E ratios:

20th century average was 14x (during world wars, Cold War, Great Depression, stagflation)

21st century average is 20x (globalization, technological progress, loose monetary policy)

First half of 2020s, 20x becomes the P/E ratio floor

Future may see 20x as the P/E ratio ceiling

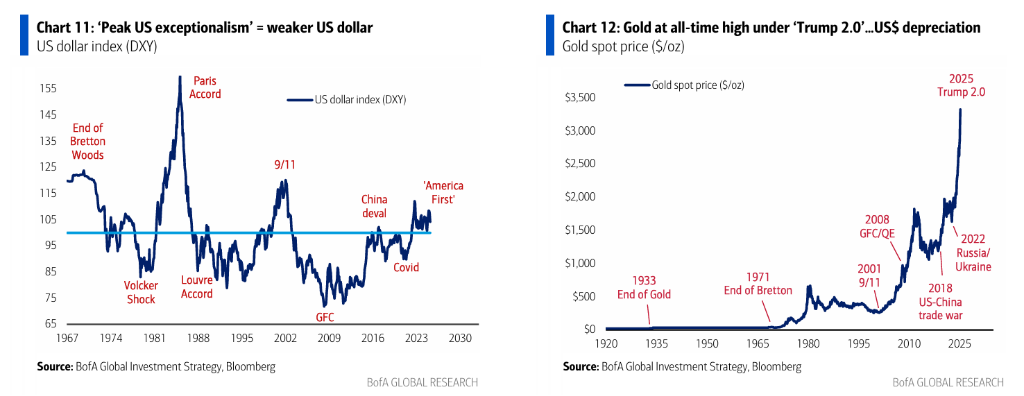

Hartnett believes continued depreciation of dollar assets is the clearest investment theme, with gold price surge being a clear signal of this trend. The dollar depreciation trend will benefit commodities, emerging markets, and international assets (Chinese technology, European/Japanese banks).