The Tide Recedes, Recession Clouds Loom

In early 2025, the US financial market shifted from euphoria to unease. When Trump won the election in November last year, investors sparked a "Trump trade" frenzy, anticipating that his tax cuts and deregulation policies would sustain economic prosperity, causing the stock market to soar. However, this optimistic sentiment quickly dissipated, replaced by concerns about a "Trump recession".

The NASDAQ index suffered its biggest single-day drop since September 2022, with tech stocks and bank shares plummeting for days, and consumer spending intentions contracting at the fastest pace in four years. AFP bluntly stated that the "honeymoon period" between the financial market and Trump has ended. JPMorgan Chase has raised its recession probability for this year from 30% to 40%, Goldman Sachs from 15% to 20%, and the probability of a US recession in 2025 on Polymarket has also reached 40%.

The market is beginning to question: Are Trump's policies pushing the US economy into the abyss? In this turmoil, everyone is asking: When will the Federal Reserve cut interest rates to hit the pause button on this storm?

Tariffs and Layoffs: The Triggers of Recession?

Less than two months into his term, Trump's policies have already caused a stir. He has revived the tariff weapon, proposing 10% to 25% tax hikes on Canada, Mexico, the EU, and even China, in an attempt to redress trade imbalances and stimulate the return of manufacturing.

Meanwhile, Musk's "Government Efficiency Department" has cut federal employees, announcing 172,000 layoffs in February alone, the highest for the period since 2009, with a potential total exceeding 100,000. These measures have unsettled the market: rising corporate costs, emerging inflationary pressures, and shaky consumer confidence.

The Atlanta Fed forecasts that first-quarter GDP growth will slow, and historical patterns show that since 1980, whenever the Federal Reserve has raised rates above 5%, a crisis has occurred within 2 to 4 years, and the current risk window is post-2022 rate hikes.

On March 9th, Trump said: "This is a transformative period, we are doing big things." However, Nomura Securities strategists believe he may be intentionally engineering a recession to slow economic growth and drive deflation. Barclays' latest forecast also reflects this trend, predicting the Federal Reserve will cut rates by 25 basis points in June and September, a more dovish adjustment than the previous expectation of just one rate cut in June, possibly due to deeper concerns about inflation and economic slowdown.

Debt Burden and the Federal Reserve Showdown

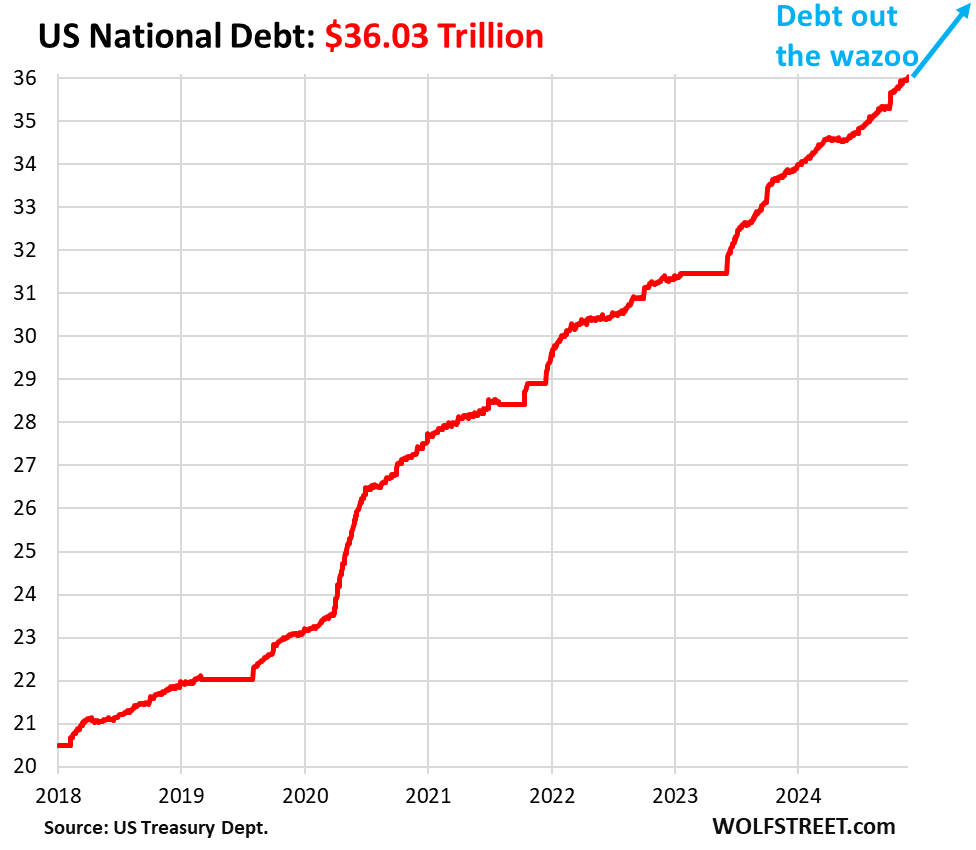

Trump's policies may be aimed at deeper targets. The US federal debt has reached $36 trillion, and interest payments have become a fiscal burden. According to the Congressional Budget Office, interest costs are estimated to reach $952 billion in fiscal year 2025 and could soar to $1.8 trillion in 10 years. If the Federal Reserve cuts rates by 100 basis points, the government could save $300 to $400 billion in annual interest, an irresistible temptation for Trump.

He has threatened to replace Federal Reserve Chair Powell, and Musk also appeared with him at the White House on March 11th, announcing layoff plans while frequently criticizing monetary policy. Treasury Secretary Besent said the economy needs "detoxification" and to break free from dependence on government spending, seemingly paving the way for short-term pain.

Currently, the federal funds rate is maintained at 4.25%-4.5%, and Powell stated earlier this month that inflation (CPI around 3%) has not yet fallen to 2%, and the economy still has resilience, so there is no need to rush to cut rates. But cracks have appeared in the labor market, with the total number of layoffs doubling in February, and if the unemployment rate rises from 4% to 5%, the Federal Reserve may be forced to act. The market speculates that June could be the starting point for rate cuts, and Barclays' forecast further reinforces this expectation, believing that a September rate cut is a response to the economic slowdown.

The Cost of Transformation and Unknown Risks

Trump's ambitions may go far beyond the present. His economic advisor Stephen Milani has proposed that the US needs to reshape the dollar system and break free from the deficit burden of the reserve currency. He envisions forcing China and the EU to sell their dollar assets and shift to long-term bonds through the "Mar-a-Lago Agreement", achieving a dollar devaluation and stimulating the return of manufacturing. If this plan succeeds, it will reshape the global trade landscape, but the prerequisite is for the economy to "detoxify" first - actively bursting the bubble and reducing leverage.

On March 11th, Trump told 100 corporate executives: "We must rebuild the nation." However, this transformation comes at a high cost: a stock market decline, a weakening dollar, and even a short-term recession may be an inevitable path.

Harvard economist Lawrence Summers warns that the recession probability is close to 50%, and inflation may return to 2021 highs; British analyst Dario Perkins points out that a true recession is not a "purifying agent" but may leave lasting scars. If it spirals out of control, the Republican prospects in the 2026 midterm elections will be clouded. From the "Trump trade" to the "Trump recession", the Federal Reserve's decision is crucial - whether Barclays' predicted rate cuts in June and September can materialize depends on the evolution of inflation and employment data, and the outcome of this high-stakes gamble remains uncertain.