Author: TechFlow

In January 2025, a survey by Coinbase and EY-Parthenon of 352 institutional decision-makers revealed that 83% of respondents plan to expand their cryptocurrency allocation this year, and 59% plan to allocate over 5% of their asset management scale to crypto assets in 2025.

A very clear signal has been transmitted: As the regulatory environment becomes increasingly clear and broader use cases emerge, institutional confidence in crypto assets is strengthening. With unprecedented institutional participation, 2025 will be a critical turning point for the outbreak of on-chain finance.

As blockchain is the critical infrastructure for on-chain finance, how can it better support the development of on-chain finance, carrying more funds, users, and complex financial strategies?

This is an arena for comparing hard capabilities, with crypto elites already rolling up their sleeves.

This includes the implementation of crypto-friendly policies by the US government, the active crypto actions of the president bringing heat and traffic, and US crypto enterprises frequently standing at the forefront of public opinion. As the most representative US crypto enterprise, Coinbase is not only a guest at the White House Digital Assets Summit, but its high-performance L2 Base is rapidly promoting the prosperity of ecological on-chain finance through the compliant stablecoin USDC path.

In the Eastern world, which also focuses on financial innovation, a transformative force surrounding financial product tokenization is also brewing:

As a leading digital asset financial services group, HashKey's financial and RWA preferred public chain HashKey Chain mainnet has officially launched, aiming to build a secure, compliant, and efficient blockchain ecosystem, and promote the deep integration of DeFi and traditional finance through financial product tokenization.

Under the major trend, a battle for discourse power in on-chain finance has been unfolded. In this competition with an undetermined landscape, who will lead the development of on-chain finance?

This report aims to explore the opportunities for on-chain finance's outbreak in 2025, how blockchain platforms should carry value, and the key factors to become important infrastructure for on-chain finance.

2025: On the Eve of Comprehensive On-Chain Finance Outbreak

The history of human financial development can be seen as a microcosm of human civilization's progress. Whether it's the Italian Renaissance nurturing the embryonic form of modern banking or Wall Street under the gold standard after World War II, every qualitative breakthrough in finance has pursued more efficient capital flow and resource allocation.

The emergence of blockchain technology, with its advantages of decentralization, permissionless nature, transparency, and higher capital gains under more efficient capital circulation, has become an important force in reforming traditional financial stagnation. On-chain finance is expected to become the core engine of capital flow and resource allocation, driving human society towards a more efficient, fair, and sustainable financial future.

As 2025 unfolds, on-chain finance is also ushering in an outbreak opportunity under the major trend of clear regulatory direction and institutional eagerness.

As early as 2024, multiple milestone developments have laid a good foundation for the development of on-chain finance.

In January 2024, we witnessed the approval of the Bitcoin ETF, a historic moment that eliminated the complexity and technical barriers of directly purchasing, storing, and managing Bitcoin, opening the door to mainstream participation and attracting substantial institutional funds:

According to Coinglass data, the total net asset value of Bitcoin spot ETFs is currently around $100 billion, of which: IBIT (BlackRock) holds about $46.3 billion; Fidelity (FBTC) holds about $16.2 billion; GBTC (Grayscale) holds about $15.8 billion.

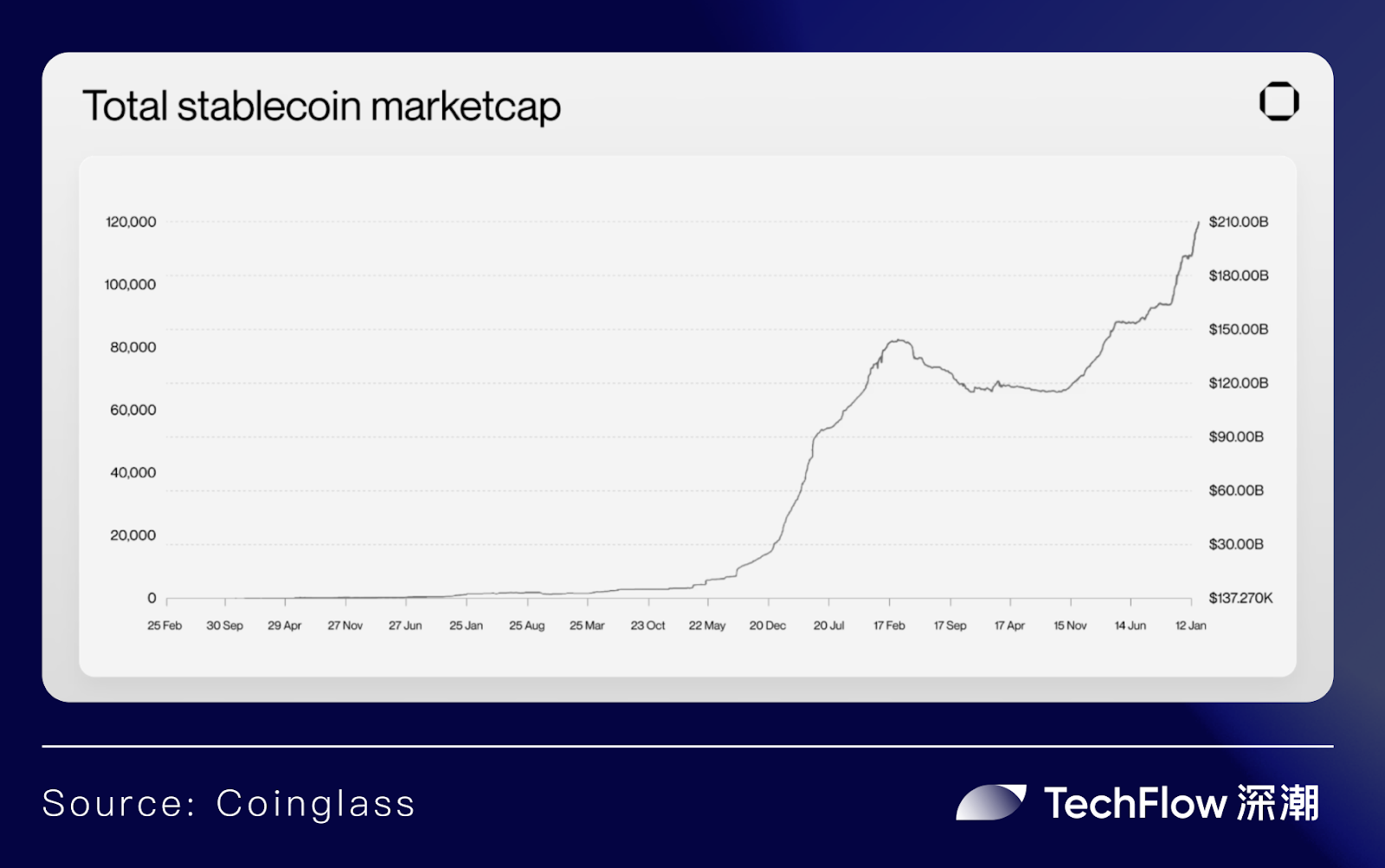

Beyond ETFs, tracks closely related to on-chain finance such as RWA and stablecoins have seen explosive growth, constructing an important bridge between on-chain and traditional finance.

In 2024, RWA experienced explosive growth, with total value exceeding $19 billion (excluding stablecoins), with an annual growth of over 85%. Tokenized credits, tokenized government bonds, and tokenized real estate became the main driving forces. Additionally, according to Coinglass data, the annual stablecoin transaction volume in 2024 exceeded $8.3 trillion, with a total market value over $210 billion. Meanwhile, traditional giants like Stripe, PayPal, and SpaceX have also been laying out in the stablecoin track.

Meanwhile, in November 2024, Trump's victory in the US election brought more positive expectations for on-chain finance outbreak.

Before taking office, whether attending the Bitcoin 2024 conference to give a speech or the emergence of the $TRUMP Meme, this always unpredictable US president has been unremittingly practicing a crypto-friendly attitude.

In just two months after taking office, over a dozen crypto policies have been signed, including the executive order "Strengthening US Leadership in Digital Financial Technology", overturning the IRS's DeFi broker rule, and announcing 5 major crypto strategic reserves including BTC, ETH, XRP, SOL, and ADA. Simultaneously, the SEC established a crypto special task force and withdrew lawsuits against multiple crypto companies.

Under the slogan "Make America Great Again", Crypto has clearly become an important tool for the US to consolidate its "global financial heart" status.

It's worth noting that the influence of this US crypto-friendly atmosphere is not limited to the United States.

As on-chain finance has bloomed in multiple global points and many countries have had to face crypto regulation, the implementation of US regulation will provide a demonstration effect, triggering follow-up from other countries/regions, thereby promoting the construction of a clearer global crypto regulatory framework. In Europe, the Markets in Crypto-Assets Regulation (MiCA), which has officially taken effect, has further brought a "rule-based" crypto development environment to European countries.

Compared to the Western world led by the US, Eastern countries/regions are more competitive in promoting clear regulation and seizing on-chain finance. Previously, regions including Hong Kong, South Korea, Japan, Singapore, Thailand, India, and Dubai have introduced policies to regulate crypto development, with Hong Kong being a leader: Recently, the Hong Kong Securities and Futures Commission (SFC) released the "A-S-P-I-Re" roadmap for the virtual asset market, with 12 specific measures aimed at further focusing on institutional investor participation.

If the efficient capital circulation of on-chain finance is the original driving force attracting traditional finance to go on-chain, then a clearer, more open, and inclusive regulatory environment further eliminates concerns and promotes more proactive on-chain strategies by institutions.

In fact, this trend has already emerged: In the Western world, institutions like JPMorgan Chase, Goldman Sachs, BlackRock, and MicroStrategy, and in the Eastern world, renowned institutions such as Sony, Samsung, and HSBC have all taken concrete actions.

Another very obvious phenomenon is reflected in the ETF application fever, with multiple institutions having submitted ETF applications to the SEC, including Ripple (XRP), Solana (SOL), Litecoin (LTC), Cardano (ADA), Hedera (HBAR), Polkadot (DOT), and DogeCoin (DOGE).

As institutions bring in more funds and users, 2025 will become a critical turning point for on-chain finance outbreak. Facing the trend, how to become a main competitor on the on-chain finance table? The focus is on internal and external cultivation:

External embrace of compliance: Compliance will become the core measurement standard for institutional participation in on-chain finance. Actively embracing regulation will further eliminate institutional concerns about regulation and bring a healthy and stable environment for on-chain finance development.

Internal self-cultivation: Continuously optimize transaction speed, transaction costs, user experience, and security guarantees, continuously improving blockchain's service capabilities as infrastructure to carry large-scale funds and users.

So how are the main competitors performing on these two paths?

East and West Compliance Titans: White House Guest and Hong Kong Regulatory Pioneer

Coinbase in the West, HashKey in the East.

This widely circulated analogy in the community stems not only from their extensive crypto empires but also from their firm commitment and similar paths to compliance.

As the first listed cryptocurrency company in the United States, Coinbase has successively obtained fund transfer licenses from various states and compliance operation permits in countries including the UK, EU, Singapore, and Japan over the past few years.

Although Coinbase's compliance journey was challenging under SEC interference, it gradually "saw the light" after the crypto-friendly government centered on Trump took office and the SEC withdrew its lawsuit against Coinbase:

As the first guest at the White House Digital Assets Summit, Coinbase CEO Brian Armstrong sat in the third position from Trump's left and publicly stated in media interviews that he was willing to serve as a government crypto asset custodian under national reserve background. Coinbase has collaborated with multiple government departments on crypto asset custody and trading. Additionally, Coinbase revealed its active efforts to promote rapid congressional legislation on stablecoin and market structure bills.

As the Eastern representative, HashKey, rooted in Hong Kong, is undoubtedly a compliance pioneer in many community members' eyes:

As one of the former Asian Four Little Dragons, Hong Kong not only has an advantageous geographical location that allows it to play a crucial role as a financial hub in the Asia-Pacific region, connecting mainland China, Japan, Korea, and Southeast Asia, but also possesses a sophisticated financial infrastructure, an active financial innovation atmosphere, and a long-accumulated pool of professional talents in finance, technology, and law that are unmatched by other cities.

Previously, Hong Kong's financial soil successfully nurtured numerous top crypto industry institutions like FTX, Amber Group, Crypto.com, and BitMEX. According to the "Hong Kong Financial Technology Ecosystem Report" released by the Hong Kong Investment Promotion Agency, Hong Kong currently has over 1,100 fintech companies, including 175 blockchain application or software enterprises and 111 digital asset and cryptocurrency companies.

In 2023, Hong Kong further clarified its direction of "focusing on blockchain as a key development area" and officially launched the Virtual Asset Service Provider (VASP) license application system. With the gradual opening of innovative products like ETFs and virtual asset funds to ordinary investors, Hong Kong is attracting global attention as a "chain-based financial innovation center".

As one of the first crypto enterprises to apply for Hong Kong licenses and a key force supporting Hong Kong's blockchain economic development and actively embracing compliance, HashKey has officially obtained the Type 1, Type 4, and Type 9 licenses issued by the Hong Kong Securities and Futures Commission (SFC), expanding its business scope and capabilities under SFC regulation.

[The translation continues in the same manner, maintaining the original structure and translating all text while preserving any HTML tags and specific terminology as specified.]The origin of Base and compliant stablecoins dates back to 2018, when Circle and Coinbase jointly launched the first stablecoin supported by a centralized exchange, USDC. This stablecoin's primary advantage is compliance, with Circle possessing a full US license and payment licenses in the UK and EU, obtaining the qualification to issue USDC and EURC under the MiCA Act last July, and recently submitting an S-1 filing to the US Securities and Exchange Commission, intending to conduct an initial public offering.

Compliant stablecoins not only provide a stable trading medium and a bridge for rapid exchange and efficient liquidity between crypto assets, but also offer a compliant pathway for traditional finance to go on-chain. Through USDC, Base not only brings users a higher-quality on-chain financial system but also promotes penetration and innovation in payment, RWA, and other financial scenarios within its ecosystem: currently, Base's ecosystem has emerged with multiple native stablecoin payment applications such as Peanut and LlamaPay.

HashKey continues to leverage its advantages in institutional collaboration, with HashKey Chain focusing on tokenizing financial products and building the preferred blockchain for finance and RWA:

Institutions manage large-scale funds and users. Institutional participation will guide significant on-chain fund deposits and new user influx, which is a crucial sign of on-chain finance's maturity and scalability. HashKey Chain aims to clear obstacles for institutional participation by providing efficient and compliant financial product tokenization solutions.

The tokenized USD money market fund "CPIC Estable MMF", initiated and managed by China Pacific Insurance Asset Management Company (Hong Kong), was successfully deployed on HashKey Chain, serving as a demonstration case of HashKey Chain's approach to building a financial and RWA-preferred platform through financial product tokenization.

For institutions, HashKey Chain significantly reduces the technical barriers and operational costs of bringing financial products on-chain through compliance-friendly, secure, high-performance, and low-cost infrastructure, empowering asset liquidity and application scenarios with a comprehensive on-chain DeFi ecosystem. This enables CPIC Estable MMF to serve as an effective digital asset allocation tool, helping institutions achieve transparent, efficient, and granular management of fund shares on the blockchain.

For DeFi users, by providing efficient financial product tokenization tools for institutions, on-chain financial users will welcome more high-quality assets with real yield and obtain more diverse sources of income.

For on-chain finance, as more institutional-level assets choose digital transformation on HashKey Chain, on-chain finance is accelerating its integration with traditional finance and playing an increasingly important role in the global financial system.

According to HashKey data, CPIC Estable MMF's first-day subscription scale already exceeded $100 million, further reflecting the massive market demand for institutional financial product tokenization. As HashKey Chain continues to advance deep collaboration with multiple institutions, it will further become an ideal platform for tokenizing financial products such as bonds, funds, and stablecoins, helping on-chain finance and RWA achieve leapfrog development.

With Coinbase in San Francisco and HashKey in Hong Kong as two centers, focusing on Base's compliant stablecinscoins and HashKey Chain's institutional financial product tokenization, facing the golden age of era of on-chain finance, we can perhaps look forward to the fact that both Base and HashKey Chain will adopt a win-win attitude to promote the construction of on of-between East and Westand, while accelerating the earlier arrival of global on-chain financial transformation.