The market, project, currency, and other information, views, and judgments mentioned in this report are for reference only and do not constitute any investment advice.

Written by 0xWeilan

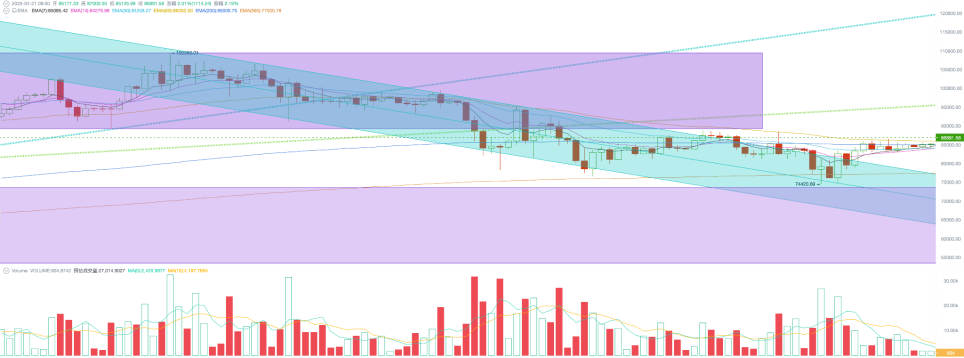

This week, BTC opened at $83,733.07 and closed at $85,177.34, rising 1.72% for the week with a volatility of 4.06%, achieving a second consecutive rebound. However, market confidence for an upward move is insufficient, with trading volume significantly shrinking. BTC price has been running outside the downward channel for the second consecutive week, currently probing the important technical indicator of the 200-day moving average.

Trump's "reciprocal tariff war" has officially entered the second stage of "negotiation", starting with talks with Japan, but the results were less than expected, putting the Trump administration in an awkward position. The main targets are strongly retaliating, secondary targets are turning hard, and these countries are very clear about buying time. In fact, when the US launches a tariff war against the world, its own pressure is unprecedented.

On Wednesday, Federal Reserve Chairman Powell stated in a speech, "At present, we are fully capable of waiting for more definitive information before considering any adjustments to our policy stance." The Federal Reserve's unchanged response to the changing tariff war has brought "stocks, bonds, and exchange" triple pressure back to Washington.

Trump urged rate cuts three times in one day and began considering removing Powell.

However, before any real breakthrough is achieved, we are more inclined to believe that politics, economy, and markets will first run rationally in the medium to long term.

Policies, Macrofinance, and Economic Data

In terms of the tariff war, the US made no substantial progress in preliminary talks with Japan, and Japan's Prime Minister's public speech before the meeting was very hawkish. After China's strong counterattack, more countries are still queuing up to negotiate with the US, but they also realize that the US's situation is not as good as claimed.

Consumer confidence continues to be low, and the business community is unclear about how to plan production. Without any assistance from Washington or the Federal Reserve, Wall Street continues to sell long positions in bewilderment and reduce trading.

In the four trading days of the week, the Nasdaq, S&P 500, and Dow Jones indexes all continued to decline, recording weekly drops of 2.62%, 1.5%, and 1.33% respectively, with trading volumes showing a clear downward trend.

The bond market situation is equally bad. The 2-year Treasury yield continued to fall to 3.7580%, and the 10-year yield fell to 4.4960%, still at high levels. The risk in the bond market is obviously on the long-end Treasuries, with last week's 11.25% surge showing that liquidity is in a critical state amid massive selling.

The US dollar index has fallen for four consecutive weeks, dropping to 99.171% this week. Funds are flowing out of the US and towards Europe. The dollar index's decline is a result of stock market drops and the bond market's inability to absorb outflowing funds. Capital outflow is something the US least wants to see.

Powell and other Federal Reserve officials' statements are generally consistent: the economy has not yet deteriorated, and tariffs will bring huge uncertainty to inflation reduction and economic development. Before the situation becomes clearer, the Federal Reserve will remain on hold.

The Federal Reserve's "hawkish" statements have cut off the market's fantasy of temporary rate cuts to save the market. By the weekend, the CME FedWatch board showed that the probability of a May rate cut had fallen to 14.4%. After the Federal Reserve intervention expectations, the market now tends to believe the Federal Reserve will make its first rate cut in June, with a 70.2% probability, and will cut rates four times this year.

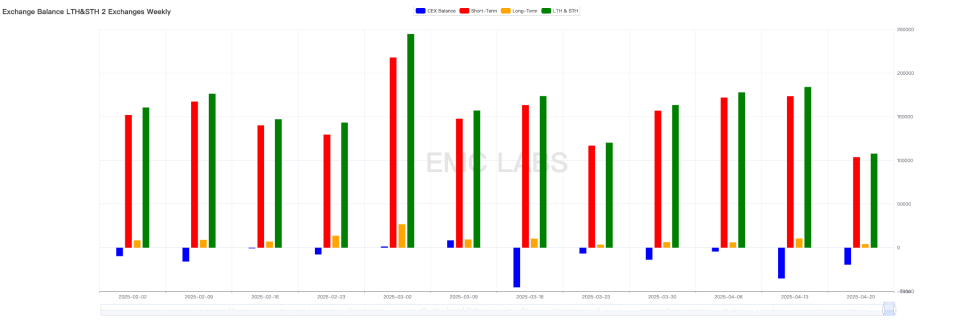

Selling Pressure and Sales

This week, selling pressure on both short and long chains continued to weaken, dropping significantly from last week. The total on-chain sales volume for the week fell to 107,810.75 coins, of which 103,713.35 were short-term and 4,097.4 were long-term. Exchange outflows continued, reaching 19,467.31 coins this week.

Statistics of short and long-term sales volumes

The long-term group is still playing a stabilizing role, "increasing holdings" by nearly 100,000 coins this week. With the price rebound, the overall unrealized loss level of the short-term group will approach 8%.

Capital Inflow and Outflow

In terms of funds, the stablecoin channel achieved the highest weekly inflow since January, exceeding $950 million. The ETF channel is seeing inflows of over $10 million, with BTC continuing to perform stronger than the Nasdaq.

Cycle Indicators

According to eMerge Engine, the EMC BTC Cycle Metrics indicator is 0.125, indicating the market is in an upward continuation period.

EMC Labs was created in April 2023 by crypto asset investors and data scientists. Focusing on blockchain industry research and Crypto secondary market investment, with industrial foresight, insights, and data mining as core competencies, committed to participating in the booming blockchain industry through research and investment, and promoting blockchain and crypto assets to bring benefits to humanity.

For more information, please visit: https://www.emc.fund