Author: Daii

Last week, US President Trump launched a tariff storm, and the global economy was instantly caught in a violent shock. US stocks plummeted, and the market value evaporated by 5 trillion US dollars in two days. Bitcoin was not immune. But do you know? The real lethality of this tariff war is actually hidden in the thing we are most familiar with but most often overlooked - currency.

The reason why the United States dares to raise the tariff stick so arrogantly is not just because of the trade deficit, but the more critical trump card is the hegemony of the US dollar. The US dollar not only controls global trade, but also becomes a hidden economic weapon. Whoever controls the US dollar controls the economic lifeline of the world.

What is even more worrying is that this war will spread from the commodity field to the currency field, and a global currency devaluation competition is taking place.

So, how should ordinary people face such a war without gunpowder? Let us uncover the truth of this war layer by layer and see who is the ultimate winner?

Contrary to many people’s expectations, the ultimate winner may not be the country, but the decentralized stablecoin.

First, let’s look at various countries’ reactions to the US tax increases.

1. Tough and gentle

In response to US President Trump's decision on April 2, 2025 to impose an additional 34% tariff on Chinese goods, China quickly responded strongly.

On April 4, China's State Council Tariff Commission announced that starting from April 10, a 34% tariff will be imposed on all imported goods originating from the United States on top of the current applicable tariff rate. In addition, China has also implemented export controls on key resources such as medium and heavy rare earths, and filed a lawsuit at the World Trade Organization (WTO), accusing the United States of violating international trade rules with its tariff measures. This series of measures shows China's firm stance in safeguarding its own rights and interests in trade disputes.

Later, the United States announced that if China did not withdraw its retaliatory 34% tariff, it would impose a further 50% tariff.

Compared with China's tough stance, Vietnam has chosen a moderate policy.

As one of the worst-affected countries, Vietnam faces tariffs of up to 46% from the United States. The Vietnamese government has moved quickly to seek a diplomatic solution to the dispute. General Secretary of the Communist Party of Vietnam To Lin held a telephone conversation with President Trump and expressed his willingness to reduce Vietnam's tariffs on American goods to zero in exchange for the removal of high tariffs on Vietnam by the United States.

In addition, the Vietnamese government asked the United States to postpone the implementation date of tariffs by 45 days to allow time for negotiations. Vietnamese Deputy Prime Minister Hu Defu was sent to the United States in the hope of resolving the tariff issue through diplomatic channels.

Prime Minister Pham Minh Chinh stressed at an emergency cabinet meeting that despite the challenges, Vietnam will stick to its GDP growth target of 8% or higher. He pointed out that this challenge is also an opportunity to promote economic restructuring, aiming to achieve rapid and sustainable development, expand markets and optimize supply chains.

Reactions from other countries:

EU: European Commission President Ursula von der Leyen said the EU is willing to negotiate with the United States to seek mutual zero tariffs on industrial products, but at the same time warned that if the negotiations fail, the EU will take countermeasures.

Japan: Japanese Trade Minister Yoji Muto expressed regret over the U.S. tariff decision and said he would consider taking appropriate measures in response.

Australia: Australian Prime Minister Anthony Albanese criticized the US tariff measures, calling them "completely unfounded", but said Australia would not impose retaliatory tariffs.

Now it seems that, except for China's strong reaction, other countries are relatively mild. In sharp contrast to China is Vietnam, especially the Vietnamese Prime Minister Pham Minh Chinh said that this challenge is also an opportunity to promote economic structural adjustment. It has a taste of turning pressure into motivation, which is especially worth savoring.

In fact, it is not that Vietnam is timid, but because the consequences of this tariff war are really unbearable for it. If a war really breaks out, not only the United States but also China will find it difficult to bear it. Vietnam's moderation is really a last resort.

2. Tariff war: two swords dividing the global economy

If a tariff war really breaks out, it will be like two sharp knives that cut the veins of the global economy and ruthlessly tear apart the texture of the global economy.

2.1 Dao Yi: The pain of supply chain reconstruction

The most direct and obvious effect of the US's wielding of tariffs is the severe impact on the global supply chain. High tariffs are like an artificial trade barrier that instantly raises the cost of imported goods. This not only directly increases the expenses of American consumers, but also puts Chinese manufacturing, which relies on the US market, under tremendous export pressure.

In order to avoid high tariffs, the global industrial chain will be forced to start another massive reconstruction. The data of the past three years (2022-2024) is a preview:

The rise of Southeast Asia: As the World Bank report shows, the ASEAN region has become one of the biggest beneficiaries of this supply chain shift.

In 2024, foreign direct investment (FDI) in the manufacturing sector in the ASEAN region will surge by nearly 30% compared to 2020. This is not groundless. We can see that industries such as electronics, textiles, and light industry are accelerating their transfer to Southeast Asian countries such as Vietnam and Thailand. For example, South Korea's Samsung Electronics closed its last mobile phone factory in China and increased its investment in Vietnam and India. Japanese clothing brand Uniqlo has also begun to increase its production proportion in Southeast Asia to reduce its dependence on a single market. The migration of these companies has directly driven local employment and economic growth.

The rise of Vietnam and Mexico: Vietnam and Mexico have gradually become important manufacturing alternatives for American companies outside of China due to their geographical location and relatively low labor costs. Taking Vietnam as an example, its exports to the United States have continued to rise in the past three years, especially in the fields of textiles, footwear, and electronic components. Mexico has attracted a large number of investments in industries such as auto parts and home appliances due to its geographical proximity to the United States and the convenience of the North American Free Trade Agreement (although it was replaced by the US-Mexico-Canada Agreement in 2020, its influence remains). In the short term, these countries have indeed enjoyed the dividends brought by industrial transfer.

Now, with US President Trump announcing a 10% tariff on all imported goods and an additional 50% tariff on goods from China, the previously seemingly "win-win" industrial chain transfer pattern will once again face severe shocks. This is like the earth's crust shaking violently again after an earthquake, and the "plates" that have already begun to migrate will face new uncertainties.

For companies that have already moved some of their production capacity to Vietnam, Mexico, etc., the new tariff policy is undoubtedly a blow. Although they may have avoided the additional tariffs of more than 50% on China, the 10% tariff imposed by the United States on all imports will still increase their operating costs and weaken their price competitiveness.

What's worse, if these companies' production in Vietnam or Mexico still relies on parts and raw materials imported from China, the cost of these intermediate products will also rise sharply due to China's tariffs of more than 50%, ultimately causing their overall production costs to rise instead of fall.

This new tariff shock will also accelerate the further decentralization and regionalization of the global supply chain. Companies may be more inclined to establish production bases in regions closer to the final consumer market, or to deploy production capacity in multiple countries to reduce dependence on a single country or region. This trend may make the global trade pattern more complicated, further reduce the efficiency of the supply chain, and increase the management costs of enterprises.

In short, the new tariff policy is like a sharper knife, which will not only intensify the pain of the original supply chain reconstruction, but also have a wider and more far-reaching impact on all aspects of the global economy. Companies and countries that have begun to adapt to the new pattern will be forced to face a new round of adjustments and challenges.

2.2 The second point: the threat of the “stagflation trap”

As the famous investor Ray Dalio warned, tariffs are like injecting a poison of "stagflation" into the global economy. Exporting countries face deflationary pressure due to reduced demand, while importing countries feel the pain of inflation due to rising commodity prices. This situation of stagnant growth and inflation is the "stagflation trap" that economists are most worried about.

Let's take a look at the actual data performance of the United States and major exporting countries:

"Rising" inflation in the United States: Since the further escalation of the US tariff policy at the end of 2024, we can clearly see the continued rise in the US Consumer Price Index (CPI). According to the US Bureau of Labor Statistics, as of February 2025, the US CPI index has risen by 0.684% from the end of 2024. Among them, commodities that are more affected by tariffs, such as electronic products, clothing, furniture, etc., have seen more significant price increases. This has directly led to the continuous rise in the cost of living of the American people and the decline in their actual purchasing power. The annualized inflation rate in the United States is about 2.8%~3.0%, far higher than the control target of 2%.

The "chill" of exporting countries: For export-oriented economies such as China, South Korea, and Germany, the tariffs imposed by the United States are undoubtedly a heavy blow. In the short term, these countries' export demand for the United States has shrunk significantly, resulting in a decrease in corporate orders and a slowdown in production. In order to digest excess production capacity, some companies have to sell at a lower price, facing the dilemma of declining profits or even losses. This will further affect the investment willingness of companies and may even trigger a wave of layoffs and increase the risk of unemployment. Taking China as an example, according to the analysis of the Economist Intelligence Unit, China's GDP growth rate is expected to decrease by 0.6% to 2.5% in 2025-2027, depending on the intensity of tariffs.

The scary thing about the "stagflation trap" within a country is that traditional monetary policy often cannot solve the problems of stagnant growth and inflation at the same time. If the central bank adopts an easy monetary policy to stimulate economic growth, it may further aggravate inflation; and if it adopts a tight monetary policy to curb inflation, it may lead to a further economic downturn. This makes governments face a dilemma when formulating economic policies.

You need to note that the "stagflation" caused by this tariff war is not stagflation within a country, but global. It is inflation for importing countries and stagnation for exporting countries. Solving this global stagflation problem is much more complicated than the predicament within a country.

For importing countries, such as the United States, the main challenge is rising prices. To curb inflation, the traditional approach is to raise interest rates. However, with economic growth already slowing due to tariffs and supply chain disruptions, raising interest rates could further hit economic activity and even trigger a recession.

For exporting countries, such as China, the main problem they face is the slowdown in economic growth caused by insufficient demand. In order to stimulate the economy, loose monetary policies such as interest rate cuts and increased credit supply are usually adopted. However, in the context of global trade tensions, this approach may lead to capital outflows and currency depreciation, further exacerbating trade frictions with the United States.

Therefore, this global stagflation dilemma makes it difficult for any single country's policies to be effective, and may even be counterproductive. Importing countries and exporting countries face completely different policy dilemmas, and it is difficult for any one party to find a balance through unilateral actions, let alone form a global joint force to solve the problem.

This is also why economists such as Ray Dalio are worried about this situation, because it indicates that the global economy may enter a difficult period of long-term low growth and high inflation.

2.3 Summary

To sum up, this tariff war, like two invisible blades, is silently tearing the nerves of the global economy.

The first blow is the pain of supply chain reconstruction, which has forced global companies to pay huge costs to adjust their production layout, resulting in reduced efficiency and ultimately higher prices for consumers.

The second knife, the threat of the "stagflation trap", has put governments in a dilemma. They have to deal with inflationary pressure while avoiding a further slowdown in economic growth. Traditional monetary policy tools are stretched to the limit.

Faced with the risk of supply chain disruption and stagflation, some countries may turn their attention to their only shield - currency. A currency devaluation race at the expense of neighbors may be quietly kicking off.

3. Currency Shield: Poison That Quenches Thirst

Deep in the fog of history, the economic time machine repeats similar stories again and again. Humans are always accustomed to learning lessons from history, but they often ignore these lessons. Currency war, this seemingly professional and complex term, has actually been repeatedly staged in human economic history.

Today, this "monetary shield" is once again being used by various countries, and it seems to be able to temporarily alleviate the economic pain, but history tells us that it is actually a veritable poison that only quenches thirst.

3.1 Currency Devaluation during the Great Depression

During the Great Depression of the 1930s, economies around the world fell into a slump and deflation. In order to stimulate exports and save the economy, countries competed to devalue their currencies. In 1931, Britain was the first to leave the gold standard and allow the pound to float freely. The pound quickly depreciated by about 30% against the US dollar, and as a result, Britain's export price advantage increased significantly, and exports rebounded briefly.

The UK's move set off a storm around the world. France, Germany, and Italy followed suit, using currency devaluation as a tool for economic recovery. This competitive devaluation triggered a chain reaction, with countries building high tariff barriers against each other in an attempt to protect their domestic markets. But the reality was extremely cruel, and global trade volume fell sharply. According to data from the International Monetary Fund (IMF), from 1929 to 1933, the scale of global trade fell by more than 60%, exacerbating the economic recession and causing unemployment rates to soar in various countries, with the unemployment rate in the United States even exceeding 25%.

3.2 Currency Devaluation during the Asian Financial Crisis

If the lessons of the Great Depression are still far away, then the most recent currency war has to mention the Asian financial crisis in 1997. At that time, many Asian economies had accumulated huge foreign debts after experiencing rapid growth, and the influx of hot money caused asset prices to soar. When foreign capital withdrew upon hearing the news, Southeast Asian currencies such as the Thai baht, Indonesian rupiah, and Malaysian ringgit collapsed one after another.

Thailand was the first to announce in July 1997 that it would abandon its exchange rate peg policy to the US dollar. The Thai baht plummeted by more than 50% in a short period of time. In order to maintain export competitiveness, other countries quickly followed suit, but this was followed by a more violent capital flight. South Korea's foreign exchange reserves were exhausted in just a few months and it was forced to apply for emergency assistance of up to US$58 billion from the International Monetary Fund.

The depreciated currency brought temporary export competitiveness, but also caused severe inflation and economic recession. Indonesia even experienced large-scale social unrest, and President Suharto was forced to step down. Data showed that during the crisis, Indonesia's inflation rate once exceeded 70%, the unemployment rate soared, and society fell into chaos.

The echo of history warns us: currency devaluation may seem like a simple economic tool, but in reality it hides huge risks that are difficult to predict. Once countries compete to devalue their currencies, not only will the export advantage be short-lived and unsustainable, but it will also bring about great turmoil in the global capital market, causing long-term economic recession and imbalance.

However, the short-term effectiveness of the monetary shield will lure more countries into an abyss of no return.

3.3 Currency depreciation: a lifeline that must be grasped

In today's tariff war, countries have once again been pushed to the brink of currency devaluation. Faced with the threat of a sharp decline in exports and an impending wave of unemployment, currency devaluation has become a "lifeline" that governments have no choice but to turn to. But history clearly tells us that this straw is not salvation, but a catalyst for economic deterioration.

Looking back at recent data, after the new tariff policy was introduced in April 2025, the RMB/USD exchange rate quickly fell from 7.05 to 7.20, hitting a new low in nearly two years; the Vietnamese dong also quickly followed suit, depreciating by more than 6% against the US dollar; the Korean won, the New Taiwan dollar, the Malaysian ringgit and even the euro, without exception, have chosen loose monetary policies. The logic of this competitive devaluation is simple and cruel: after the devaluation of the domestic currency, export goods appear cheaper in the international market, thereby temporarily boosting exports.

However, behind this short-term prosperity, there are huge hidden dangers. Once the currency continues to depreciate, the actual value of domestic assets will inevitably shrink, and foreign capital will quickly withdraw out of risk aversion. Take Turkey in 2024 as an example. The lira depreciated by more than 40% in one year, which immediately triggered a large-scale withdrawal of foreign capital, rapid consumption of foreign exchange reserves, and inflation rate soaring to more than 85%. The cost of social living rose sharply, and the economy was on the verge of collapse.

What is even more worrying is that when currency depreciation becomes a defensive measure that countries around the world have to take, the global capital market will fall into panic flow, and a large amount of funds will flow into US dollar assets. At this time, the United States itself will fall into the "dollar trap". The rapid appreciation of the dollar will crush the domestic manufacturing industry in the United States, and the liquidity of the global economy will dry up. A "lose-lose" situation will inevitably come.

In fact, if it is not the United States, any other country, if it does not want to be the leader, it is a reasonable request to propose reciprocal tariffs. However, the United States is different. Because of the existence of the dollar hegemony, the so-called trade deficit is not as unfair as the United States says, or the trade deficit is only part of the truth.

4. Trade deficit under the hegemony of the US dollar

To understand the hegemony of the US dollar, we must first trace it back to after World War II. The Bretton Woods system established the status of the US dollar pegged to gold, making the US dollar the world's main reserve currency and settlement currency. However, this system collapsed in 1971 after the Nixon administration announced the decoupling of the US dollar from gold.

So how did the US dollar maintain its dominant position after the collapse of the gold standard?

4.1 The formation of US dollar hegemony

One of the key factors is the establishment of the "petrodollar" system. In the 1970s, the United States and Saudi Arabia reached a landmark agreement. Saudi Arabia agreed to use the US dollar as the only settlement currency for its oil exports, and the United States promised to provide security for Saudi Arabia. Since oil is the lifeblood of the global economy, this agreement means that most of the world's oil transactions must be conducted in US dollars.

Imagine that countries around the world need to buy oil to keep their economies running. And the only way to buy oil is to own dollars. It's like there is only one universal "entry ticket" in a large international market - the dollar. In order to get this "entry ticket", countries must earn dollars by exporting goods and services to the United States, or hold dollar assets.

In addition to the petrodollar system, the U.S. dollar has further consolidated its hegemonic position as the world's main reserve currency. Central banks of various countries need to hold a certain amount of foreign exchange reserves in order to deal with the balance of international payments, intervene in the foreign exchange market, and store national wealth. Due to the large size of the U.S. economy, developed financial markets and relative stability, the U.S. dollar has naturally become the preferred reserve currency for central banks of various countries.

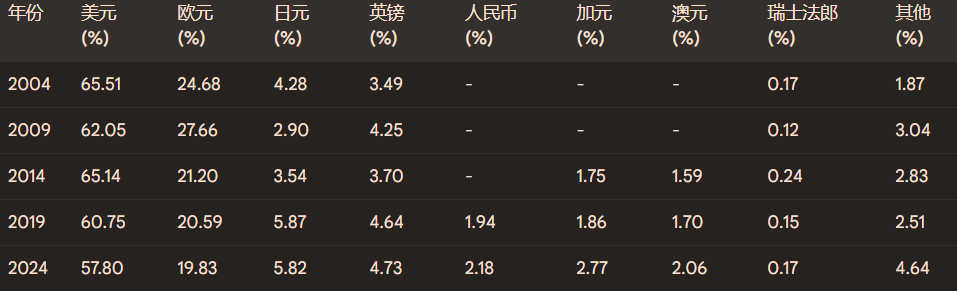

According to data from the International Monetary Fund (IMF), by the end of 2024, the U.S. dollar will still account for about 57.8% of global foreign exchange reserves, far exceeding other currencies such as the euro, yen and pound, as shown in the figure above. This means that more than half of the world's foreign exchange reserves are in the form of U.S. dollars. If you are interested in how the U.S. dollar hegemony was formed, I recommend reading "Escape from the "Currency Trap" and Return to the "Time Standard"", which is not just about the U.S. dollar, but almost all currencies. The history of the history of all currencies is sorted out.

4.2 The “privilege” brought by the US dollar hegemony: low-cost financing and seigniorage

It is precisely because of the special status of the US dollar that the United States enjoys "privileges" that other countries cannot match. The two most notable aspects are low-cost financing and seigniorage.

Low-cost financing: Due to the huge global demand for US dollar assets (such as US Treasury bonds), the United States can borrow funds at relatively low interest rates. This is like a company with excellent credit, which is more likely to obtain low-interest loans from banks. If other countries have trade deficits, they often face pressure from depreciation of their own currencies and rising financing costs. However, due to the hegemony of the US dollar, the United States is relatively less under such pressure.

For example, even as the US government debt continues to rise, global investors are still willing to buy US Treasury bonds, which has to some extent lowered the borrowing costs of the United States. Imagine if other countries had such a huge debt, their Treasury bond yields would likely soar.

Seigniorage: Seigniorage refers to the difference between the revenue from issuing currency and the cost of issuing it. For the United States, since the US dollar is the world's main reserve currency, many countries need to hold US dollars. This is equivalent to the United States being able to obtain a portion of wealth "for free" because other countries need to export goods and services to the United States in order to hold US dollars.

You can think of this as a "banker" who has the right to issue a universal currency. He only needs to print money to buy goods and services around the world. Although it is not so simple in practice, the global status of the US dollar does give the United States certain "seigniorage" benefits.

4.3 The trade deficit is only part of the truth

When we discuss trade deficits, we tend to focus only on the import and export of goods and services. But in fact, international trade also includes the flow of capital. Under the hegemony of the US dollar, the US trade deficit is often accompanied by a large net inflow of capital.

This is because when the United States buys goods and services from other countries, dollars will flow to these countries. And these countries tend to reinvest the dollars they earn into the U.S. financial market, such as buying U.S. Treasury bonds, stocks, real estate, etc. This capital repatriation makes up for the U.S. trade deficit to a certain extent.

You can think of it like a giant shopping mall. Customers (other countries) buy goods in American stores (the U.S. economy), and then deposit the money they earn back into the mall's own bank (the U.S. financial system).

According to the data from the U.S. Department of Commerce, the United States has maintained a trade deficit for many years, but at the same time, the U.S. financial account has shown a surplus, which means that the capital flowing into the United States exceeds the capital flowing out. This explains to a certain extent why the United States can maintain a trade deficit for a long time without triggering a serious economic crisis.

4.4 Triffin Dilemma: Intrinsic Contradictions under US Dollar Hegemony

The status of the US dollar as the world's reserve currency itself contains a famous economic problem - the Triffin Dilemma, which was proposed by American economist Robert Triffin in the 1960s.

Triffin pointed out that in order to meet the growing demand for dollars in global economic development, the United States must continue to export dollars, which means that the United States needs to maintain a trade deficit for a long time. Because only through a trade deficit can the dollar flow to all parts of the world and become the reserve currency and transaction medium of other countries.

However, a continued trade deficit will eventually lead to the accumulation of US debt and the credibility of the US dollar will be questioned. If the credibility of the US dollar declines, countries may reduce their holdings of US dollars and choose other currencies as reserves, which will shake the hegemony of the US dollar.

This creates a dilemma: in order to maintain liquidity in the global economy, the United States needs to maintain a trade deficit; but a long-term trade deficit will threaten the long-term stability of the US dollar.

In a word, it’s not easy to be a leader.

4.5 Summary: Trade Deficit under the Dollar Hegemony

In short, under the background of dollar hegemony, the US trade deficit has its own particularity. It is not just a simple difference between imports and exports of goods and services, but is also closely related to the status of the US dollar as the global reserve currency and settlement currency. The dollar hegemony has given the United States many economic "privileges", but it has also brought inherent contradictions and potential risks.

Back to the current tariff war. US President Trump claims that he wants to reduce the US trade deficit by imposing tariffs, believing that this can protect US jobs and industries. But from the perspective of US dollar hegemony, the US's true intentions may be more complicated.

Some analysts believe that the real purpose of the US tariff war is not just to reduce the trade deficit, but to maintain its leadership in the global economy and technology. By putting pressure on tariffs on specific countries and industries, the US may hope to force these countries to make concessions in terms of trade rules, intellectual property protection, technology transfer, etc.

In addition, tariffs can also be seen as a geopolitical tool used to adjust economic and political relations with specific countries. Simply put, tariffs are being "weaponized" due to the existence of the US dollar hegemony.

For the world, addressing the dollar hegemony is the fundamental solution to the weaponization of US tariffs.

5. The Achilles’ heel of the dollar hegemony

The hegemony of the US dollar is like the ancient Greek hero Achilles. No matter how powerful it looks, it always has a fatal weakness. Behind the powerful hegemony of the US dollar, there are many fatal economic and political loopholes. Once these loopholes are pierced by market forces or political changes, the US and global economies will usher in unprecedented turmoil.

5.1 The unsustainability of excessive debt

To understand the problem of dollar hegemony, let's first look at the data. As of March 2025, the US federal government debt has exceeded 36.56 trillion US dollars, equivalent to more than 124% of its gross domestic product (GDP). What does this data mean? Simply put, the scale of debt generated by the US government each year has exceeded the total of its annual economic production.

However, it is strange that the huge debt of the United States has not brought higher financing costs. On the contrary, over the past few decades, the United States has relied on the international status of the dollar to continuously lower borrowing interest rates, making the cost of debt extremely low. The yield of U.S. Treasury bonds has remained low for a long time - for example, between 2020 and 2024, the average yield of the 10-year U.S. Treasury bond was only about 2%, while other highly indebted countries, such as Brazil, had a yield of more than 10% or even higher during the same period.

Behind the seemingly beautiful situation of huge debt and low-cost financing is actually an economic miracle that is difficult to sustain. Once global investors lose confidence in the US debt repayment ability, the debt cost will rise rapidly and the credit of the US dollar will face severe tests.

The 2008 subprime mortgage crisis was the first time that the hegemony of the US dollar was seriously questioned. Although the Federal Reserve finally saved the situation with super-large-scale quantitative easing (QE), the United States temporarily overcame the difficulties, but it also buried deeper debt and inflation risks.

Since the outbreak of the COVID-19 pandemic in 2020, the U.S. federal government and the Federal Reserve have conducted more than $4.5 trillion in QE. Such an astonishing "printing money"-style money-printing operation has once again put the credibility of the U.S. dollar on the brink of collapse.

5.2 Global resistance to the US dollar system

The United States has long imposed economic sanctions and trade restrictions through the dollar system, which has led to serious dissatisfaction with the dollar in countries around the world. Data shows that between 2010 and 2024 alone, the U.S. Treasury Department imposed more than 20,000 financial sanctions and asset freezes on other countries, companies, and individuals through the dollar clearing system.

To give a recent example, after the outbreak of the Russia-Ukraine conflict in 2022, the United States quickly imposed the most severe financial sanctions in history on Russia: freezing Russia's foreign exchange reserves of approximately US$300 billion and prohibiting Russian banks from entering the SWIFT (Society for Worldwide Interbank Financial Telecommunication) US dollar clearing system.

Faced with the "financial hegemony" of the US dollar, more and more countries around the world have begun to actively seek alternatives and try to bypass the US dollar clearing system. Taking the BRICS countries (Brazil, Russia, India, China, and South Africa) as an example, since 2023, they have accelerated the promotion of non-US dollar trade settlement agreements. Data shows that in 2024 alone, non-US dollar settlements accounted for more than 70% of China-Russia trade; India and the UAE signed an agreement in 2023 to settle bilateral trade in rupees; Brazil and Argentina actively promoted local currency transactions to reduce their dependence on the US dollar.

Furthermore, in August 2024, the BRICS summit formally proposed the establishment of a "BRICS common currency". Although this concept is still in the exploratory stage, it undoubtedly shows that the trend of de-dollarization is accelerating.

5.3 Challenges of decentralized currency

If the efforts of various countries to de-dollarize are still just preliminary attempts, then the rapid development of digital currencies has opened up a whole new battlefield for the global financial market.

Cryptocurrencies, represented by Bitcoin, have gradually attracted the attention of more and more investors, companies and even governments around the world due to their decentralization and the fact that they cannot be controlled by a single country. According to a 2024 research report by the University of Cambridge, more than 300 million people in the world have owned or used cryptocurrencies.

Although Bitcoin has not yet truly challenged the dollar's position as the world's reserve currency, it provides a new wealth storage and cross-border payment solution. El Salvador became the first country in the world to make Bitcoin a legal tender in 2021, followed by the Central African Republic in 2022. Although these countries are small, such actions send a clear signal to the world: monetary sovereignty does not necessarily have to rely on the US dollar system.

5.4 Possible Paths to the End of US Dollar Hegemony

From historical experience, no currency's hegemony is permanent. The Spanish silver dollar, the Dutch guilder, and the British pound all enjoyed great success in history, but eventually declined. Although the US dollar is still strong, it will inevitably face periodic challenges.

Experts believe that there are roughly three paths that may lead to the end of the US dollar hegemony:

First, the trend towards global multipolarization continues to accelerate. The United States' international economic status is gradually declining, and the global economic center of gravity is shifting to emerging markets such as East Asia, South Asia, and the Middle East. More countries are promoting the popularization of non-dollar settlement mechanisms based on their own interests. The demand for the US dollar as a reserve currency is gradually decreasing, and the US dollar hegemony is being diluted.

Second, the credit system of US debt is seriously questioned by the market. The US cannot continue to raise funds at low cost. The soaring debt interest rate has led to the outbreak of the government debt crisis and the credibility of the US dollar has encountered an unprecedented crisis. In this case, the global capital market will sell off US dollar assets, causing the credit of the US dollar to collapse and the US dollar system to collapse instantly.

Third, the rapid popularization of digital currencies has made global cross-border trade no longer highly dependent on the US dollar clearing system. Especially after the digital RMB and decentralized digital currencies such as Bitcoin became mainstream international payment tools, the world's dependence on the US dollar has been greatly reduced. The US dollar no longer has the absolute function of a "financial weapon", and its hegemony has automatically ended.

However, decentralized stablecoins, especially those that are not related to US dollar assets, will become a strong competitor to replace the US dollar.

6. Decentralized stablecoins end the hegemony of the US dollar

Over the past decade, the rapid rise of cryptocurrencies has allowed people to see more possibilities beyond the traditional monetary system. In this trend, stablecoins have gradually become an important force in changing the existing monetary landscape with their relatively stable value anchoring, convenient cross-border payment functions, and decentralized potential. But it is worth noting that not all stablecoins are qualified to become "candidates" to end the hegemony of the US dollar in the future.

6.1 Classification of Stablecoins and Their Operating Mechanism

In order to understand stablecoins in depth, we first divide stablecoins into three categories:

Category 1: Fiat-collateralized stablecoins

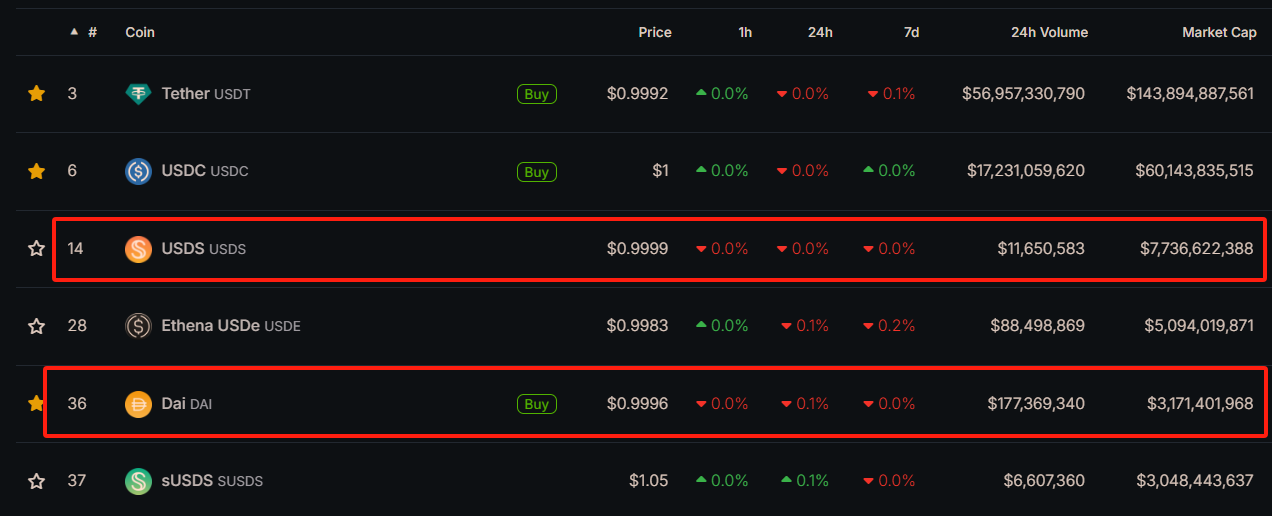

As the name implies, fiat-collateralized stablecoins are tokens that are collateralized by traditional fiat currencies such as the U.S. dollar and the euro and are pegged 1:1 to these currencies. The most famous examples include USDT (Tether) and USDC (USD Coin). As of April 9, 2025, the market value of USDT is as high as 140 billion U.S. dollars, and that of USDC is 60 billion U.S. dollars. Together, they account for more than 85% of the stablecoin market, as shown in the figure below.

The biggest advantage of this type of stablecoin is that it is easy to understand and has low risk. As long as the issuer actually holds the same amount of legal currency assets as the issuance amount, the price of its token can be effectively guaranteed. But because of this, the stability and reliability of this type of stablecoin is highly dependent on the credit of centralized institutions (such as Tether and Circle).

However, this is the core of the problem - centralized institutions are inevitably constrained by political power, jurisdiction, and financial regulation.

Category 2: Crypto-collateralized stablecoins

Cryptocurrency-collateralized stablecoins are collateralized by other crypto assets (such as ETH, BTC) and use over-collateralization to ensure price stability. Representative examples include DAI (MakerDAO) and decentralized stablecoins such as LUSD (Liquity) that have emerged in recent years.

MakerDAO underwent a major rebranding in August 2024, changing its name to Sky and renaming its stablecoin DAI to USDS. For the sake of convenience, we will continue to use the old name for the time being.

As of the end of March 2025, the market value of DAI + USDS exceeded 10.8 billion US dollars, making it the leader of cryptocurrency-collateralized stablecoins, as shown in the figure above. This type of stablecoin is far more decentralized than fiat-collateralized stablecoins, because its collateral is decentralized crypto assets, and the collateral and issuance process are automatically completed through smart contracts, so there is no room for human manipulation in theory.

Category 3: Algorithmic Stablecoins (Uncollateralized)

The concept of algorithmic stablecoins was first proposed by Basis and later TerraUSD (UST). This type of stablecoin does not have any fiat currency or other assets as direct collateral, but automatically adjusts the supply through complex algorithms, trying to anchor the value to fiat currency (usually the US dollar). The collapse of TerraUSD in 2022 caused severe market turmoil, and the market once believed that algorithmic stablecoins had failed, but recent new algorithmic stablecoins such as Frax and Reflexer have tried to gradually restore market confidence.

Nevertheless, due to the lack of real asset endorsement, the long-term stability of algorithmic stablecoins has not yet been recognized by the market.

6.2 Why can’t USDT and USDC end the dollar’s hegemony?

Let’s get back to the core question of this article - why is it difficult for USDT and USDC, stablecoins backed by US dollar assets, to replace the US dollar and become the new hegemonic currency?

The key reason is that their value foundation is still firmly tied to US dollar assets, and the control of US dollar assets belongs to the US government and its regulatory agencies.

First, let's look at some actual data and examples:

During the 2022 Russia-Ukraine conflict, the United States launched unprecedented financial sanctions against Russia, freezing more than $300 billion of Russia's foreign exchange reserves, including a large number of financial instruments backed by U.S. dollar assets. Subsequently, the U.S. Treasury Department issued a clear warning, requiring all stablecoin issuers under U.S. jurisdiction to freeze any accounts related to Russian entities.

Circle (the issuer of USDC) responded quickly and froze millions of dollars worth of USDC accounts. This move clearly demonstrated the fact that USDC and similar USD-collateralized stablecoins are essentially just blockchain versions of the US dollar, and their essence has not changed - their assets are still subject to the strong jurisdiction of US regulators.

Let's look at USDT. From 2021 to 2024, USDT froze dozens of addresses at the request of the U.S. Department of Justice (DOJ) and the New York Attorney General's Office (NYAG), with a total amount of hundreds of millions of dollars. This also shows that even though Tether, the issuer of USDT, claims that it is registered in the British Virgin Islands and is not subject to U.S. jurisdiction, under the pressure of sanctions from the global U.S. dollar settlement network, Tether still has to "bow its head" and cooperate with the implementation of the freezing measures.

More importantly, this power is actually exactly the same as the SWIFT system of the traditional financial system. The United States only needs to issue an order to any stablecoin issuer backed by US dollar assets to quickly freeze the account and cut off the capital link. This means that stablecoins backed by US dollar assets cannot escape the direct control of the US dollar hegemony, and cannot truly replace the hegemony of the US dollar in global trade and finance.

6.3 Stablecoins that can truly end the hegemony of the US dollar - decentralized stablecoins without US dollar asset collateral

Therefore, the stablecoin that can truly break this deadlock must be a stablecoin that is completely decoupled from US dollar assets, cannot be blocked, and is completely decentralized.

What are the characteristics of such a stablecoin? Taking MakerDAO’s decentralized stablecoin DAI as a starting point, the ideal stablecoin model in the future may be:

Collateral assets are diversified and decentralized: the main collateral is no longer the U.S. dollar or U.S. dollar financial assets, but decentralized assets such as BTC and ETH, and may even be tokenized forms of gold or other non-U.S. dollar assets.

Completely decentralized governance mechanism: The mortgage, minting, and liquidation mechanisms are completely implemented through smart contracts. No centralized entity or state power can unilaterally control or freeze assets.

No regulatory single point of failure risk: All collateral assets are distributed across different nodes around the world. No government or institution can freeze or control them alone, which means that this stablecoin will be completely free from the influence of the United States’ financial hegemony.

When the collateral assets of stablecoins are completely de-dollarized, the United States is actually kicked out of the center stage of this currency game, which directly leads to the complete disappearance of the seigniorage income it has always enjoyed.

Seigniorage is essentially the additional benefits that the United States brings by issuing US dollars and allowing the world to actively hold US dollar assets. For example, the US government saves up to hundreds of billions of dollars in interest costs each year by relying on the US dollar's global reserve status (the estimated cost savings on US Treasury bond interest in 2023 alone will exceed US$250 billion).

But when stablecoins completely shift to non-US dollar assets such as BTC, ETH or gold, countries and institutions around the world no longer need to hold US dollars or US dollar bonds as collateral assets, which means that the United States loses the right to print US dollar "paper bills" at zero cost in exchange for real goods around the world.

From this moment on, the U.S. Treasury can no longer issue Treasury bonds and easily obtain global funds at low cost by relying on the global settlement currency status of the U.S. dollar as in the past. This new stable currency pattern is actually cutting off the hidden economic channel for the United States to harvest global wealth by relying on seigniorage and low-cost financing.

6.4 Summary: Decentralized stablecoins are the key to ending the hegemony of fiat currencies

Once such decentralized stablecoins are truly widely adopted, they will completely subvert the existing financial landscape:

Trade between countries will no longer need to go through the US dollar clearing system (such as SWIFT), and will be free from the threat of sanctions and freezes.

The free flow and security of global funds have been greatly improved, and funds will not be arbitrarily blocked or frozen, nor will they be used as a weapon in geopolitical struggles.

The cost of capital has been greatly reduced, and there is no need to pay invisible "seigniorage" and "dollar tax" to the US dollar hegemony.

With the maturity of blockchain technology and decentralized governance mechanisms, the global economy may gradually break free from the shadow of the US dollar hegemony and usher in a new era of truly free and open finance.

Decentralized and de-dollarized stablecoins will become a new world currency, a world currency that will not form a new hegemony.

Conclusion

The era of the US dollar may be coming to an end, not because the United States is no longer powerful, but because the world is no longer willing to entrust its fate to a piece of paper money that can be turned into a weapon at any time.

History reminds us time and again that money is not just about cold numbers, but also about human trust and freedom. When the US dollar repeatedly uses its hegemonic position to drag the global economy into the abyss of division and stagflation, a new financial order will quietly rise.

The emergence of decentralized stablecoins not only means the innovation of financial instruments, but also the awakening of the human spirit of monetary freedom. Truly secure wealth is never protected by power, but is built on technology and consensus. The future global economy is destined to belong to decentralized currencies that cannot be frozen or banned by any power.

When stablecoins no longer rely on U.S. dollar assets as collateral, the U.S. dollar hegemony will also fade. We are standing at the turning point of an era, witnessing not only the victory or defeat of a tariff war, but also the historic moment of the end of monetary hegemony.

Stablecoins no longer rely on the US dollar, what should they rely on the most? Bitcoin, the native cryptocurrency. Now, how should ordinary people face the problem at the beginning? The answer naturally emerges. It's very simple. From now on, save enough DCA Bitcoin for living expenses. For more details, please see "Bitcoin: The Ultimate Hedging Solution for Long-termists?"

Perhaps many years later, when people look back on today, they will be amazed to find that:

It turns out that the dawn of monetary freedom quietly began in such a silent war.

Maybe it is not earth-shattering, but it will profoundly change the world.