Introduction: Survival Rules After the Collapse of Faith

On March 31, 2025, Ethereum encountered two iconic events: the market's collective expectation of a whale's liquidation fell through, and the ETF staking proposal's "silent abortion". These two events tore open the most brutal truth of the crypto market - when Ethereum sheds its "King of Public Chains" halo, its price fluctuation has completely become a gambling chip among Wall Street institutions. This article will analyze the deep logic of ETH that has not yet hit bottom from five dimensions: capital flow, staking mechanism, market narrative, competitive landscape, and regulatory trends.

I. Capital Flow: Strategic Intent Behind Institutional Coldness

1.1 The "Hot and Cold" of ETF Capital Flow

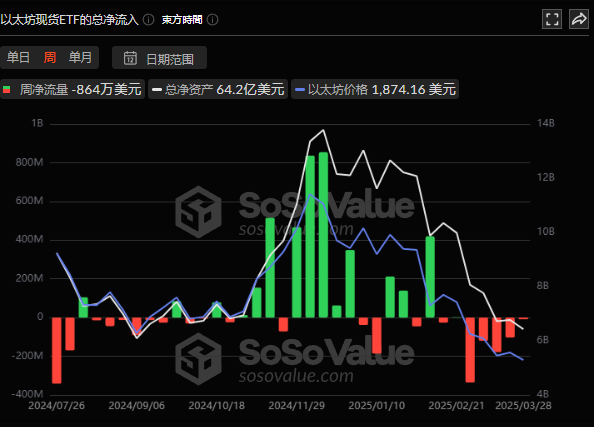

According to SoSoValue data, in the first three months of 2025, the US Ethereum spot ETF cumulatively net outflowed $240 million, while the Bitcoin ETF maintained a net inflow of $790 million during the same period. This divergence is no coincidence:

- Institutional risk-aversion preference: Bitcoin's "digital gold" positioning better aligns with traditional asset management institutions' allocation logic, while Ethereum's complex smart contract attributes make it difficult to incorporate into traditional valuation frameworks

- Lack of staking returns: Existing Ethereum ETFs cannot provide staking returns (approximately 3.12% annually), which is utterly unattractive compared to 5-8% staking returns of competing chains like Solana

- Liquidity trap: Ethereum mainnet gas fees have dropped to a historical low (0.758 Gwei), and the seemingly prosperous Layer 2 ecosystem actually diverts value capture capability

1.2 BlackRock's "Silent Conspiracy"

Market observers are generally puzzled: As an asset management giant holding $500 million in ETH, why hasn't BlackRock submitted any staking application? This exposes the deep considerations of top-tier institutions:

- Cost control strategy: By suppressing market sentiment and creating panic selling, creating space for subsequent low-price accumulation. Data shows that when ETH fell below $2,000, BlackRock had counter-trend positions

- Regulatory arbitrage space: Waiting for the Pectra upgrade (EIP-7251) to raise the validator node staking cap to 2048 ETH, significantly reducing operational costs before entering

- Time difference tactics: Using "small institutions" like 21Shares to test regulatory boundaries while reserving a late-mover advantage. Just as Bitwise adopted a "point-and-click" staking mode to avoid risks, top-tier institutions need a safer entry posture

II. Staking Mechanism: A Castrated Value Capture Tool

2.1 The "Triple Paradox" of ETF Staking

Although the market views ETF staking as a lifeline, its design flaws are destined to fail to reverse the decline:

- Misaligned return attribution: Proposals by 21Shares stipulate that staking returns belong to the trust, with investors only indirectly benefiting through net value changes, directly weakening the attractiveness of the 3.12% annual return

- Liquidity shackles: Ethereum staking requires a 57.69-day entry and 28.47-day exit cycle, which is equivalent to a risk amplifier in a highly volatile crypto market

- Centralization dilemma: Coinbase's custody accounts for over 27%, which goes against the "decentralization" narrative. Institutions prefer Lido's liquidity staking solutions, but SEC's regulatory ban has closed this path

2.2 Structural Defects in Staking Economics

The transition from PoW to PoS has fundamentally changed Ethereum's value support logic:

- Disappearance of miners' moat: In the PoW era, miners' fiat cost constituted the price floor (about $800/ETH), while PoS validators only have $0.12/day server costs, leading to fragile support

- Ineffective deflationary mechanism: Layer 2 causes a sharp drop in mainnet gas burning, with annual inflation rate rebounding to 0.76%, losing the scarcity premium created by EIP-1559

- Staking returns trap: The current 3.12% annual return is far below the US Treasury yield (4.8%), and institutions prefer to hold interest-bearing US bonds rather than bear volatility risks

III. Narrative Collapse: When Technical Innovation Becomes a Capital Game

3.1 The Lost "Killer Application"

Ethereum once topped the public chain rankings through three narrative waves: DeFi (2020), Non-Fungible Token (2021), and Layer 2 (2023), but its ecosystem in 2025 presents:

- Developer exodus: Solana's daily processing volume of 65 million transactions far exceeds Ethereum mainnet + Layer 2's 20 million, causing DApp development to migrate to high-performance chains

- Capital migration: MEME coins, RWA, and other new hotspots are concentrated on chains like Solana and Ton, with Ethereum's TVL share plummeting from 56.37% to 32%

- Technological upgrade stagnation: Delayed Pectra upgrade exposes development bottlenecks, with key innovations like Verkle Trees remaining at the roadmap stage

3.2 Deconstructed Valuation Logic

Institutions are reassessing ETH's value with a new model:

- Discounted cash flow method fails: Network income (gas fees) has decreased by 82% year-on-year, unable to support DCF valuation

- Metcalfe's law reversed: Active address count has dropped to a new annual low, with network effects showing negative growth

- Inventory model trap: 27.85% of ETH is locked in staking, which should have pushed up prices, but increased whale concentration (now 61%) instead exacerbates liquidity crisis

IV. Competitive Landscape: Value Dilution Amid Encirclement

4.1 Survival Crisis Under Layer 1 Siege

- Performance crushing: Solana 6500 TPS vs Ethereum 15 TPS (including Layer 2)

- Compliance advantage: Ripple's settlement with SEC shapes a new regulatory paradigm, while Ethereum remains trapped in "securitization" controversy

- Capital support: Market makers like Jump Trading fully support the Solana ecosystem, forming an institutional clustering effect

4.2 Layer 2's "Separatist Rebellion"

The prosperous Layer 2 ecosystem is now biting back at the mother chain:

- Value outflow: Layer 2 tokens like ARB and OP capture ecosystem growth dividends, with ETH reduced to a "gas fee voucher"

- Settlement layer crisis: Solutions like zkSync's Validium directly bypass mainnet settlement, shaking Ethereum's fundamental positioning

- Developer defection: Base chain's DApp numbers grew 300% in 3 months, far exceeding mainnet growth

Conclusion: Value Reconstruction in the Darkest Moment

When the ETH/BTC exchange rate falls below 0.022, when gas fee burning hits a historical low, when BlackRock coldly observes staking approval... All of this indicates that Ethereum is experiencing the most brutal value reconstruction in blockchain history. Institutions hover like vultures, waiting to feast on the corpse of this once-king after it bleeds its last drop.

However, the ironic twist of history is that new life is often born in the darkest moments. The Pectra upgrade may revive developer confidence, and if the ETH ETF staking resolves the revenue distribution issue, it could attract hundreds of billions of dollars in traditional funds. The "secret weapon" being brewed by Vitalik's team - reportedly involving the fusion of ZK-EVM and AI agents - might reignite market enthusiasm. The game between institutions and technology is far from over, with the only certainty being: when Wall Street completes its chip collection, Ethereum's phoenix-like rebirth will truly begin.