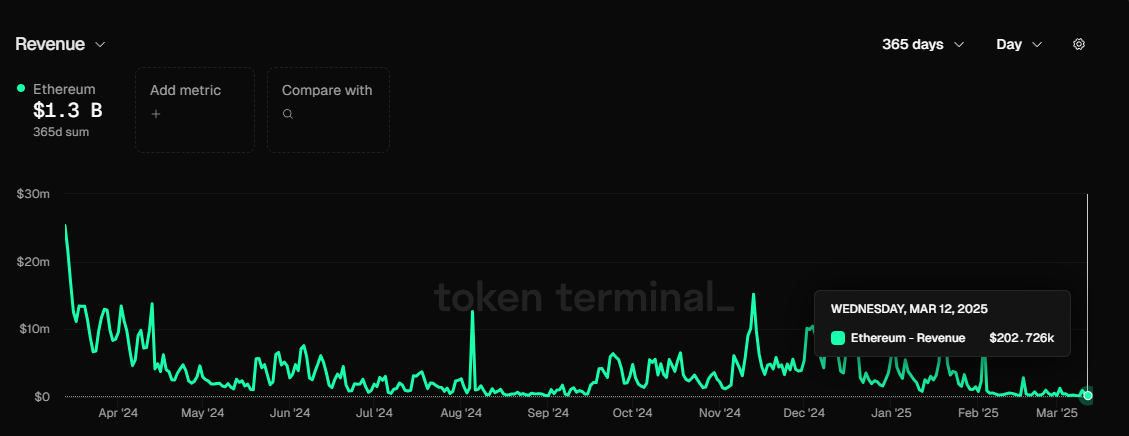

On March 13, 2025, a set of data shocked the Ethereum community: in the past 24 hours, the mainnet revenue was only $200,000, falling out of the top 20 on the public chain rankings. Recalling the DeFi craze days of 2020, a single transaction's gas fee could easily reach tens of thousands of RMB, and scrambling for popular projects was like a battlefield. Now, all of this seems to have become a distant memory, and the on-chain activity of Ethereum is eerily quiet. The former king of public chains, how did it come to this? Has it really fallen into the "midlife crisis" that people talk about?

From Peak to Trough: Ethereum's Dilemma Emerges

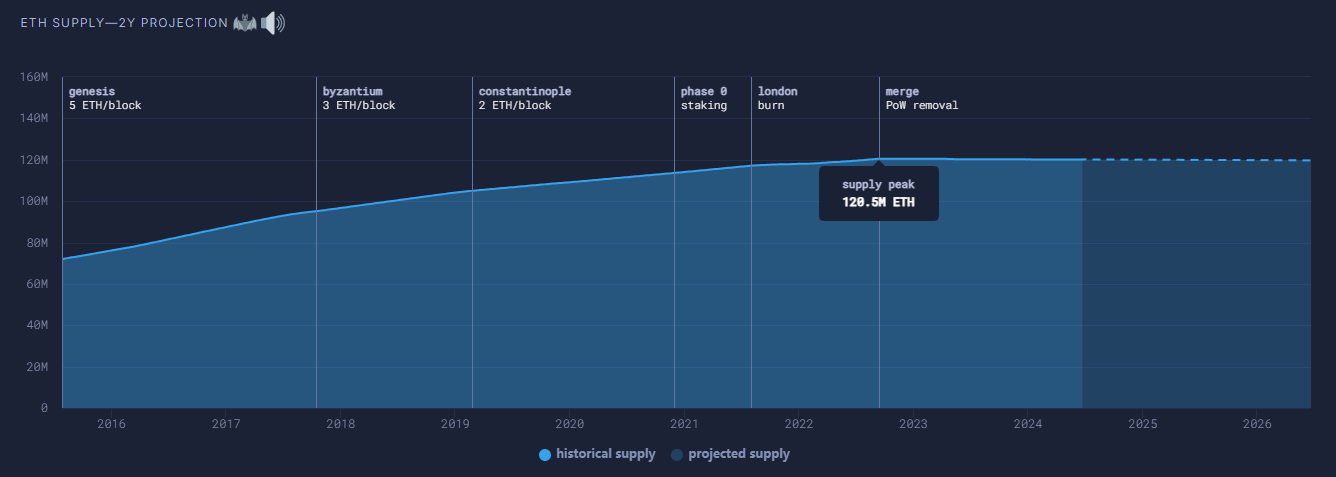

Ethereum's current state can be summarized in one word: "depressed," but this depression did not come overnight, but rather the result of a slow fermentation of multiple factors. The first and foremost is the cliff-like drop in mainnet transaction fees. In 2021, the DeFi and NFT craze easily pushed Ethereum's daily revenue to tens of millions of dollars, and the EIP-1559 burning mechanism even once made ETH a potential "deflationary asset." However, with the shrinkage of on-chain activity, the gas burning volume has dropped significantly, while the issuance of staking rewards has not stopped, causing the supply of ETH to start inflating, and the dream of deflation has been shattered. Holders see the actual value of their account balances shrinking, and their confidence is naturally shaken.

At the same time, Ethereum's application layer seems to have lost the magic of the past. Once, this was the birthplace of decentralized finance, the cradle of innovations like Uniswap, Aave, and CryptoPunks, and every wave of heat could ignite market enthusiasm. Now, the DeFi wave is gradually receding, the NFT market is dormant, and the emerging blockchain games and AI narratives are more prevalent in the ecosystems of competitors like Solana and TRON. Ethereum not only lacks original breakthroughs, but even the successful cases of imitating others seem to be beyond its reach. This stagnation of innovation makes people wonder whether its ecosystem can regain its former glory.

Looking at Layer 2 (L2), which was supposed to be Ethereum's killer solution to the scalability problem, it has now become the focus of controversy. The Dencun upgrade in March 2024 significantly reduced the transaction costs of L2, and projects like Base and Arbitrum were once highly anticipated. However, reality has been disappointing: the prosperity of L2 has not led to widespread participation of retail users, and the fragmentation of liquidity has made the user experience fragmented. Worse, the revenue of L2 has not been fed back to the mainnet, but rather exacerbated the "parasitic effect." For example, Base, backed by Coinbase, is making a fortune, but the mainnet only gets a negligible amount of gas fees. This wholesale block space strategy has ultimately become a shell with no one to turn to.

At the governance level, the performance of the Ethereum Foundation (EF) is also a source of concern. Compared to Solana's rapid rise through foundation support and capital operations, Ethereum appears too conservative. The EF's decision-making pace is slow, and its disconnect from the frontline market has caused it to miss many new trends, such as the Meme coin craze and AI narratives. Although the voices in the community are many, it is difficult to coalesce into effective action, and this rigidity has gradually sapped Ethereum's vitality in the competition.

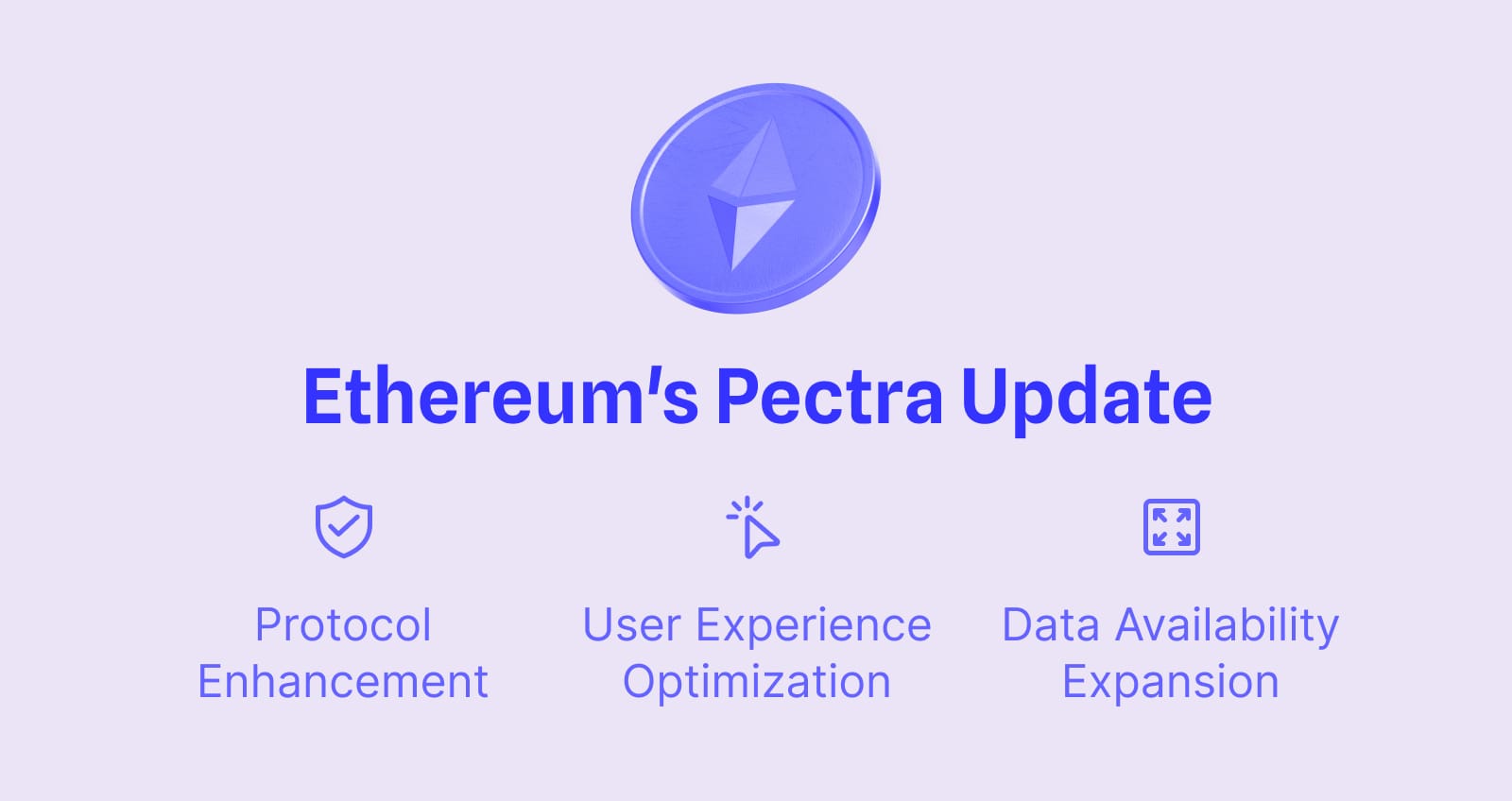

Pectra Upgrade: Dawn or Mirage?

Against this backdrop, on March 5, 2025, Ethereum welcomed the Pectra upgrade. This upgrade integrates the Prague (execution layer) and Electra (consensus layer), containing 11 EIPs, aiming to optimize the staking experience, improve L2 scalability, and expand network capacity. The mainnet deployment is expected to be completed on April 8, and the community has both expectations and doubts about it.

Pectra brings some obvious improvements. For example, account abstraction (EIP-7702) makes wallet operations more flexible, and users can even use USDC to pay gas fees, with batch transactions and gas sponsorship becoming accessible. The staking limit has been raised from 32 ETH to 2048 ETH (EIP-7251), lowering the threshold for large institutions to participate, and improving the management efficiency of validators. The Blob capacity of L2 has been increased from 3 to 6 (EIP-7691), and the transaction cost is expected to further decrease, while the validator activation time has been shortened from 9 hours to 13 minutes (EIP-6110), making the network's operation smoother.

However, can these technical advancements really reverse Ethereum's decline? The answer is not optimistic. While the increase in staking limits has attracted institutions, it has squeezed out retail participants, quietly deepening the shadow of centralization. The increase in L2 capacity seems positive, but if the application layer cannot keep up, user growth will still be empty talk. More crucially, the downward trend in mainnet revenue has not been reversed by Pectra. The prosperity of L2 is still draining the vitality of the mainnet, with Base's profits flowing to Coinbase and Arbitrum's earnings going to the DAO, while Ethereum mainnet can only watch itself being marginalized. Vitalik Buterin has recently expressed a strong view on this, warning that if the L2 ecosystem does not calm down and solve the interoperability problem, Ethereum will raise the data block fee by 200%. This statement reflects his dissatisfaction with the current fragmentation of L2, and also hints at a possible future adjustment - by raising the cost to force L2 integration, or redirecting resources back to the mainnet.

The Root of the Dilemma: The Cost of Choices and Competition

Ethereum's current predicament is not without a trace. Its dilemma is both the cost of its own choices and the result of external competition.

First, Ethereum's positioning has determined its fate. As a highly decentralized public chain, it refuses to sacrifice security and decentralization for higher TPS. This persistence has won it the status of DeFi hegemon and attracted countless believers. However, when Solana swept the market with a single chain's high throughput and low cost, Ethereum's shortcomings were exposed. L2 became an inevitable patch, but it cannot cover the innate insufficiency of mainnet performance. The cost of this positioning is becoming increasingly apparent in the intensified competition.

Secondly, the competition in the public chain arena has never ceased. The block space business is not the exclusive patent of Ethereum, as EOS had a brief moment of glory and Solana rose to prominence later, each new public chain's rise eroding Ethereum's market share. The moat of public chains is far more fragile than imagined, with ecosystem activity generally dropping 95% in bear markets, and without grasping new narratives, the first-mover advantage will be lost. In this cycle, Meme coins and AI hype have become Solana's boosters, while Ethereum has missed the opportunity.

The most fatal flaw may be the design defect of the PoS mechanism. The merger in 2022 saw Ethereum abandon PoW and move to PoS, trying to balance supply and demand through staking rewards and gas burning. However, this mechanism has sown the seeds of inequality from the beginning. Stakers enjoy rewards, while transaction users burn gas, and the more active the on-chain activity, the higher the cost for the underlying users. In times of deflation, the "old money" benefits, while the retail users are squeezed out of the ecosystem by high fees. This structure not only fails to challenge the unfairness of the fiat system, but even exacerbates it. When new entrants join, they face a set of rules tilted in favor of existing beneficiaries, shaking the faith in ETH's value.

A Lost Direction: What is the Future of Ethereum?

Bitcoin has a clear positioning as "digital gold", Solana has proclaimed the ambitious slogan of "on-chain Nasdaq", but the goal of Ethereum is becoming increasingly blurred. DeFi was once its trump card, but now most activities have migrated to Layer 2, significantly reducing the fee capture on the mainnet. New narratives such as AI and RWA have not yet taken shape, and while the Pectra upgrade brings technical improvements, it has not been able to point the way forward for Ethereum. Vitalik's latest stance may provide a clue. His emphasis on Layer 2 interoperability suggests that Ethereum may no longer be satisfied with the current fragmented ecosystem, but rather hopes to drive collaboration between Layer 2s through higher fee pressure, and even reshape the relationship between the mainnet and Layer 2. Does this mean that Ethereum will return to the mainnet-first approach? Or is it just a warning to the Layer 2 ecosystem? The answer is not yet clear, but at least it shows his dissatisfaction with the current situation.

The repeated setbacks of Ethereum spot ETFs further expose the problems. Investors holding ETH through ETFs cannot participate in the 3.5% annualized staking rewards, and still have to pay management fees, greatly reducing the appeal. The deeper reason is that Ethereum's strong decentralization makes it difficult for any capital force to "control" it. The "fruits of victory" that Wall Street expects have not yet arrived, and the enthusiasm of institutional capital has naturally cooled. The Pectra's increase in the staking cap to 2048 ETH may be the first step in opening the door to institutions, but whether this is enough to drive up the ETH price remains to be seen.

Meanwhile, the rise of Solana provides another approach. Relying on high throughput, low cost, and the support of US capital, Solana's single-chain model maintains the integrity of liquidity, and the DeFi and AI narratives have quickly gained traction. In comparison, Ethereum's Layer 2 aggregation path appears fragmented, with innovation diluted by fragmentation, and even replicating others' success has become a challenge. Although Base has the backing of Coinbase, the silence of other Layer 2s has cast doubt on Ethereum's expansion strategy.

Conclusion: A Critical Moment of Choice

Ethereum's predicament is not a one-day cold, nor a mistake in a certain decision, but the inevitable result of the interweaving of positioning, mechanisms, and competition. It has not done anything wrong, it is just that the wheels of the times are rolling forward, and the time left for it to adjust is getting less and less. The Pectra upgrade may inject temporary vitality into the ecosystem, but if it cannot solve the fundamental problems of mainnet revenue shrinkage, Layer 2 parasitism, and narrative loss, Ethereum may find it difficult to regain its former glory.

How to go forward in the future? Continue to adhere to the belief in decentralization, even if it means being marginalized by the market? Or embrace institutional capital, reshape the price narrative through centralization? Or find a completely new breakthrough, rekindle the spark of innovation? This is not only a choice of Ethereum's technical route, but also a questioning of its soul. At this critical moment, Ethereum needs not just an upgrade, but a thorough self-renewal. Otherwise, the throne of the king of public chains may really have to be handed over to others.