Get the best data-driven crypto insights and analysis every week:

Unpacking Circle's IPO Filing and USDC’s On-Chain Footprint

By: Tanay Ved

Key Takeaways:

Circle generated $1.7B in revenue in 2024, with 99% coming from interest income on USDC reserves. Distribution costs to partners like Coinbase & Binance totaled $1.01B, reflecting the pivotal role of exchanges in scaling USDC’s reach.

USDC’s total supply has rebounded to $60B, with 30-day average transfer volumes reaching $40B—pointing to renewed market confidence and adoption across chains. However, USDC remains sensitive to shifts in interest rates, competitive pressures, and regulatory developments.

USDC usage across major exchanges continues to grow, now representing 29% of Binance spot volume, boosted by Circle’s strategic partnerships.

Looking ahead, Circle’s next chapter may hinge on diversifying beyond passive interest income toward active revenue streams tied to tokenized assets, payment infrastructure, and capital markets integration.

Introduction

Circle, the largest U.S.-based stablecoin issuer and the company behind the $60B USDC, recently filed for an IPO, offering a window into the financial health and strategic outlook of one of crypto’s foundational companies. As the only direct way to gain exposure to crypto’s fastest-growing vertical in public markets, Circle’s filing comes at a pivotal moment. While the IPO may still face delays amid market conditions, it arrives as stablecoin legislation begins to take shape and competition intensifies across issuers and blockchains.

In this issue of Coin Metrics’ State of the Network, we unpack key takeaways from Circle’s IPO filing and pair them with USDC’s on-chain data to understand how Circle generates revenue, how factors like interest rates affect its business, and the role of platforms like Coinbase and Binance in shaping USDC’s distribution. We also explore USDC’s on-chain footprint to assess Circle’s positioning in an increasingly competitive landscape.

Circle’s Financials At a Glance

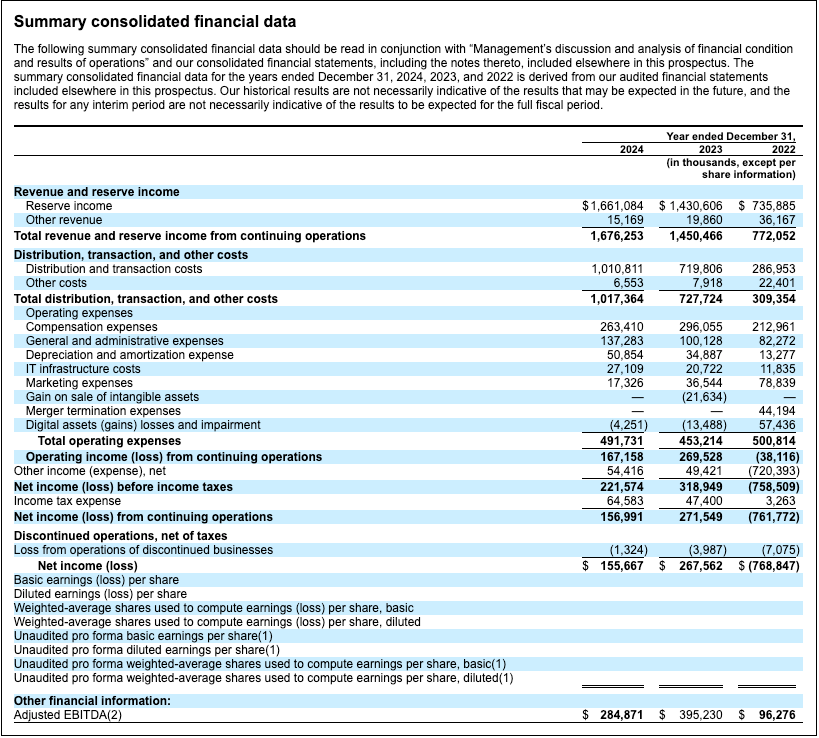

From its beginnings as a bitcoin-based payments app to becoming a leading stablecoin issuer and crypto infrastructure provider, Circle has navigated a series of challenges over its 12-year journey. After explosive revenue growth in 2021 (450%) and 2022 (808%), the pace moderated in 2023, with revenue rising 88% in a quarter where USDC was exposed to the fallout of Silicon Valley Bank. For year-end 2024, Circle reported revenues of $1.7B, up 15% year-over-year, suggesting a shift towards steadier expansion.

However, profitability compressed, with net income and adjusted EBITDA falling 42% and 28%, to $157M and $285M, respectively. Notably, Circle’s financials reveal that revenues are highly concentrated towards interest income on reserves, with distribution costs towards partners like Coinbase and Binance totaling a material ~$1.01B. However, both these factors contributed to a resurgence in USDC’s supply, which grew 80% over the year to $44B.

USDC’s On-Chain Growth

USDC is at the heart of Circle’s business, introduced in 2018 with a joint venture with Coinbase. USDC is a tokenized representation of the U.S. dollar, allowing end-users to store value in a digital form and to transact across blockchain networks, enabling near-instant settlement, at low costs. It follows a full-reserve model, backed 1:1 by highly liquid assets such as short-term U.S. Treasury bills, overnight repurchase agreements, and cash held at regulated financial institutions.

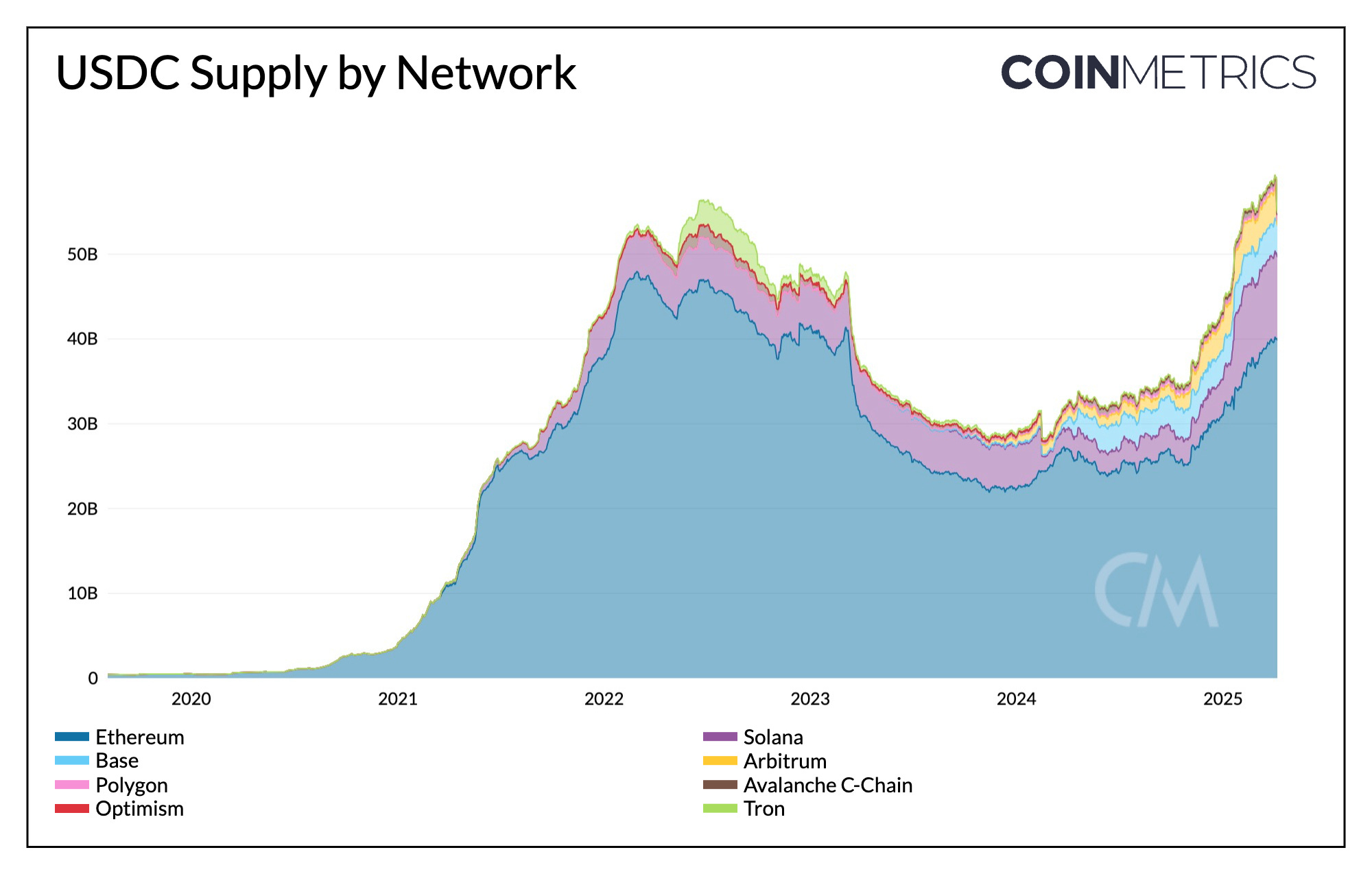

Source: Coin Metrics Network Data Pro & Coin Metrics Labs

The total supply of USDC has grown to ~60B, firmly placing it as the second largest stablecoin in existence behind Tether’s USDT. While its market share came under pressure in 2023, it has since rebounded to 26%, reflecting renewed market confidence. Of this, ~$40B (65%) is issued on Ethereum, ~$9.5B on Solana (15%), ~$3.75B on the Base Layer-2 (6%), with the remaining issued across Arbitrum, Optimism, Polygon, Avalanche and others.

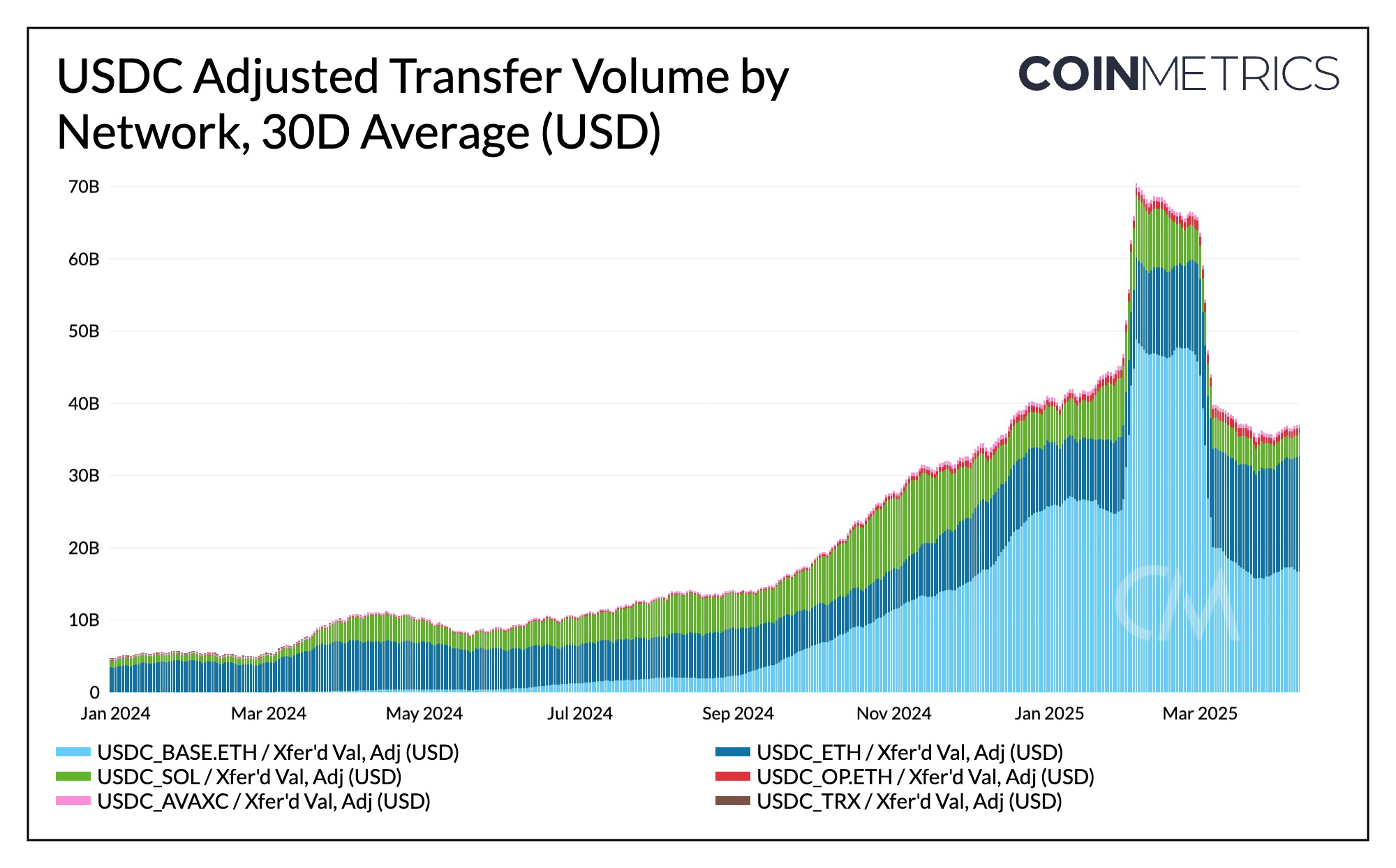

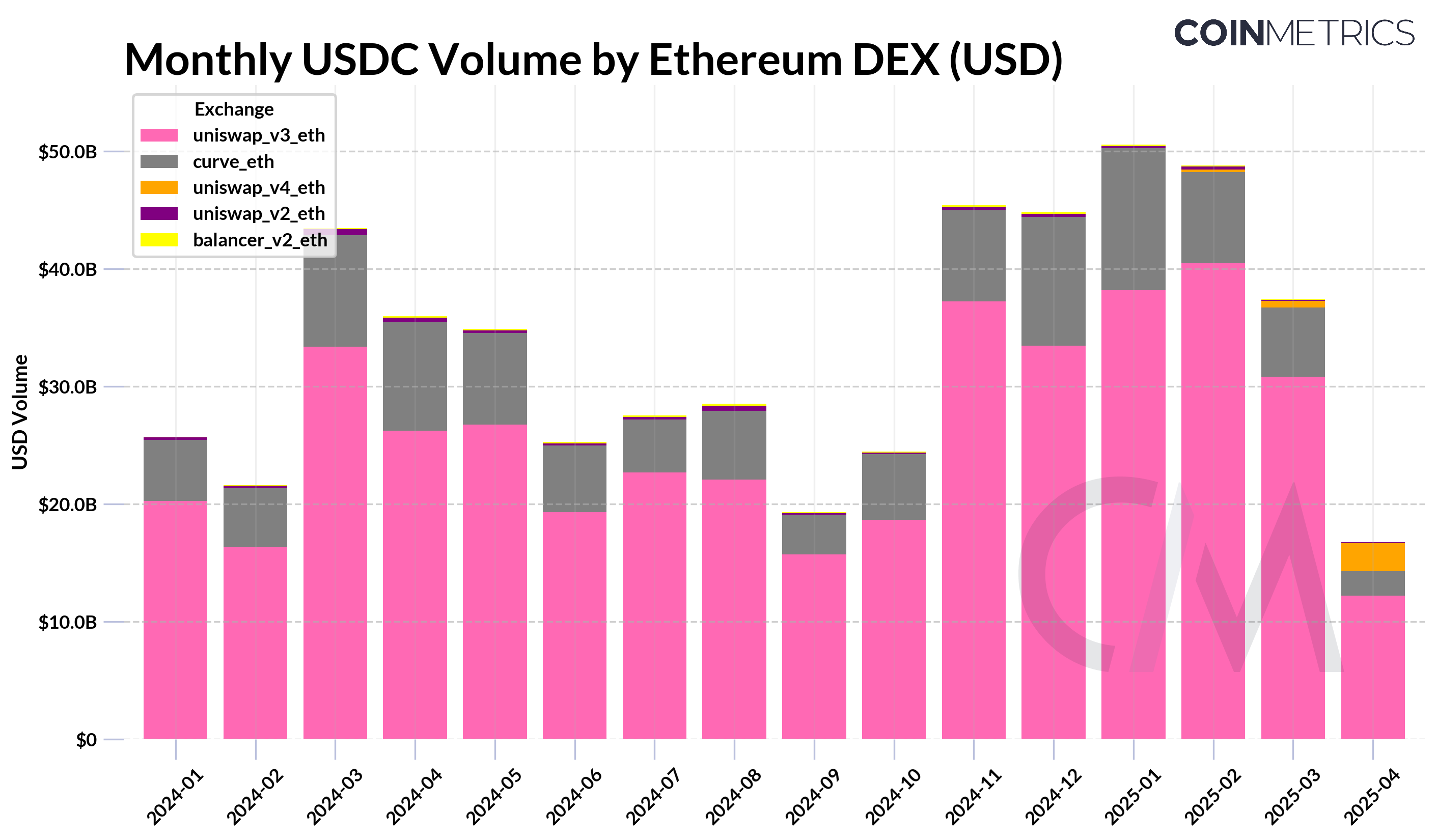

USDC’s velocity and transfer volume have also seen impressive growth, reaching ~$40B on a 30D average. In 2025, the majority of USDC transfer volume occurred on Base and Ethereum, at times accounting for up to 90% of total adjusted transfer volume.

Source: Coin Metrics Network Data Pro

These metrics point to USDC’s growing usage as stablecoins gain traction as a dollar substitute in emerging markets and as infrastructure for payments and fintech. They also exemplify Circle’s cross-chain strategy, with USDC ubiquitously available across major blockchains and supported by interoperability tools like Cross-Chain Transfer Protocol (CCTP).

Reserve Composition & Sensitivity to Interest-Rates

For every dollar of USDC issued, Circle invests the backing reserves in a portfolio of highly liquid, low-risk assets such as short-dated U.S. Treasuries and cash deposits. This structure allows Circle to generate yield on reserves while ensuring liquidity and redemption stability for USDC holders. In its filing, Circle revealed that it earned a reserve income of $1.6B in 2024. This represents 99% of its total revenues, suggesting a highly concentrated revenue mix tied to interest-rates.

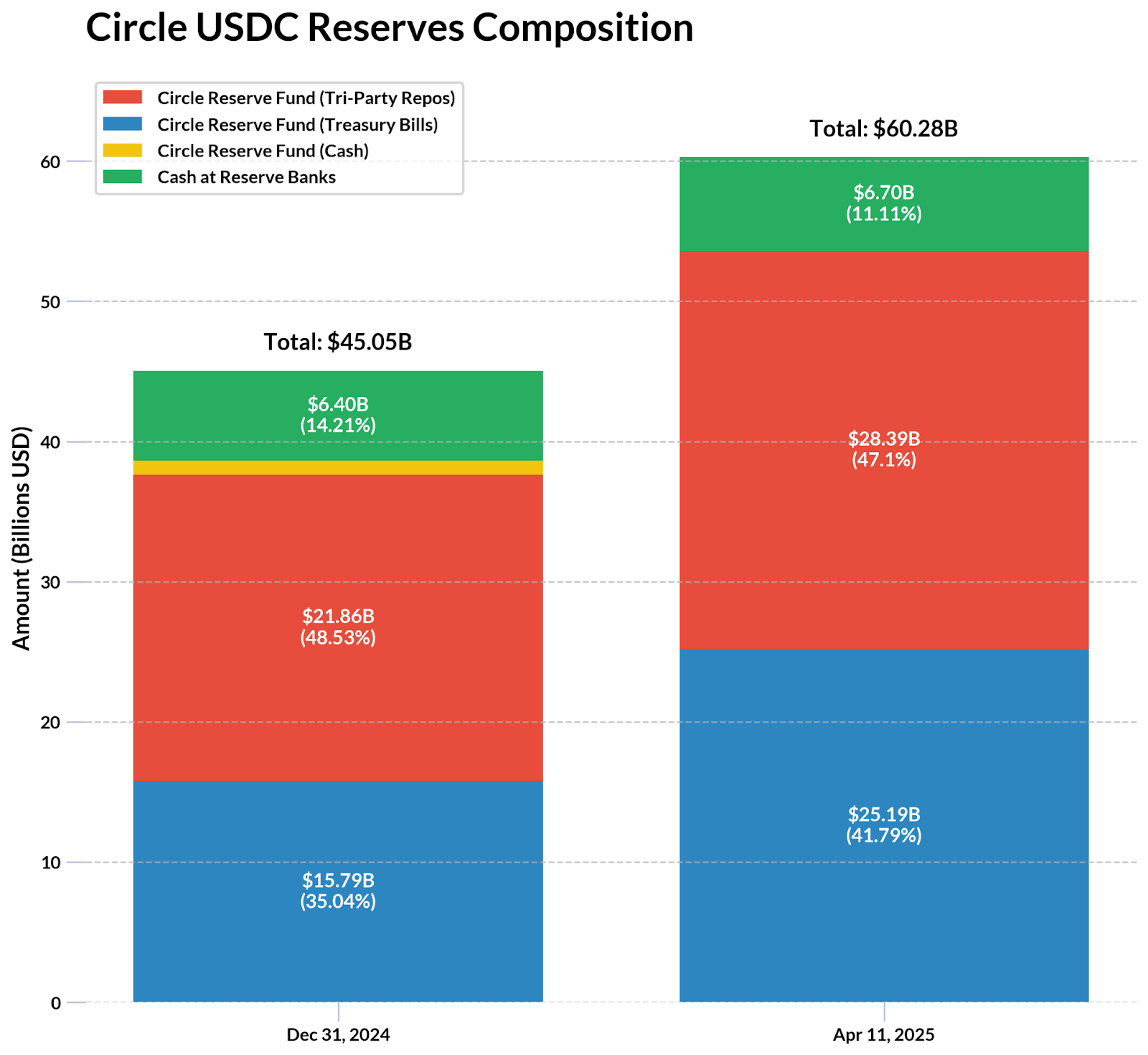

The majority of USDC reserves are held in the Circle Reserve Fund, an SEC registered government money market fund managed by BlackRock. Using Circle’s monthly attestations, financial statements and the aforementioned BlackRock Circle Reserve Fund, we find that as of April 11th, $53.5B (~88%) of USDC reserves are composed of US Treasuries and overnight repurchase agreements with a variety of financial institutions, all with a maturity of less than 2-months. Additionally, 11% of its reserves include cash deposited at regulated banks.

Source: Circle Transparency & BlackRock Circle Reserve Fund

Based on Circle’s 2024 reserve income of $1.6B on approximately $44B in reserve assets, the implied annualized yield comes out to around 3.6%. If interest rates remain around current levels, Circle’s reserve income could hold steady, assuming USDC supply remains flat or grows.

Our previous issue focusing on USDC’s supply drop in an era of rising interest-rates, revealed the highly correlated nature of Circle’s reserve income and prevailing interest-rates, showing how sensitive its revenue model is to rate changes. While the effective Fed Funds rate was between 4.58-5.33% throughout 2024, what would this imply for Circle in an environment where rates come down? In the S-1, Circle estimated that just a 1% decrease in interest rates could result in a $441M drop in stablecoin reserve income, a key risk outlined in the filing.

Given Circle retains the entirety of this yield—unlike issuers like Ethena and Maker that pass interest on to holders, its business model remains sensitive to future rate changes, competitive pressures, and regulatory evolution.

Distribution, Distribution, Distribution

The Role of Coinbase & Binance

Circle’s IPO filing also revealed the importance of partners like Coinbase and Binance in driving USDC adoption. In 2024, their distribution costs amounted to $1.01B, a material 40% increase from 2023 and 150% from 2022.

While Coinbase’s relationship with Circle is well known, the filing reveals just how financially intertwined the two have become. Coinbase earned $908M from USDC-related activities in 2024, accounting for ~13.8% of its total revenue. Under the revenue sharing agreement with Circle, Coinbase earns 100% of the interest on USDC held on its platform, and 50% on USDC held elsewhere. With the supply of USDC held on Coinbase’s platform now at 20%, up from 5% in 2022, much of the economic upside appears to accrue to Coinbase. The filing also disclosed a one-time payment of $60.25M to Binance, aiming to similarly boost distribution.

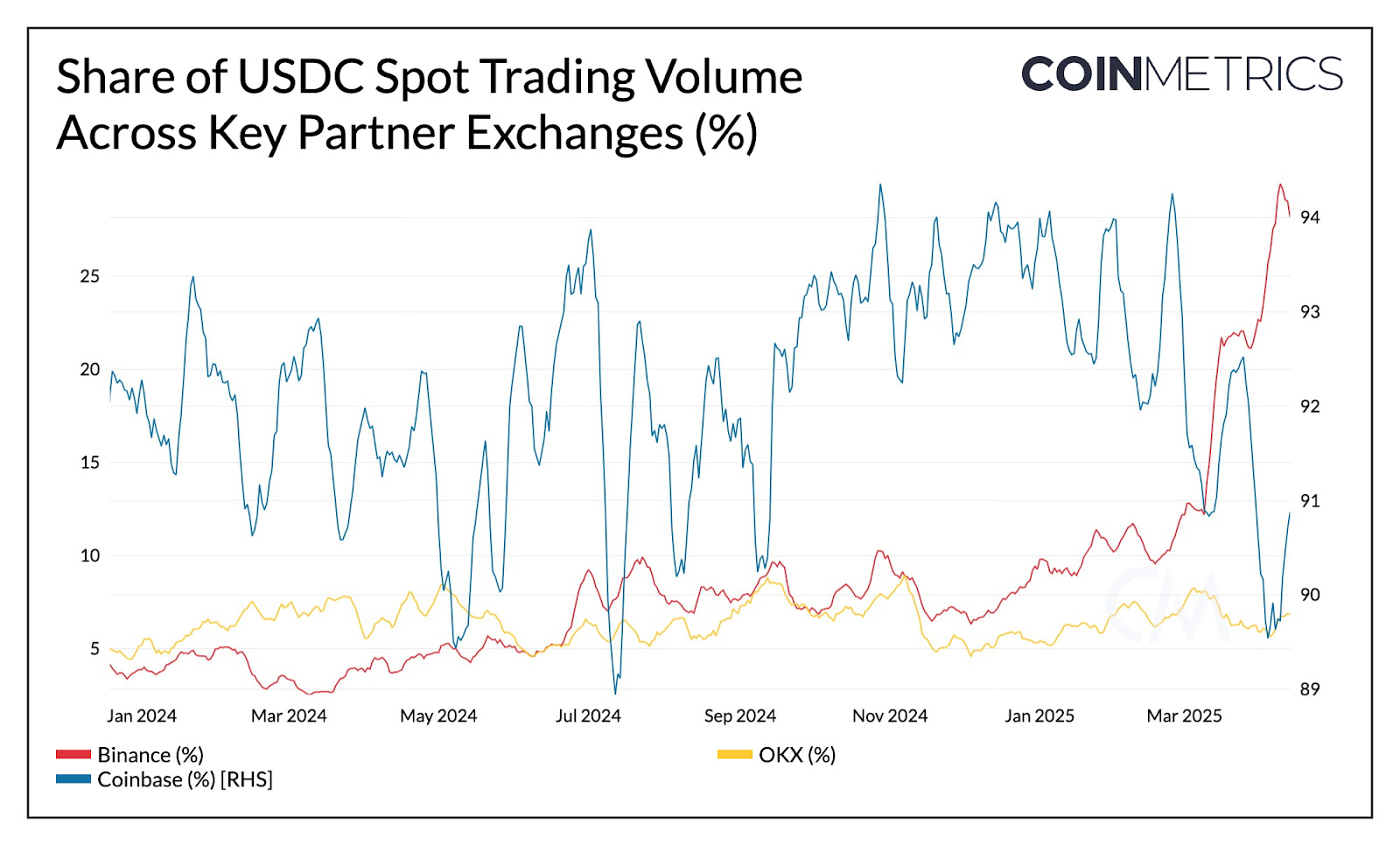

Source: Coin Metrics Market Data Feed

Looking at spot trading activity across key partner exchanges, USDC now accounts for over 29% (~$6.2B) of spot trading volume on Binance, surpassing FDUSD following its recent depegging. It ranks second only to USDT, which holds around 50% of Binance’s volume. On Coinbase, USDC powers approximately 90% of spot trading across merged USD and USDC markets.

Though costly, Circle’s distribution efforts have translated into meaningful exchange-level adoption—driving USDC liquidity and $10B in trusted spot volumes across exchanges.

Beyond Exchanges: Powering DeFi and Commerce

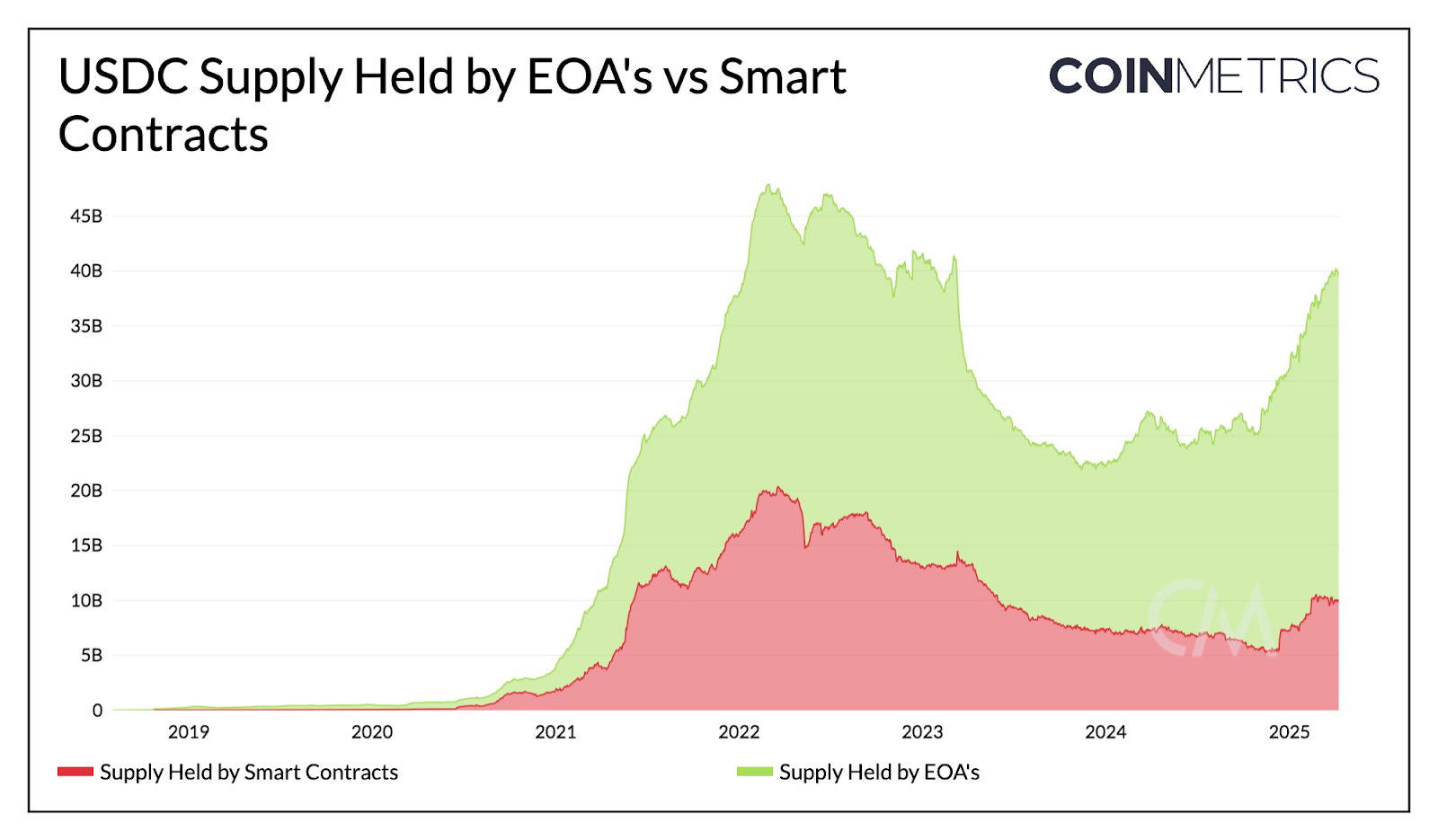

Segmenting supply held in smart contracts versus externally owned accounts (EOAs) reveals how USDC is distributed across user wallets and applications on Ethereum. Currently, ~30B is held by EOAs, growing by 66%, while ~10B sits in smart contracts, a ~42% increase from a year ago. This rise in EOA balances may reflect growing exchange custody and individual user holdings, while growth in smart contracts points to USDC’s utility as collateral in DeFi lending markets and a source of liquidity on decentralized exchanges (DEXs).

Source: Coin Metrics Network Data Pro

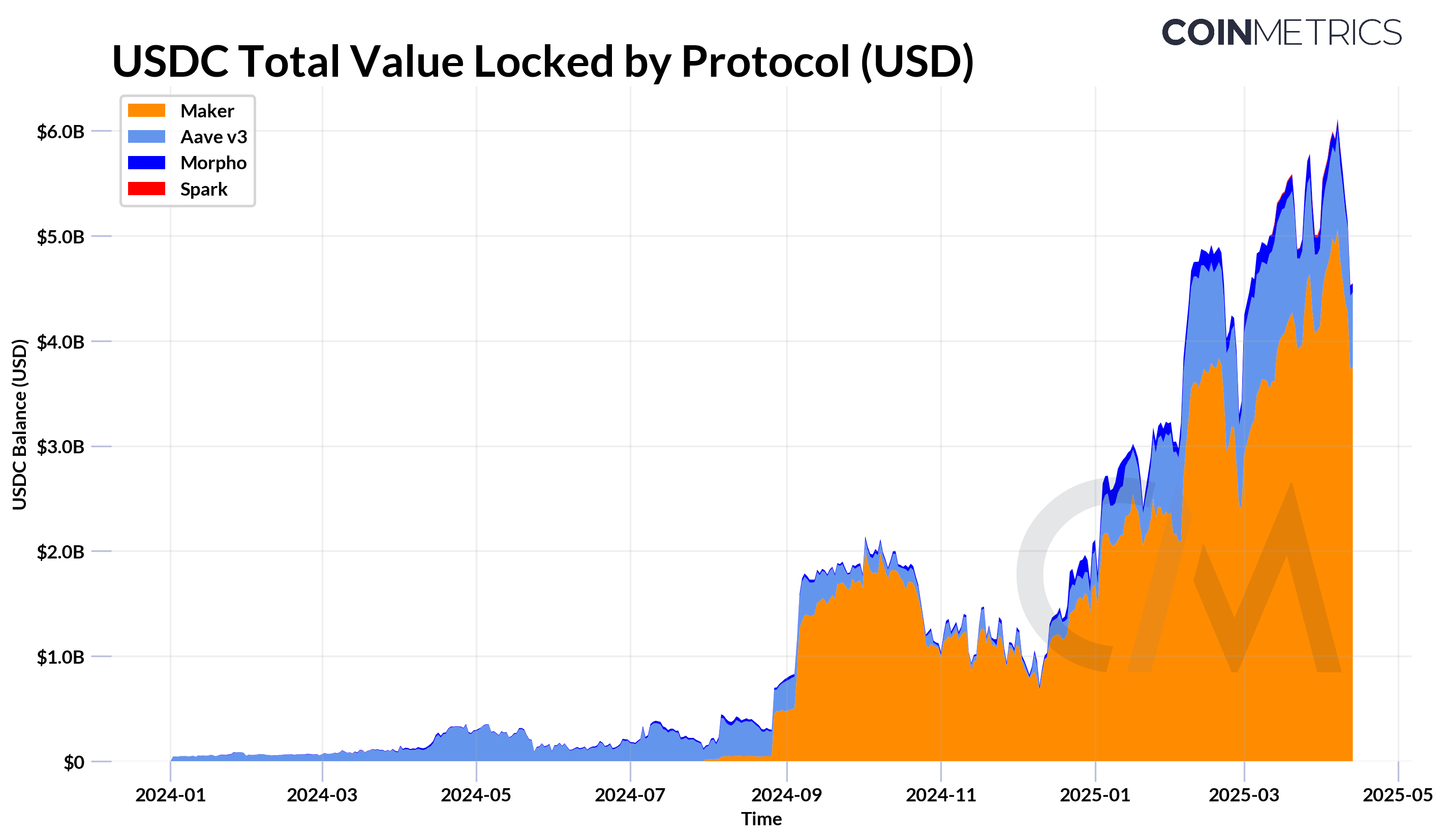

USDC continues to play a foundational role in DeFi lending markets with over 5B locked across protocols like Aave, Spark and Morpho (representing the portion of supplied USDC that hasn’t been borrowed). For collateralized debt protocols like Maker (now Sky), ~4B USDC also backs the issuance of Dai/USDS via its peg stability module.

Source: Coin Metrics ATLAS & Reference Rates

Similarly, USDC is a key source of liquidity across various DEX pools, facilitating trading into and out of stable value. It also increasingly underpins on-chain FX markets, especially as other fiat-pegged stablecoins like Circle’s MiCA compliant EURC gain traction.

Conclusion

USDC’s on-chain growth reflects renewed market confidence, but Circle’s filing also highlights key challenges, particularly high distribution costs and a heavy reliance on interest income. To sustain momentum in a lower-rate environment, Circle is aiming to diversify its revenue through active product lines like Circle Mint and by expanding into tokenized asset infrastructure via its acquisition of Hashnote, the largest issuer of tokenized money market funds.

With regulatory clarity improving, especially around the SEC’s stance that stablecoins are not securities, Circle is well-positioned. But it now faces growing competition from both offshore issuers like Tether and a new wave of U.S.-based challengers looking to capitalize on shifting policy momentum. While Circle’s valuation remains to be seen, its IPO will mark the first opportunity for public markets to directly invest in the growth of stablecoin infrastructure

Coin Metrics Updates

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Subscribe and Past Issues

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you'd like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.