The market, project, currency, and other information, views, and judgments mentioned in this report are for reference only and do not constitute any investment advice.

Written by 0xWeilan

The chaos and anxiety caused by Trump's tariff war, coupled with the rebound in U.S. inflation expectations, have strengthened market expectations of potential "stagflation" or even "recession" in the U.S. economy. This is extremely negative for high-risk assets.

This expectation has hit the valuation of U.S. stocks, which have been rising for two years, and then transmitted to the crypto market through the BTC ETF.

Short-term BTC investors are selling to lock in the maximum loss within this cycle, initially completing BTC's latest pricing. Long-term investors have once again shifted from "selling" to "buying" and absorbed part of the sell-off, bringing the price to a new balance around $82,000. However, the market remains fragile, with short-term investors still having high unrealized losses. If U.S. stock market chaos triggers BTC ETF fund sales, short-term investors will inevitably participate in selling, which will further drive down prices.

The current moderate adjustment in U.S. stocks is basically complete, but further trends depend on the extent of the tariff war's impact on April 2nd and whether the March employment data shows a significant recession. If both exceed expectations and worsen, further downward pricing will occur.

Contrary to expectations. As the chaos unfolds, both U.S. stocks and BTC have undergone significant corrections, and selling pressure and panic have been largely released.

We believe that as the negative impact of the tariff war gradually dissipates and the Federal Reserve gradually resumes rate cuts, BTC's reversal in the second quarter is a high-probability event.

Macro Finance: Economic and Employment Data Strengthen "Stagflation" and "Recession" Expectations, U.S. Stocks Break Down

After the "Trump 2.0 trade" fizzled out, U.S. stocks essentially returned to the starting point of November 6, 2024, the day Trump was elected. A new trading judgment framework was initially established in late February, and the entire month of March revolved around the output of this framework after inputting various economic, employment, and interest rate data.

This framework is the game between the possibility of "economic stagflation" or even "economic recession" caused by Trump's tariff policy and the Federal Reserve's choice between prioritizing employment or controlling inflation.

On Friday, March 7th, the U.S. Bureau of Labor Statistics first released February employment data: February non-farm employment increased by 151,000, lower than the market expectation of 170,000, indicating slowing job growth but still maintaining relative stability. The unemployment rate rose from 4.0% in January to 4.1%, showing a slight loosening of the labor market. Average hourly wages increased by 0.3% month-on-month and 4.0% year-on-year, higher than the inflation rate, indicating improved real wages but potentially putting pressure on inflation.

This "acceptable" employment data partially allayed fears of an economic recession, causing U.S. stocks to initially fall and then rise. However, concerns remain, as employment data was below expectations and the unemployment rate is rebounding.

On March 12th, the U.S. Department of Labor released CPI data: February's overall Consumer Price Index increased by 0.2% month-on-month and 2.8% year-on-year, slightly down from January's 3.0%. Core CPI (excluding food and energy) increased by 0.2% month-on-month and 3.1% year-on-year, showing some moderation in inflation, but core inflation remains above the Federal Reserve's 2% target.

The PCE data, which the Federal Reserve pays more attention to, was released on the 28th, showing: February's overall Personal Consumption Expenditures Price Index increased by 0.3% month-on-month and 2.5% year-on-year; core PCE increased by 0.4% month-on-month and 2.8% year-on-year, reflecting that the inflation downward path is obstructed, with core indicators showing strong stickiness.

The PCE data shows that February's overall Personal Consumption Expenditures Price Index increased by 0.3% month-on-month and 2.5% year-on-year, higher than January's 2.5%; core PCE increased by 0.4% month-on-month and 2.79% year-on-year, higher than January's 2.66%.

Although the increase is small, both CPI and PCE indicate that price increases have begun to rebound, meaning the Federal Reserve's inflation reduction target is facing a serious challenge.

After the two-day meeting on the 18th-19th, the Federal Reserve announced maintaining the federal funds rate at 4.25-4.50%, pausing rate cuts for the second consecutive time. The statement noted steady economic expansion, a solid labor market, but slightly high inflation, with increased economic uncertainty due to Trump's policies. This is the first time the Federal Reserve explicitly stated that tariff policies might affect economic downturn, but the risk of economic recession has "increased but is not high".

Perhaps to comfort the jittery stock market, Fed Chair Powell stated that inflation might be delayed in returning to the 2% target due to policies like tariffs, and hinted at rate cuts if the job market deteriorates. As a preemptive measure against tariff impact, the Fed slowed down U.S. Treasury sell-off from $25 billion/month to $5 billion/month.

The relatively "dovish" stance by the Federal Reserve boosted the market, driving the three major indices to rebound significantly. By the end of the month, the CME Fed Watch board showed that the market first raised the expectation of rate cuts in 2025 to three times. Goldman Sachs also predicts three rate cuts this year.

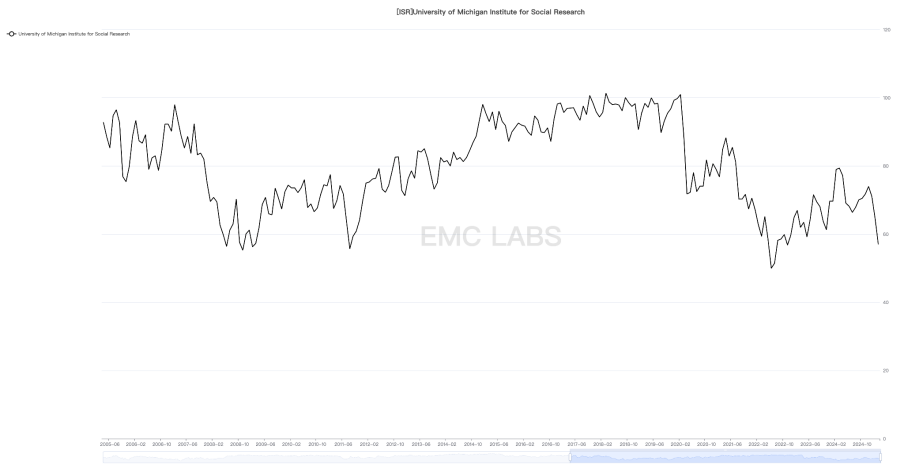

On Friday, the 28th, the University of Michigan released the March Consumer Confidence Index final value, dropping from February's 64.7 to 57, slightly lower than the initial value of 57.9 and below the median estimate of surveyed economists. Consumers expect the annual inflation rate in the next 5 to 10 years to be 4.1%, the highest since February 1993, up from the initial value of 3.9%. The expectation for the next year's inflation rate is 5%, the highest since 2022.

The University of Michigan Consumer Confidence Index is subjective data but fully reflects the decline in end-consumer confidence. On the same day, the Atlanta Fed's GDPNow model showed that as of the 28th, the predicted Q1 U.S. real GDP growth rate was -2.8%. This value resonates with the University of Michigan Consumer Confidence Index, and like in February, the three major indices responded with significant drops, with the VIX index rising 11.9% in a single day.

University of Michigan Consumer Confidence Index

Regarding Trump's tariff policy, there were multiple back-and-forth developments this month. By the end of March, tariffs on Canada, Mexico, China, and steel and aluminum products had already been implemented.

Starting April 2nd, the U.S. will impose a 25% tariff on all imported vehicles, covering passenger cars and light trucks. A 25% tariff will also be imposed on core automotive parts (such as engines, transmissions, electrical systems), with the effective date no later than May 3rd.

The "reciprocal tariffs" on major trade deficit countries remain undecided, with the specific list to be released on April 2nd. April 2nd is currently viewed by the market as the most significant date for tariff wars.

Due to uncertainty about tariffs and concerns of "economic stagflation" or even "economic recession", funds continued to withdraw from equity markets in March, causing the Nasdaq, S&P 500, and Dow Jones to drop 8.21%, 5.75%, and 4.20% respectively, breaking or approaching the 250-day moving average, achieving a moderate technical adjustment.

Safe-haven funds flowed into U.S. Treasuries, pushing the 2-year U.S. Treasury yield down 1.15% for the month. The 10-year Treasury yield dropped 0.45%, but combined with inflation expectations, long-term funds' expectations for long-term economic growth have fallen to negative growth.

Another safe-haven asset, gold, was particularly favored by mainstream funds, with London gold officially breaking the 3000 mark this month, rising 8.51% to $3,123.97 per ounce.

Low consumer confidence, rising inflation expectations, pessimistic about U.S. economic growth, and even worried about uncontrollable and unpredictable tariff wars driving the U.S. economy into "stagflation" and "recession". EMC Labs judges that Trump's tariff uncertainty is the biggest variable, pushing U.S. economic and consumer confidence to deteriorate, thereby driving market "stagflation" and "recession" trading. With Powell's relatively "dovish" remarks, the market began to speculate on the Federal Reserve's potential rate cut intervention in June, and as U.S. stocks fell, the number of rate cuts increased from two to three. The inflation issue might be temporarily shelved but has not disappeared and may even be exacerbated by the tariff war. The impact of the tariff war will only be fully understood after it is finalized.

Crypto Assets: Running in a Downward Channel, Extreme Market Might Drop to $73,000

Traders' anxiety and fear dominated the capital market volatility in March. BTC, after a significant drop at the end of February, remained relatively stable in March but lacked momentum for a rebound, ultimately recording a 2.09% monthly decline.

In February, BTC opened at $84,297.74, closed at $82,534.32, with a high of $95,128.88, a low of $76,555.00, and a volatility of 22.03%, with trading volume slightly expanding compared to the previous month.

Temporally, after the sharp drop at the end of February, BTC conducted a technical rebound in the second and third weeks of March, but the rebound was weak, with a maximum increase of only 16% from the low point. In the following week, with the chaos of US tariff policies and the decline in inflation data, especially consumer confidence data, BTC oscillated downward with US stocks, ultimately recording a monthly decline.

Technically, it ran within the downward channel since February, below the first upward trend line of this cycle. After the initial drop at the beginning of the month, trading enthusiasm sharply decreased, with trading volume declining weekly. It mostly ran below the 200-day line, briefly touching the 365-day line on March 11.

Although centralized exchanges showed BTC outflows and the BTC ETF channel had slight fund inflows, BTC, as a high-risk asset, still struggled to attract buying power under the tense US stock market atmosphere.

[The translation continues in the same manner for the rest of the text, maintaining the specified translations for specific terms.]BTC Different Holder Profit and Loss Statistics

This pressure, if converted into selling pressure, could push BTC down to $73,000, which is the upper limit of the new high consolidation area and the price before Trump's election.

Conclusion

From an external perspective, the current BTC price is completely subject to the game between tariff chaos and inflation stickiness leading to economic "stagflation" or even "recession" expectations and whether the Federal Reserve will compromise on interest rate cuts.

From an internal perspective, short-term holders have experienced the largest sell-off losses in this cycle over the past month. Currently, selling pressure has weakened, but the floating loss pressure is still significant. It cannot be ruled out that further selling may occur to alleviate pain, though the probability is low. Long-term holders' shift from selling to buying has a stabilizing effect on the market.

Stablecoins continue to flow in, and BTC ETF channel funds also show signs of inflow. However, if US stocks decline, ETF channel funds may sell again, becoming the primary force driving prices down.

On April 2nd, Trump's tariff war will reach a phased high point, when US stocks may find a short to medium-term bottom. Conversely, if tariff policies do not severely deteriorate, the US economy shows recession signs but not severely, and the Federal Reserve cuts rates again in June, BTC, which has already experienced a massive valuation massacre, turning around in Q2 becomes a high-probability event.

After the first quarter's turbulence, the second quarter's prospects remain unclear, but the most painful moment may have passed. Once Washington and the Federal Reserve return to rational negotiation, the market should return to its own operating rules.

EMC Labs was established in April 2023 by crypto asset investors and data scientists. Focusing on blockchain industry research and Crypto secondary market investment, with industrial foresight, insights, and data mining as core competencies, committed to participating in the booming blockchain industry through research and investment, promoting blockchain and crypto assets' benefits for humanity.

For more information, please visit:https://www.emc.fund