- Complex on-chain activities are being simplified, and the technical infrastructure is mature;

- Everything old faces the historical opportunity of being reshaped, and new opportunities have emerged;

- Intent, TG/Onchain Bot, and AI Agent all need to solve the authorization problem.

On April 16, Glider completed a $4 million financing led by a16z CSX (startup accelerator). It was able to gain a foothold in the on-chain investment field, which looks simple but is complicated to implement, thanks to the favor of technical trends such as Intent and LLM. However, DeFi as a whole does need to be reorganized to simplify the investment threshold.

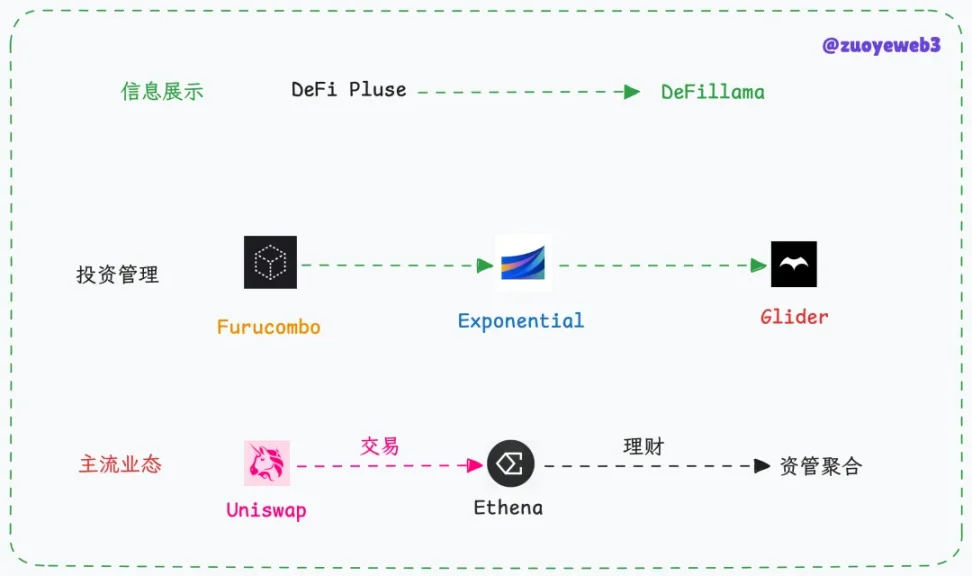

Image description: History of DeFi tools, Image source: @zuoyeweb3

The DeFi Lego era is over, and the era of securely coupled financial management has arrived.

Past: Furucombo failed before it could achieve success

Glider started as an internal startup of Anagram at the end of 2023. At that time, it was in the form of Onchain Bots, which combined different operation steps to facilitate user investment and use.

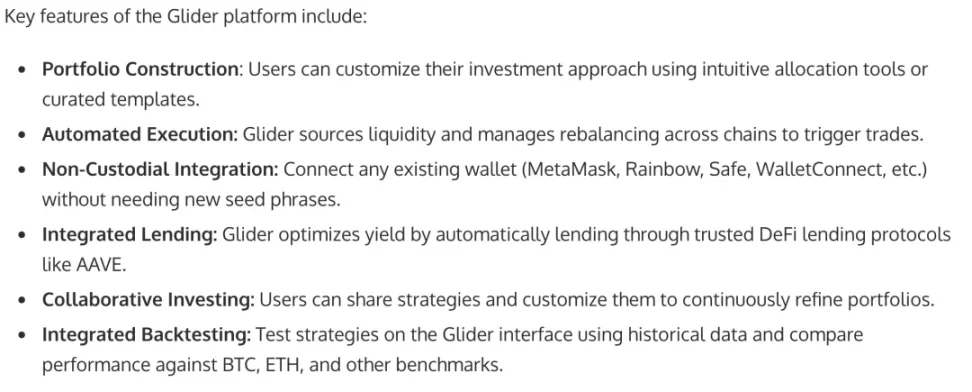

Image caption: Glider function preview, Image source: businesswire

But this is not a new business model. Helping users manage their finances is a long-term business, as is the case with TradFi and DeFi Summer. Currently, Glider is still in the internal research and development stage, and its general idea can be described only from the content of the PR draft:

- Link existing DeFi tools, including leaders in each track, and emerging protocols, and build B2B2C customer acquisition logic through API access;

- It allows users to build investment strategies and supports sharing, so as to facilitate follow-up investment, copy transactions or collective investment in exchange for higher returns.

With the cooperation of AI Agent, LLM, intent and chain abstraction, it is not difficult to build such a stack from a technical perspective. The real difficulty lies in traffic operation and trust mechanism.

The flow of user funds is always sensitive, which is also the most important reason why on-chain products have not yet defeated CEX. Most users can accept decentralization in exchange for fund security, but basically do not accept decentralization to increase security risks.

In 2020, Furucombo received investments from institutions such as 1kx, focusing on helping users reduce panic when facing DeFi strategies. If we have to make a forced analogy, it is most similar to today's Meme Coin tools such as GMGN, except that the DeFi era is a combination income strategy, while GMGN is about discovering high-potential, low-value memes.

However, most people did not stay in Furucombo. The on-chain profit strategy is an open market. Retail investors cannot compete with the whale in terms of servers and funds, which means that most profit opportunities cannot be captured by retail investors.

Compared with the unsustainable returns, security issues and strategy optimization are secondary. In the era of high returns, there is no room for prudent financial management.

Now: The civilian era of asset management

ETFs for the rich, ETS for retail investors.

ETF tools can not only be operated in the stock market, but exchanges such as Binance have also tried them out in 2021. The tokenization of assets from a technical perspective eventually gave birth to the RWA paradigm.

Image description: Exponential page, Image source: Exponential

Furthermore, how to complete the on-chainization of ETF tools has become the focus of entrepreneurship. From DeFillama's APY calculation and display to Exponential's continued operation, it shows that there is a market demand for it.

Strictly speaking, Exponential is a strategy sales and display market, with massive expertise, precise calculations, and manual and AI-assisted strategy decision-making. However, the on-chain transparency means that no one can truly hide efficient strategies from being imitated and modified, which in turn leads to an arms race and ultimately to a flattening of yields.

In the end, it’s just another boring game of big fish eating small fish.

However, it has never been standardized and developed into a project that redefines the market like Uniswap, Hyperliquid or Polymarket.

I have been thinking recently that after the Meme Supercycle ends, it will be difficult to revive the old DeFi form. Is the industry’s peak temporary or permanent?

This is related to whether Web3 is the next step of the Internet or the FinTech 2.0 version. If it is the former, then the way human information flow and capital flow operate will be reshaped. If it is the latter, then Stripe + Futu Niu Niu is the end of everything.

From Glider's strategy, it can be decoupled that on-chain income is about to be transformed into the era of civilian asset management, just as index funds and 401(k) have jointly created the long bull market of US stocks. With the absolute amount of funds and a huge number of retail investors, the market will have a huge demand for stable income.

This is the significance of the next DeFi. In addition to Ethereum, there is Solana. The public chain still has to undertake the innovation of Internet 3.0, and DeFi should be FinTech 2.0.

Glider adds AI assistance, but starting from the information display of DeFi Pulse, to the initial attempt of Furucombo, and then to the stable operation of Exponential, the stable on-chain income of about 5% will still attract the basic population outside of CEX.

Future: Interest-earning assets on the blockchain

As crypto products have developed to this day, only a few products have truly gained market recognition:

- Exchanges

- Stablecoins

- DeFi

- Public Chain

Any remaining product types, including NFT and Meme coin, are only phased asset issuance models, and they do not have sustainable self-sustaining capabilities.

However, RWA began to take root and grow in 2022, especially after the collapse of FTX/UST-Luna. As AC said, people don’t really care about decentralization, but care more about returns and stability.

Even if the Trump administration had not actively embraced Bitcoin and blockchain, the productization and practical application of RWA were accelerating. If traditional finance can embrace electronicization and informatization, there is no reason to give up blockchain.

In this cycle, whether it is the complex asset types and sources, or the dazzling on-chain DeFi strategies, they are seriously hindering CEX users from migrating to the chain. Regardless of the authenticity of Mass Adaption, at least a huge amount of exchange liquidity can be sucked away:

- Ethena converts fee income into on-chain income through interest alliance;

- Hyperliquid pumps the exchange’s perpetual contracts onto the chain via LP Tokens.

Both of these cases prove that it is feasible to put liquidity on the chain, and RWA proves that it is also feasible to put assets on the chain. Now is a miracle moment in the industry. ETH is considered dead, but everyone is obviously putting it on the chain. In a sense, fat protocols are not conducive to the development of fat applications. Perhaps this is also the last dark night for the public chain to return to infrastructure and application scenarios to shine, and the dawn is dim.

Image description: Profit calculation tool, Image source: @cshift_io

In addition to the above products, vfat Tools has been running as an open source APY calculation tool for more than several years. De.Fi, Beefy, and RWA.xyz all have their own focus, showing the APY of the project party. The focus of income tools has become more and more concentrated on interest-bearing assets such as YBS over time.

At present, if such tools increase the trust in AI, they will have to face the division of responsibilities and enhance human intervention, which will reduce the user experience and is difficult to handle.

It may be a better way out to separate the information flow and capital flow, create a UGC strategy community, let the project parties compete internally, and let retail investors benefit.

Conclusion

Glider has gained market attention because of a16z, but long-term problems in the track will still exist, such as authorization and risk issues. The authorization here does not refer to wallets and funds, but whether AI has the ability to satisfy humans. If AI investments suffer heavy losses, how will the responsibilities be divided?

This world is still worth exploring, and Crypto, as a public space in a collapsing world, will continue to thrive.